Gas markets have been on a bumpy ride recently and it has been difficult to keep track of the news flow. This blog provides an update on some of the key events of the past few weeks.

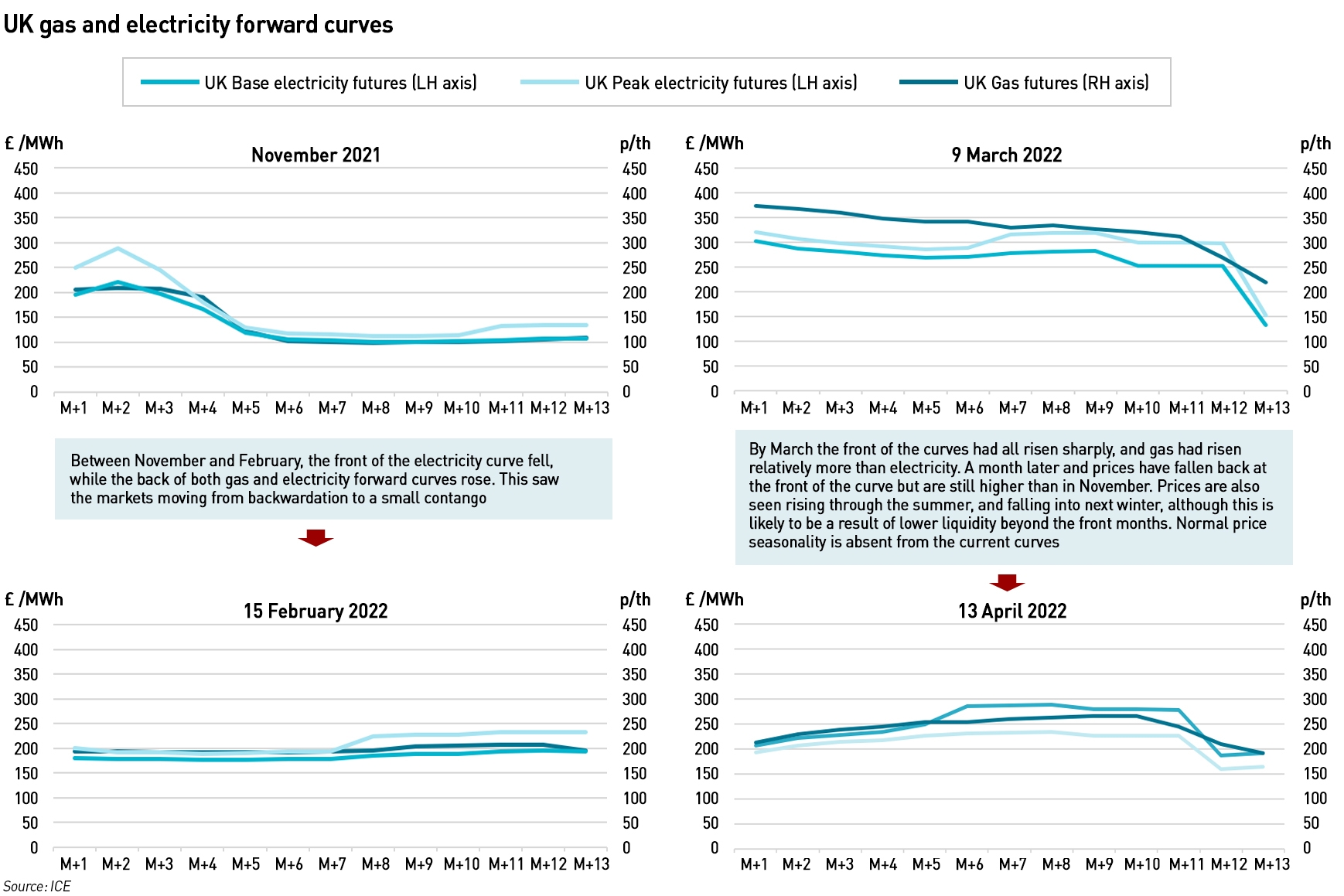

Prices have retreated from their highs but the forward curve makes little sense

Gas prices have been on a roller-coaster ride. Last autumn prices began to rise significantly as the post-covid demand recovery outstripped the increase in supply. At the time, the consensus was that provided the winter was not unduly cold, the global gas market would re-balance at some time in 2022, probably the second half of the year. As the winter progressed, it became clear that this view was optimistic – while the winter proved to be mild, storage levels had fallen to a degree that meant it would be difficult to restore them to usual levels before next winter. A flood of LNG arrived in Europe at the beginning of the year as high prices secured cargo diversions away from Asia, so there was some hope that after another winter, markets would re-balance.

