It’s always interesting at the start of the year to look back at what I was thinking this time last year. In my opening remarks I said: “I suspect that by the end of 2022 we will have finally moved on and by the end of the following year things will be more or less back to normal in a social sense (sadly I think we will be paying the price of dealing with the pandemic for many years to come).” I think I can safely say that this prediction was correct! But how about the rest?

My other predictions for 2022 were:

- More supplier failures

- More regulation of the supply segment

- More focus on security of supply; and

- International interconnector tensions

I was “more confident” in my predictions for 2022 than I had been in the past saying “certainly I think there is little doubt about the first three on my list. The last one may not really emerge this year, but I definitely see this as a growing risk, so if not in 2022 then at some point soon”.

Perhaps my predictions were reasonably safe bets. We did see a small number of additional supplier failures, and we have certainly seen both more regulation, particularly proposals for prudential regulation, and a renewed focus on security of supply. We also saw signs of discontent from Norway about its interconnectors with GB and Germany in particular with two reports commissioned by the Norwegian Government stating that these had both inflated costs and undermined energy security in the country. The Government has outlined plans to link electricity exports with reservoir levels.

However, I completely failed to anticipate the biggest energy story of 2022 which was the invasion of Ukraine. In my defence, I don’t recall any other energy commentator predicting this either, but it had a seismic effect on the market which will take some years to unwind. Also, I don’t think even the Russians expected the impact it would have…when Putin’s tanks crossed the border on 24 February the Russian aggressors believed they would quickly seize Kyiv and that the Ukrainian Government would crumble and its officials flee. President Volodymyr Zelenskyy, a former comedian who became famous pretending to be the Ukrainian president, has turned out to be anything but a joke, and has emerged as a bona fide war hero inspiring his people in a spirited and surprisingly successful defence. There is now talk not only of Ukrainian victory but of Russia even being expelled from Crimea which was illegally annexed in 2014.

In any case, this was no Crimean campaign – Ukraine failed to collapse and rather than turning a blind eye as it did in 2014, the international community piled economic sanctions on Russia, triggering an energy war in which Russian supplies to the EU collapsed, with the most serious impact being in the gas market. As a result, global gas prices soared, and with them electricity prices across Europe. In turn these high prices have triggered various policy interventions – most European countries are subsidising their citizens as energy costs became increasingly unaffordable, in part funded with windfall taxes on those benefitting from high gas prices. Other interventions such as market price caps have also been introduced.

In the closing moments of 2022, China was forced into a sudden reversal of its zero covid policy which may see its demand for gas grow in 2023 as its economic activity recovers.

Energy market outlook for 2023

In some ways the resolution of the conflict in Ukraine will have much less impact that its inception: the world is unlikely to quickly forgive and forget and Russia will probably never recover its energy relationships with the West. However, there are still ways in which the conflict will influence energy prices.

