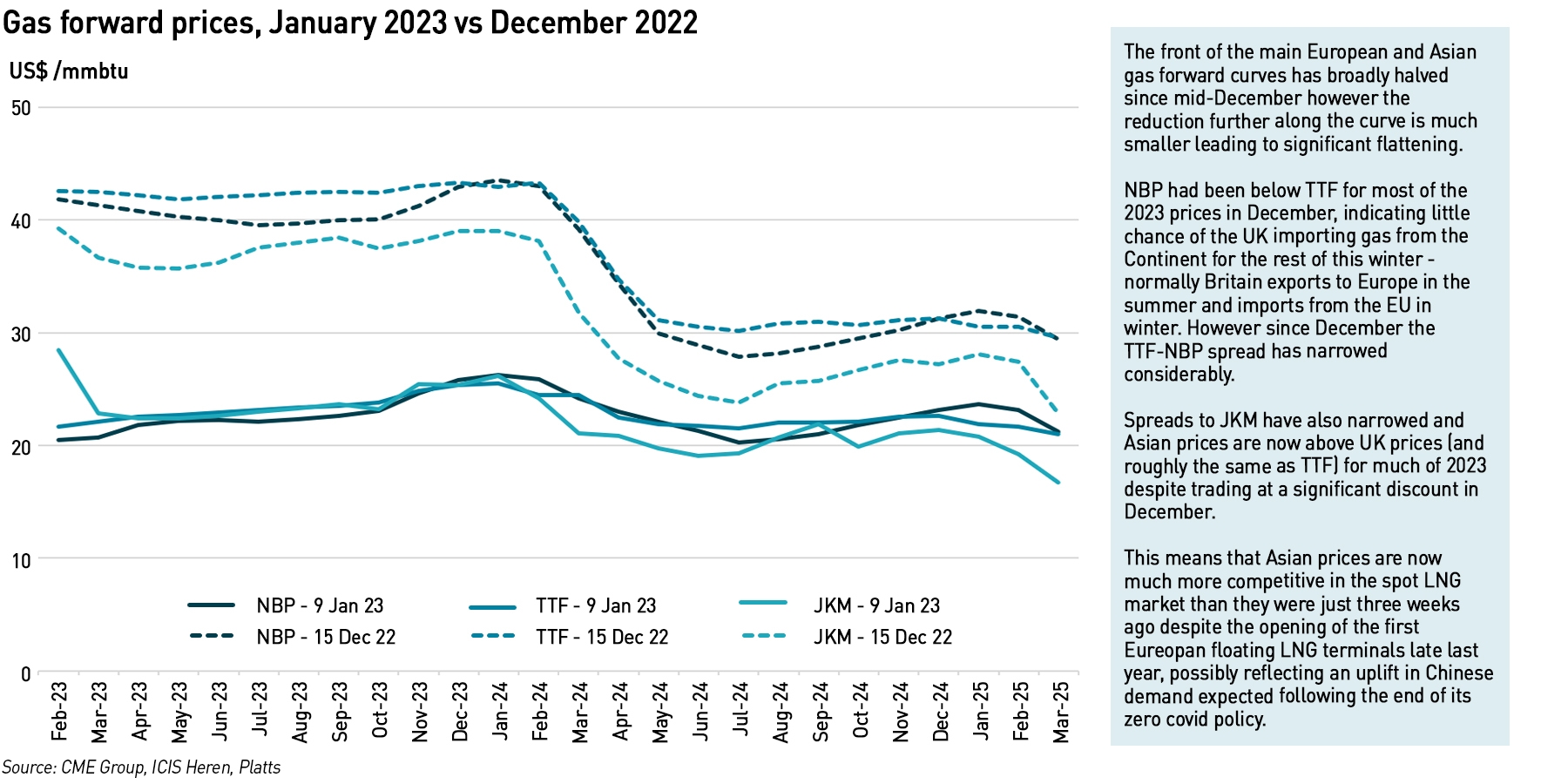

Gas prices have fallen across the curve in recent weeks, returning to levels last seen before the war in Ukraine (but still higher than they were before the covid recovery began in September 2021). The reasons for these reductions appears to be the fact that mild weather has seen much lower levels of gas demand so far this winter than usual, and comments by the Russian Deputy Prime Minister suggesting that the Russia may re-open the Yamal pipeline through Poland. The opening of new LNG import terminals has also reduced Europe’s reliance on Russian gas.

