If anyone had any residual doubts as to Ofgem’s performance in regulating the retail energy market, or whether BEIS was able to exert any sort of positive influence, they were dispelled this week when first former CEO Dermot Dolan and then his successor, Jonathan Brearley and a couple of his senior colleagues, and finally Business Secretary Kwasi Kwarteng were interrogated by the BEIS Parliamentary Select Committee. In this blog, I summarise the proceedings, alongside some of the conclusions of the report by consultancy firm Oxera which was commissioned by Ofgem in the wake of the many supplier failures last year.

Ofgem’s approach to regulation

Ofgem’s primary responsibilities are set out in the Gas Act 1986 and the Electricity Act 1989, as amended and are described as being shared between the Secretary of State and the Gas and Electricity Markets Authority. The principal objective is to protect the interests of existing and future consumers taken as a whole. However, the Oxera report found that Ofgem had no ex ante framework for defining and measuring consumer outcomes and saw no evidence that any quantitative impact analysis was undertaken to inform important policy decisions such as the 2018 Supplier Licensing Review, and there was no subsequent ongoing market monitoring of outcomes.

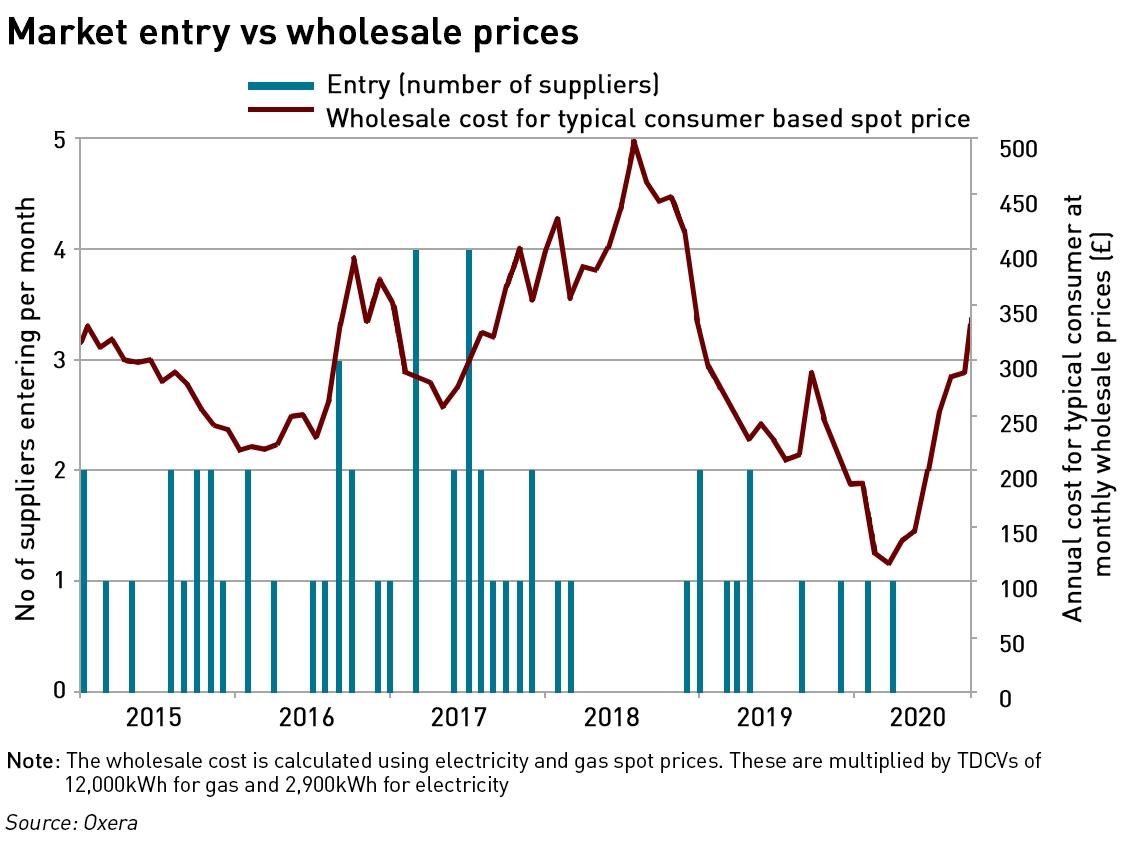

“…we find that Ofgem’s approach to regulating the market created the opportunity for suppliers to enter the market and grow to a considerable scale while committing minimal levels of their own equity capital. This was justified largely on the grounds of increasing the degree of competition in the market, and created the opportunity for prospective suppliers to enter the market on the basis of a ‘free bet’. By pursuing a high-risk/high-reward business model, such suppliers would benefit from any upside, while being able to exit at no or minimal cost if the downside materialised.

This regulatory approach does not seem to have been justified by an evidence-based assessment of trade-offs or a detailed understanding of the supplier business models and supplier incentives that arose as a consequence of Ofgem’s regulatory approach. In the pursuit of higher levels of competition, Ofgem did not seek evidence on trade-offs on an ongoing basis (e.g. between competition and financial resilience). Nor did Ofgem sufficiently test whether the economic incentives at the point of entry and exit were aligned with the protection of the consumer interest, through promoting effective competition. For example, Ofgem did not fully analyse systemic risks that might arise, and test how the probabilistic costs of failure would rise as new players with low levels of financial resilience acquired growing market shares, especially after 2015,”