A week before the Russian invasion of Ukraine, Eni’s Chief executive predicted that gas markets would remain tight for at least the next four years…a slightly more pessimistic forecast than other analysts had been making, but indicating that there was no immediate prospect of the markets re-balancing as had been hoped by many, including me, when prices began to ramp up in the autumn. A week later Russia invaded its neighbour and the picture changed dramatically.

The idea of a full-scale invasion of a sovereign European country by a hostile power had seemed far-fetched, but it happened, and the rest of the world reacted with shock. Most countries are strongly opposed to this outrage, and the response has been swift and more extensive than might have been expected. For the first time ever a country has had its foreign reserves frozen – this did not even happen to Germany in World War II. Wide-ranging sanctions have been imposed on Russia and both the country and its businesses have been largely excluded from the financial markets.

As far as energy has been concerned, the response has been more nuanced. The UK has very little dependence on Russian energy and can easily replace these volumes, but within the EU there are countries for whom reliance on Russian gas, oil and coal make it impossible to embargo all things Russian. For its part, Russia also relies on the income these sales generate, so while threats to cut off gas supplies have been made, that would be a significant act of self-harm by Russia. Under any sort of “normal” circumstances, countries would be expected not to act against their own interests, but the conduct of the war in Ukraine has exposed legitimate questions about the rationality of the Russian leadership. On the other side, the horrors taking place in Ukraine are leading the European public to an increasing willingness to endure some hardship if by those actions the suffering of the Ukrainian people can be ended sooner.