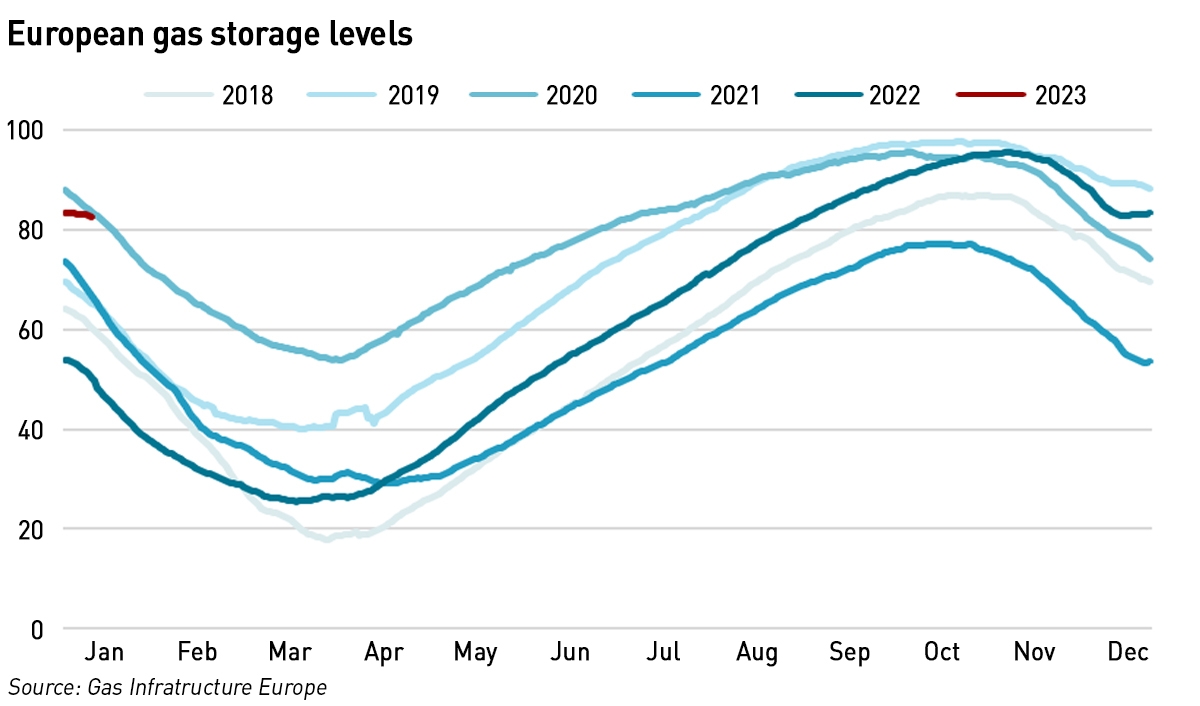

The reduced demand for gas across Europe this winter means that storage levels are much higher then seasonal norms, and the bloc is on track to end the winter need to buy less over the summer than would normally be the case. Based on average Q1 consumption over the past five years, EU gas storage facilities could be almost half full (c 47%) at the beginning if April – higher than the 5-year average of 35% and possibly the highest seen in five years. This assumes the rest of the winter is not colder than normal, or that other factors do not increase demand – as gas prices fall they will pass the coal-to-gas switching level for electricity generation, increasing gas consumption.

At these prices the EU cap is unlikely to have an impact, and while some colleagues have speculated that the cap is leading traders to migrate their activities OTC, similar price reductions can be observed in the OTC indces. The prospect of increased use of gas in electricity generation is causing concern:

“Market participants believe that the European gas balance is not comfortable enough to afford a significant boost in gas demand for power generation, particularly as the price decline could also trigger a restart of some industrial demand,”

– EnergyScan, Engie

There are further worries that since the price differential to JKM has disappeared, LNG cargoes are heading to Asia instead of Europe, just at a time when Chinese demand is expected to recover following the end of its zero covid policy, which has reversed faster than expected. This is exacerbated by the slow return of the Freeport LNG terminal in the US whose re-start has been further delayed to the second half of January.

“In case cargoes are diverted, substantial amount of baseload volumes are missing, setting a natural floor to price levels…Eventually Europe has to attract LNG cargoes during the year to replace Russian supply,”

– Simone Turri, head of western European structured trading at MET International

The question in everyone’s minds is whether these price reductions will be sustained. Colder weather, increased consumption through coal-to-gas switching, and LNG diversions to Asia can all threaten European gas balances, and we have seen dramatic price reversals in the past for example the dramatic increase in prices at the end of August due to Nord Stream concerns was quickly reversed. Attention is turning to next winter which has seen prices reduce by much less than this winter. Lower prices make it harder for Europe to secure LNG, and optimism around Yamal might be mis-placed…there has been no further indication the pipeline might re-open since the comments in mid-December from the Russian Deputy Prime Minister. My feeling is that it is too early for optimism…

I have to agree, especially given the threat of colder weather moving in and more nuclear turnarounds in France in Feb. I have seen little sign of LNG at the new FSRU terminals. Eemshaven has seen about three cargoes since opening, while no ship has docked at the Wilhelmshaven FSRU yet. Yamal LNG flows now include an occasional reload at Montoir for FEAST in addition to the Chinese ships plying via Suez and a couple of Arc-7s braving the Northern Arctic route. As I commented recently Yamal flows otherwise continue into Belgium, Spain and France apace, with sporadic cargoes for the Netherlands.

A second lng ship, the Melanje is expected at Willhelmshaven on 31 January from Angola.

Maran Gas Ithaca is there today.

