On Monday, the new Chancellor, Jeremy Hunt, shocked the energy market by potentially limiting the domestic Energy Price Guarantee (“EPG”) to just six months, rather than the two years initially promised only last month. Of course, the Government is in utter disarray, and who can say whether this will be the last policy reversal and whether the markets can rely on anything the Government has to say. Indeed, many commentators believe that the current administration is doomed, and we may see yet another Prime Minister take office before the year end, so it is difficult to have confidence in the current policy direction.

The Chancellor has said that HM Treasury will now carry out a review into the support scheme for households, indicating that after April, it will no longer be universal but would be targeted at those most in need. The level of the support may also change.

“…the biggest single expense in the Growth Plan was the Energy Price Guarantee. This is a landmark policy supporting millions of people through a difficult winter and today I want to confirm that the support we are providing between now and April next year will not change. But beyond that, the Prime Minister and I have agreed it would not be responsible to continue exposing public finances to unlimited volatility in international gas prices.

So, I am announcing today a Treasury-led review into how we support energy bills beyond April next year. The objective is to design a new approach that will cost the taxpayer significantly less than planned whilst ensuring enough support for those in need. Any support for businesses will be targeted to those most affected. And the new approach will better incentivise energy efficiency,”

– Jeremy Hunt, Chancellor of the Exchequer

Before this announcement, the Government had committed to two support schemes: the EPG for households which was to hold prices at an average of £2,500 for a dual fuel, standard credit household for two years until the end of winter 2023; and a business support package which was to run through this winter with further support for as yet undefined vulnerable sectors to be implemented thereafter.

There was also talk that after the expiry of the two year support scheme for households, the Government would abolish the price cap, potentially allowing the market to revert to its state of operation prior to 2019.

So what can we expect now?