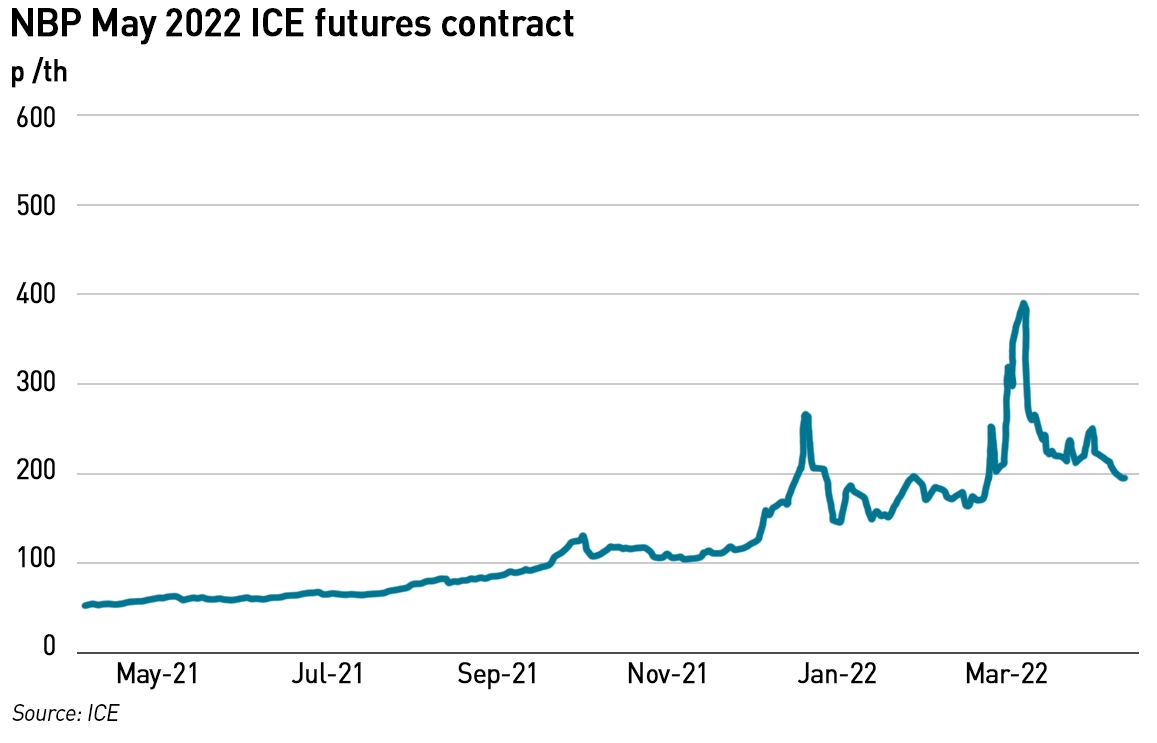

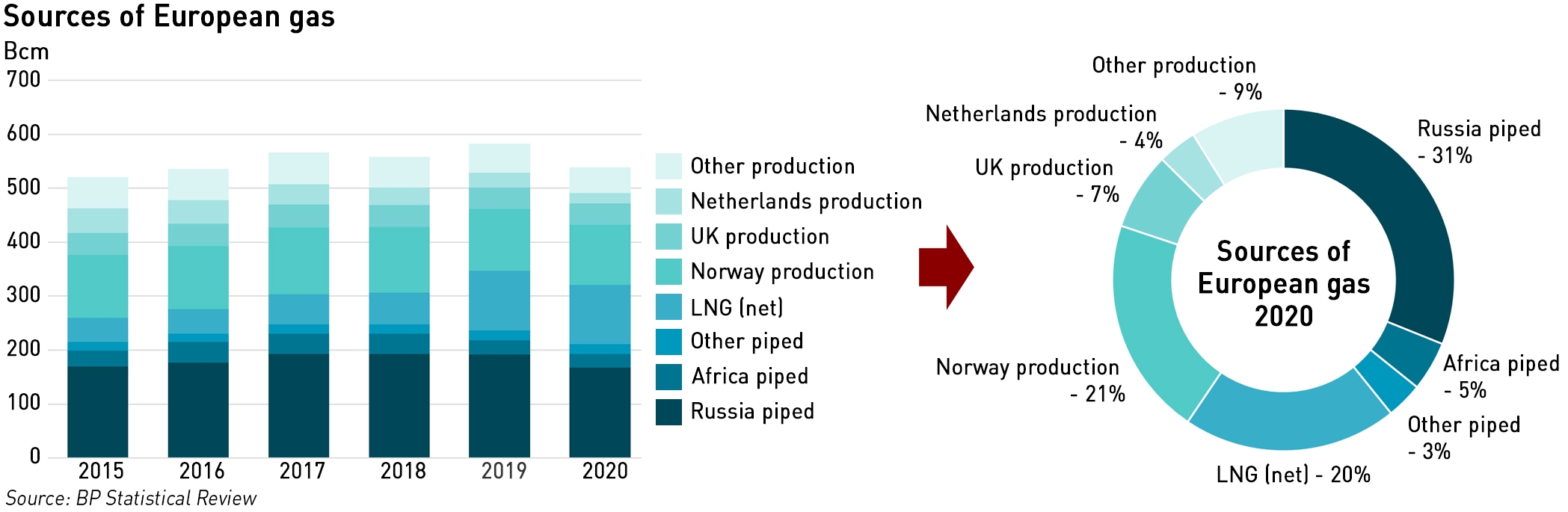

The ups and downs of this have been reflected in gas prices. Early March saw gas prices spiking with intraday prices reaching 800 p/th on the 7th as the US asked its allies to consider a ban on Russian oil imports. The following day, Russian deputy prime minister Alexander Novak threatened to cut gas supplies to Germany through Nord Stream 1 and the US announced it would ban imports of Russian crude oil and oil products, gas and coal. At the end of March, the US agreed to supply the EU with around 10% of the gas it currently buys from Russia by the end of the year, and new LNG terminals are planned for northern Europe. But as Russia supplies around 40% of Europe’s gas, replacing it will not be easy.