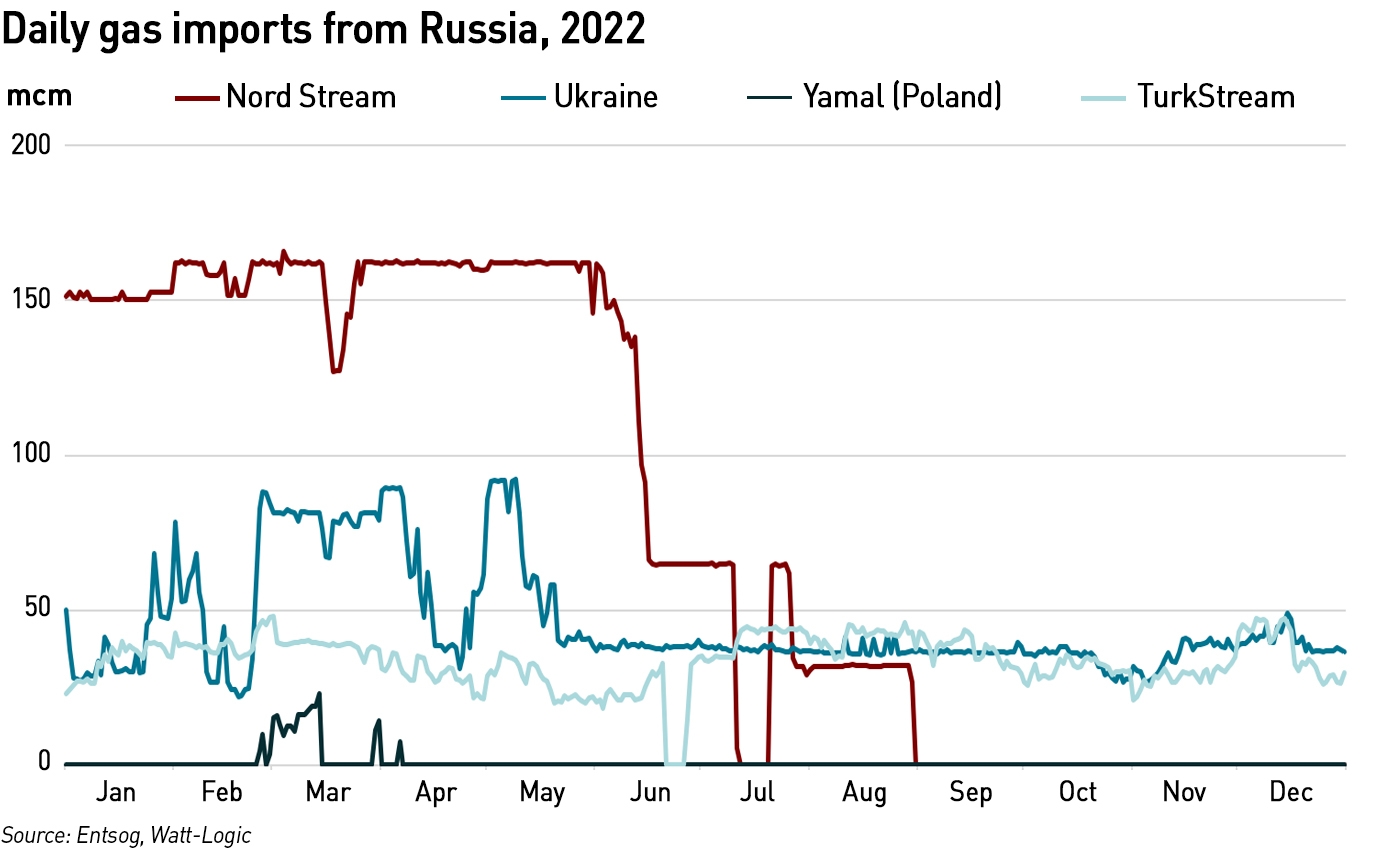

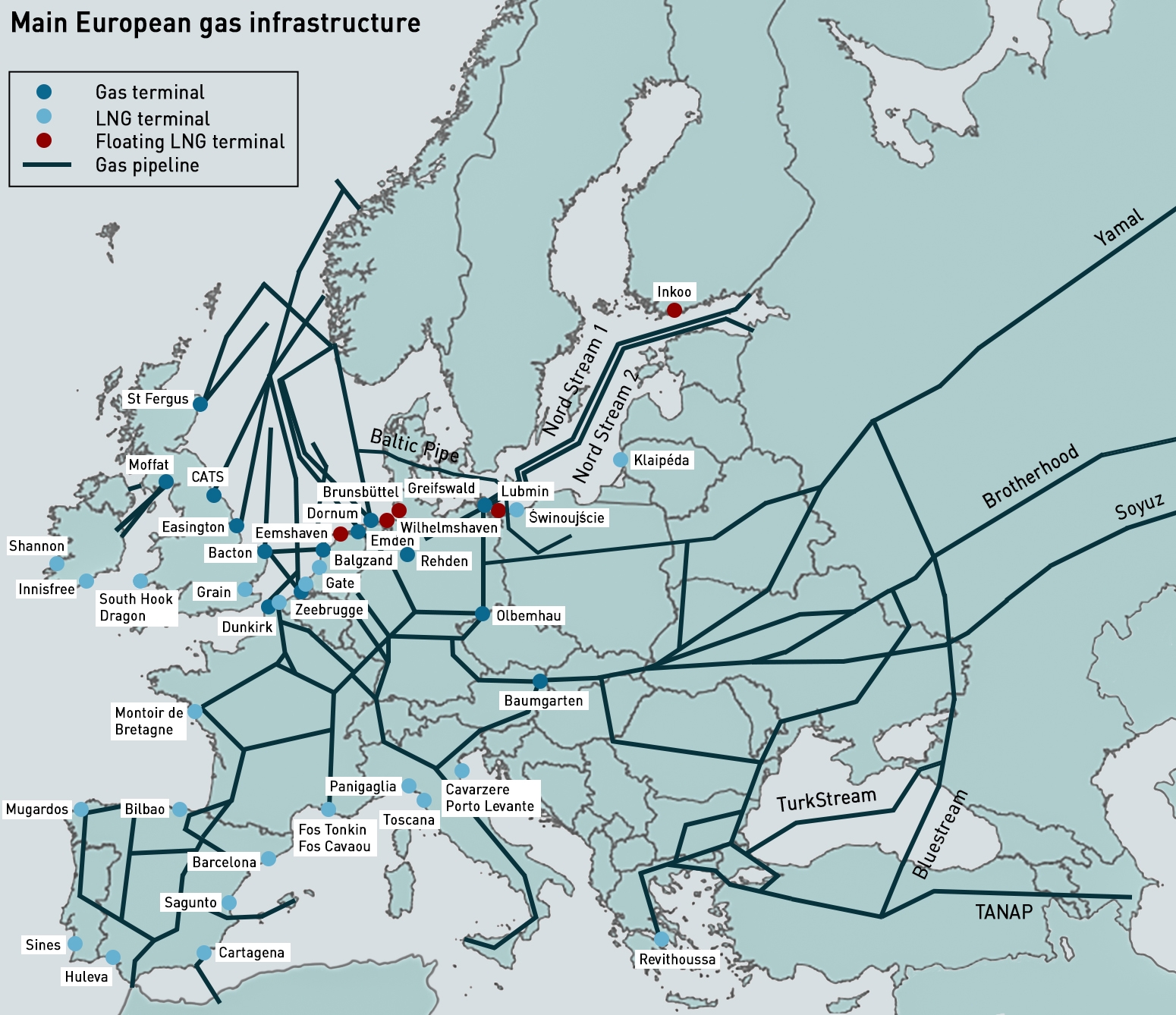

Russian gas exports to Europe

There are four main transit routes for Russian gas into Europe: Nord Stream through the Baltic Sea, Yamal through Poland, Brotherhood and Soyuz through Ukraine and Turk Stream. In May 2022 flows through Yamal were halted as the Polish gas operator was sanctioned by the Russians for refusing to pay for gas in roubles. Flows through Nord Stream gradually declined until they stopped altogether in late August, and with the dramatic destruction of sections of the pipes in September they will not resume operations any time soon. Volumes though Ukraine have stabilised at roughly half of their potential capacity while flows though Turk Stream have been more consistent.

In mid-December, Russian Deputy Prime Minister Alexander Novak suggested the country might be willing to resume gas supplies to Europe through the Yamal-Europe pipeline:

“The European market remains relevant, as the gas shortage persists, and we have every opportunity to resume supplies,” TASS cited Novak as saying in remarks published by the agency on Sunday. For example, the Yamal-Europe Pipeline, which was stopped for political reasons, remains unused,”

– Alexander Novak, Russian Deputy Prime Minister

The markets have received these comments positively, but the fact is that these “political reasons” were imposed voluntarily by Russia and could have been removed at any time. While the prospect of the resumption of exports through Poland is positive, there remains a threat to flows through Ukraine where the Naftogaz, the pipeline operator is in dispute with Gazprom which has threatened to cut off supplies if Naftogaz does not suspend its arbitration case against the Russian supplier.

This all matters because the gas which was used to fill EU gas storage facilities ahead of winter 2022 came primarily through Nord Stream. If Yamal does not re-open to replace this gas, and/or if flows through Ukraine are reduced, the EU will need to attract larger volumes of LNG. It has successfully deployed a number of floating LNG terminals to boost import capacity, but with the prospect of an uptick in Chinese buying, prices could start to rise again. Winter 2023 is widely expected to be more challenging than the current winter, and much will depend on the weather in the coming weeks, and how low gas inventories will be going into the summer injection season.

European policy interventions

In 2022 we saw four main areas of policy interventions in the EU:

- Subsidies for both business and domestic consumers

- Gas price caps

- Demand reduction measures

- Windfall taxes

With the exception of demand reductions to protect precious gas inventories, the other interventions may have perverse consequences. Subsidies and price caps can both incentivise gas consumption to be higher than it would have been without the measures – when Iberia introduced its cap on the price of gas used in electricity generation in May, it saw both demand increase and exports to France increase (although the French nuclear problems might have caused an increase in exports regardless). At the same time, price caps can also deter suppliers from selling gas to EU countries, and might impact market liquidity since the cap applies to futures contracts and not OTC trades.

