On Tuesday, Centrica announced the permanent closure of Rough, its large seasonal gas storage facility. This is the UK’s only long-term gas storage asset, with a capacity equivalent to about 10% of winter peak demand and 70% of the country’s total gas storage capacity, so its closure marks the start of a new period in the UK gas market, of growing dependence on imported gas by pipeline from Norway and Russia, or by LNG from the US and Qatar. The market has widely been expecting this news, and National Grid anticipated no availability of Rough gas in its outlook for the coming winter.

Why is it closing?

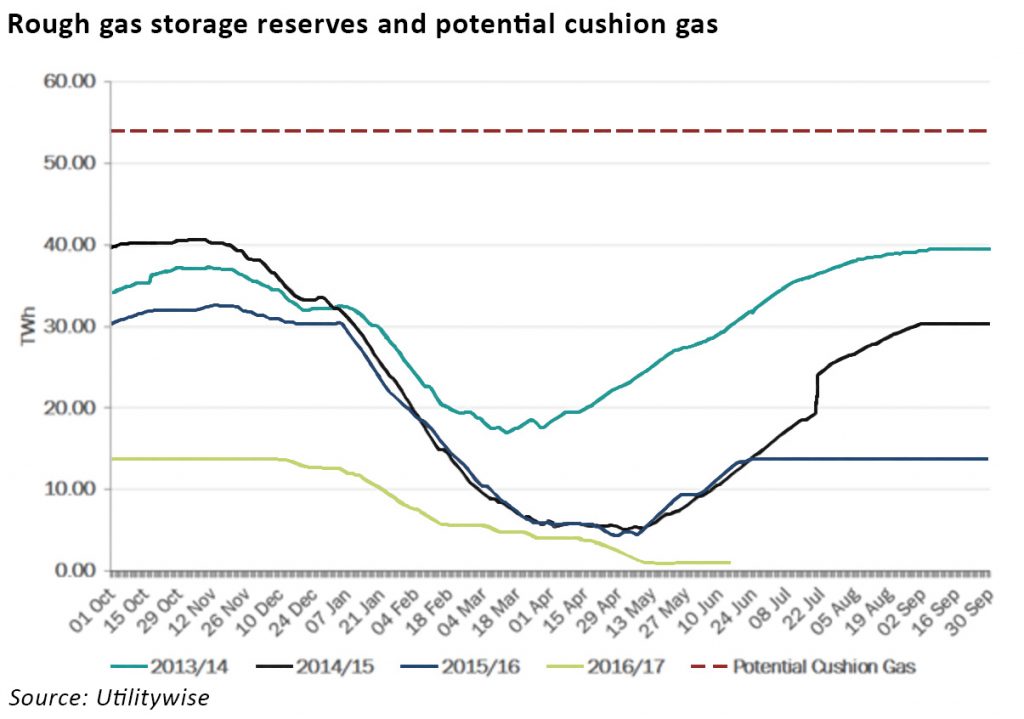

Rough began operating as a storage facility in 1985, after 10 years as a producing gas field. There have been operational concerns about the facility for some time, with Centrica curtailing its use last year for further investigations into the integrity of its wells. On Tuesday, the company announced it would close the facility permanently citing safety concerns.

It now plans to produce all the remaining recoverable gas from the field, pending approval by Ofgem. The cushion gas, which was used to maintain the minimum pressure levels needed for the field to operate as a storage facility, is estimated at 54 TWh (approximately 1.8 billion therms, which compares with expected UKCS gas production in 2017 of 12.5 billion therms). This process is likely to take several years, and as both the timing and volume are uncertain, so the impact on the market has been muted.

Falling demand for gas storage was in any case threatening the commercial viability of the asset, so it may well have been forced to close even without the additional investment needed to fix the well integrity problems. European utilities are losing billions of euros on gas storage, triggering site closures and divestments in a market suffering from oversupply and weak demand. In 2015, announced it would mothball a third of the withdrawal capacity at its Hornsea site.

The cost of decommissioning the facility is seen as broadly neutral when the value of the cushion gas is taken into account.

Reliance on imports

The closure of Rough leaves the UK more reliant on imported gas, at a time of increased political uncertainty. The UK imports gas either by pipeline from Norway or Russia (via pipelines across the EU), or by ship from Qatar and (in future) the US.

Statoil, the Norwegian state oil company, has indicated that it does not plan to materially increase its volumes to the UK, although there is some capacity to provide short-term boosts in supply if needed.

34% of Europe’s gas now comes from Russia, and this share could be expected to increase with the construction of the Nord Stream 2 pipeline, however, the EU is currently facing internal divisions over the project, with Eastern European countries opposing the scheme in the face of strong support from Western countries. In addition, the recent decision by the US Senate to reinforce sanctions against Russia, which would particularly affect companies involved in the Nord Stream 2 project.