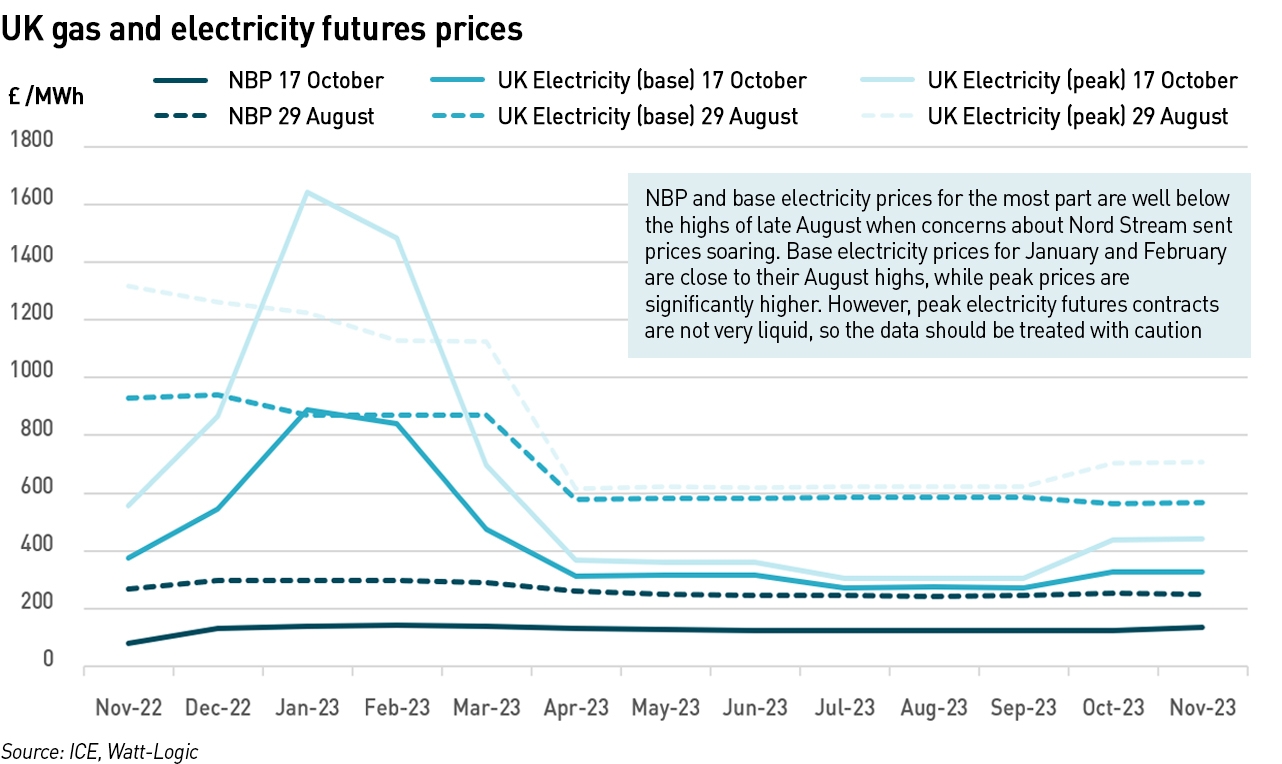

Subject to the potential-further-u-turns caveat, we can now expect the price support to only apply to vulnerable households, and that potentially the support level may change. It is possible that by limiting the scope of the support, prices could be lowered for vulnerable households, possibly to the previous cap level or lower. Since late August when the normal price cap level was anounced, and the price supports were designed, market prices have actually fallen significantly.

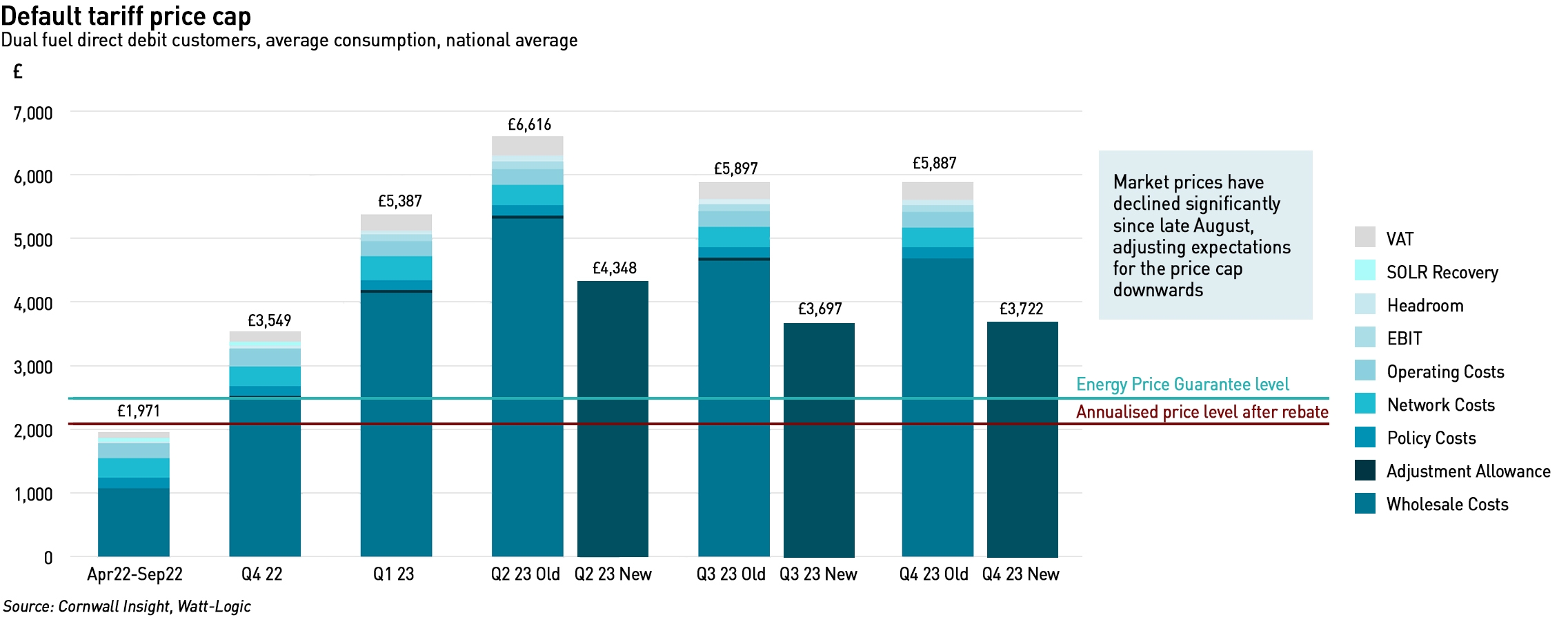

Where Cornwall Insight had previously forecast the April cap level to rise to over £6,600 before coming down to around £5,900 for the second half of next year, it is now predicting a cap level of c£4,350 in Q2 23 and £3,700 in H2 23.