The cap is by far the most controversial of these measures, but it may be just sound and fury with the Commission giving itself widespread powers to suspend the cap or not activate it in the first place. Some countries were concerned about the impact of the cap while others felt it did not go far enough, so it will be interesting to see what happens next, particularly if either ICE moves trading of the benchmark TTF futures contract out of the EU eg to London, or if traders move their trades OTC to avoid the cap which only applies to TTF futures.

UK policy interventions

It was difficult to keep track of UK energy policy in the final months of 2022 after two rapid changes of Prime Minister and their ministerial teams. However, what seems to have survived the upheavals are:

- Subsidies for both business and domestic consumers

- Windfall taxes

- New focus on energy security

The Government has introduced separate support schemes for business and households, but with changes in government there have been changes in the support being offered. Businesses are particularly unhappy that the support scheme is set to expire at the end of March and the Government has missed its 31 December 2022 deadline for announcing what measures will be adopted after that date. There is more clarity for households but as the support is being offered universally, it is very expensive, so may yet change again.

The first windfall taxes were applies to gas producers who have seen profits rise significantly, however, after the Autumn Statement, the carve-outs for new investments were weakened creating a major dis-incentive to new gas production in the UK. This is the exact opposite to what is needed, and several companies have indicated an intention to re-evaluate their activities in the North Sea as a result.

More recently the tax has been extended to electricity generators benefitting from high gas prices driving up electricity prices. This includes renewable generators and nuclear operators. While renewable generators are squealing, some mechanism to re-balance and overly-generous subsidy regime was overdue, which they well know, and so the impact on future investment is unlikely to be significant. However the inclusion of nuclear operators is perverse – Britain has an aging fleet and at a time when EDF is considering investments to extend the lives of two reactors set to close in little over a year, this tax is likely to tip the decision against any upgrade (I contributed to the linked article which was on the front page of the Daily Telegraph on New Year’s Day).

On energy security, there is a new Bill going through Parliament and is now in the Committee stage, but while it is badged as an “Energy Security Bill” it does not really address the key aspects of energy security, particularly around collapsing winter margins, not least because in the next 2 years a further 2 nuclear reactors and all of the remaining coal plant will close. While a review into “energy market regulation to address issues of long-term energy security and affordability” was announced on 8 September, there has been no further information about it. The Energy Supply Taskforce set up by Liz Truss to lead “negotiations with domestic and international suppliers to agree long-term contracts that reduce the price they charge for energy and increase the security of its supply” was abolished by Rishi Sunak.

.

I would venture to guess that the main themes in the energy markets in 2023 will mirror those in 2022:

- How will the EU fill its gas storage facilities in summer 2023?

- Will Russia resume flows through Yamal to replace lost Nord Stream volumes?

- Will competition for LNG remain high supporting prices?

- Will France succeed in re-starting its nuclear reactors?

- Will Norway act to restrict electricity exports?

- Will policy interventions reduce gas production in Europe and gas imports to Europe?

- Will there be blackouts during periods of low wind output in any of the European countries relying on wind power?

In the UK we can also expect further changes in the retail market…

- Will Ofgem change its mind again on ring-fencing customer credit balances?

- Will the price cap be replaced with a social tariff?

- Will the Octopus acquisition of Bulb conclude successfully and how much will it the Bulb bailout end up costing consumers?

And more broadly…

- Will the UK Government get serious about reducing heat losses from homes?

- Will the Government change its mind about the application of windfall taxes?

- Will the Government and NG ESO act on falling winter capacity margins?

I guess my conclusions are that there are currently more questions than answers when it comes to the energy markets. I would encourage the Government to act on those which are within its control.

.

I wish you all a very happy and prosperous New Year!

So the politicians continue to fiddle while Rome fails to burn through lack of fuel.

Happy New Year Kathryn and all those that read and contribute to your excellent blog.

The coal stations maybe old but they don’t have to close and shouldn’t be closed but if they are they need to be mothballed NOT demolished before the boilers have even gone cold for some political photo opp. Mothballing is energy security in action.

Im more optimistic on gas prices albeit they will be settling at a level that is 3 times the 10yr average and our prices won’t be going lower anytime soon ever – reality was there was never going to be any cost benefit from renewables so all this has done is get energy at a price level that support all technologies now. Of course govt will have to progressively unwind its support schemes as they are plainly unaffordable on an indefinite basis.

