In researching the new gas courses for my training programme, I discovered the etymology of the word “gas” – appropriately, it derives from the Greek word khaos meaning “chaos”. Sixteenth century Flemish scientist Joannes Baptista van Helmont, was interested in the process of combustion, and conducted an experiment in which he burned 28 kilograms of charcoal and found only half a kilogram of ash remained. He concluded that the rest of the matter had escaped into the air as “gas”.

This choice of word was surprisingly accurate, since the movement of molecules within gases can be considered to be mathematically chaotic, something which has long been believed to be true but only recently observed experimentally.

Molecular chaos is an assumption that the velocities of colliding particles such as molecules in a gas are uncorrelated and independent of position. An example this is the air in a room – while the nitrogen and oxygen molecules move with some average square speed because of the temperature in the room, they are not related, which is clear because the air does not spontaneously fly off in one direction without some sort of external pressure change, such as a window opening.

Of course most people are currently more concerned with the chaos in the gas markets and energy markets more broadly.

Gas market fundamentals take a turn for the worse

Global gas markets look to be tighter than previously thought following the recent news from China, where power outages and rationing have led the authorities to take additional measures to secure fuel supplies.

The origin of the latest squeeze is a shortage of coal in China, where domestic production has struggled to respond to the increased demand for electricity as its economy recovered after the pandemic. Output has been constrained due to tough new safety measures introduced after a series of deadly accidents. In addition to the new safety measures, Chinese authorities have capped the growth in coal mining as part of the country’s efforts to be carbon neutral by 2060.

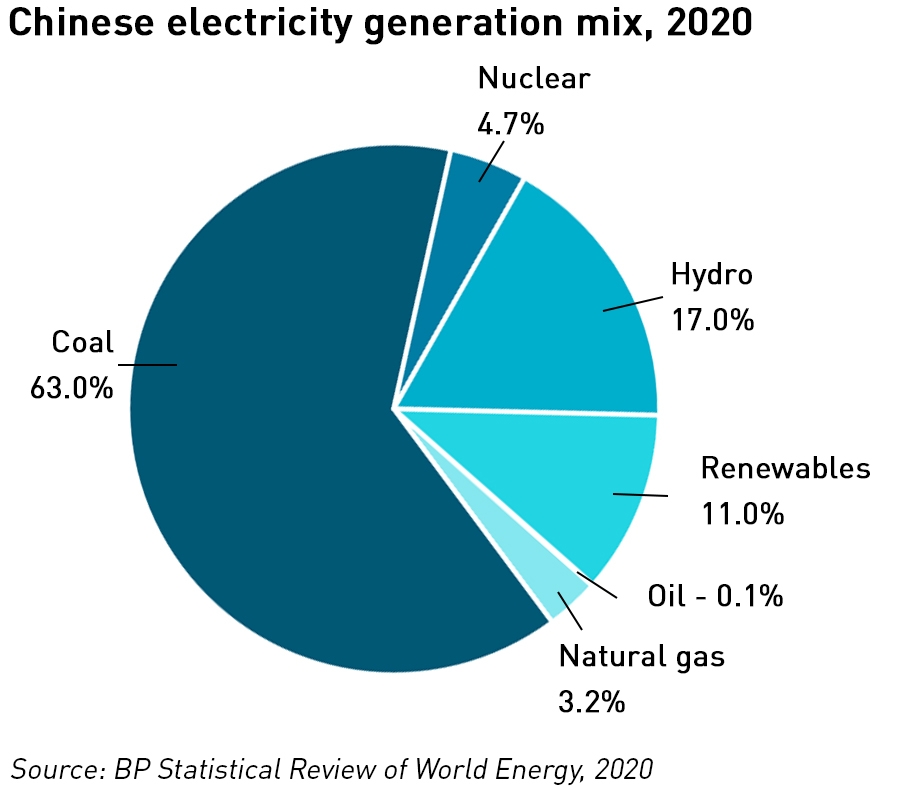

The Chinese economy relies on coal for 63% of its power, making the country to world’s largest coal consumer. Chinese demand for electricity has grown by 15% this year but coal output is only up by 5%. As a result power station coal inventories have fallen significantly as winter approaches. Average inventories across seven large eastern provinces were just 12.5 days last week according to data from CQcoal, the lowest since at least 2015 and less than half the average in Q4 2020. According to Argus Media, Chinese coal prices have risen to Rmb 1,700 /MT (US$ 263 /MT).