On this basis, it is not unreasonable to explore whether the price support remains appropriate, although these prices are still materially higher than the £1,971 cap level in place prior to 1 October. Indeed, before the announcement of the Energy Price Guarantee, I had called for a more targeted approach, suggesting that at least until January the support should be universal as it was impractical to develop a targeted scheme within just a few weeks, but that from the New Year, a support should be directed to those in need. My proposal was to link the support levels to income tax brackets, recognising that with energy prices as high as they have been, even middle-income households might struggle to pay their bills.

“…if gas and power prices fall, it could be argued that keeping the EPG as it is currently would contain few risks. I would suggest though that as suppliers bought ahead for this winter there are likely to be c£30bn of costs already locked in. If gas and power prices rise into winter 23-24, without any change to approach, there would be exposure to heightened cost risks over which no UK Minister has real control. We can hope that they won’t, but in a febrile economic and market environment, hope is not a strategy and leaving uncovered downside risk would be very challenging indeed…

A world in which we move back to the default tariff cap cannot credibly be one that is amongst those options given the heightened cost environment likely to prevail in the medium term and the situation that arose before the EPG was implemented,”

– Gareth Miller, CEO, Cornwall Insight

The question is what will the Government come up with now? Fortunately, there is a reasonable amount of time to develop a scheme for April 2023 onwards – ideally suppliers would be notified no later than the beginning of March, but a shorter notice period is manageable as it was ahead of the implementation of the EPG.

Prior to the EPG, suppliers hedged their gas and power exposure in line with the price cap methodology as far as they could given credit and liquidity constraints. However, it is unclear whether they continued to do this since the announcement of the EPG (perhaps readers involved in the discussions with BEIS might add some comment…). If I had designed the support scheme, I would have required suppliers to continue to hedge based on the price cap methodology since this is well defined and can be used as an objective basis for reimbursing suppliers under the EPG. While I don’t love the fact that this methodology constrains suppliers to a particularly narrow method of hedging, it does provide a baseline for quantifying the amounts that should be paid to suppliers to fund the discount to their customers.

Developing a more targeted approach will be more complex, since now some means of customer segmentation must be developed. My preference is to utilise existing data…there is precedent in that suppliers receive eligibility data for the Warm Homes Discount (“WHD”) from the Department for Work and Pensions, but a new type of segmentation might require significant upgrades to supplier IT systems.

As regular readers will know, I disapprove of the Government using suppliers to distribute welfare…in my opinion the Government should administer the WHD itself. So I’m inclined to the idea that instead of forcing suppliers to make potentially complex changes to their databases and billing systems, the Government could incorporate additional support for energy bills within the existing tax and benefit system. For example, if support is linked to income tax brackets then why not simply adjust the tax rates and increase benefits for people that do not pay income tax?

Is the business support scheme distorting the market?