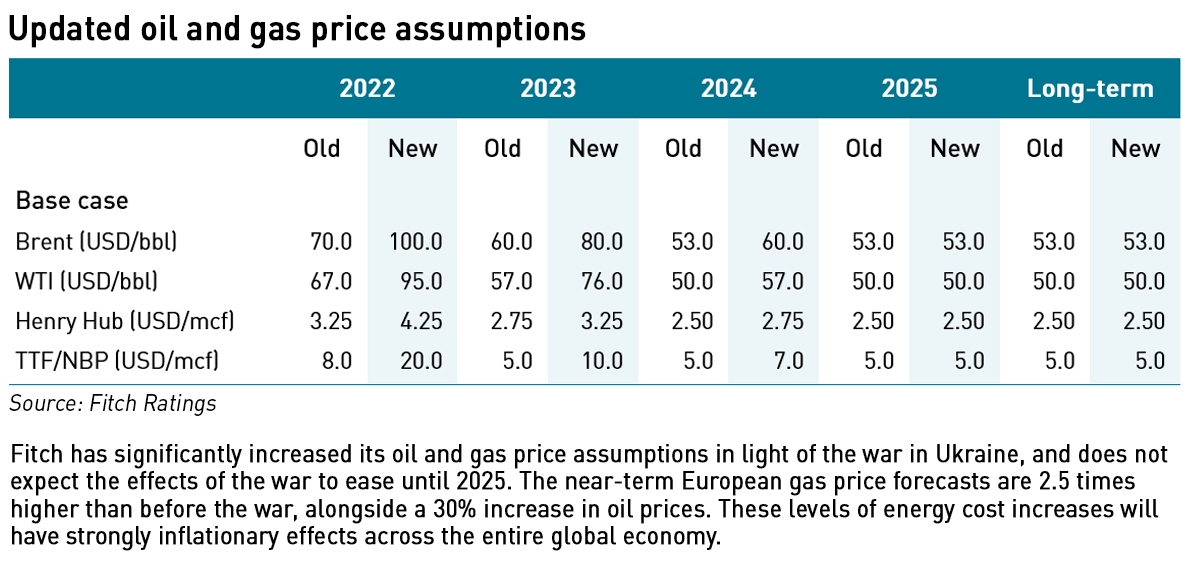

Forward curves have taken an unusual journey, but the markets are not functioning well – liquidity is concentrated at the front of the curve and normal seasonality has broken down. Analysts are all predicting higher prices. Fitch Ratings increased its European gas price forecast for 2022 by 2.5 times to US$20 /mcf while J.P. Morgan increased its TTF forecast for summer 2022 to €77.5 /MWh, keeping its full-year forecast at €81.25 /MWh. BoA Global Research expects the 2022 TTF to average €105 /MWh falling to €75 /MWh if the conflict can be resolved. On the downside, it sees prices rising as high as €200 /MWh should restrictions in Russian supplies lead to major structural deficits.

Then on 23 March Russian President Vladimir Putin shocked the market again by announcing that he had signed a decree saying foreign buyers must pay in roubles for Russian gas from 1 April, and that contracts would be suspended if these payments were not made. The decree set out a mechanism for buyers to transfer foreign currency to a special account at a Russian bank, which would then send roubles back to the foreign buyer to make payment for the gas. This is seen as a move to support the Russian currency which fell to historic lows after the invasion.

“In order to purchase Russian natural gas, they must open rouble accounts in Russian banks. It is from these accounts that payments will be made for gas delivered starting from tomorrow. If such payments are not made, we will consider this a default on the part of buyers, with all the ensuing consequences. Nobody sells us anything for free, and we are not going to do charity either – that is, existing contracts will be stopped,”

– Vladimir Putin, President of Russia

However, this is not how contracts work. The contracts for Russian gas supplies to Europe require payment in euros or dollars, and neither party can unilaterally impose a change in the payment or any other terms – any attempts to do so would likely lead to lengthy arbitration processes. At the same time, Putin insisted that Russia would honour its contracts in a seemingly contradictory statement.

“Should renegotiations start at the insistence of Russia, it is likely that importers will be offered value elsewhere in their deals with Russia in return for the change to rouble payments. The challenge to put this in practice is that each buyer may have different conditions, while some may not even be willing to alter contractual terms. This suggests that negotiations might take some time, which means there is still no abrupt deadline for the payment to switch to roubles,”

– Vinicius Romano, senior analyst at Rystad Energy

A week later there were signs of softening in the Russian position, with a Kremlin spokesman stating that the switch to roubles would likely be a “gradual process” alleviating the risk of supply disruptions which had prompted several EU countries to draw up plans for rationing gas. Germany has urged consumers to reduce consumption in anticipation of possible shortages, and Austria has said it is increasing its monitoring of the gas market. The countries have existing gas emergency plans and have begun the “early warning phase” which is the first of three steps designed to prepare for a potential supply shortage. In the final stage, the governments would implement gas rationing.

