Since the appalling attack on Israel by Hamas terrorists on 7 October, oil prices have been volatile. Historically, conflicts in the Middle East have had a major impact on oil prices, from the price shocks of the 1970s to the Iraqi invasion of Kuwait in 1990 to the Libyan civil war in 2011, and this is prompting fears of a repeat, given the risks of the current conflict spreading.

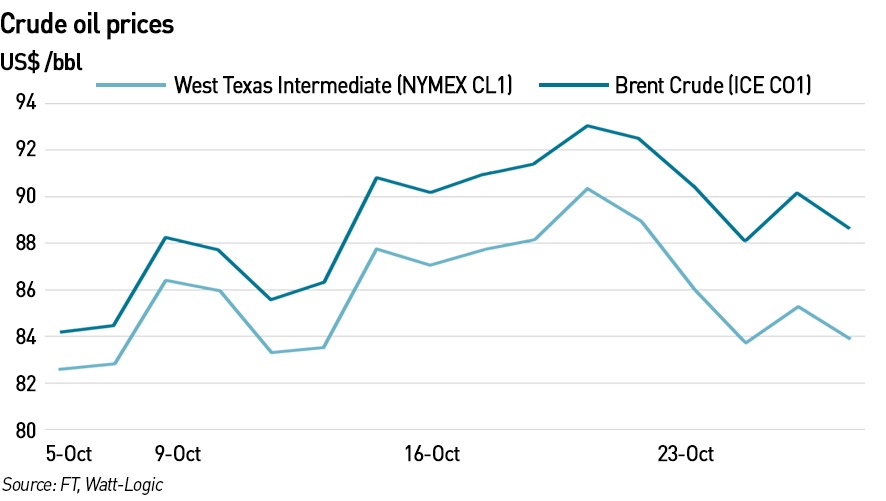

Global oil market prices have climbed in the two weeks since Hamas launched its shock attack on Israeli civilians. Front month brent futures prices jumped from US$ 84 /bbl just before the atrocity to over US$ 90 /bbl at yesterday’s close. This has reignited fears among oil traders and economists that markets could breach the US$ 100 /bbl mark again for the first time since briefly hitting that level in summer 2022.

There are concerns that an escalation of tensions in the region could drive oil prices much higher by disrupting a key transit route for seaborne oil and gas cargoes from the Middle East to the global market – threatening efforts by central bankers to address high inflation.

“Escalating wrath in the region will strengthen economic headwinds, potentially rising oil prices will push global inflation higher, monetary tightening could resume, and global oil demand growth will be dented,”

– Tamas Varga, analyst at PVM

There are also fears that the US may impose additional sanctions on Iran, further restricting oil exports from the country. Iran is a long-standing supporter of Hamas, and Lebanese terrorist group Hezbollah, which has also historically engaged in attacks on Israel. Over the past year, the US has turned a blind eye to some exports of Iranian oil to countries such as China, despite existing sanctions in relations to Iran’s nuclear programme. The reason for this relative flexibility has been a desire to reduce upward pressure on gasoline prices, a politically sensitive topic in the US.

Were the US to enforce existing sanctions more strictly, the oil market would tighten again. Politicians from both sides of US politics have been urging President Biden to cut the flow of oil revenues to the Iranian regime. Robert Ryan, the chief strategist at BCA Research, believes there is a one in four chance that Iranian oil output could fall by a 1 million bbl/d as a result of stronger US sanctions. Which could send oil prices over US$ 140 /bbl next year.

I also covered this topic in a recent article for The Telegraph

The impact could be mitigated if Saudi Arabia – which is currently restricting its output – were to increase production to help steady the market, however, there is significant uncertainty around the potential reaction of Saudi Arabia any tightening of US sanctions. Oil analysts suggest that while the Saudis may welcome recent oil price increases, they would not want a large spike which would fuel inflation, leading to higher central bank interest rates and a possible recession in oil-consuming countries that would ultimately harm global demand for oil.

