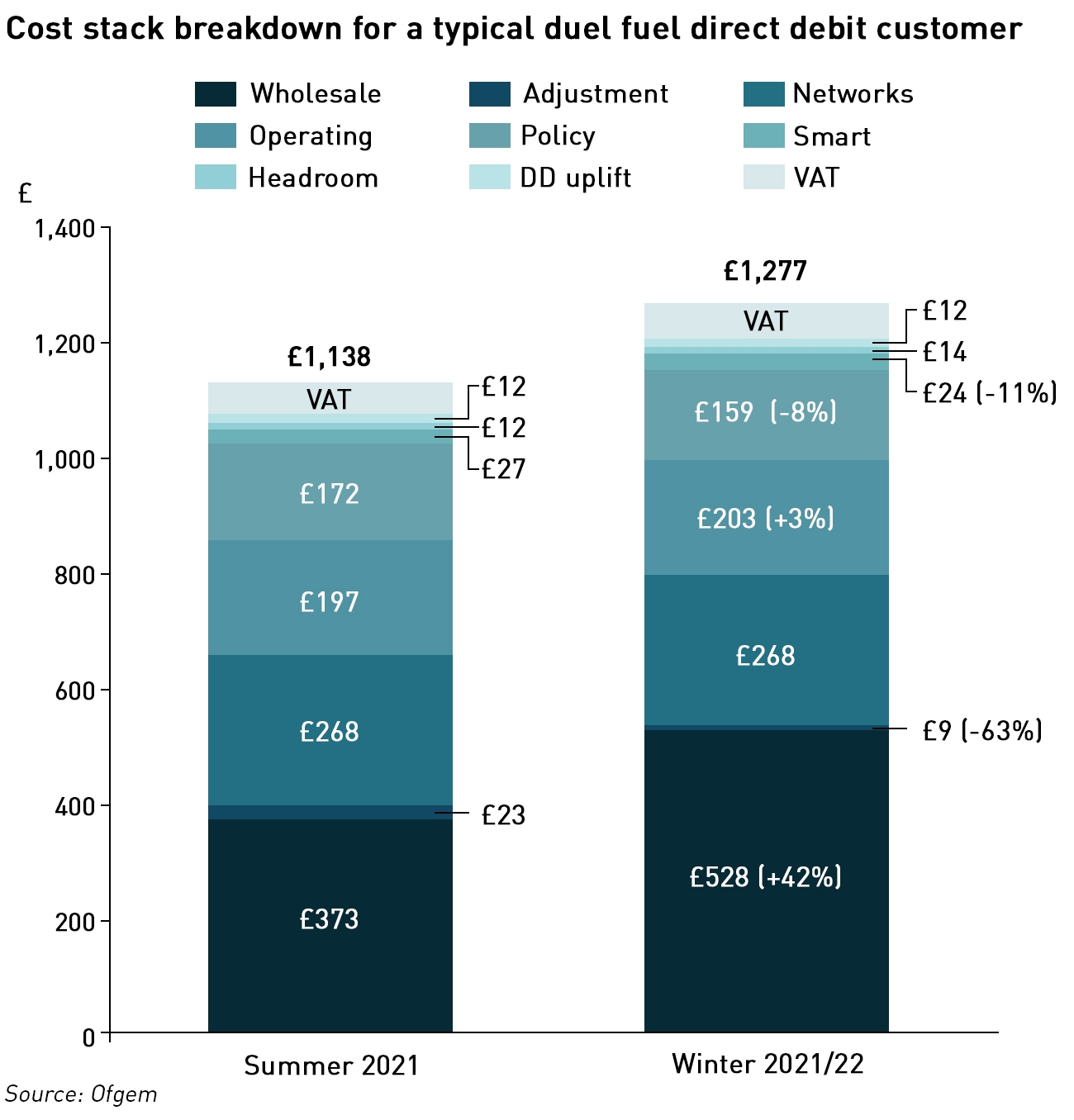

Last week Ofgem announced another increase to the price cap on so-called default energy tariffs, which will take effect from 1 October, the start of the winter season. This comes after a previous increase to the cap last February, and will be a blow to households struggling with the economic effects of covid and rising cost inflation. The cap level will increase by £139 from £1,138 to £1,277 a year for a dual fuel direct debit customer with typical usage. For pre-payment customers, the level will rise by £153 from £1,156 to £1,309. The change will affect around 15 million consumers.