Analysts at political risk consultancy Eurasia Group believe it is unlikely Gazprom will violate its contracts by suspending supplies to customers who refuse to pay in roubles in the short term, saying that it is more likely to try to re-negotiate these contracts in the context of the periodic reviews already anticipated within the deals.

The EU’s new gas storage rules may make matters worse

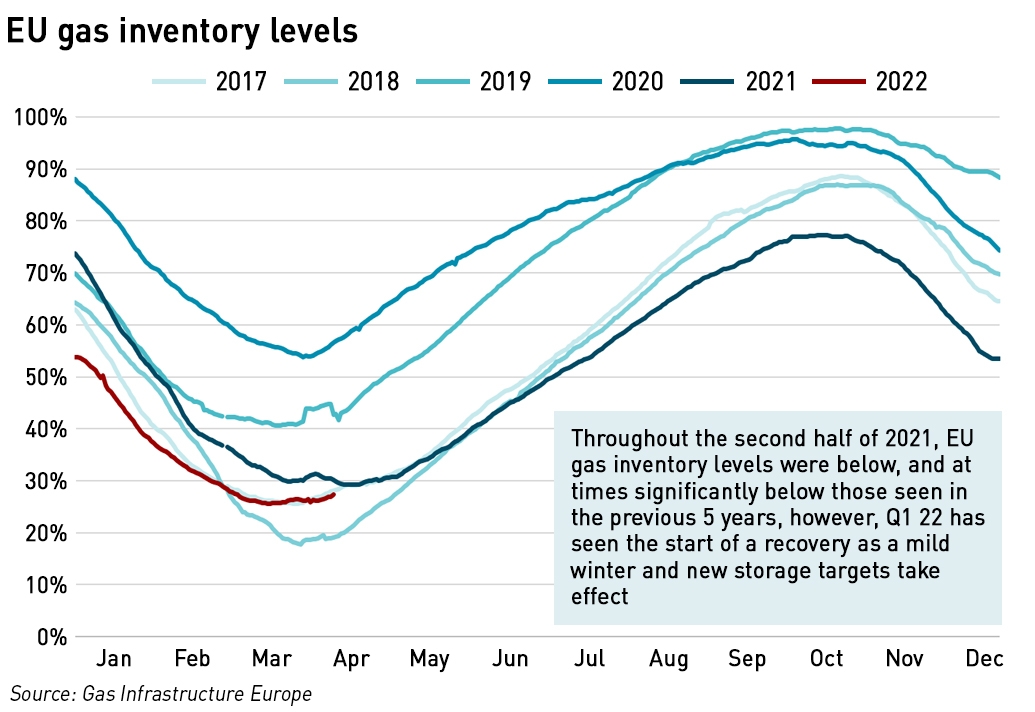

In response to the ongoing crisis in the gas markets, and concerns over low inventory levels the European Commission has outlined its intentions to require underground gas storage across the EU to be filled to at least 90% of capacity by 1 October each year. The proposal would “entail the monitoring and enforcement of filling levels and build in solidarity arrangements between Member States”. To put this target in context, in only two of the past six years have inventory levels exceeded 90% (although in one year they were only very slightly under). At the beginning of this year’s injection season on 1 April, EU gas storage facilities were 26.4% full at the lower end of what is normal for the time of year, but a mild winter and an influx of LNG helped levels to recover. Market prices jumped on this news, forcing the Commission to modify its proposal for this year to a target of 80% by 1 November, rising to 90% in future years.

Seasonal gas storage is certainly helpful in ensuring security of supply, but gas can only be injected into storage facilities if it is not needed for immediate use. So far flows from Russia have remained stable, but the EU would like to discontinue buying from the country as soon as possible, and there remains the risk of disruptions, either for political reasons or as a result of the destruction of physical infrastructure, some of which runs through Ukraine. Last summer injections were limited because catch-up maintenance after covid reduced supplies, particularly from Norway, and while Norway has agreed to reduce maintenance outages over the near term it is currently producing at close to capacity.