– Oxera

Oxera notes that despite its aim to increase competition in the market, Ofgem had limited historical experience of regulating large numbers of non-legacy suppliers. Oxera does not say so, but implies that there is no evidence that Ofgem recognised its lack of experience or sought to remedy it. In fact, Oxera pointed out that Ofgem could have drawn on the practices of other regulators, including its own network regulation team, for insights into how some of these challenges could be met.

Oxera identified that the new entrants encouraged by Ofgem’s policies tended to adopt one of two business models:

- A growth model, where businesses relied on receiving customer balances prior to the provision of services to fund growth in the business, a strategy that was unlikely to be sustainable over the long term; or

- A timing model, where businesses undercut hedged rivals by entering the market at times when market prices were favourable, entering into long-term supply agreements with customers based on prevailing low spot rates, with limited hedging, a strategy that would be vulnerable if prices rose.

Ofgem was primarily concerned that restricting these models might limit competition in the market, and, as Nolan confirmed in his evidence, the regulator believed that some new entrants would fail and that the costs of failure were not a cause for concern.

Oxera determined that Ofgem’s approach to assessing the financial resilience of the retail sector was reactive rather than proactive, and while it did identify certain risks it was at times slow to design new policies to address them, for example the Supplier Licensing Review was delayed over 2016–17, and consultation began in late 2018, something Dermot Nolan attributed to resources being taken up with the price cap. When Ofgem did act to introduce stricter new entry controls in 2019, its assessment of the trade-offs was mostly qualitative in nature and Ofgem lacked a clear framework for comparing different options for intervention.

Ofgem didn’t routinely carry out inspections of suppliers’ governance or financial arrangements, and implicitly relied on external auditors to validate the suppliers’ financial statements and going concern status. But, given the retrospective nature of company accounts, this could not provide ongoing assurance that companies remained sound, and relied on assumptions that either material supply or demand side shocks would not occur, or that the companies would have sufficient financial resources to withstand them. The water regulator, Ofwat, takes a different approach, making provision for additional annual audit arrangements.