At the same time imports are being disrupted by heavy rains in Indonesia and China’s ongoing dispute with Australia, China having effectively banned Australian coal imports in late 2020 as relations deteriorated. While China has been able to replace most of these volumes from other sources, there is still a 10% deficit versus 2020 figures. China’s push to re-build its power station inventories has pushed up coal prices across Asia, and is diving up Asian LNG prices as coal-to-gas switching takes place.

Coal shortages have led to a power crunch with some regions now experiencing a second week of outages or power rationing, affecting both industrial and domestic consumers. As many as 20 provinces are believed to be experiencing shortages, with factories having to shut down operations or work reduced hours. Shopkeepers are reportedly lighting stores with candles, and mobile phone networks have suffered disruptions in three north-eastern provinces.

“China’s latest measures to cap energy consumption have been widely blamed for causing the current power crisis, but the curbs more likely ignited a tinderbox of issues accumulating for months around soaring fuel prices and coal shortages, highlighting the difficulties in implementing energy policy in the context of a huge economy with numerous moving parts,”

– S&P Global

To a certain extent the current energy crisis in China is a result of poor policy decisions – something that has been the case elsewhere including the UK. The National Development and Reform Commission (“NDRC”), China’s main economic planning agency, announced updated measures under its existing dual control policy on 16 September.

The new restrictions were intended to reduce energy intensive demand in anticipation of more severe fuel shortages and disruptions while efforts to improve supplies continue. However, the dual control policy is designed to improve China’s long-term energy efficiency and is not well suited to tackling short-term market disruptions.