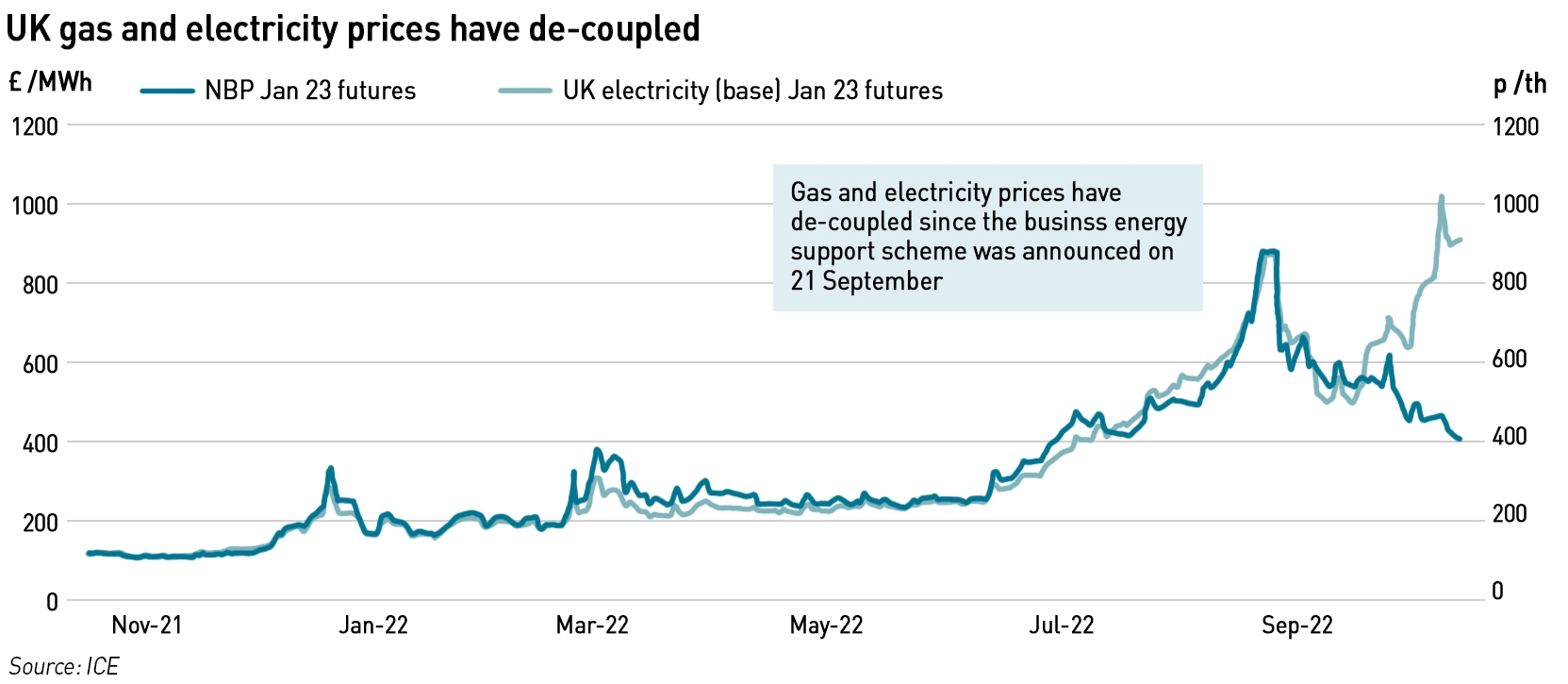

Since the Energy Bill Relief Scheme for non-domestic consumers was announced on 21 September there has been a breakdown in the relationship between UK gas and electricity prices, possibly explaining the higher electricity futures prices for January and February described above. The scheme effectively limits the costs of energy to £211 /MWh for electricity and £75 /MWh for gas, with discounts of up to £345 /MWh for electricity and £91 /MWh for gas available.

The question is why have prices de-coupled in this way? Some commentators are suggesting that this is a result of the price cap being more generous for electricity than for gas, allowing businesses to spend more, particularly if they had cheap partial hedges in place. Certainly, the timing of this de-coupling suggests some connection with the price support scheme, and if this is the case, then the Government and Ofgem should investigate to ensure that no-one is attempting to profit from the price support.

“Non-domestic suppliers and consumers must not profit from the scheme other than for its intended purpose of providing relief on necessary energy bills. Any such activity will result in support being refundable to government and may be liable to further penalties,”

– UK Government

But I wonder if there isn’t another explanation…the market seems to be pricing in a large premium for electricity in January and February next year, particularly for peaks. This might be an indication that the market believes there could be electricity shortages but not gas shortages at the coldest part of the winter. The timing makes less sense though since the prices began to diverge several days before the winter outlooks were published on 6 October, and in any case, the market has been forming a view on the prospect of shortages or not for months…industrial consumers were telling me as early as March this year that they were worried about electricity shortages and possible curtailment this winter.