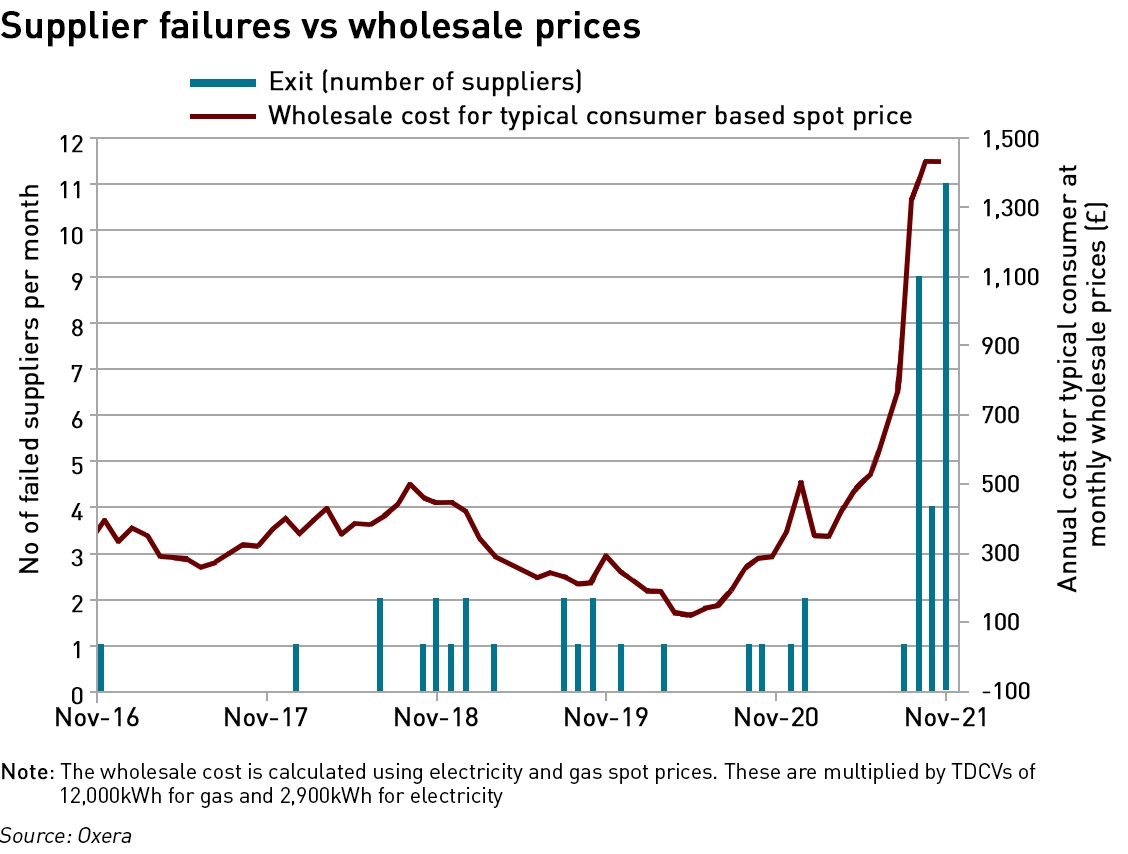

The first time that Ofgem collected industry-wide financial resilience data was in March 2020, although this was introduced to address concerns around bad debt levels during the pandemic, and not the ability of firms to withstand price shocks. It also turned out that the metrics available from this exercise did not necessarily enable Ofgem to anticipate the supplier failures that followed the increase in wholesale prices from September 2021.

When asked what he would have done differently, Nolan said that he regretted not moving faster in 2017-18, and in particular not introducing stricter controls over existing firms, and that Ofgem did not change the price cap to allow reviews “every two or one months” – the six-monthly reviews were implemented following the advice of the Competition & Market Authority. He went on to say that there had been a failure of imagination within Ofgem for not anticipating the possibility of price shocks and what their impact could be in the context of the price cap.

Ongoing failure to protect consumer credit balances (ie customer money)

The issue of suppliers using customer credit balances to fund their businesses was raised repeatedly by MPs during the session. The only firm that has committed to ring-fencing credit balances is Centrica, which by coincidence is also the only firm that is also regulated by the Financial Conduct Authority by virtue of its insurance business. Ofgem is now proposing to require all firms to ringfence customer money and prevent it being used for working capital.

