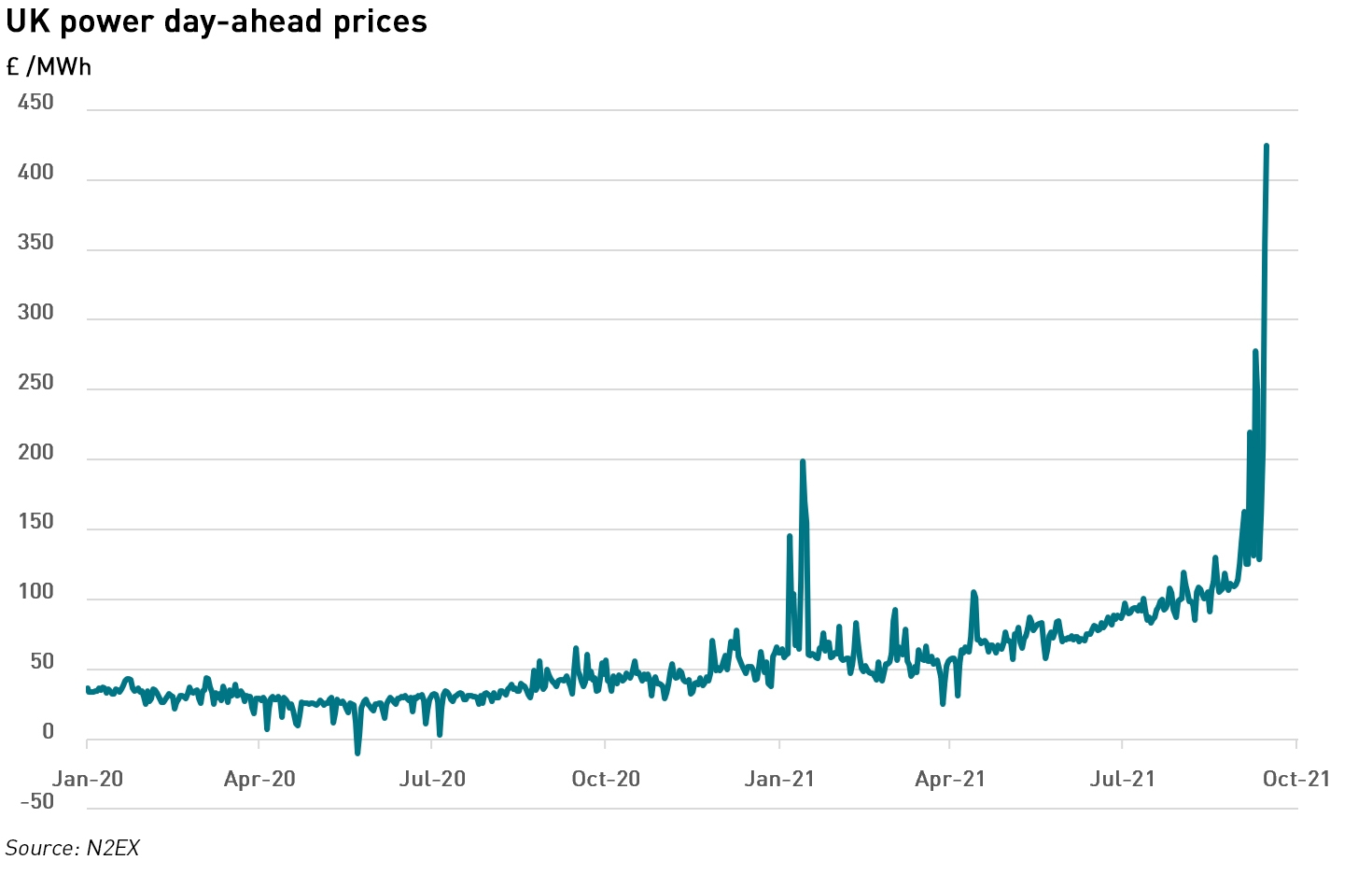

In the year and a half from the beginning of 2020 to July 2021 UK power day-ahead prices effectively doubled, and everyone from suppliers, three of whom have closed in recent weeks, and another two today: Utility Point and People’s Energy, to end consumers facing another increase in the retail price cap have felt the impact. But the past week has seen prices double again and with prices exceeding £400 /MWh.

The question is why is this happening and will these price levels be sustained? And what does this mean for the market?

Tight generation margins driven by low wind and unplanned outages

Power prices continue to be supported by high gas and carbon prices, and when combined with tight system margins due to low wind output and low interconnector availability, this puts significant pressure on prices.