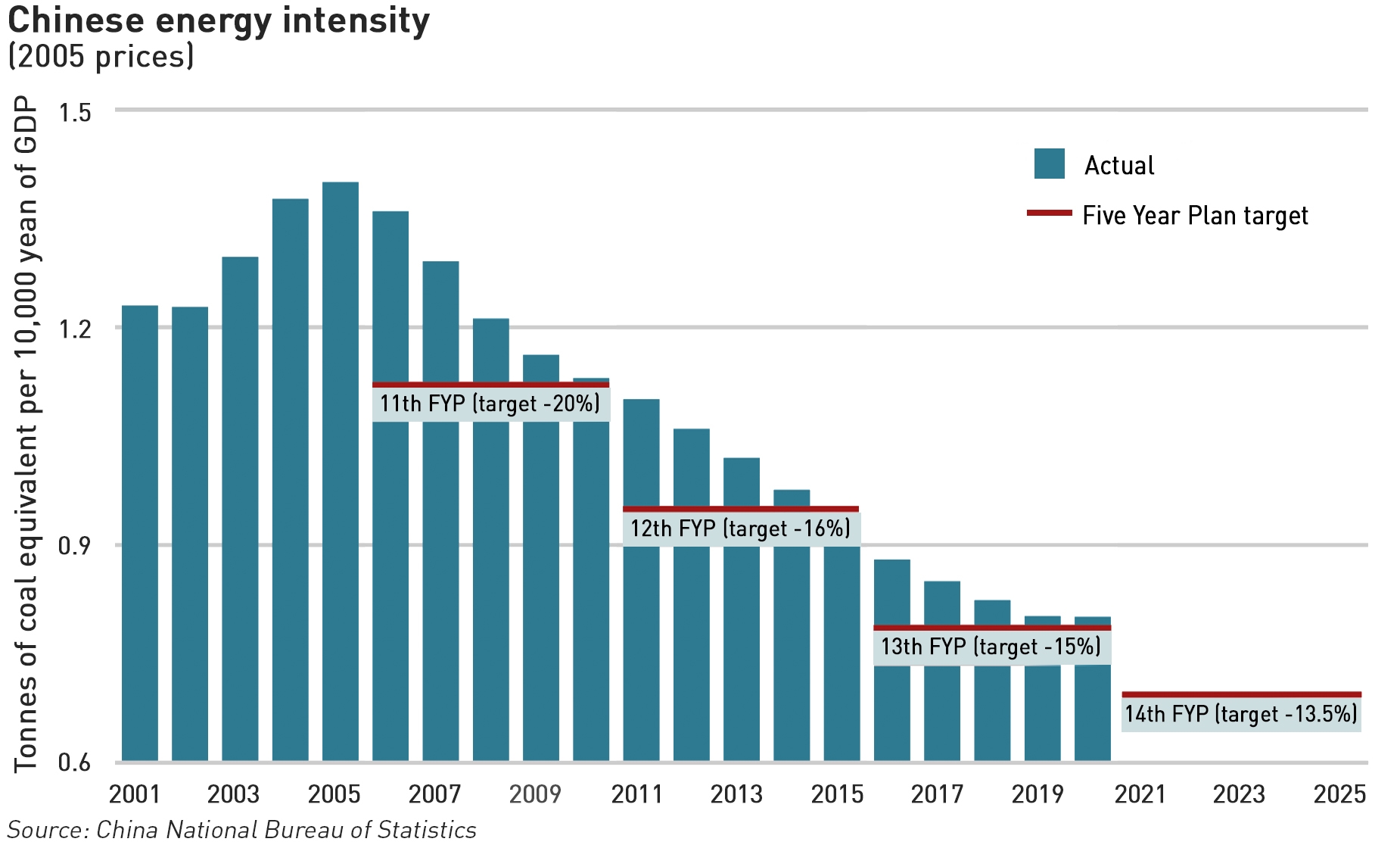

The dual control policy was implemented 15 years ago and seeks to curb both energy consumption and energy intensity – energy intensity being the amount of energy consumed for each unit of GDP growth. Between 2015-2020 China had a national target for a 15% reduction in energy intensity while the newest Five Year Plan approved in March targets a further 13.5% cut by 2025. In 2020, the consumption cap was met, but energy intensity was only reduced by 13.2%.

The measures introduced in September tighten the approvals and supervision of projects with an annual energy consumption above 50,000 MT of standard coal equivalent, halt financial support to unqualified energy-intensive projects and require authorities to tighten supervision and financing of projects with both high energy consumption and high emissions, including coal-fired power stations.

Many Chinese provinces struggled to achieve their targets under the previous Five Year Plan, leading the NDRC to issue “red alert” notices to 10 provinces requiring them to take corrective actions. As a result, many have cut power supplies to energy-intensive industries.

A further challenge has been due to the economic pressures on coal-fired power stations. Regulated power prices are below the true market price, so while thermal coal prices remain high, power generators have been reducing production in order to limit financial losses.

“China’s power rationing manifests the challenge of managing energy transition in developing countries. The outcome will have a significant impact on the global commodity market and even the global economy,”

– Dr Shi Xunpeng, principal research fellow at the Australia-China Relations Institute, University of Technology, Sydney

With power shortages now affecting the general population, the authorities are taking measures to secure energy supplies. Under the new arrangements, power generation and heating companies have signed new contracts with coal mines, with coal mines in good working condition being selected as key emergency suppliers. The NDRC has emphasised that energy supply to households will always be prioritised, noting that residential demand accounts for less than 20% of total consumption for electricity and 50% for gas.

The NDRC has said it will further boost domestic coal production, imports, and coal storage and has encouraged local governments and enterprises to increase storage capacity and emergency coal stockpiles. China has also increased domestic gas production and reserves, accelerated the construction of gas storage facilities and increased gas imports. Its efforts to secure those gas imports are helping to drive Asian LNG prices to record highs.