Nolan was questioned extensively on this point, being asked why Ofgem had, during his tenure, allowed poorly capitalised suppliers to spend customer money on growing their business, and in some cases making loans to other companies controlled by the shareholders, which was then lost when these suppliers failed. In particular they highlighted the situation at Avro, where the shareholders had deployed no external capital in the business – indeed it had been set up by “a student in his bedroom”, and had subsequently paid out almost £1 million in loans to affiliated companies. Nolan claimed not to have been aware of this until he read Avro’s evidence to the Committee, which he described as “disturbing”. One Committee member asked the hapless Nolan that if Ofgem didn’t understand a business it regulated after it had been trading for six years, as was the case with Avro, then “what is the point of Ofgem?”

When asked whether Ofgem approved of suppliers using customer balances for business growth, Nolan said that he did not, and that Ofgem had established a principle, after concerns were raised by civil servants, that this should not be done. When asked what actions the regulator had taken in relation to this principle, he said that a call had been made to a supplier to ask them to stop doing it (this supplier was identified as Ovo). However, Nolan admitted when questioned that this was the only action taken, and that Ofgem had taken no steps to determine how widespread the practice was. As we now know (and knew at the time) this practice was and continues to be employed by all suppliers, with only Centrica (recently) committing to stop.

Nolan’s evidence on this point did not seem credible – if such a principle had been established by the Ofgem Board, it must have been done in a very casual way, with little serious consideration of how to ensure the practice stopped. By his own admission, Ofgem did next to nothing about it, so it is reasonable to question whether the description of this as a “principle” is accurate, or whether this is something that was simply raised in passing at some point but not followed up, or, worse, not even raised at all.

Nolan repeatedly said that the supplier failures during 2016-2019 had not cost any money, either to consumers to taxpayers. Of course this was not true, but he later elaborated that these failures had only added around 50 pence per year to the average bill and were therefore negligible. In his view, and apparently in the view of the Ofgem Board, these losses were acceptable, and as no-one was disconnected when their supplier failed, he felt the process worked well. This was despite some of these failures individually costing the market more than one hundred million pounds.

Ofgem – poor governance and lack of accountability

One thing that came through very clearly in both the evidence of Dermot Nolan and Kwasi Kwarteng is Ofgem’s lack of accountability. Nolan painted a picture of relaxed governance at the regulator, where important discussions were held informally, at dinners, and un-minuted. Kwarteng painted a picture of a lack of oversight where ministers can only “nudge” regulators since they are independent and “arm’s length”. It is reasonable to ask to whom Ofgem is accountable and who oversees its performance.

Nolan was challenged vigorously by Darren Jones MP, the Committee’s Chairman, who repeatedly drew attention to failings at Ofgem during Nolan’s tenure, while Nolan tried to deflect criticism away from himself to the Ofgem Board more broadly, and to ministers who set priorities and pressured the regulator to act in certain ways. For example, Nolan asserted that significant resources were diverted towards implementing the price cap, at the behest of ministers, and that left fewer resources for the supervision of suppliers. When challenged on this point by Jones, who not unreasonably asked why Nolan had not alerted ministers to the fact that Ofgem was unable to exert adequate supervision of suppliers during the implementation of the cap, Nolan replied that the regulator did supervise companies effectively, despite all evidence to the contrary. His evidence on this point was evasive and inconsistent.

The Oxera report also identified governance failures, with important decisions being taken by operational teams rather than the Board and in some cases, reversing decisions made by the Board. An analysis of Ofgem’s Board Effectiveness Review papers found that the Board has not consistently been able to dedicate sufficient time to critical issues; that the materials and board papers are not always of high quality; and that the Board does not always have full sight of the information required to make informed decisions and comment on the functioning of Ofgem.