A possible explanation that covers both the price diveregnce and the timing is that the Winter contracts expire at the end of September and normally market participants would refine their hedges, building positions in individual months and the peaks to better manage their shape exposure. Given the Government had indicated to the market that an intervention would be made, it is possible that market participants delayed their re-hedging until after the announcement on 21 September. At this point, prices began to reflect a shift in fundamentals for January and February with the effect being strongest in the peaks which would refect a view that it might be difficult to meet peak demand at times in winter.

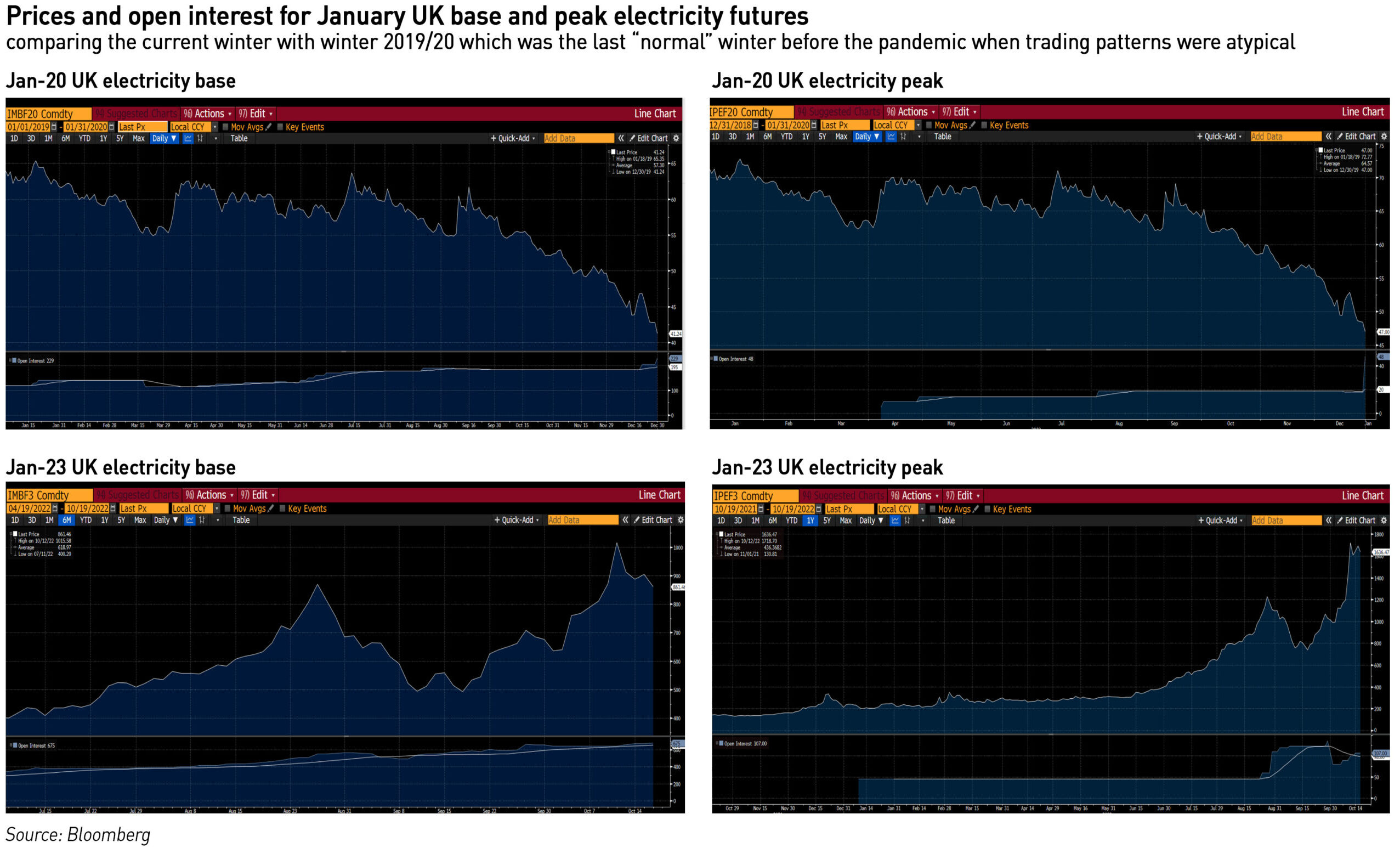

Trading patterns might support this hypothesis. The open interest in the Jan 23 Peak contract shows a trading pattern that is not observed in previous years, although the unusual pattern began in late August, and the open interest in the Jan 23 Base contract is materially higher than in previous years. Of course, the main UK power market liquidity is OTC, but these differences in futures trading patterns are interesting. It isn’t possible to fully explain this behaviour from the futures trading data, but I’m inclined to believe that the divergence in gas and power prices reflects the fundamentals with the timing being affected by Government announcements, rather than attempts by any market participants to profit from the price support. I would be interested in readers’ comments on this.

In any case, recent pricing and trading patterns yet again highlight the dangers of creating market distortions from interventions, however well intentioned. Given the very high prices the market was facing, it was necessary for the Government to provide support, but this should potentially direct future support mechanisms to the tax system rather than intervening in market pricing. When designing the next phases of support to be introduced to vulnerable sectors and households, the Government should give serious thought to whether it should leave the energy market alone and deploy the support through other means.

The BoE has launched the Energy Market Financing Scheme to allow suppliers to access collateral to support forward hedging so this could be exploited to lock in lower prices now becoming prevalent although they could go lower they could go higher so suppliers should be encouraged to utilise it.

Also i can’t see govt can reliably meddle in the market and not avoid unintended outcomes be it domestic or business without really knowing what arrangements suppliers have in place already.

I gather that EMFS requires applicants to set out their net zero plans. I hope some would have the necessary fortitude to say that they will comply with government directives to shut down and leave the public freezing in their homes.

The Government cannot afford for another energy supplier of a million customers or more to hit the wall. Bulb has been an expensive lesson and has to be the last.