Gas prices still rising with no immediate relief in sight

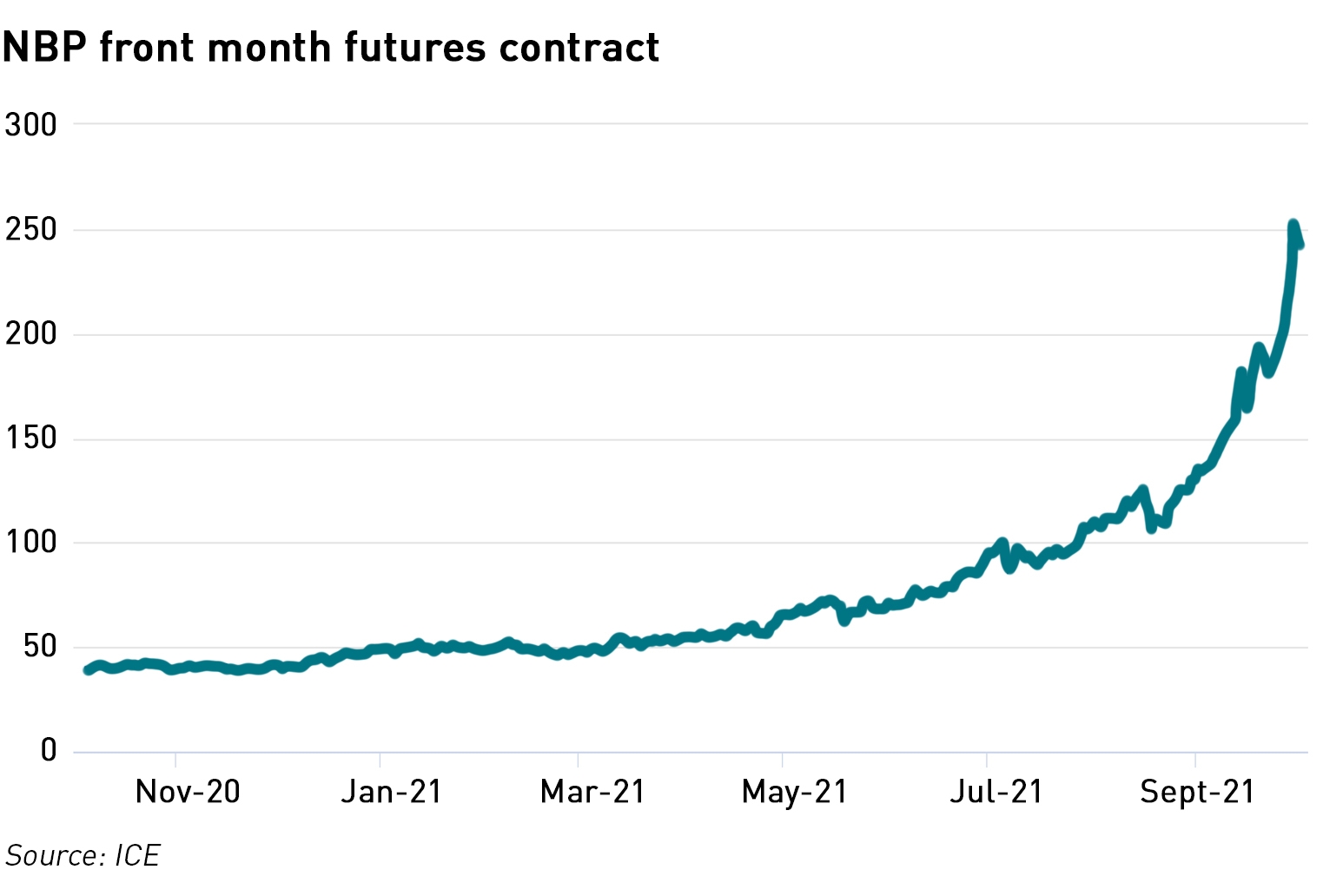

Gas prices continue to rise around the world: JKM prices are supported by strong Chinese demand, and prices in Europe are following suit. The NBP front month contract closed at 251 p/th on Thursday before declining slightly to 241 p/th on Friday.

