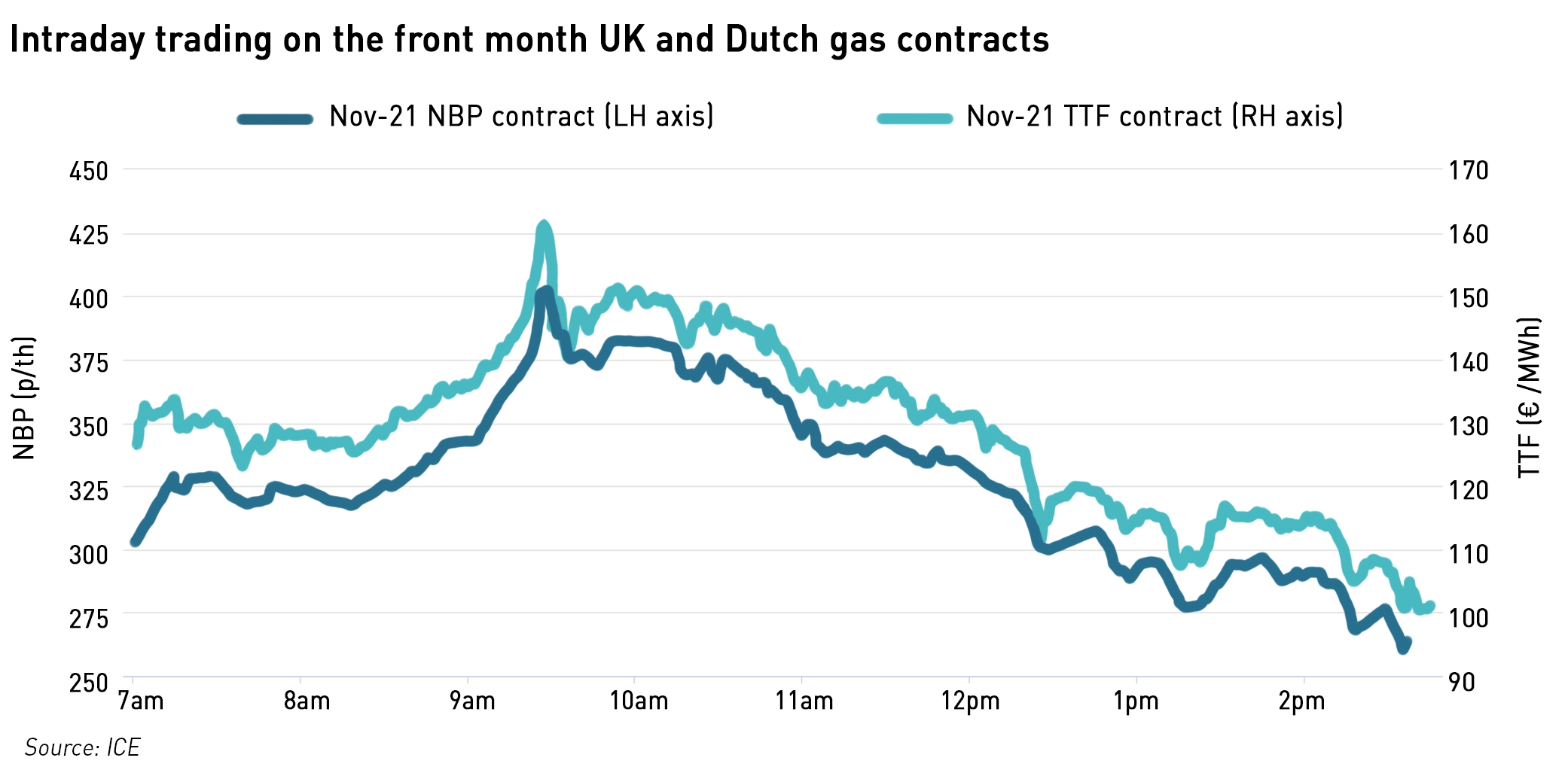

Gas markets were highly volatile today as prices went on a roller-coaster ride – front month NBP futures on ICE reached an unprecedented £4 /therm! Similar trends were seen in European markets with the key TTF benchmark exceeding €160 /MWh. This meant gas traded above US$ 200 /bbl oil equivalent which is almost three times the actual current price of crude oil.