The support package continuing past April 23 will be guided by the data they hold on customer account debt sensitivity to price change. If the Government get it wrong, large suppliers will fail (withdraw), consumer spending across the economy generally will drop, public purses will suffer and we are back into crisis (or deeper into crisis depending on your viewpoint). Announcing a shortening of the energy bill support package served a purpose to stabilise the markets. But the problem hasn’t gone anywhere for millions of households. With the change in wholesale prices of late however, fortunately it may have reduced somewhat.

I like the idea of energy support payments going through benefits. Within that system there is already a record of those who are struggling financially and by how much so support can be targetted much more effectively.

However, payments from central government is a patch and not a solution to energy poverty. Although more complex if the cost of energy support could be pushed to local councils (refunded centraly) then local councils might be able to come up with cost/benefit plans for investment in housing energy efficiency upgrades. Imagine for instance, if a council upgraded the heating system to a block of flats rather than make lots of small individual payments. The upgrade could pay itself back and we would have something for it at the end. This would require though that energy payment support to combat energy poverty be permanent going forward, because jobs and skills need that kind of guarantee.

The problem is that there will be a whole new gamut of people who were formerly just managing who are outside the benefits system, and who will now be plunged into extreme difficulty. Also those facing a double whammy with rising mortgage costs.

This is true but it’s why I would use the tax system as well as the benefits system. By adjusting the tax rates you can simulate different levels of support for different income groups.

“My proposal was to link the support levels to income tax brackets”. This is fraught with potential unfairness. Many households have a low income for tax purposes but have high capital assets. It is also an incentive for ‘cash-in hand’ self-employment if lower declared income leads not only to lower tax but the prospect of a government hand-out as well. Energy used for home heating has no or minimal tax, in contrast with road fuel. Ideally, all fuels used for all purposes should cost the end consumer the same per unit of carbon emitted. This would encourage energy efficiency and energy use reductions where they are most effective.

The problem with your proposal is that it massively penalises people on low incomes that have low levels of assets. How can such people afford demand reduction measures such as more efficient appliances, better insulation, solar panels etc. This is the exact problem with the current method of recovering green levies (absent the current relief) – it assumes everyone has the means to reduce their consumption, but for many households that means harmful choices between heating and eating. Families coping with disabilities are being particularly badly affected by the current high prices.