While day-ahead prices on the N2EX exchange breached £400 /MWh, OTC prices have been even higher. According to S&P Global Platts, day-ahead baseload prices for delivery on 14 September reached £540.15 /MWh, up from £171.15 /MWh for 10 September. Platts Analytics is forecasting October baseload power prices to average around £122 /MWh, and expects market tightness to continue into Q1 2022, with average prices rising to £126 /MWh – more than double last year’s winter average of £55 /MWh. Intraday prices have been recorded a £1,750 /MWh on N2EX, and prices have become so volatile that EPEX doubled the price cap for UK intraday power prices to £6,000 /MWh.

At the same time imbalance prices have hit a record £4,037.80 /MWh with several generators bidding into the Balancing Mechanism at £4,000 /MWh on 9 September. Last week units at West Burton A were accepted into the Balancing Mechanism at £3,950/MWh, while Uniper’s Grain 6 combined-heat-and-power plant was accepted at £4,950/MWh. Even this evening, West Burton was accepted at £4,000 /MWh.

“Power prices are being driven by high gas prices but when prices start to get really, really high, it’s being driven by scarcity, rather than just the underlying cost of production. When we have scarcity events and wholesale prices spike, the cost is going to go up for consumers,”

– Marlon Dey, research lead for Great Britain at Aurora Energy Research

UK month ahead gas prices have increased from 28 p/th a year ago to 145p /th on 10 September, with NBP futures rising above 150 p /th for the first time ever. Gas prices continue to be supported by low storage levels across Europe, competition with Asia for LNG cargoes, and concerns over supplies from Russia. Although coal prices are also rising (from US$ 140 /MT in late July to US$ 170 /MT in September), gas-to-coal switching is a possibility with generation economics from coal improving significantly. This is despite all-time highs on the (admittedly still new) UK ETS of £54.05 /tCO2.

“There’s a lot of nervousness in the market. It’s been a long time since Europe has entered a winter with such little gas in store,”

– Thomas Douglas, ICIS

The UK’s domestic gas production has been significantly lower this year due to a heavy schedule of planned maintenance and delays to new projects such as Tolmount which was expected to come onstream in July and is now delayed until the end of the year after faults with off-shore electrical systems were found during final commissioning and testing. UKCS production year-to-date is down by 5.7 Bcm from the 25.9 Bcm produced in the same period last year.

The UK has also seen a drop in LNG imports as higher JKM prices attracted cargoes into the Asian markets – with imports of 10.4 Bcm YTD, 4 Bcm lower than last year.

In the electricity market, five nuclear units are currently offline, four for un-planned outages, removing about 3 GW of available generation and there is a partial outage on the 2 GW IFA interconnector with France reducing capacity by 1 GW until 17 September. CCGT availability has been low since the beginning of the month aside from the on-going absence of the two 850 MW Calon units, although plant has steadily come back on line in recent days, and there have also been unplanned outages at coal and biomass units.

“It’s very unusual for this time of year. This is the sort of thing we start to see when we get cold snaps. The worrying thing is that this is happening now, in September. We’re approaching a winter with not too much margin for error,”