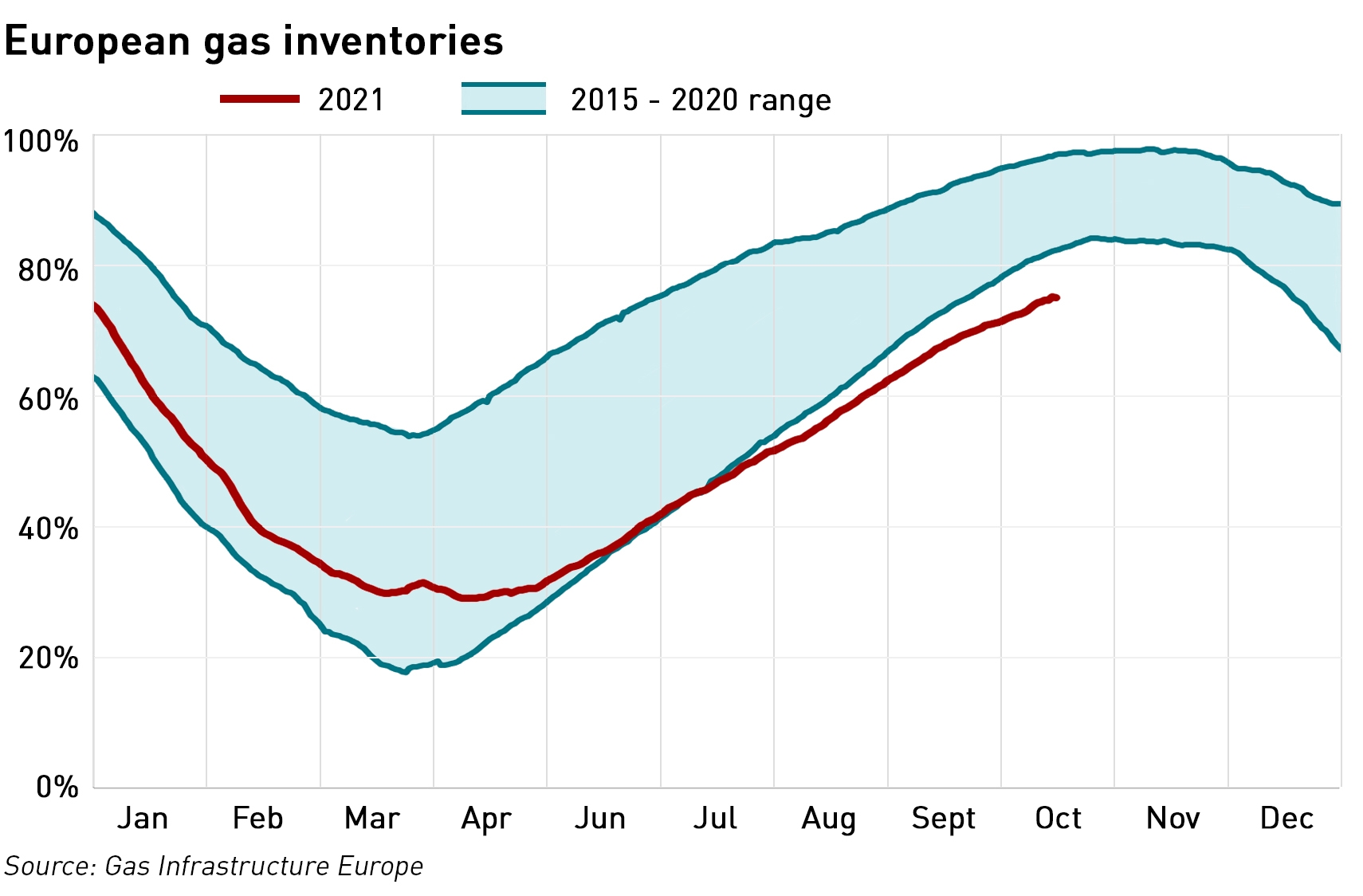

European gas storage facilities are continuing to fill but are still only 75% full compared with a range of 82% – 97% for the same time in 2015-2020. With high Asian demand drawing any spare LNG cargoes, and Russian gas flows still constrained, there are concerns that Europe may face shortages this winter. The Nord Stream 2 pipeline has the potential to deliver higher volumes of Russian gas into Europe, but the German regulators are yet to approve its use, and may take up to 4 months to make a decision

At these price levels, fuel switching will lead to some demand destruction, particularly in industrial segments and power generation where the cost of coal generation has fallen significantly below the cost of gas generation despite higher carbon costs. Although coal capacity in the UK is limited and is declining across Europe, it is likely that coal plant will see high utilisation this winter. In the UK, Drax has offered to delay the closure of its remaining coal units in response to the crisis.

“We forecast industrial gas demand destruction (especially fertilisers) and refineries switching from gas to liquids, as well as the final unprecedented source of flexibility which is gas-to-oil switching in the power sector,”

– Platts Analytics

With gas prices remaining strong, probably for the rest of the winter, and vulnerable to upward pressure in the event of cold weather, power prices will also remain high. A period of cold, still weather with low wind output will further stress a tight electricity market and see even higher price spikes. Gas really could be synonymous with “chaos” this winter.

The Chinese success in reducing energy intensity over 15 years is impressive even though they have not quite met the last target. Obviously, this reflects the growth in high-tech industries but it really should be a warning to western economies of the way things are going.