It will be difficult to design a scheme that does not have high admin costs and also avoids unfairness. I think we can live with a bit of unfariness if we can develop a system that is easy and cheap to administer and does not waste money on lots of new systems and processes.

I can see no alternative to linking at least a portion of the support to the market in some way. It clearly makes no sense to hand out cash willy-nilly if prices turn out to be much lower, for instance. It would make sense to cap the volume of that support to give a stronger incentive to economise at the margin while market prices remain tight. It is probably a useful simplification to consider winter demand of say 600TWh of gas including CCGT demand, supplemented by other market priced electricity (ROC renewables, nuclear etc.) of say another 100TWh which is another 200TWh of gas equivalent exposure. That may be too big, and there are ways to finesse the numbers, but for the purpose of estimating exposure it is probably good enough, allowing for the extra volatility of electricity at times of capacity shortage. The price guarantees are for an average over the winter. In the case of industry, the effect is an Asian collar, with a floor price at £75/MWh and a ceiling at £166/MWh for gas, with the government taking the risk between those prices, but an allowance for network and other non commodity costs must be subtracted before comparison with wholesale cost can be made. The exposure is reduced for hedges actually already in place. For electricity, the collar runs between £211/MWh and £556/MWh, but again network and other costs must be subtracted before comparison with wholesale power prices can be made. In the case of domestic consumers, the guarantees are in fact an Asian cap: if prices were miraculously to fall there would be no subsidy required, but government liability is uncapped to the upside.

To illustrate the arithmetic, assume gas network etc costs are £25/MWh, so the underlying wholesale would be £50/MWh before the price guarantee kicks in for gas for industry. However, any excess in average wholesale prices beyond £141/MWh is for customer account.

These are complex derivatives to price even in more normal markets. However some underlying features are worth noting. Once the averaging period has started the effective market volatility is just a third of the volatility that applies to normal options where the payoff is determined by prices on expiry. Also, the effective strike price gets altered as more of the average is priced, and the exposure to market price changes rapidly either falls away or becomes total.

The positions are of course completely unhedged naked options, whose real cost will ultimately fall on taxpayers. There is one available hedge: encourage more production that will reduce prices.

It is of course highly doubtful whether the position has been properly analysed in government, the OBR or the BoE. Perhaps commodity traders in banks will have had a go to advise their bond and currency dealing colleagues.

While I love a good derivatives solution, I think it would be complicated to implement (and actually there is no market for electricity options in the UK anyway). If I were in Government I’d keep this high level…people are struggling with energy costs and inflation (which is itself partly driven by energy costs). Many of these effects are temporary, so the value of coming up with complex solutions is going to be limited.

In the short term I’d just use a simple method to give people more money eg cutting taxes / increasing benefits, and in the longer-term I would ditch the price cap and develop a social tariff that would target support at the fuel poor. I would also set up a proper scheme for addressing heat losses in homes starting with the fuel poor so that beneficial demand reductions are achieved.

I wasn’t trying to propose a derivatives solution, which in any event is not feasible given the size of positions being taken by governments and the illiquidity of markets. It is more a case of analysing the exposure the government has taken on. The initial analyses were I think simple mark to market affairs relative to the strike prices, and were thus wrong. Proper evaluation is to recognise the embedded options in their scheme and value those. The fact that prices have fallen for gas across the winter and those lower prices are now being incorporated into the averaging will limit the upside exposure. Of course historic forward hedging will likely impose a big cost to begin with, because it is likely to have been at much higher prices.

I note that the winter Baseload Market Reference Price has been set at £405/MWh. Drax and Lynmouth appear to have shuttered their CFD backed woodburners in response, since every MWh produced incurs a tax of over £270/MWh, and I imagine they are barely profitable at the underlying CFD prices, with woodchips likely indexed to coal prices to make it theoretically hedgeable. These units will now only run when we get high peakload prices. The ones on ROCs will of course continue to coin massive profits. Another scenario that I suspect was unplanned for.