– Murray Douglas, head of European gas research at Wood Mackenzie

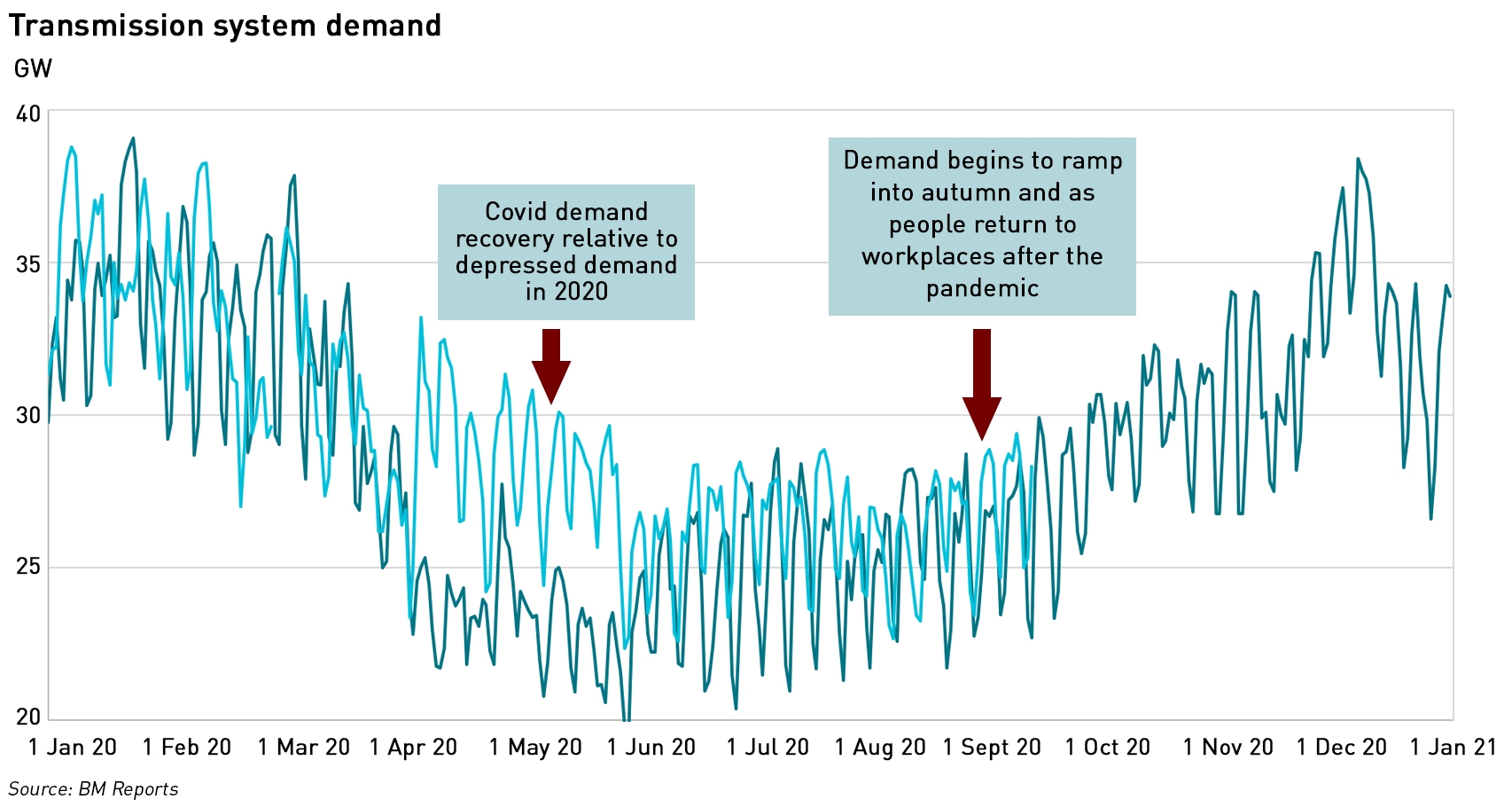

Demand began to rise again at the start of September as the holiday period came to an end, and people started returning to workplaces after the pandemic.

It’s time for the Government to act

With three suppliers having exited the market in the past few weeks, and a further two announcing their closure today, there are expectations that more will follow, particularly next month with the late payments deadline for the Renewables Obligations, an annual stressor for suppliers paying in to the buyout fund.

The problem all suppliers are facing, although it affects smaller suppliers more with their reduced access to hedging, is that the retail price cap is only re-set twice a year. With prices rising as rapidly as they are, suppliers will be forced to sell at a loss, which will inevitably push more of them out of business.

Suppliers can offer fixed price deals that are above the level of the price cap, and indeed, this is currently happening, but for suppliers that are unable to hedge in the markets, fixed price deals represent a risk. However, against a backdrop of capped variable tariffs, the smart play might be to try to move customers onto expensive fixed price deals in the hope that they switch to another supplier – shrinking may be the best survival strategy this winter.