“This is a devastating increase [to the cap]. Millions of household budgets are already stretched to the limit and this massive increase could not be coming at a worse time. As well as a significant rise in general inflation – driving up spending on other essentials such as food – the new cap level takes effect in October when millions of people will see a reduction in their incomes, as furlough winds down and the uplifts to Universal Credit are likely to be withdrawn. This toxic combination of higher prices, reduced incomes and leaky, inefficient housing, will lead to a further surge in utility debt and badly damage physical and mental health this winter,”

– Peter Smith, Director of Policy and Advocacy at fuel poverty charity National Energy Action

Why is the cap increasing?

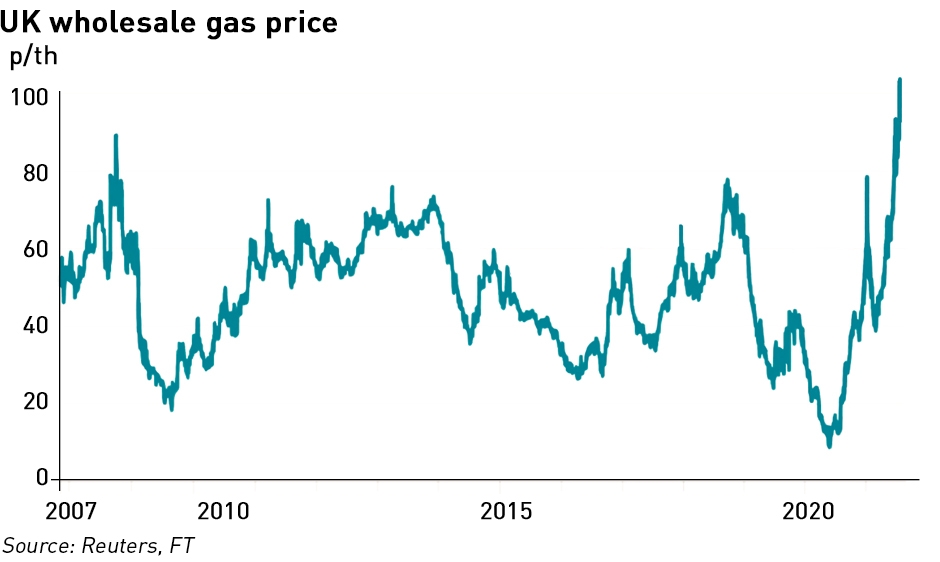

Since the previous adjustment to the cap level, wholesale gas and electricity prices which account for around 40% of the cap level have increased by over 50%. Gas prices have risen to record highs in Europe due to a recovery in global demand and tighter supplies with prices in the UK rising above 100p /therm, the highest level since 2005 and a record for the summer. European prices reached €40 /MWh for the first time.

“If anything, it’s surprising there hasn’t been more concern. In terms of additional supply, there aren’t many options on the table globally. Russia is really the only discretionary source of supplies out there but we don’t know when additional deliveries might start. So traders around the world, from Japan to Brazil, are starting to watch European prices too,”

– Tom Marzec-Manser, ICIS

Exports of Russian gas to Europe have been lower than usual, possibly to add political pressure to encourage EU approval of the opening of the controversial Nord Stream 2 pipeline. Norwegian production was relatively low in Q2 2021 due to major maintenance works while Dutch production is ramping down fast with the Groningen field on track to close by the middle of next year. Global supplies have also been constrained by increased demand – Brazilian LNG imports have reached record highs as droughts have reduced the output of its hydropower plants.

Extended periods of cold weather last winter depleted European gas storage levels, and UK domestic gas storage is minimal since the closure in 2017 of the Rough gas storage facility. European storage levels were low coming into the summer injection season. Cold weather in April saw aggregate storage inventories fall to around 30%, compared with 60% last year and a 5-year average of 40%.

Electricity prices are being driven by a combination of higher gas prices and increased carbon prices. Higher carbon prices directly impact coal to gas switching levels, boosting demand for gas and therefore pushing prices higher. May saw the price of EUAs exceed €50 /mt for the first time, and it’s not immediately clear why carbon prices have risen so sharply this year. From a fundamentals perspective, the need for high carbon prices to provide an economic driver for de-carbonisation is not new, but there seems to have been a shift in sentiment that is bringing new money into carbon trading, and it this new interest from hedge funds and institutional investors that is driving prices up.