This means that in order to accelerate the filling of storage more gas will need to be precured than would typically be the case over the summer, and the purchase of additional volumes from Russia will almost certainly be avoided – in fact the EU has pledged to cut demand for Russian gas by two thirds by the end of this year. Lithuania is the first EU country to stop Russian gas imports entirely. Russian deliveries via Ukraine have increased to their contractual maximum since the invasion, however flows through the Yamal-Europe pipeline remain erratic and mostly at zero, having seen reverse flows during parts of the winter.

“Platts Analytics forecasts continued strong LNG deliveries and record Norwegian gas production for Q2, with production permits increased, maintenance delayed, and gas over oil prioritisation continuing… Industrial and power sector gas demand destruction and switching are also forecast to continue, with residential/commercial demand in Europe now trending below 2018-2021 averages,”

– S&P Global Commodity Insights

The US has pledged an additional 15 Bcm of LNG this year to help Europe, and Azerbaijan is also now producing at maximum capacity. Qatar has agreed a long-term LNG deal with Germany and gas promised to maintain supplies to Europe even if other buyers are willing to pay more, and the EU has dropped its 4-year anti-trust investigation into Qatari LNG deals with Europe.

Italy has announced a new supply deal with Algeria. Italy buys about 30 Bcm of gas from Russia each year, 40% of its total consumption, and 21 Bcm from Algeria representing 31% of annual consumption. The Trans-Mediterranean pipeline which brings gas from Algeria to Italy via Tunisia is currently operating at only two-thirds of its 33 Bcm capacity, providing scope for increased deliveries, however domestic consumption in Algeria is rising and with existing fields possibly producing close to maximum levels, it may be difficult for exports to be increased significantly in practice, at least in the near term.

It remains to be seen whether these agreements will help the EU reach its storage targets this year, but it seems doubtful if purchases from Russia are to be reduced at the same time.

The Commission intends to make collective purchase agreements for gas and other fuels in order to increase its market power when negotiating with sellers. However, previous efforts to establish a common gas buying system failed, for several reasons: it raises problems under competition law, could see countries arguing over access to supplies, and creates potential clashes between energy companies and governments. Efforts for voluntary joint purchases of nuclear fuel failed in the past because some countries, particularly France, opposed it and insisted on limitations that made it unworkable.

Longer-term, the European Commission has outlined a plan to make Europe independent from Russian fossil fuels well before 2030, starting with gas. REPowerEU will seek to diversify gas supplies, accelerate the use of renewable gases and replace gas in heating and power generation, measures which could reduce EU demand for Russian gas by two thirds by the end of the year.

“We must become independent from Russian oil, coal and gas. We simply cannot rely on a supplier who explicitly threatens us. We need to act now to mitigate the impact of rising energy prices, diversify our gas supply for next winter and accelerate the clean energy transition. The quicker we switch to renewables and hydrogen, combined with more energy efficiency, the quicker we will be truly independent and master our energy system,”