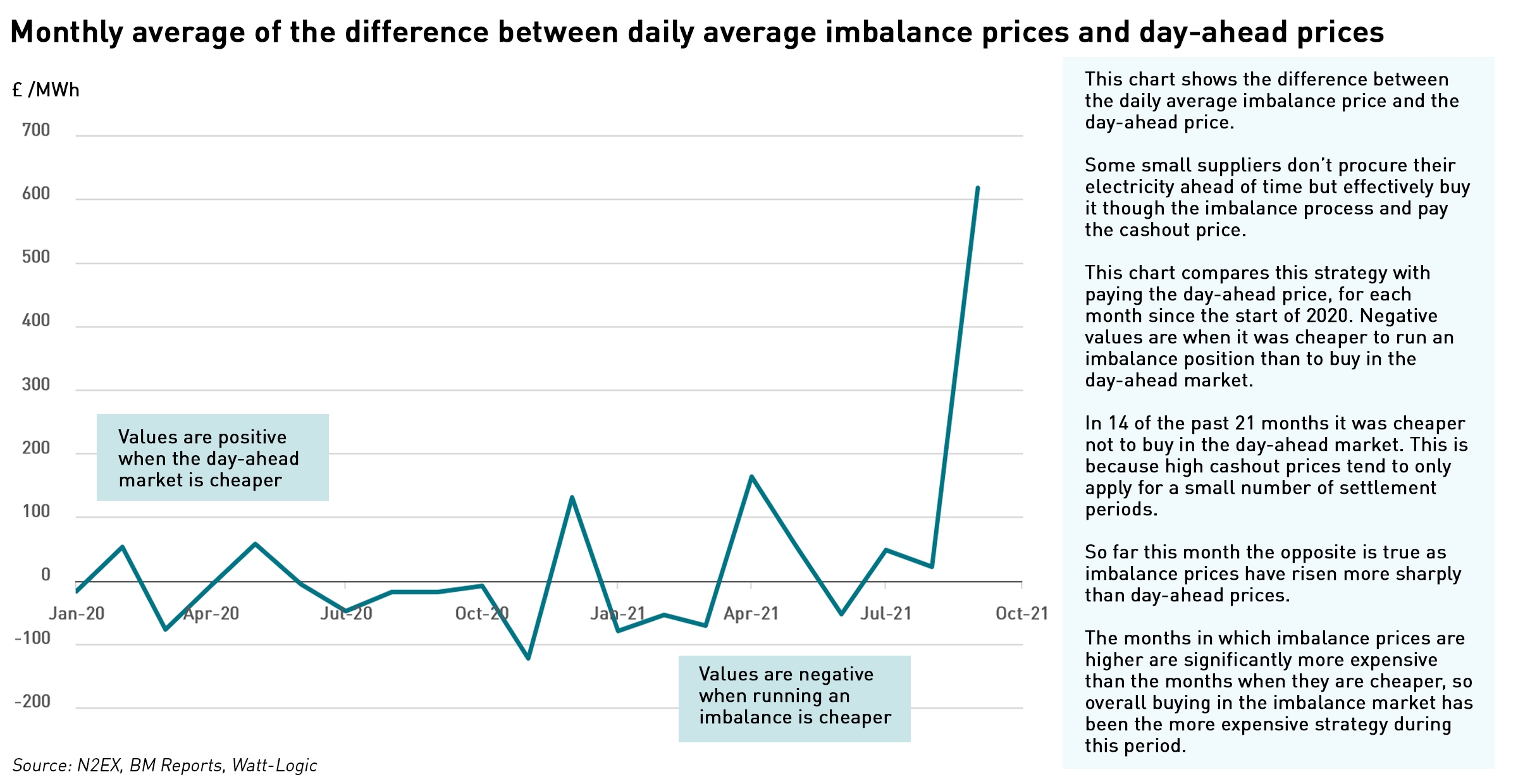

Access to hedging has long been a problem for smaller suppliers due to a combination of onerous credit requirements and difficulty in trading the small sizes needed to manage shape risk. Due to the difficulty in managing shape risk, as well as the additional systems and back office operations involved in market trading, some small suppliers opt not to have an active procurement strategy and instead simply run imbalance positions and pay the cashout price for the electricity that they deliver to their customers.

Although imbalance prices can rise rapidly, the typically only remain high for a few settlement periods, so the risk is considered acceptable, and the majority of the time, this approach is cheaper than buying in the wholesale markets. However, as the analysis below shows, in periods of market tightness and high price volatility, this approach become much more expensive than buying in the day-ahead market, more than overwhelming the savings made the rest of the time.

“In no other sector is the government forcing a loss on the supplier. The cap is fixed like some kind of tablet in stone from God; the market doesn’t work like that. Whether it’s quarterly or monthly; it needs to be calculated more frequently,”

– Steven Day, co-founder of Pure Planet

This makes life even harder for small suppliers – if they lack the resources to buy in the day-ahead markets and are forced to pay the cashout price things can get very expensive very quickly. The existence of the price cap, and the low frequency with which the cap is revised, exposes them to the risk that they will be unable to pass these costs through to consumers.

According to former Ofgem CEO, Dermot Nolan, consideration was given to re-evaluating the price cap every two or three months but the idea was deemed inappropriate. This decision needs to be re-visited as a matter of urgency, and the case for abandoning the cap altogether is growing. The fact of low energy margins is now being widely reported in the press – if consumers can be persuaded that suppliers are not profiteering at their expense and that they face genuine challenges, they may be prepared to accept the withdrawal of the cap.

“There’s certainly a case for moving to every four or two months now. It would probably avoid distortions, but the question is would consumers tolerate prices changing every month,”

– Dermot Nolan, director at Fingleton, former Ofgem CEO

Removing the price cap would remove a major source of risk for suppliers in the short term, and although there are arguments that market entry should be made harder by requiring suppliers to be more financially resilient, even the best resourced firms will struggle in these markets. However, in the short term, large numbers of supplier failures will create chaos, and Ofgem may find it difficult to find suppliers willing to take on SOLR responsibilities, particularly when compensation for honouring customer credit balances can take a long time to materialise.

The other issue is that against the backdrop of higher taxes to fund the NHS and social care, these energy price rises could not come at a worse time. Life is about to get very expensive for consumers, pushing more of them into fuel poverty. The chances of making meaningful progress on net-zero ambitions that require investment from consumers will fall as those investments become less affordable.