Oxera’s report provides an example of poor controls and decision making by the Ofgem Board, where the Board took a decision that 50% of consumer credit balances should be protected. This decision was subsequently reversed by staff within the organisation, and a replacement policy was announced to the market before any further discussion at Board level. The decision was provided to the Board in the form of an Information Paper and the minutes state that this paper was “noted”. Interviews with stakeholders have highlighted among other things, a perception of infrequent challenge by the Board on the evidence base used, and the balance of risks and costs of different policy options advanced in decision-making. The report also found that operational silos within Ofgem restricted horizontal information flows and limited the regulator’s effectiveness.

These findings demonstrate a worrying lack of professionalism within the Ofgem Board, and a lack of understanding by Board members of their duties. While Oxera noted that Board discussions were consistent with the matters that were reserved to the Board rather than delegated, it is reasonable to question whether the Board exercised sufficient review the way in which it considered which matters should be determined directly by the Board, which decision-making powers should be delegated, and whether there was effective use of Board committees as a means of increasing oversight in respect of important decision-making. From both the Oxera report and Dermot Nolan’s evidence, it appears that the Ofgem Board was entirely too relaxed about its governance, and while it undertook effectiveness reviews, it does not appear to have acted on their conclusions in a timely manner.

Confirmation that Bulb’s gas and electricity exposures are not being hedged

Business Secretary, Kwasi Kwarteng was challenged on the costs of the Bulb Special Administration and in particular the rumours that Bulb’s gas and electricity exposures were not being hedged. While he made one point which was reasonable – Bulb is now on the Government’s balance sheet and the Treasury manages risks collectively and not incrementally across different units (ie there may be a natural hedge given the Treasury likely has a long exposure to gas as a result of taxes on UKCS production) – he made other remarks that were shocking in that they exposed how little he understands the concept of hedging:

“The thing with hedging is that it’s, you know, very risky because essentially, you’re taking a bet or you’re trying to insure yourself against price movements, and that insurance as Dan, Mr Osgood, said, costs money, um, and in terms of managing public money the Treasury rightly doesn’t think that that’s the business of what the taxpayer should be doing,”

– Kwasi Kwarteng, Secretary of State for Business, Energy & Industrial Strategy

Not hedging is taking a risky bet…when you set up a business that has an underlying exposure to a set of market prices, you are essentially taking a bet on those prices unless you are able to pass market price changes on to consumers. Since retail gas and electricity prices are subject to a statutory cap, failure to hedge input costs is extremely risky. We now have the bizarre situation where the regulator asserts that not hedging is risky and irresponsible while the Business Secretary says that hedging itself is “very risky”.

His suggestion that insurance is also risky because it has a cost is also bizarre – the Government requires every car owner to purchase car insurance and driving an uninsured vehicle is a criminal offence. If insurance is so inherently risky, why have governments taken this position for decades? The answer of course is that insurance is not risky – as with hedging – failing to buy appropriate insurance can lead to devastating losses. It is deeply worrying that the Business Secretary does not understand these basic concepts.

Perhaps Jonathan Brearley and Kwasi Kwarteng can get together, and decide between them on a unified position on the riskiness and therefore desirability of hedging, ideally after they have each found out what it actually is.

Energy is too important to allow such a lackadaisical approach

While it was at times entertaining to watch Nolan being skewered by the Committee, the session, along with the findings of the Oxera report are sobering. Millions more households are facing fuel poverty as the price cap is set to rise again by a significant amount in October – early indications are that it may rise by £830 (or 42%) to £2,800 on average. Although further support measures have subsequently been announced by the Chancellor, in most cases this will only cover half of the cost increase. Significant regulatory failures on the part of Ofgem have contributed to these costs, by allowing poorly capitalised suppliers with weak business models to fritter away their customers’ money.