If anyone hoped these prices might attract spot LNG cargoes to ease the supply constraints, the Asian JKM prices exceeded US$ 50 /mmBtu. The S&P Global Platts JKM for November was assessed US $16.655 /mmBtu higher at US$ 56.326 /mmBtu today which was both the largest single-day price rise and the highest level since Platts starting assessing the benchmark in 2009. Asian prices are in part responding to surging European prices with Asian buyers bidding at a premium to European hub prices in order to secure LNG cargoes.

“JKM is pricing even higher than TTF which is close to plus US$3 /mmBtu, as Asia needs to draw cargoes from Europe. But eventually you may get LNG sellers taking profits and the premium will disappear and could pressure prices,”

– Singapore-based trader quoted in S&P Global Platts

I haven’t found a good reason for the sudden jump in prices today. The fundamentals remain bullish for gas prices, and the speed with which prices are rising suggests the market has reached the limits of fuel switching and natural demand reduction, meaning that buyers have no choice other than to pay more to secure supplies.

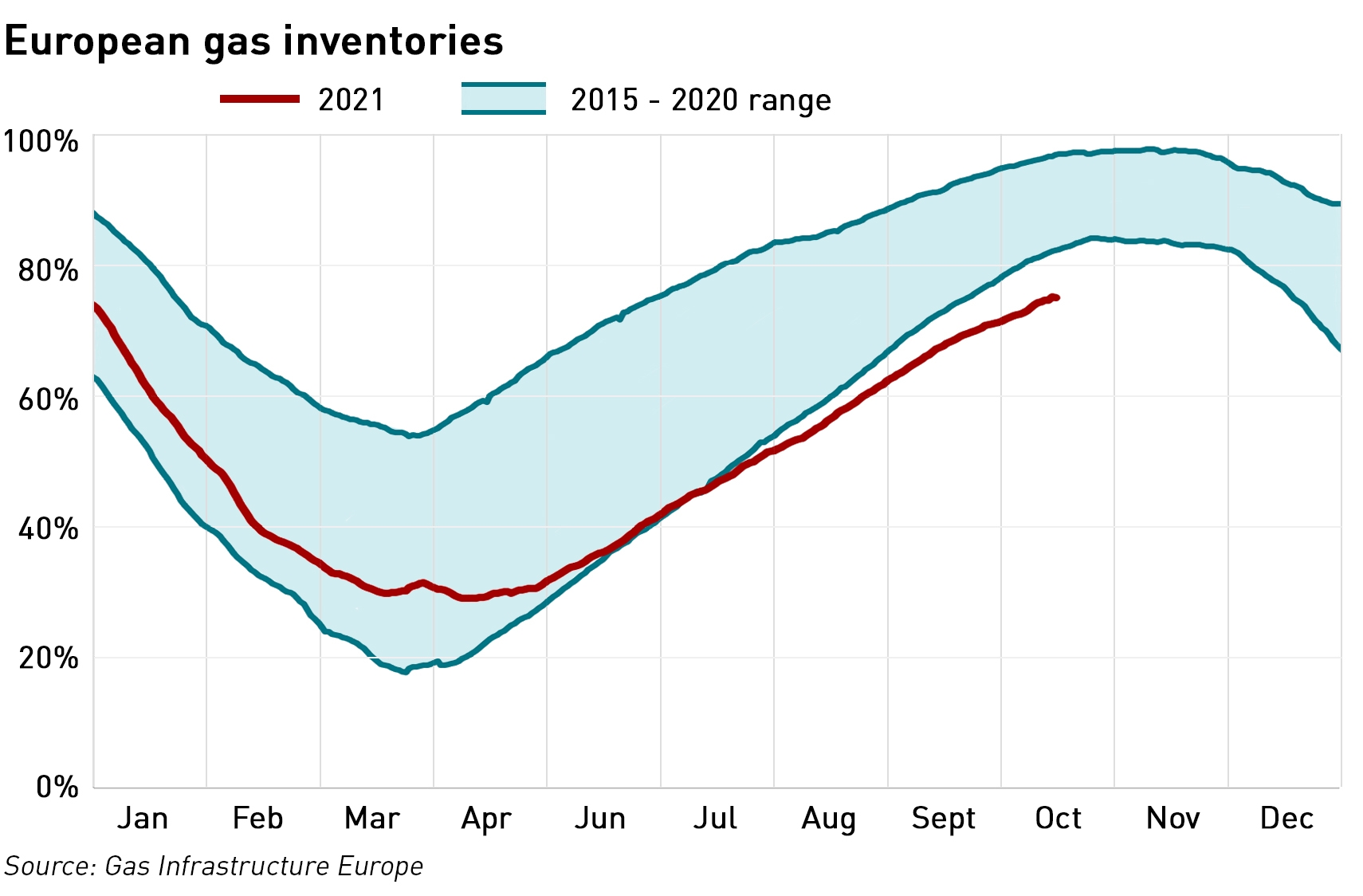

European inventories remain below seasonal norms, and the weather across northern Europe is forecast to turn colder next week, also heading below seasonal norms meaning a demand boost from heating, particularly in the UK where almost 80% of homes are heated by gas.

However, the reason prices retreated from today’s peak prices was the news that Russian gas flows may be set to increase. Despite describing the European energy situation as one of “hysteria and confusion”, Russian president Vladimir Putin has today suggested the country will increase exports to Europe. This includes sending more gas via Ukraine, something Russia has been avoiding in recent years.

Apparently there is some ambiguity in Putin’s remarks, but the markets appear to be pricing in increased Russian flows. He is reported as having asked his government and energy executives for proposals on how to stabilise the energy market, on “an absolutely commercial basis, taking into account the interests of all participants in this process.”

Putin described the trend in recent years of moving away from long-term oil-indexed pricing to hub-based pricing as a mistake:

“The practice of our European partners has confirmed it once more that they made mistakes. We talked to the European Commission’s previous lineup, and all its activity was aimed at phasing out of so-called long-term contracts. It was aimed at transition to spot gas trade. And as it turned out, it has become obvious today, that this practice is a mistake,”