While there is no magic cure for rising global gas prices, there are things the Government can do to address the risks the market faces:

- Reform the retail energy market to remove non-supply obligations from suppliers

- Act on greenwashing to restore confidence in the sector

- Abolish the price cap, which creates un-necessary pressures for suppliers

- Take meaningful action on the growing capacity deficit

On this last point, the closure of the remaining coal plant in the next few years, and the likely earlier than expected closures of the aging nuclear fleet are all likely to happen before Hinkley Point C opens. If the Government wishes to nip these damaging price trends in the bud it needs to act on the growing capacity deficit in periods of low wind generation.

Approving Wylfa Newydd should be an easy choice, and consideration should be given to allowing the remaining coal plant to remain open at least until Hinkley Point C is able to open. This would be very controversial, but could be justified on the basis that when the Government decided they should close there was an expectation that the AGR fleet would remain open until new nuclear came online. As this is now looking less likely, something has to give.

The alternative is a renewed focus on gas, but this is hampered by the fact that since the closure of Rough in 2017, the UK has not had a large-scale seasonal gas storage facility. Developing a new facility of that size in the time available would be expensive, and relies on suitable sites being available. Keeping the last remaining coal plant open for a few extra years would be a cheaper and more reliable option, and a special reserve product could be developed to ensure it only ran when absolutely necessary to mitigate the political risk of the decision.

In the end, the three prongs of the trilemma are not equal. Security of supply is the most important part of the equation – in the end, people will be willing to pay higher prices if the alternative is supply disruptions, but only if other options have been exhausted. At some point high prices will become politically untenable, at which point all bets will be off on net zero. It’s time to restore balance to the market in more ways than one.

Lots of good points well argued about the current situation in both the generation side and supply side in the GB market. Two areas I would disagree on – approving a new nuclear plant at Wylfa is not going to solve anything with regard to supply issues in the short or medium term as if approved now it would not be operational for at least 10 years. If the government wants to intervene on the supply side now it needs to do something to get the 2.3GW of gas plant owned by Calon that has been sitting idle since they went bankrupt back into active use. Also extending coal plant lifespan will be very controversial, approving new gas plant would get more capacity in play in c.5 years as some plans are quite well advanced (oven ready as some would put it). Perhaps some sort of CFD for these new plants? Also getting rid of the cap completely would be politically difficult as on current wholesale price trajectory prices would shoot up this Winter and customers are not going to wear that at all when other prices are rising. By all means review it more often to help suppliers even out their revenue stream, but ditching it when prices are rising so fast seems incredibly difficult politically.

I completely agree that Wylfa won’t address the short-term supply problem, but unless we get some large dispatchable generation into the pipeline, this short-term problem will turn into a long-term problem.

Also agree on Calon – this is a no-brainer. The problem with CCGTs is gas storage – electricity prices are being pushed up because the gas markets are super tight. Partly this is due to geoppolitics with Russia, but with no domestic seasonal storage any more we rely on European storage which is currently much less full than it usually would be going in to the winter. I can’t see the Government wanting to invest in new gas storage now, so keeping coal open a bit longer would be a safer bet.

Yes, it would be controversial, but the earlier-than-expected closures of the nuclear fleet (and their reliability problems in the meantime) mean things have chnaged since that decision was made. Abandoning the cap would also be difficult, but the Government should grant emergency powers to Ofgem to either suspend it or raise it more often (and Ofgem could effectively suspend it by temporarily making it very high). More failures are coming, and Ofgem is going to find it increasingly difficult to find people willing to act as a SOLR. The utlimate consequences of not revising the cap would be bail-outs which is exactly what happened in California when they capped retail prices…

Our gas “storage” is LNG tankers coming for discharge, and extra pumping from Norwegian fields (I doubt we have much capability for that left in the UK sector, although it used to be substantial). We import very little gas over the interconnectors these days, especially now the Netherlands has largely shut Groningen creating a local shortage in place of surplus.

https://datawrapper.dwcdn.net/W0qOT/2/

Perversely, in recent days we have seen simultaneous drawdown from our limited ~16 TWh of storage (plus up to about 9TWh in LNG terminal tankage) and export to Zeebrugge, Belgium. I guess the Germans are getting nervous about Nordstream2 volumes proving insufficient. Storage in Europe is a long way behind where it should be. This time last year it was at 1,050TWh, compared with not yet 800TWh now.

That’s right. I hadn’t realised though that production at Ormen Lange has dropped significantly and the field is well past its peak (https://www.norskpetroleum.no/en/facts/field/ormen-lange/).

Troll production is still strong though (https://www.norskpetroleum.no/en/facts/field/troll/)

I don’t think Norwegrian swing production should be the strategy though. There’s political pressure in Norway to halt exploration on the NCS which might make them reluctant to increase exports.