Not only did BEIS lack any insight into the ongoing failures in the regulator, it is clear that it has limited powers to address them, although one power it does have is to replace the Ofgem Board, something that does not appear to have occurred to the Business Secretary. And although the BEIS Select Committee was at times forensic in its dissection of the problems at Ofgem during Nolan’s tenure, it would have been rather more helpful had these interventions occurred during the period in question rather than with the benefit of hindsight.

The energy sector is altogether too important to be left to such amateurs. I renew my calls for the Financial Conduct Authority to take over the regulation of the retail energy markets – at least it understands the difference between hedging and insurance, and the relative riskiness of each.

“The energy sector is altogether too important to be left to such amateurs. I renew my calls for the Financial Conduct Authority to take over the regulation of the retail energy markets – at least it understands the difference between hedging and insurance, and the relative riskiness of each.”

Unfortunately, we have a Government of amateurs, and an incompetent FCA. We have no one of any intelligence or ability or integrity in any responsible position. Is this the result of decades of dumbing down in the schools and universities? Of decades where dishonesty and incompetence has been increasingly rewarded rather than punished?

It’s a slow but sure slide to third world conditions and no one has the will to resist. The Parliamentary Select Committee may criticise but nothing will happen. The incompetent and crooks will continue to collect their salaries and bonuses.

I think it’s a combination of things. We have certainly as a society downgraded hard science in schools, and declining numbers of people have really strong analytical skills.

Savvy consumers had a gut feeling that the electricity market, and the way it was regulated, was not working. I noticed this first when they stopped publishing the tariff raw data for customers to interrogate because the data set was too big and customers would be confused. My guess is that this was a deal with the switching sites so customers could not easily go it alone.

One very important customer issue that OFGEM ignored completely was the parlous position that users of electricity for heating (off peak tariffs) were in. Almost all suppliers would attract customers with a low E7 tariff and then increase this disproportionately to overall energy costs, sometimes more than doubling. Many such customers were just unable to deal with the need to switch twice a year to minimise their overall energy costs. Responses to letters I sent on this subject merely stated that OFGEM could not get involved in pricing.

Use of electricity for heating is becoming fundamental to the UKs strategy for reducing carbon emissions and governments will have to work very hard to make this happen. Certain groups within the industry will try and argue that flexible time of use tariffs are the answer to this. They are not. Heating is fundamental to human needs and uncertainty about pricing for customers will just lead to anxiety for us and more confusion from supliers, not to mention less risk and bigger profits for them.

Ed H

Heating, or at least the basic human right not to be cold part, should perhaps be nationalised. There are many potential advantages in making the basic condition of UK homes a national concern in reaching net-zero.

https://www.linkedin.com/pulse/national-heat-health-service-steffan-cook-?trk=portfolio_article-card_title

So did at anytime anyone put a price on this regulatory failure. The last price cap rise included £68/customer as a down payment on the additional SOLR costs incurred by suppliers who took over other accounts. There will be another contribution in next price cap rise as well although maybe lower if Bulbs costs are going straight to govt borrowing. Also unseen is the 100’s millions of pounds worth a ROC costs that they didn’t pay along with millions owed to NG and the DNO for UoS charges. All this is being socialised onto bill payers ultimately.

I also delved into the administrators reports for the earlier failures and was staggered to find out how many customer bills were in arrears at each supplier and ones that had issued there six month updates on progress of teh administration were reporting that chasing down the debts wasn’t worthwhile and debts were being written off in accordance with OFGEM guidance not pursue debts >12mths. What this is doing is leaving unsecured creditors with nothing or at best very little recovery in that group is NG, DNO’s and gas carriers along with lots of smaller suppliers always caught out in administrations. The Insolvency practitioners stands to gain nearly £50m in fees plus whatever Bulb costs.

Pretty abject failure of regulation in my book but no one will be held to account and at best they will trot our there stuck record phrase “lessons will be learnt” which if they are they are never implemented anyhow.

Agreed – there is a total lack of accountability.