I reckon Europe will end winter season in good shape on reserves and market will have enough gas for replenishment as it will pay high prices and other countries will resort to the black stuff so it will be a climate impact issue but guess thats the price that needs to be paid to get everything back on an even keel. Wind production has been good since the fall and is helping on gas substitution.

Norway Hydro reserves are better than 12mths ago even NO2 is on a par with last year so that threat looks diminished to me. Weve also been readily importing from Europe even on high wind day which tells you how distorted our market is so is that going to be sorted or not?

Of course im sure it wont turn out that simple but one can but hope.

I agree with the exception of WBA which really does need to close according to EDF. I would keep Rats and Drax open as long as possible and at least until HPC opens.

I also think European gas reserves will be OK come April, but am less confident about how they will be re-filled over the summer. One comment by the Russian deputy PM does not mean that Yamal is set to re-open, and flows through Ukraine could be cut so I think there are a lot of risk factors ahead of next winter.

While the NO2 hydro balance has recovered, I’m not sure the concerns there have gone away. As you say, we keep importing even on high wind days (it’s a DA only market so perhaps that is part of the reason) and the Norwegians have been pretty burned by the past year, orimarily due to the preventable behaviour of its neighbours.

Another very throughly researched piece on ENERGY, Kathryn, but WOEFUL in its first few paragraphs on the geo-politics, suggesting a complete failure to read beyond our legacy media. To catch up, a vast investment in time is required. There are 100s of articles on the Net putting a different viewpoint, mostly American. [names of articles removed by the moderator because I don’t want to link this material to my site].

This is an energy blog, and I believe it is correct to say that no energy commentators predicted the war or that it would impact energy markets which had been largely unaffected by the Cold War. As to the rest of your comments, I have removed the references because I am not interested in sharing pro-Russian propaganda and justifications on this site. Even if Ukraine was full of Nazis which I dispute, they were not acting outside their own borders so no other country had a right to invade them. We do not invade Russia or Iran despite the abuses their regimes perpertate against their citizens. The other logical inconsistency in those arguments is that if Ukraine was full of anti-Polish Nazis, the Polish people would not have provided such high levels of support to their Ukrainian neighbours.

Thank you for this blog.

I feel history will judge what you describe as the Russian Invasion of Ukraine very differently.

I also feel that the upheaval in the global energy industries resulting form this conflict, between a weakening NATO and Russia, and the resulting changing newer emerging world trading alliances will lead to a complete re-evaluation of global energy policy.

It is clear to me that large parts of the world are not seriously buying into Net Zero. This will force the UK and Europe to change track for sure as our industry simply becomes uncompetitive with the rest of the world.

The sooner we realise this the better. As is well outlined within your pages we have a dynamic energy Industry in the Uk with all options open and desperate for the debates to begin, there seem to be so few people in politics trying to open the debate, John Redwood perhaps?

My appeal to you is to, obviously carefully, use your platform to facilitate good debate.

Your points about insulation are very smart. I have over the last 15 years had great enthusiasm for and spent some energy perusing this promise.

I trained as a Home Inspector, Energy Assessor and Green Deal advisor. As such I surveyed many properties and saw many of them gain improvements such as external wall insulation, internal insulation in particular as well as solar panels and heat pump systems. Most of my work came to abrupt halt due to the uncertainty of funding over ECO etc whilst I are my sandwiches by a park in Swindon in 2014 my work on wall insulation was suddenly cancelled. Disappointing for me but devastating to some terrific efforts made by Industry to provide solutions. Time and time again I learned that government was far to volatile to be trusted.

However I was also never comfortable with subsidies especially where wealthy home owners, Landlords, were taking advantage of having tenants on benefits to gain heavily subsidised home improvements as the expense of the general bill payer!

However I have just put in my gas and electric readings for the quarter. Yes I admit I have taken a lot more interest in this than ever before but I am genuinely surprised that I have cut my consumption by over 20% and hardly noticed. Ok I have sometimes changed into thermals and a woolly hat after getting in from work rather than the other way around but I have been comfortable and warm.

I do feel that if people are properly advised they can all make savings. I have spoken to tenants recently horrified by the bills in new properties with Air Source Heat pumps where it was so obvious that they were not using the systems correctly, simply not understanding how to work their heating, professional educated people with instruction booklets at their finger tips.

There is an army of people out there desperate to help their neighbours, yet where are the energy advisers! A great idea not fulfilled!