Whether this trend is sustainable remains to be seen, but the pressures on gas prices are more likely to sustain higher power prices even if carbon prices fall back. Without a reduction in wholesale gas and power prices, the price cap is unlikely to be revised downwards.

“The price cap means suppliers only pass on legitimate costs of supplying energy and cannot charge more than the level of the price cap, although they can charge less…I appreciate this is extremely difficult news for many people, my commitment to customers is that Ofgem will continue to do everything we can to ensure they are protected this winter, especially those in vulnerable circumstances,”

– Jonathan Brearley, Ofgem Chief Executive

Rising energy prices damage both consumers and suppliers

In March the Government published its latest fuel poverty statistics, finding that in 2019 around 13.4% of households (3.18 million) were living in fuel poverty in England under the Low Income Low Energy Efficiency metric, down from 15.0% (3.52 million) the previous year. According to research by National Energy Action and the environmental group E3G on average 9,700 deaths each year are believed to be caused by living in cold homes.

Those figures are likely to be worse for winter 2020-21, when households faced the combined effects of covid lockdowns and prolonged cold weather. The impact of the pandemic was devastating for many households aside from the obvious health challenges, particularly for those having to shield, and low income households suffered a proportionally higher impact than more affluent households. People on low incomes were more likely to be in jobs which required them to continue working leading some commentators to suggest that there was no real lockdown, there were just middle-class people hiding at home while working-class people brought them stuff.

According to National Energy Action, low income households were hit particularly hard economically. The requirement to minimise travel meant people shopping more at small local shops which tend to be more expensive than large supermarkets, therefore spending a larger proportion of their incomes on food and having to reduce spending on energy. At the same time, normal coping strategies such as spending time in warm libraries and cafes were no longer available.

People living in fuel poverty also typically live in homes that are harder to heat with higher heat losses: in May last year, the Energy & Climate Intelligence Unit suggested that a second lockdown in winter would see families in cold, leaky homes facing average heating bills of £124 per month, compared with £76 per month for those in well-insulated homes.

Utility providers took steps to support vulnerable consumers who also faced problems with topping up prepayment cards, and credit terms for non-prepayment customers became more generous, with payment holidays and reductions in minimum direct debit payments. These measures were important, but also put pressure on already stressed supply businesses which in addition to the usual difficulties in the supply market, were also having to transition staff to working from home while continuing to provide appropriate levels of customer service.

In February, the Government’s Fuel Poverty Strategy set out the Government’s approach to tackling these issues with the following measures:

- Invest a further £60 million to retrofit social housing and £150 million in the Home Upgrade Grant

- Expand the Energy Company Obligation, a requirement for larger domestic energy suppliers to install heating, insulation in the homes of those on low incomes and other vulnerable consumers

- Invest in energy efficiency through the £2 billion Green Homes Grant, including up to £10,000 per low income household to install energy efficient and low-carbon heating in homes

- Extend the Warm Home Discount, a requirement for energy companies to provide a £140 rebate on the energy bill of low income households with high energy bills

- Drive over £10 billion of investment in energy efficiency through regulatory obligations in the Private Rented Sector and to drive improved energy efficiency through the Future Homes Standard and Decent Homes Standard

(Disappointingly, the document uses EPC ratings and energy efficiency interchangeably, which is incorrect since the EPC measures theoretical heating costs and not energy efficiency or heat losses. Homes can have a high EPC rating but still be expensive to heat, either because the flawed EPC methodology ignores problems with the condition of buildings, or because a more expensive form of heating is used.)

Several of these measures place extended obligations on energy suppliers that are already weighed down with multiple obligations that have little or nothing to do with the supply of energy. While those are primarily burdens on large suppliers, smaller suppliers face other challenges. Many struggle to access traded markets for hedging, and a desire to grow market share quickly often leads to them offering tariffs which are unsustainable. 22 suppliers have entered bankruptcy since 2018, often after failing to meet payment deadlines under the Renewables Obligation (“RO”).