Interestingly, Centrica is considering bringing Rough back into use for hydrogen with a £1.6 billion investment, but wants Government backing (https://www.business-live.co.uk/economic-development/rough-return-16b-plan-britains-20984442). If they got the money/guarantees then I wonder if it could be used for both – obviously not at the same time, but I’d be interested to know if it was technically possible. If so it could be a good option…

We have long term agreements o Norwegian supply. What they choose to do by way of further development is of course a matter for them. Meanwhile I took a look at what is going on at Statnett given our new interconnector to Norway which seems to have been pressed into action in topping up our supplies. Norway has been exporting almost 4GW in recent days, and the effect on its already lower than normal hydro reservoirs levels is noticeable. They are in effect gambling on being able to slow drawdown when it gets windy over the winter by importing from the UK and Germany and Denmark.. If they are not careful they could end up sharing the Europe wide energy shortage, and despite the agreement we just signed that supposedly gives us the right to demand imports, we could be severely disappointed by reality.

Reports suggest that part of the reason for Rough closure was increasing problems with leaks. If the reservoir is compromised, filling it with hydrogen is not the right answer – and it will in any case take a long time before there is enough production capacity to fill it. I see they are considering using CO2 as cushion gas. An interesting choice given the phase diagram at 100bar or so…

Well, I agree on that – if there were issues with methane leaks then with the smaller hydrogen molecules those issues would be worse. I’m interested to know if a depleted field that had been repurposed for hydrogen could be then used to store methane instead for some period of time. This might be a neat way for the Government to square the circle of investing in methane infrastructure while also trying to get people to stop using methane. Clearly that requires the reservoir to be suitable in the first place…

Your posts are always informative – thank you – and I never cease to be amazed at the way energy markets operate and are distorted by Govt policy.

Another great analysis.

I don’t really see the point of the price cap. It seems to be there to protect people from being ‘ripped off’, right? But the people who don’t care about their energy bills are usually those who can most afford it, while everyone in fuel poverty probably watches their credit balance/meter tokens like a hawk. That the rich(er) pay more (out of neglect) that inadvertently helps out the poor(er) doesn’t seem so bad to me. This is true for all ‘working’ markets, people who have more disposable cash are less price concious.

The price cap was introduced because the CMA falsely told the Government that suppliers were making £1.4 bn of EXCESS profits per year. This was complete rubbish, but the Government bought it and decided it was an outrage, hence the introduction of the price cap. It was never based in reality and has done nothing to help either consumers or challenger suppliers.

Some short term things the government could do:

Issue more UKA emissions permits, since with the IFA outage we will be needing more GB generation, and the current high price of UKAs affects the whole market, even outside balancing mechanism prices. It’s a needless impost in present market conditions, and could even be sensibly abandoned altogether over the winter.

Instruct OFGEM to find ways to stop Drax et al. from gaming the market by not making offers in the day ahead market even at £450/MWh knowing that they will clean up at £4,000/MWh+ in the Balancing Mechanism. These markets are not functioning properly.

Restructure the forthcoming CFD capacity auction away from more reliance on wind and towards reliable capacity.

Find a way to get the Calon units back into operation.

Support further North Sea oil and gas development: the important thing here is sentiment as much as anything else. If industry believes that government is going to damage domestic fossil fuel supply it will assume that very expensive alternatives are planned, and therefore it will lobby accordingly for subsidies and highly distorted markets. That will echo through into high pricing in gas and electricity markets.

The difficulty of course is that they won’t feel like even trying to do any of this ahead of COP26 if it is going ahead in November, so perhaps the best thing of all would be to announce it will be deferred sine die while the problems are dealt with.

I’m not sure that Greg Hands as the new minister has the necessary grasp of the issues. I note that John Redwood is ratehr more onboard (after a little prompting…):

https://johnredwoodsdiary.com/2021/09/16/we-need-more-electricity/

So I’m afraid I disagree on the BM gaming…remove the ability to do that and capacity market prices will go up. Ultimately, generators need to make enough money to cover low utilisation rates, and whether that money comes from the BM or CM is irrelevant.

I completely agree on N Sea gas E&P. This is necessary regardless of climate ambitions, because even on rapid de-carbonisation pathways, we will still need a lot of hydrocarbons in the economy…scarcity leads to high prices, and high prices lead to economic shocks. Unfortunately, I’m not sure there’s enough gas on th UKCS that can be economically extracted to address our supply issues. Another approach would be to invest in a new seasonal storage faility, perhaps by taking one of the sites earmarked for CCS, but I think that will be a hard sell.

In the short term they need to do two things – get the Calon assets running again (maybe a juicy black start contract or other AS can sweeten the deal), agree to keep coal open until 2026 (to incentivise re-stocking of coal supplies), and suspend the price cap. The first two to address near-term capacity issues and the second to stop more suppliers going bust.