There is further uncertainty around supplies from Venezuela. Oil markets were somewhat calmed last week by US moves to suspend sanctions on the country, after a Venezuelan government deal with opposition parties to work together on election reforms. Some sanctions on oil gas and gold have been temporarily suspended. This could see Venezuelan production increase in 2024, possibly ramping by 200,000 bbl/day, taking it close to 1 million bbl/day which is still far below the more than 3 million barrels produced each day by Iran. In any case it is unclear whether this softening by the US will last in the face of some strong political opposition.

There are also serious concerns over the security of physical transit routes for oil routes to market for oil through the Strait of Hormuz. More than 20% of the oil consumed globally together with a third of the world’s seaborne gas shipments travel through the Strait of Hormuz between the Persian Gulf and the Gulf of Oman. If Iran attempted to block this route it would have major implications for Europe’s supplies of gas from Qatar, which are crucial following the decline in pipeline gas imports from Russia since its invasion of Ukraine last year. These concerns explain recent moves by the US to position two aircraft carriers in the eastern Mediterranean, to deter Iran or Hezbollah from joining in the Hamas war against Israel.

Russia, meanwhile, is able to benefit from higher prices, since its sales of oil and gas are major contributors to its economy and funding of the war in Ukraine.

Some comfort might be taken from the fact that the world is less dependent on oil than it was in the 1970s, when oil accounted for over 40% of global energy consumption. Now it is just a third, but this is still a lot, and large enough that oil prices have a significant economic effect. It is also the case that any wider conflict in the Middle East would also affect gas supplies – indeed, Israel itself has cut gas production from its Tamar field in the Mediterranean over fears that its infrastructure is too close to Gaza, and could be vulnerable to attack from the shore. This has cut exports to the EU via Egypt – last week a liquified natural gas tanker was turned away empty from an Egyptian port.

The European gas market is currently well supplied after a warm winter last year helped maintain gas stocks ahead of this coming winter. The picture could change quickly when the weather turns cold as heating demand sees gas use ramp up and inventories decline, and prices are already rising over these concerns.

Another major difference between now and the 1970s is that the US is no longer reliant on oil imports – since the shale revolution it is a major oil and gas exporter in its own right. But its position is threatened by net zero policies which would reduce its energy independence and ability to supply Europe. President Biden has committed to “ending” fossil fuels, while Britain’s Labour Party is determined not to allow new oil and gas drilling in the UK North Sea.

Key minerals which are necessary for the energy transition are also largely under the control of not entirely friendly, or even outright hostile nations, in particular China for metals and Russia for uranium. Much of the world’s supplies of copper, lithium and graphite are under Chinese control, and its near-monopoly on the rare earth minerals used in wind turbines and electric cars leave America and Europe vulnerable to a country which is at best a major competitor, and at worst, an ally of nations such as Russia and Iran, whose oil it remains happy to buy.