– Vladimir Putin, President of Russia

Gazprom has historically resisted moving to spot trading in Europe preferring long-term contracts which can have tenors as long as 25 years.

Putin reiterated that Russia has been a reliable energy supplier to Europe, following on from comments from his spokesman, Dmitry Peskov, earlier who said that Russia has played no part in Europe’s surging gas prices. Peskov said Moscow was ready to discuss new long-term contracts for European consumers, but it is unlikely that there will be many takers for decades-long oil-indexed contracts when this creates a significant mis-match between the costs of gas and the price at which it is sold to European businesses and power generators.

Gazprom has been accused by the International Energy Agency and members of the European Parliament of not doing enough to increase its supplies to Europe, while there has been speculation that Russia has been using the situation to pressure the EU and German authorities to open the Nord Stream 2 pipeline.

.

Day-ahead electricity prices on N2EX jumped from £198.45 /MWh yesterday to £272.50 /MWh today reflecting the rise in gas prices. At the same time, nuclear availability is down with Hartlepool, Heysham 1 and one of the units at Hinkley Point B all off-line for un-planned maintenance. There are also two units off-line for planned maintenance (Heysham 2 reactor 8, and Torness reactor 1).

The cold weather forecast for next week could see significant volatility across both gas and electricity markets, particularly if combined with low nuclear availability. If the additional Russian gas fails to materialise, gas market volatility will again increase, and prices could head back to the levels seen this morning.

My guess would be that someone failed to meet their mark to market margin calls this morning – a producer or a short speculator/intermediary/hedge fund of reasonable size and maybe presence across both TTF and NBP. That would have given rise to a position liquidation order with enough size to tempt the vultures to bid up prices before taking advantage. Filled and killed, as they say. I’ve seen it several times over the years. Look for someone in financial stress.

Putin’s remarks came only late morning by which time prices had already subsided somewhat whereas the frenzy peaked shortly after 9 a.m.