– Ursula von der Leyen, President of the European Commission

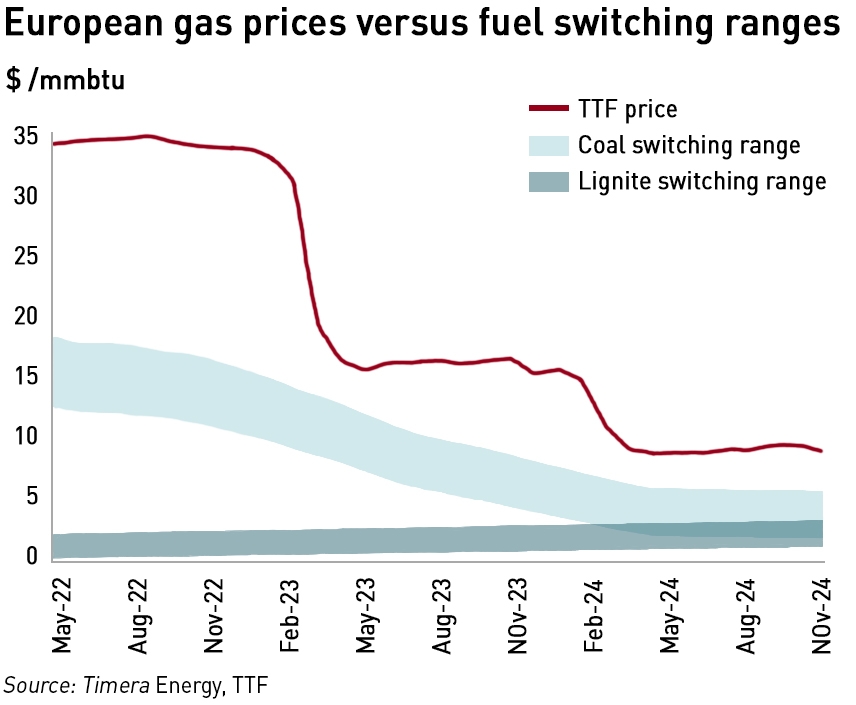

Unfortunately, as analysis from Timera Energy indicates, power sector switching within Europe, which is the main source of gas market flex, has already been fully activated with little scope for further switching. Coal plants are running at maximum output, with the TTF forward curve remaining well above coal and lignite switching ranges until at least 2024.

The Commission has also put in place measures to help Member States to mitigate the impact of high energy prices on vulnerable consumers, including allowing price regulation in “exceptional circumstances”. State Aid rules enable the provision of short-term support to companies affected by high energy prices, and to help reduce their exposure to energy price volatility in the medium to long term, and further adjustments to State Aid rules are under consideration in relation to the Emission Trading System and a Temporary Crisis Framework which would widen the scope for states to support companies affected by high energy prices.

Short-term emergency steps could also include a cut in excise duties and VAT on energy products, and/or creating a state electricity counterparty that would buy electricity in the wholesale markets and sell on to suppliers and utilities at discounted prices. Such measures would depend on the budgetary flexibility of individual states – Britain, which has the powers since leaving the EU to set its own VAT rates has opted not to provide VAT relief on energy products despite widespread calls for such a measure. Chancellor Rushi Sunak described this as an unjustified subsidy that would likely become permanent, ignoring the fact that energy is already subsidised since it attracts only a 5% rate compared with the standard VAT level in the UK of 20%.

Another option to reduce end-user prices would be the setting of a reference price for the wholesale market, or a cap on the wholesale price. This could apply to gas prices in order to avoid contagion into electricity markets, or to the electricity price. For example, electricity generators would be subsidised for the difference between their actual fuel costs and the cap level. Spain and Portugal are strongly supportive of wholesale price caps, however other countries including the Netherlands, Denmark, Germany, Estonia and Finland have warned against intervening in the wholesale market and oppose price limits. The EU requires unanimity to adopt these types of measures, and as Member States have widely varying sources of energy it would be difficult to formulate a policy that would work across the bloc.

The strange story of Gazprom

On 1 April, in what many originally took to be a bizarre April Fool’s joke, Gazprom PJSC announced it was “exiting” its subsidiary, Gazprom Germania. Gazprom Germania is the parent company of a number of European energy companies including Gazprom Marketing & Trading (and its retail subsidiary) in the UK, European gas supplier Wingas, and storage operator Astora. The following week Gazprom announced that its former subsidiaries would no longer be able to use its brand name and logo. In response, the German energy regulator, Bundesnetzagentur, has stepped in and taken over Gazprom Germania.

“I think this means Gazprom is drawing a curtain on being an active participant in the European gas market. Essentially it is going home because it no longer feels welcome…I think Gazprom understands it is going to face a hostile political and regulatory environment in Europe and therefore wants to consolidate and conduct all of its business in one place – St Petersburg, most likely with the political support of the Russian government,”

– Katja Yafimava, senior research fellow, Oxford Institute for Energy Studies

Gazprom Germania’s energy trading, gas storage and transmission businesses are now under the control of the German state, including the UK subsidiaries. All voting rights in the company have been moved to the Bundesnetzagentur (also known as BNetzA), which will be entitled to remove executives, hire new staff and ask management how to proceed, and a re-branding is planned. It has asked businesses to continue trading with the company to avoid a collapse of its operations. The regulator will retain control until the end of September but there are rumours that a buyer is being sought for the business. A source told Bloomberg that buyers would be offered guarantees and loans through the state-owned development lender KfW IPEX-Bank.