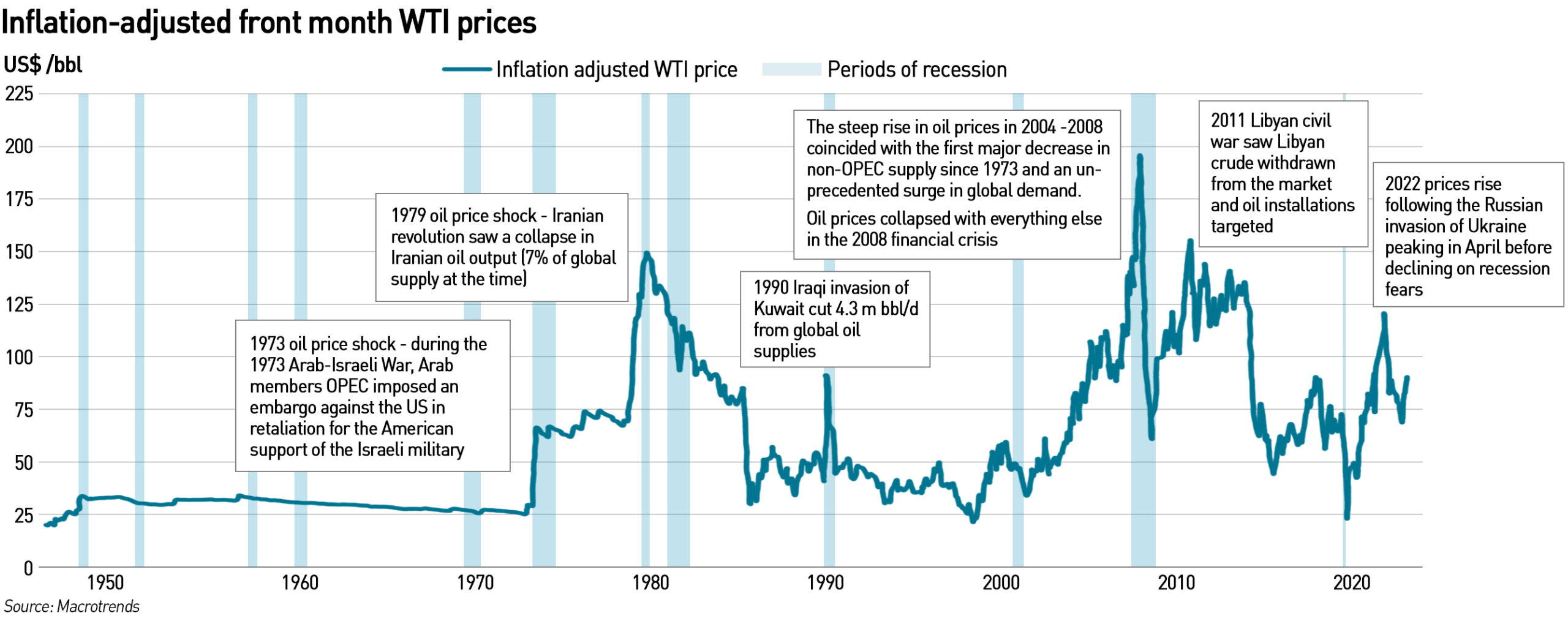

Oil price shocks of the 1970s followed conflicts in the Middle East

Two major oil price shocks in the 1970s, both linked to conflicts in the Middle East, had a significant impact on western attitudes to energy security, connected to the risk of further upheaval in the area, which remains the world’s biggest oil-supplying region.

In 1973, the Middle East supplied over a third of the world’s oil, so when Arab members of the Organisation of Petroleum Exporting Countries (“OPEC”) imposed an embargo against the United States in retaliation for US support for Israel during the 1973 Arab-Israeli War (also known as the Yon Kippur War), it had a major impact. The embargo was extended to include the Netherlands, Portugal, and South Africa, banning petroleum exports to the targeted nations as well as introducing cuts in production – between the imposition of the embargo in October 1973 to December that year, production was cut to just 25% of their September 1973 levels. These cuts nearly quadrupled the price of oil from US$ 2.90 /bbl to US$ 11.65 /bbl in January 1974. The embargo lasted until March 1974, however higher prices persisted.

The embargo strained a US economy that had become increasingly dependent on imported oil. It also coincided with a devaluation of the US dollar and other economics factors, leading to a global recession. As a result of the embargo, countries such as the US and the UK developed strategic petroleum reserves – stockpiles which would provide a cushion against any future restrictions in global oil supplies.

The oil price shock of 1979 also had its origins in the Middle East, this time with the Iranian Revolution which saw the creation of the current theocracy. During the revolution, Iranian oil output declined by 4.8 million bbl/d (7% of world production at the time), with fears over further disruptions and suggestions of hoarding causing oil prices to surge, more than doubling between April 1979 and April 1980. These events coincided with a period of high global oil demand, putting further strain on prices. The situation was further exacerbated when Iraq invaded Iran in 1980, leading to a further loss of output of 2.7 million bbl/d.

High oil prices exacerbated already high inflation, triggering another recession in the early 1980s. In response, central banks increased interest rates, with US rates spiking at 19% in July 1981 while UK rates peaked at 17% in November 1979. Eventually, a combination of slowing economic activity in industrial countries, investment in additional production capacity, and the implementation of conservation measures helped restore the supply and demand balance, ending the oil crisis. From mid-1980, real oil prices began to subside, igniting a decline that would last for much of the next twenty years.

A brief price spike in 1990 coincided with the Iraqi invasion of Kuwait, and the Libyan civil war of 2011 also caused prices to surge.