The issues with administrators was raised by the Committee because of previous evidence that the interests of creditors and those of consumers conflict in insolvency. Kwarteng (rightly) said that if the interests of creditors are not protected then no-one would invest in energy companies, but that does not mean that administrators could not be given additional obligations for energy suppliers where they are required to provide data to new suppliers in a timely fashion.

A big failure by OFGEM and it almost sounds like they knew it was happening.

But I also think the blame was with Government for not leaving OFGEM at arms length. I still think that even now Government is bankrolling ‘innovative’ energy suppliers in an attempt to get some net-zero stuff (like TOU) working. OFGEM would only have made life difficult for small and innovative suppliers so Gov’t kept OFGEM on a leash and the environment friendly. However, this preference for ‘innovation’ rather than competence is costing us money and will continue to cost us money.

I don’t think OFGEM will disappear or get better until Gov’t gets out of the energy supplier market. Sure, we should support technology innovation, but the energy market itself seems too big for the Gov’t to be able to interfere with directly with innovation cash.

Except there has been very little innovation. The same Committee asked the CEOs of the largest suppliers a few weeks ago why they were not innovating more – the unspoken answer was that there are no incentives to innovate in a structurally loss-making industry.

Nolan said that the price cap was designed to be tough and to reduce profitability in the industry because Ofgem thought legacy suppliers were inefficient. Either this analysis was wrong, or they went too far in reducing profitability.

The only thing I would like Brearley and Kwarteng to agree is announcing their resignations pronto. We should remember that the “as amended” feature of the Gas and Electricity Acts is to give primacy to green interests over consumers, and the current move is to give net zero policy the overarching role. Therein lies disaster. It has already led to complete disregard for consumer interest at BEIS and OFGEM, neither of whom have made any move towards creating a lower cost, competitive energy supply system. That Hinkley B has now said it is too late to consider refurbishment to provide capacity over next winter is down to continued dithering by Kwarteng and Brearley and Slye (who should also be in the dock for feathering the interests of National Grid at consumer expense). How long ago is it that we started getting NISMs?

Trouble is even if they resign, who replaces them? Whatever obligations Ofgem has, it’s clear it hasn’t developed any way of quantifying and measuring its performance against those objectives, which is extraordinary. When I took up my first NED role (for a small charity) I signed up for various training courses and read Charity Committion guidance so I understood my duties as a director and trustee. While I knew there was a lack of operational competence in Ofgem I was genuinely shocked at the poor Board-level governance…where did they find these people, were they very inexperienced, or did they just not care about their duties (or both)?

I’m not even a little bit surprised that HPB won’t stay open – it was closing for safety reasons and the year before the closure was announced it had had quite a bit of downtime while the issues were investigated. It seemed pretty unlikely to me that extending the life into this winter would be viable, or that EDF, given the more pressing issues in its home market, would be inclined to bother.

This winter’s capacity margin is likely to be a very round number…NISMs (or EMNs as I think they are now) will be the least of it. I think there will be mandatory curtailment of industrial demand, and if the weather doesn’t play ball, we’ll have a genuine risk of rolling blackouts or even unplanned blackouts due to reduced system resillience.

Do you fancy running OFGEM or BEIS? Between us we would make a much better job of it!

I’m sure we could, but unless we could replace most of the people and processes, it would be a struggle…

Just spotted this example of government arithmetic:

Schemes such as the Green Homes Grant have previously been introduced to help make energy efficiency more affordable, however the Green Homes Grant closed early after a number of administrative problems, with just 20% of the £1.5 billion initially allocated to the scheme having been spent.

Recent figures did show that installations under the scheme are resulting in an annual bill saving of £641,000, however.

So that’s £300m spent to save £0.641m per year. A 468 year payback, before financing costs.

It’s so depressing because reducing heat losses is important and needs to be done. But the schemes need to be done properly and deliver value – which so far they have failed to do due to poor, rushed design…