Closer to home, Brexit means there is uncertainty over the operation of the gas interconnectors with the EU. Following Brexit, the remaining EU countries will be slightly more dependent on foreign gas (losing access to the UK’s own production), however, assuming Brexit means exiting the customs union, there will need to be a negotiation on the terms of UK access to EU gas, and the operation of the pipelines.

The other consideration is that Ireland will become cut off from the rest of the EU – Ireland depends on the UK for the majority of the gas it uses, and as Ireland has even less storage capacity than the UK, there is uncertainty over how Ireland will be able to implement the EU Security of Supply directive.

On the LNG front, Qatar, the UK’s largest supplier, is facing a diplomatic crisis over alleged support for terrorist groups. This issue is unlikely to have broad price impacts for LNG, but the consequences for European buyers relate to the diversion of LNG ships round the Horn of Africa, rather than using the usual shipping lanes in the Suez canal. This doubles the transit time, and the unexpected diversion of two tankers to the UK in recent weeks lead to price spikes.

“It takes two weeks for a cargo of LNG to arrive from Qatar, which is not a politically stable place right now. That does raise the political implications quite a lot, along with Brexit. So it’s a perfect storm in terms of security of supply for the U.K.”

– Graham Freedman, principal analyst for European gas and power,

Wood Mackenzie Ltd.

Qatar Petroleum has said it’s business as usual, however if all imports were to suddenly stop, the UK would now only have access to 10 days worth of natural gas, compared with 24 days when the Rough was operating. By comparison, Germany and France each have more than 100 days of fuel stored.

Bloomberg reports that Energy Aspects Ltd is predicting a 39% increase in the UK’s LNG imports next year, partly in response to the closure of Rough, which it has anticipate in its recent forecasts. However, predictions of significant waves of new LNG coming to Europe have not previously been delivered….supply was expected to build up last year but increased demand in Asia, the Middle East and Latin America made those markets more attractive.

With the news this week that South Korea plans to end its reliance on nuclear power, even more Asian LNG demand can be expected in future, although any Korean nuclear exit would not happen quickly. The UK may well have to pay up if it wants to see significant numbers of cargoes landing at its terminals.

Prices likely to be spikier and more volatile

Analysts expect the closure of Rough to increase price uncertainty and volatility.

“Though we haven’t seen a material impact on prices yet – most probably because there is still a significant amount of recoverable gas in the field, which could last for years – the pressure could come in the winter months, especially if we experience very cold conditions.”

– Matt Osborne, risk manager at energy consultancy Inenco.

Timera Energy described the price impact of Rough’s lack of availability in April, anticipating increases in spot price volatility as any closure would reduce the buffer of supply flexibility available to respond to swings in daily demand, citing evidence of volatility recovery in 2016, following the partial Rough outage.

The loss of storage capacity is likely to mean that supply shocks such as major infrastructure outages would have a stronger and more prolonged price impacts. This would be positive for the value of other gas assets in the UK, including the remaining gas storage facilities and LNG terminals.

Although the idea of more price spikes and higher volatility sounds worrying, there is some precedent suggesting the closure of Rough will not have a dramatic effect. In 2011 there was a prolonged cold snap in the UK at the very end of winter when storage sites were cyclically empty. At the same time, a brief outage occurred on the interconnector with Belgium, leading to within-day prices of over 150 p/th.

As I described previously, the duration and amount of the raised prices was not sufficient to attract LNG away from Asian markets, which were then the highest priced markets for gas in the wake of the Fukushima disaster. This confirmed the prevailing view that the European market was significantly long gas and that additional investment in gas storage was not justified.

As the UK is generating about 50% of its electricity from gas, following the closure of various coal plants, there is likely to be a knock-on effect on power pricing. In addition, as some 80% of British homes are heated with gas, there will be further upward pressure on domestic energy bills.

What next?

The government’s efforts to decarbonise the heating segment, has led to the recent announcement of funding for two new projects: £25m for research into whether existing gas pipes can be used for hydrogen, and the impact on consumers of using hydrogen boilers in their homes rather then natural gas boilers. A further £10m is being invested in “smart heating”.

These projects are still in their very early stages, and the idea that the gas network can be converted to using hydrogen faces many challenges (not least the need for a viable CCS solution, which is still somewhat remote).

The closure of Rough coming as it does at the same time as declining North Sea production and increases the in political risks facing the UK energy market, it would not be surprising to also see renewed interest in domestic shale gas production.

In the near term, the price impacts will probably be modest, but there are definitely more pressures than previously, and in times of system stress, the consequences may well be more significant than in the past.

Leave A Comment