There seems to be a present difficulty in unloading lng at the British terminals. Over the holiday season ships were not arriving and departing as quickly as they do normally to the extent that 5 ships are waiting to enter Milford Haven right now. At the same time there are 4 or more tankers waiting at anchor off Freeport.

Last year the question was whether there was enough shipping to supply the lng available, the present indications are yes. Over 50 new ships were launched last year and the same or more will be launched this year. (Over 150 are on the order books many more than in the past in part in readiness for Qatar’s new terminal.) There should be no delay in loading for next winter and some 100 extra ships hold significant stocks of gas to ensure that offloading could be continuous at every port. Europe has done very well to restrain demand and whilst price has been a persuader to many people European governments will want and need to keep demand lower for next winter too.

The wind generation of electricity in the UK has been fantastic this winter so far. And with French nuclear coming back on line and with the new wind farms coming on stream over this summer in both UK and European waters we should see 15 to 20 GW of potential supply next winter over and above last autumn. That alone could offer some 350 GW of gas saving a day. I am not overly confident in converting units of gas but is that not the equivalent of the UK’s gas consumption? The markets need to take that into consideration, I have a hunch that they haven’t yet and see gas is overpriced for the rest of the year.

Brian interesting stats on number of new LNG tankers quite extraordinary and surprised that there has been that amount of extra liquefaction capacity added to make that sort of investment. Mind you just as well as voyages are longer into Europe and holding time off terminals been increasing in some areas. As to the UK we have plenty of LNG storage capacity in hand currently according to the prevailing gas view ( https://mip-prd-web.azurewebsites.net/ ) and that also records inflows on 6 of the 13 days so far this year although which terminal isn’t clear so could have been Grain although not sure how many berths they have.

Ive also noticed with good wind in NW Europe the system price drops away on the mainland and the interconnectors are back in full import mode again as our system price still being kept too high even with reduced gas generation.

Gas production in the US has been ramped up to meet European demand. So whilst we lost Freeport, Australian lng came back on line mainly to serve the Far East. We have been receiving cargoes from Peru, Angola, Nigeria, Qatar mainly early in the winter as well as numerous ports in the States. And I guess the reduction in consumption both in Europe and locked down China and some poorer countries priced out, consumption has been satisfied.

@Brian Griffiths “The wind generation of electricity in the UK has been fantastic this winter so far.”

Do you have data to support that? Wind output in early December was dismal (all over Europe).

Tim you can download data from here https://bmrs.elexon.co.uk/generation-by-fuel-type but its only NG metered wind not embedded. Over last month lowest half hour has been 1.8GW highest 17.4GW. During the last 28 days wind has been above 10GW for 71% of the time and above 15GW for 24% of the time. This is substantially better utilisation than 12mths ago although need factor in additional generation added to draw a fair comparison but from watching this for several years we have certainly experienced good long run wind generation, rather than swinging between peaks, but there will always low wind days and there’s no getting away from the fact gas is here to stay for decades.

You can access capacity utilisation at http://www.ref.org.uk but data has some lag unless you pay by the looks of it.

There has been one cargo into Willhelmshaven, it arrived on the 6 January iirc.

Wind generation in the UK can be downloaded from http://www.Gridwatch Templar.co.uk but the better signal is the use of CCGT. Which is mostly below about 3GW, even during the day time and except during early December hasn’t been anywhere near peak output. That has allowed gas stocks to be replenished in the UK whilst at the same time gas has been pumped to Europe via one of the interconnectors since the cold weather in December.

The more you dig around the more interesting things are. Germany has received 2 cargoes via Willhelmshaven, the floating terminal brought a full load with it. Lubmin has a terminal ready to go but despite having state permissions to start operations the local administration hasn’t given permission despite the state override. It is waiting to start unloading. And that connection goes into what was Nordsee pipeline straight into the main grid. Meanwhile Brunesbuttel is almost ready to start operations, they were predicted to start by January so there is time yet. These 3 terminals can replace about half the gas that Russia supplied. With gas flowing from West to East Europe’s gas needs for next winter are almost assured. Storage is unlikely to be anywhere near depleted by the end of winter and with fresh arrivals via the new terminals likely assured by the growing tanker fleet it looks as though the markets have it wrong.

This morning there are 4 lng tankers unloading in the UK. Even more are offshore some ‘Awaiting Orders’ though likely to go to Milford Haven. It is hard to understand why National Grid are showing LNG stocks as half full, at the rate of tanker unloading they should be full?

Meanwhile we continue to send small but significant amounts of gas to Europe.

Sorry to hog this…. But I have done some more trawling around and found 6 LNG tankers moored off Cadiz environs. And more are arriving off Milford Haven. Isle of Grain has just about finished unloading the Sonangol Benguela and the Gaslog Windsor is taking on the pilot heading into the port. There hasn’t been this much activity all winter with 4 ships unloading in the UK simultaneously but also rapid turnaround at the terminals. The Grid’s prevailing view is showing LNG stock at about half full. And for a week or two output has been below capacity. With some cold weather ahead that might change but the ships queuing can replace the stocks quickly.