Net zero is something supported by eco-warriors and politicians who bought into the eco ideology. As you say there are many countries that do not buy in to it and there are many ordinary people in countries with net zero policies which also do not buy into it, particularly when they understand the costs involved. I think it’s important to differentiate between “net zero” and sustainability, and I have always been sceptical that a single-minded focus on carbon dioxide is the right approach – should we encourage pollution of major fresh water sources in order to process the lithium needed for all those electric cars for example?

I am against net zero by 2050 and am not persuaded that net zero at any time is a reasonable goal. However I am very much in favour of sustainability starting with avoiding (eg not replacing well maintained ICE cars with EVs until they reach the end of their lives) and reducing waste eg through better insulation.

I also agree that a cultural change is needed – too many people have heated their homes to a level where they can be comfortable in t-shirts and bare feet in the middle of winter, and increasingly bedrooms are heated at night because more people want to sleep naked. I think these are irresponsible choices and should be discouraged – the first response to being cold indoors should be to put on more clothes, not to turn the heating up. The University of Bath study I reference on here a lot showed that heating controls in individual rooms save a great deal of energy – when you do need to turn the heating up, you often don’t need to do it in the whole house.

Not understanding heating controls is a widespread problem, not just with new types of heating – I know people with electric UFH in flats who can’t operate the controls, and often it is because they are very unintuitive. This would be another useful areas for regulation – standardisation of heating controls with a requirement for them to be clear and usable without reference to a manual.

Happy New Year Kathryn! Thanks for your wonderful reads in 2022, and all the very best for 2023.

“Will the Government and NG ESO act on falling winter capacity margins?”

Out of curiosity, do you know if there were any capacity concerns during the Arctic Blast cold snap just before Christmas? I used a lot more heating than I wanted to, and wondered if National Grid was being stretched nationally, and whether this could have any knock-on impacts should we have another icy period later on in Jan/Feb.

HNY to you too!

Yes, the grid was definitely challenged in the cold snap with the DFS coming close to being exercised for the first time. I think any further cold periods will be independent of this though…the previous one won’t impact a later one other than from operational learning.

I note that supply via EUstream has cut back in the new year, but it does not seem to have troubled the markets. OTOH, Russian LNG continues to flow from Sabetta and Vysotsk particularly to Belgium, Spain and France, with some to the Netherlands. Volumes to the FEAST remain muted, and are mostly via Suez with transshipment usually off Murmansk.

PF Bach has an excellent annual review concentrating on Scandinavia and Germany. There are interesting lessons and watchpoints for the UK.

http://pfbach.dk/firma_pfb/references/pfb_challenged_european_electricity_markets_2022_12_14.pdf

We still have to get through the French nuclear maintenance for February, which could prove another tight period if the weather conspires. I note that in the US, Duke was forced to implement rolling blackouts in the Carolinas over Christmas. Wise of them not to let the situation escalate out of control as happened in Texas in Feb 21. Dispatchable capacity shortage is becoming a general theme. The Germans are planning lots of new CCGT. We are planning bigger shortages.

Thanks for this… will add it to my growing reading list!

The issues with dispatchable generation are leading to a lot of US states back-tracking on nuclear closures and not before time…

I see BEIS has published a consultation on altering the capacity mechanism to adjust the composition of capacity towards net zero. It seems to be full of unicorns, and fails to recognise the catastrophe in dispatchable capacity that is looming. 4 year time horizons are far too short when major investment will be required. Cost doesn’t even enter their equations. Delusional.

This is another thing on my reading list and I was mulling submitting a response, time allowing.

My big issue with the CM is the procurement target – I think NG ESO is under-estimating the need because it ignores the correlation between cold and still weather in winter and the fact that still weather in summer coincides with CCGT and nuclear maintenance outages. They seem overly reliant on their monte carlo models but I wonder if they are paying enough attention to the model inputs and model design. Garbage in garbage out is a real thing, and just because you have a monte carlo model doesn’t mean your outputs are reliable.

I had a chat with Fintan Slye about this in December and am trying to write a blog about it but have not had time to run some of the numbers I need to for it. He did recognise that at some point they would need to change their modelling approach, and made a valid point that this would lead to procuring more generation capacity which has a cost to consumersif it isn’t needed, but I worry that being overly concervative means they will run out of time to get new capacity built in time. You can build a CCGT in 2 years (not easily but it is possible)…with a huge amount of capacity coming off in 2024, that winter is going to be interesting. Good news that RATS is keeping all its units open for now though.