“The order of the trust administration serves to protect public security and order and to maintain the security of supply. This step is mandatory,”

– Robert Habeck , German Economy Minister

The Economy Ministry said the move was to avoid a possible acquisition of Gazprom Germania by JSC Palmary and Gazprom Export Business Services LLC, Russian companies with obscure ownership structures. Selling the business piecemeal might be difficult because the different parts of the group are intertwined – for example, Gazprom Marketing & Trading, holds the hedges not only for Gazprom Energy, but also Wingas. There had been reports that the British Government was considering appointing a Special Administrator to take over Gazprom Energy, which was at risk of collapse as customers fled, but this is probably no longer necessary (and may not even be possible) now that the German state has stepped in.

The German Government may also consider nationalising Rosneft’s business in the country if no private sector solution is found. Rosneft Deutschland accounts for roughly a quarter of the German oil refining business.

.

Attitudes towards Russia are hardening further as news of atrocities and crimes against humanity emerge from Ukraine on a daily basis. It is also clear that Russia is engaging in unexpected acts of self-harm both on an off the battlefield (the stories about the behaviour of Russian troops at Chernobyl for example), which makes it difficult to predict what may happen next. European governments and energy market participants are taking more or less the steps that could be expected under the circumstances – while they can certainly be criticised for allowing themselves to become so dependent on such a volatile trading partner, what matters now is how they manage the situation going forwards.

Gas prices will inevitably remain high for the foreseeable future, and while many may be tempted to see this as a sign that more renewables are needed and that heating should be electrified, care must be taken not to add further costs to the system due to the hidden costs of renewable generation. Rather than attempting to cap wholesale (or retail) prices, policy-makers should direct their efforts towards supporting end users, with measures to reduce energy waste, direct financial support and tax relief.

Longer term, we are likely to see a major shift in the approach taken by European governments including the UK, which is far less exposed to Russia than its EU counterparts, and this should extend across all areas of the economy, not just energy. We can anticipate a renewed desire to diversify sources of raw materials and even re-establish local manufacturing to avoid similar issues with other authoritarian or potentially aggressive regimes. Russia’s illegal war in Ukraine will have a major impact on the global economy and the way in which countries approach their trading relationships for many years to come.

It doesn’t look like Russia is that worried that it’s biggest customer is preparing to walk away. In fact, if Putin loves the cold-war so much maybe he will try and sever all ties between Russia and the West as a matter of principle. Maybe the UK & EU should prepare for a hostile Russia that wants zero-trade.

I think at this point trying to second guess Putin is futile, and the markets should prepare for all outcomes.

“Rather than attempting to cap wholesale (or retail) prices, policy-makers should direct their efforts towards supporting end users, with measures to reduce energy waste, direct financial support and tax relief.”

Any evidence new measures to reduce energy waste are actually happening?

Not sure what caused the markets to fall out of bed on Thursday just ahead of a holiday weekend, especially with NBP falling faster than TTF. I did see the Russians claiming that some companies had established rouble accounts, which I suppose is some prospect of continued supply, along with the new Gazprom Marketing arrangements. I monitor Baumgarten

https://transparency.entsog.eu/#/points/data?from=2022-03-31&points=sk-tso-0001itp-00168exit%2Cat-tso-0001itp-00062entry%2Cat-tso-0003itp-00037entry%2Cat-tso-0001itp-00162entry&to=2022-04-18&zoom=hour

Griefswald and Kondratki (on the Yamal line at the Belarus/Poland border) for signs of changes in flows. Some sligjtly lower flows via EUstream, and Yamal staying at around a quarter capacity, but Nordstream unaffected so far. Use the search bar at the link to see the others. Meanwhile Russian LNG continues to flow via direct shipment ex Sabetta, transshipment off Murmansk, and shipments from Vysotsk, where the regular vessels are less well known than the Arc7 LNG icebreakers, with Portugal, Spain, France, Belgium and the Netherlands all still receiving.

Spot prices for UK Gas dropped 22% last Thursday and are close to a 12mth low. LNG cargoes have been very heavy into UK over last month with the BBL & IUK gas interconnectors to Europe running at max throughput since start of month suggest UK is being used because its high quantity of LNG terminals. Also according to ENTSOG plenty of gas still coming from Russia currently and Norway to UK running at much increased levels since the start of the month.

Of course we are at end of prime heating season so spot prices would be expected to drop back so will be interesting to see how short term futures react now.