“A massive train crash is about to happen because their models are unsustainable. Prices have gone through the roof and they can’t cope,”

– Keith Anderson, chief executive ScottishPower

Centrica’s chief executive Chris O’Shea said in July that he expected more suppliers to fail as a result of rising wholesale price increases, and that he believed some suppliers “must be trading whilst insolvent”, using customer deposits to meet other financial obligations, including the RO. With suppliers having until the end of this month to make this year’s payments into the RO buyout fund, the next few weeks could expose further weakness within the sector.

Change is overdue

After years of prioritising competition in the market, Ofgem eventually began to act to reduce the chances of supplier failure by raising barriers to entry. This was necessary since in the energy market, some costs of failure are socialised through the Supplier of Last Resort (“SOLR”) mechanism – because consumers cannot be left without gas or electricity when their supplier fails, Ofgem appoints another supplier, known as the SOLR, to take over their accounts.

Where consumers had credit balances that have to be honoured by the SOLR, Ofgem allows these to be recovered from the market as a whole (otherwise no supplier would ever agree to step in), and ultimately these are added to the bills of all consumers. When most businesses fail, the shareholders bear the financial consequences, but in energy markets, some of those costs are borne by other suppliers who pass them on to their customers.

Ofgem is considering further protections, such as ringfencing customer deposits, and there have been suggestions that the RO should be amended so that suppliers pay in to the buyout fund monthly rather than annually to reduce the likelihood of defaults.

These would be a step in the right direction, but do not address the structural problems facing suppliers. The market is failing for a number of reasons. Firstly energy supply is a low margin, commoditised business which makes it very difficult for suppliers to differentiate themselves. Secondly, suppliers are expected by the Government to do far more than simply supply electricity: they must collect taxes, install network equipment (smart meters) and pay for home improvements. This makes business models un-necessarily complex.

Thirdly, as a result of Government policy, suppliers have relatively little control over their cost bases which makes differentiation even more difficult. And finally, the Government (and its predecessors) has deliberately obscured the costs of environmental targets, preferring to pursue a narrative that suppliers are greedy and profiteering. This undermines public trust in the industry.

The price cap was born of this mis-trust. In 2013, the Leader of the Opposition, Ed Miliband, proposed a 17-month energy price freeze, which was dismissed by the Conservative Government as Marxist and a gimmick. Yet in 2017 the Conservative election manifesto promised an energy tariff cap which was introduced in 2019 with the intention that it should continue until 2023 at the latest, however the Government is now considering extending it beyond that date.

But as Stephen Littlechild, former Director General of Electricity Supply and now a Fellow of the Judge Business School told the Telegraph this week (and as I have been arguing since 2017), the CMA assertion that suppliers were making £1.4 billion of excess profits which motivated the introduction of the price cap was incorrect.

“The CMA calculation was quite simply a mistake. The CMA compared actual costs against “a hypothetical construct” that was essentially “an idealised perfectly competitive market” with unrealistic costs. This was inconsistent with conventional economic analysis, with previous competition authority practice, and with the CMA’s own guidelines. So there is not, and never was, a detriment of £1.4bn to £2bn a year. Consequently, the tariff cap is simply a mistake. Rather than looking to extend it, the Government should be looking to remove it,”

– Stephen Littlechild

My analysis was to simply add up the profits made by the Big 6 suppliers in their retail energy businesses, and found that in 2016 the total was just over £1 billion, and in the period 2013-2016 it never exceeded £1.1 billion in any year.

Now BEIS, in its on-going concern that too few consumers switch supplier and are therefore subject to “loyalty penalties” are proposing opt-in and opt-out switching where consumers could be automatically switched to other suppliers. Yet, as Littlechild points out, these proposals are fraught with problems around data protection and the risk of being transferred to a supplier with poor customer service or low financial stability. The approach seems overly complex when other approaches are taken in other markets. In insurance the Government is making it illegal for insurers to offer higher prices to consumers renewing their products than for new customers – a similar approach could be take in energy markets.

In fact only by switching with great regularity can any value to captured by consumers and most find it to be not worth the administrative inconvenience, particularly when billing errors can and do arise on switching. Switching also assumes there is no value to building long-term relationships between suppliers and their customers, something which would clearly be of benefit when asking suppliers to engage with consumers on installation of smart meters and energy efficiency measures.