Over the medium term we need a hear think about how to deal with low wind when thermal and nuclear plant has low availability due to age. I still think Wylfa could be built before HPC, so I’d get that done, and then there needs to be some hard choices about whether new CCGTs should be built and whether they can be reliably supplied with gas. There’s talk in the markets of gas shortages this winter – I don’t know how real those are – but it’s enough to make me re-think my previous “build more CCGTs” approach…

I think the capacity market needs a redesign too. We saw that an energy only market like Texas fails to provide sufficient capacity once you start to grant grid priority to unreliables and start pushing down utilisation levels – and arguably the UK market is suffering the same fate. Just as your elegant demonstration of the difference between hedging and accepting grid settlement pricing for retailers, the UK capacity market for firm dispatchable capacity essentially leaves the market unhedged for Dunkelflaute – too much money is on the table for unreliables, who should not be permitted to bid for firm capacity they are unable to provide. The point is backup is needed in extreme circumstances, not average ones, and therefore the money should only go to those capable of providing for extreme circumstances. The Dieter Helm solution of forcing unreliables to team up with dispatchable capacity is perhaps one way to go. The downside is that it would make plain that essentially close to 100% backup is required, and so long as you mandate renewables in the equation you are inevitably opting for high cost solutions.

The capacity market has failed because the backup capacity demanded by the state has proved to be too small, and because those capable of supplying backup power understand the economics of market squeezes and being excluded from the market due to too high a bid on the capacity market. They know that the alternatives are expensive diesel STOR, at least once it is back out of mothballs. They know they can maximise shareholder return while leaving supply perilous.

Back in the day we had a much more competitive market that was able to meet demand and provide insurance against over reliance on any particular fuel by promoting switching on economic grounds. The system was designed with baseload and variable elements in mind. I think we should benchmark against such a system design which probably would include next to no renewables. Then we can begin to understand what this mess is costing us.

I agree – the capacity market doesn’t really work because the sole objective seems to be to avoid blackouts. But blackouts here (based on 2 data points in 13 years) have been due to technical rather than economic failures. Now we have a massive supply side failure, and while we’re probably not in blackout territory, things are getting very uncomfortable.

The problem isn’t just Dunkelflaute, it’s the fact that because conventional generation economics have eroded so much old plant hasn’t been renewed, so is less reliable. This is particularly acute with nuclear. The CM was designed to back-up when it’s not windy but I think the reliability of the conventional fleet has been taken forgranted when it shouldn’t have been. The mixture of low wind and low conventional availability with the odd interconnector outage thrown in is what’s hurting us now.

Hi all…..great analysis/debate on a looming crisis often alluded to on this forum.

I do agree however that existing green targets need to be relaxed before crazy policies bankrupt the UK.

As always punching well above my weight here, but dare I mention tidal barrage yet again ?

Need your patience plus apologies for a local theme, but here goes:

The recent AUKUS pact to build a fleet of nuclear powered subs. is a landmark moment.

Sure the west cumbrian existing major facilities including BAE Systems, Rolls-Royce etc. are likely benefit massively.

The Barrow conurbation continues to be isolated from the main transport network (2 hrs by road)

A toll free causeway (17 miles) across Morecambe Bay & Dudden estuary would reduce the journey from M6 exit 34 to 30 mins.

Oh! there’s also the byproduct, providing greener than green electricity at predetermined times 365 days a year from 31 turbines embedded beneath the carriageway.

http://www.cumbriachamber.co.uk/wp-content/uploads/2019/04/NTPG_update.pdf

IMO these schemes, sure there are other suitable estuaries around the UK, need a revisit & some serious funding.

Tried to refrain from including that old boring chestnut, the Severn although linking Weston Super Mare & Cardiff, a mere 11 miles plus favourable tidal flows can’t be ignored.

I just feel that some of the billions spent on wind & solar could have been directed to R&D of tidal barrage schemes.

The linking of coastal communities is so important & should figure more in Boris’s levelling up sentiments.

What better than achieving this & producing green energy.

Wind turbine or solar farm only produce random intermittent electricity.

I believe both are proving to attract high maintenance cost & reduced life span.

I know lots has been done re tidal barrage schemes, the CEGB got to almost shovel ready with the Severn 20/30 years ago. Just feel the whole subject has been undersold or am I missing something ?

Barry Wright Lancashire.

The problem with tidal is that if it was really viable I’m sure there would be more of them. There are only two “big” tidal schemes which are c 250 MW – Sihwa Lake and La Rance.

It’s also not entirely clear that they are environmentally sustainable since they disrupt local ecosystems which can be quite fragile. And then there’s the cost – the Swansea Bay scheme wanted a CfD for a century (https://watt-logic.com/2017/01/16/tidal-lagoons-too-good-to-be-true/)! Tidal is also intermittent – Euan Mearns did some analysis and showed that all the proposed tidal sites had tides which were in phase, so you wouldn’t get anything close to baseload. It would be more predictable than wind, but sadly, predictably intermittent!

I’ve always wanted to believe in tidal power. I lived on the Thames in East London where the tidal height was about 8m between high and low tide, and the volumes of water are phenomenal, but the problem is how to make it economic.