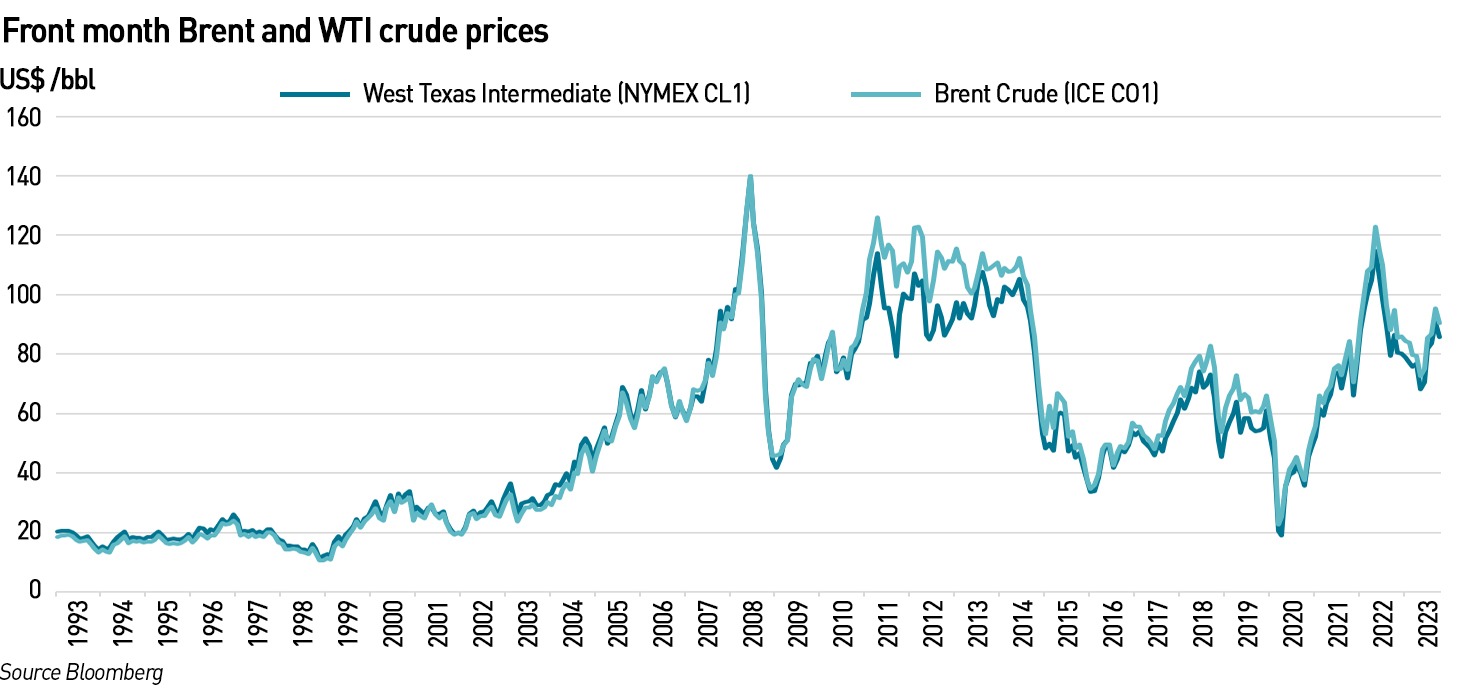

From the beginning of 2000, oil prices began an 8-year bull run which only ended with the financial crisis of 2008. The main driver of oil prices during this period was the demand growth in China, including a significant increase in car ownership as personal prosperity also increased. There were similar developments in India, albeit on a smaller scale. Economic performance elsewhere as also strong in the early 2000s, causing oil consumption to rise in the rest of the world as well.

Conflicting views of the oil price cycle

It’s been two and a half years since WTI prices turned negative for the first time in history. Just before the front month futures contract expired, with the market well supplied and storage facilities full, traders were desperate to offload contracts to avoid holding them to delivery, knowing the oil would be difficult to sell and expensive to store. This briefly pushed prices of the expiring May 2020 contract into negative territory. As a seaborne market, brent crude is not affected by storage availability to the same extent, and did not see similar pricing behaviour.