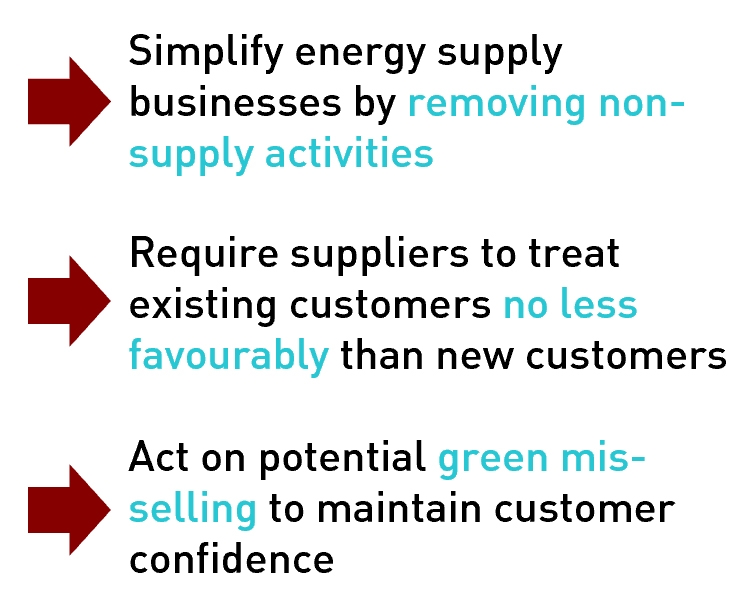

The price cap creates more problems than it solves. If the Government really wanted to make the market work better for consumers, it would simplify the role of suppliers – recovery of environmental subsidies through general taxation rather than energy bills would be a good place to start, and other non-supply related activities should be removed from suppliers and made the responsibility of other organisations or Government agencies. Simplifying supply businesses will reduce costs and improve customer service.

To protect consumers from the “loyalty penalty”, the Government should legislate to require suppliers to offer existing customers tariffs that are no worse than those offered to new customers. There is no reason that a consumer should not be placed on a new fixed tariff once a previous fixed price deal expires for example – this could become the new industry standard rather than defaulting to a variable tariff.

To protect consumers from the “loyalty penalty”, the Government should legislate to require suppliers to offer existing customers tariffs that are no worse than those offered to new customers. There is no reason that a consumer should not be placed on a new fixed tariff once a previous fixed price deal expires for example – this could become the new industry standard rather than defaulting to a variable tariff.

And action should be taken to avoid the mis-selling of green tariffs which mis-lead consumers into believing they are receiving 100% renewable energy, when this is a technical impossibility (such tariffs being backed by the purchase of green certificates based on annual volumes despite the fact that the actual electricity delivered to consumers has the carbon intensity of the electricity system as a whole at each point in time – on days where there is little wind generation, consumers may well receive electricity generated by coal-fired power stations but few consumers understand that this is the case).

Removal of the non-supply related costs from bills, acting to require suppliers to treat existing customers no less well than new customers, and reducing the risk of mis-selling would all be of significantly more benefit to consumers than the ever-increasing price cap.

I agree with your three reforms to the supply market, especially with regard to funding environmental activities via general taxation . Currently electricity bills are a form of regressive taxation where those on lower incomes with the least energy efficient houses (who are less likely to engage with switching supplier so are on the default tariffs) are paying proportionately more towards environmental measures than more engaged wealthier customers whose homes are more energy efficient. Unfortunately this has suited successive governments who dont have to raise taxes to fund these measures and (as you note) can paint the suppliers as greedy profiteers.

It also would have been sensible to have network companies provide the smart meters as most other European countries have done, as the roll out of these in the UK has been slow, overbudget and a mess of conflicting technological standards. Sadly that ship has sailed, but a good argument for taking these kind of non-supply activities away from supply businesses in future.

I’m hopeful that the tax issue will be resolved soon since the Government is starting to recognise the difficulty of persuading to switch from gas to electric heating when electricity is so much more expensive…

The metaphorical ink was barely dry on this post when Ofgem announced that another supplier, the third this year, has ceased trading with a SOLR appointed. Lancashire-based Hub Energy served about 15,000 customers, and now joins Green Network Energy and Simplicity Energy which both closed in January. The news comes just days after Ofgem sent an open letter to suppliers reminding them of the need to maintain financial stability

https://www.ofgem.gov.uk/sites/default/files/2021-08/Open%20letter%20-%20Retail%20financial%20stability.pdf