The fundamental problem is the UK is over-dependent on two primary energy sources: unreliables and gas.

A stand-out comment from Helm was how the uncertainty of wind will be projected onto UK gas demand (as gas fired generation is relied upon to balance wind). The UK will therefore face the challenge of forecasting wind resources at the 1-2 week-ahead stage to be able to lined-up gas for delivery when unreliables fall short. This is unachievable, and therefore some level of loss of continuity of energy supply will happen if the UK banks on the above two energy sources. And – as we are finding out today – there is nothing to say the UK will be able to live with it.

I don’t agree the Calon assets are an answer to out problems right now. More CCGTs add generating capacity but today’s problem is shortage of primary energy, and reliance on two primary energy sources. Having more metal on the ground to make power doesn’t address the problem.

It might be a bitter pill for some to swallow, but keeping the remaining coal units open will be crucial, and this is probably now only a matter of the timing of a difficult announcement (if COP26 is still going to happen).

Extending the life of the existing coal fired capacity will not be an easy and cheap option. Having been told by authority that they must close soon, asset owners will have saved on maintenance and parts replacement (but still satisfying statutory obligations and safety imperatives). It will take an “investment-grade business case” to inject significant sums of money to prepare them for several more years’ operation. There will be long-lead-time components to order, and extended periods of outage to get through.

Lifetime extension also faces challenges with skills retention, as coal fired generation will now be seen as an unattractive and dying sector for younger people starting their careers today. Echoes of the HGV driver shortage.

The UK needs to bite a bullet right now. It needs a fleet of large new coal fired generating stations.

This gives the UK primary fuel diversity for security of energy supply, This gives the UK the capability to economically store large quantities of fuel for protection against uncertainty in short-term primary energy supplies. It aligns UK energy costs with international competitors to make sure we might have something to export.

The order to close coal fired generating capacity has to go. The ban on granting planning permission for new coal fired capacity has to go. The CO2 taxation (the only reason why coal fired generation cannot compete) has to go. The government must do the above in a way which creates confidence in the sector to keep physical supply lines open, and to attract youngsters into the industry to maintain the skills necessary for safe and reliable operation.

Didn’t somebody once say something like: “Build back better”?

Hi Kathryn…..Thanks for a excellent series of in depth interesting postings, promoting lively debate.

Apologises should my posting today stray off topic, but I need to raise several points at this crazy time.

In short, a voice from the street based on my thoughts.

The problem with tidal is that if it was really viable I’m sure there would be more of them.

There are only two “big” tidal schemes which are c 250 MW – Sihwa Lake and La Rance.

A valid point but how much global scrutiny is devoted to troubled failed nuclear projects around the world ?

Your posting charting EPR projects is a great summary, yet we push on.

The stats & science seem to drive a narrow focus IMO, irrespective of the actual failures time & time again.

On the other hand we see tidal schemes dismissed as not viable based on others not embracing the concept.

Couldn’t be worse than the nuclear debacle we face; why pursue such troubled technology ?

Little doubt nuclear has to be part of the energy mix for the future.

However I still feel tidal barrages have been back shelved over the years in favour of wind & solar.

Summerising:

Why view a world of nuclear projects & continue to push on along the same troubled path.

Discount tidal schemes just because others don’t adopt the concept.

I fail to appreciate the logic in this, strong stats. & science aren’t always a sound basis.

Construction of Heysham 1 started 1970.

I was involved (1960’s) in building/uprating of the network to accommodate the output.

From my apartment I see the overhead line infrastructure I helped build.

Maybe new conductors but the overhead line towers remain, every one a story.

The station was designed by the nationalised Central Electricity Generating Board (CEGB).

The build was handed over to a private consortium with a brief to adhere to a compact layout.

Already in trouble due to the reactor building sitting on a seismic fault preventing all future on line refuelling.

A serious dent to the income stream.

The compact layout also contributed to a major over spend & 13 year delay (comm. 1983)

No station transformers, back up from a couple of Rolls Royce Olympus gas turbines.

Often referred to as watch making by the ton the troubles continued throughout construction.

As we approach Heysham 1 closure 2024 I see a complete picture with mixed feelings.

When generation ceases we are left with a 250 ft. high grey concrete reactor building.

A blot on a beautiful coast line for ever more.

A 40 year life span of a plant that I’m sure could never repay the Capex costs.

Thinking the Morecambe Bay tidal barrage in a similar vain.

Possibly twice the life span or more, 120 years quoted.

Say all 130 turbines in the causeway reached end of life & decommissioned.

Reaching my point of widening the focus referred to earlier.

Nil generation maybe but we are left with a trunk road across the bay linking Barrow & beyond to the main transport network.

A 75 square mile inter tidal lake for multi leisure activities.

Control of the annual flood threat to 1000’s of homes & businesses around the bay coastline.

Barry Wright Lancashire.