During the summer of 2020, the covid pandemic was in full swing. Global demand for oil had slumped, and producers began to cut output in response. Prices rose from this point, as these production cuts, and later demand recovery sent prices higher, boosted further by the Russian invasion of Ukraine in February 2022, only declining from June 2022 onwards on the back of growing concerns over a possible recession and increased output from Saudi Arabia.

According to research group Rethink Energy the covid pandemic was always likely to prompt a new supercycle for oil as pent up demand in key areas of the economy was unmet due to reduced production capacity, saying back in 2022 that unlike previous super-cycles, the “fundamentals behind this one were set to make it more dramatic”. It said that the oil price boom between 2008 and 2014 was predicated on a low investment period of 20-plus years, and demand growth over a six-year period. This was followed by a six-year decline in prices.

Indeed, prices rose steeply from the covid lows of mid-2020 to July 2022, and the company predicted that prices would subsequently plummet, continuing to fall through 2024 on onwards on the back of electric cars displacing conventional alternatives in response to higher fuel prices. In fact, this logic is not holding since electricity prices are also high and a lack of charging infrastructure deters some consumers. Countries across Europe have recently delayed or watered down electric car mandates over cost of living concerns.

Looking at inflation-adjusted oil prices since the 1940s, it’s tempting to conclude that super-cycles are becoming shorter – prices rise dramatically, only to collapse over similar timeframes, before repeating the cycle over ever shorter periods. Earlier this year, Reuters analyst John Kemp has argued that the ongoing sell-off is part of a Kitchin cycle that lasts for 3 to 4 four years. Kitchin cycles are attributed to the accumulation and liquidation of excess inventories. As economic growth increases, supply responds and the market becomes “flooded” with commodities. Conversely, as growth declines, falling demand leads to falling prices and inventories of produced goods accumulating.

There are other business cycles that can be used to understand and even predict the behaviour of commodities markets, including the Juglar and Kondratiff cycles. Juglar cycles last 7 to 11 years, and are attributed to investment in fixed assets such as machinery. The investment delay in the Juglar cycle is usually 1-2 years, while the investment delay in the Kitchin cycle – which applies to short-term investments – is only 4-7 months. Juglar cycles can be used to predict capital investment levels.

Kondratieff waves are long-duration cycles lasting 45-60 years attributed to the diffusion of major new technologies, and theorise that economic growth in capitalist countries comes in long waves driven by technological innovations.

At the beginning of the year, Kemp suggested that the Kitchin cycle implied that the slowdown in energy prices was likely to be a mid-cycle soft patch, and oil prices could strengthen in the latter half of 2023. Prices continued to fall until May, and since then have followed a broadly upward trajectory.

Kemp noted that global inventories of oil and more cyclically sensitive components such as distillates were below the long-term averages, meaning that inventories were likely to deplete quickly in the event of an economic recovery leaving little spare capacity to rebuild them in the short-term. This would lead to a supply squeeze. On the other hand, were the economic slowdown to descend into a recession, both oil and gas prices would come under downward pressure where an accumulation of inventories and increase in spare production capacity would create some degree of cyclical slack which could delay the next upswing in prices until 2024.

A technicals-based analysis also suggests prices will rise. I’m not a huge fan of technical analysis on asset pricing – I favour a fundamentals approach. But the more liquid an asset is, the more people trade it, the more behavioural dynamics will affect pricing, and this, together with the fact that some people do trade on technicals, means they cannot be ignored.

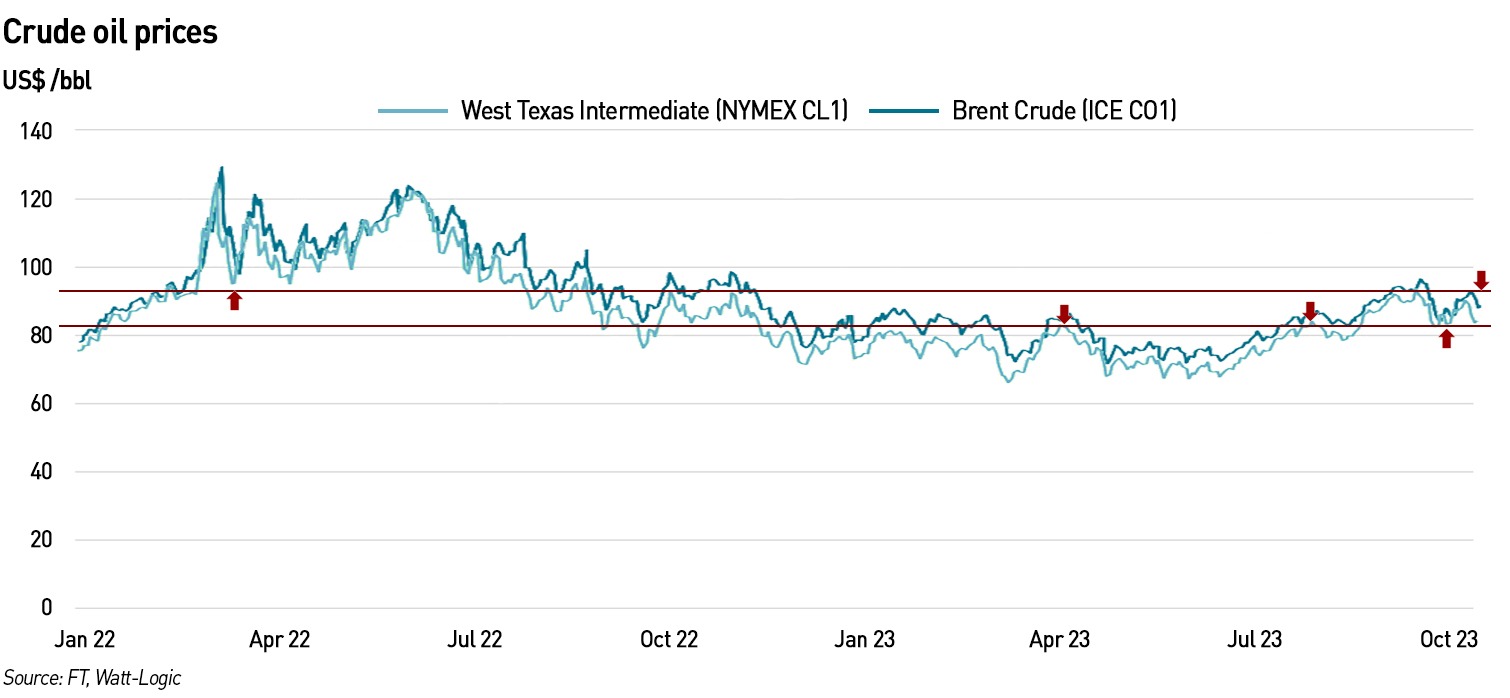

A technical analysis of WTI prices indicates that until recently it was range trading between about US$ 63 – US$ 83 /bbl, but has broken out of this range and is now trading between US$ 83 and US$ 93 /bbl. If it breaks above this new support level, some analysis suggest it could head up towards US$ 115 /bbl, and if former levels are re-tested, it could go to US$ 130 /bbl. Technical analysts point out that historical commodity cycles were longer and would not bet against this one being similar, and on that basis oil prices could approach US$200 /bbl again over the next 2-3 years .

.

Of course, all bets are off in the event of geo-political upheavals such as wars. Markets will continue in a wait-and-see pattern with short-term prices likely to react strongly to developments in the Israel-Hamas conflict. But even if the situation is contained, it is unclear whether prices will resume their previous downward trajectory, or whether that was temporary softness which would have quickly reversed. Much depends on whether recessions can be avoided, in which case, oil prices will likely rise.

Certainly, on an inflation-adjusted basis it appears that oil price cycles have accelerated, and that since the beginning of this century there has been little price stability, a far cry from the largely range-bound trading of the preceding fifteen years. My view is that any new period of price stability is unlikely, reflecting the wider lack of economic and political stability around the world. Should energy transition policies succeed in reducing oil demand, that may change, but we are decades away from such an outcome. In the meantime, oil prices are likely to continue to swing between highs and lows, with volatility peaking in times of higher political conflict.

Leave A Comment