The 1 GW BritNed interconnector linking GB with the Netherlands has suffered another fault and is expected to be out of service until late April, meaning it has spent much of this winter out of action. In addition to contributing to a tight GB market, these outages illustrate some of the challenges facing offshore electricity infrastructure, particularly in sub-sea environments.

BritNed tripped on 8 December and did not return to service until 9 February due to a cable fault. The damaged cable section was found approximately 100 km off the Dutch coast at a water depth of 40-50 meters. Repairs were successfully carried out within 29 days despite severe weather. But now the interconnector has developed another fault, probably with the cable again, and is expected to remain out of service until 22 April.

These outages mean that BritNed will have been offline for a significant portion of Winter 2020, a risky position given it holds a capacity market contract for the current delivery year. There have been two Capacity Market Notices (“CMNs”) issued this year, the second of which came just days before BritNed’s first outage. While a failure to deliver following a CWN does not attract penalties unless a Capacity Market Stress Event occurs, the issuance of both CWNs and Electricity Margin Notices this winter, combined with high price volatility, indicate the markets have been much tighter than usual.

These outages mean that BritNed will have been offline for a significant portion of Winter 2020, a risky position given it holds a capacity market contract for the current delivery year. There have been two Capacity Market Notices (“CMNs”) issued this year, the second of which came just days before BritNed’s first outage. While a failure to deliver following a CWN does not attract penalties unless a Capacity Market Stress Event occurs, the issuance of both CWNs and Electricity Margin Notices this winter, combined with high price volatility, indicate the markets have been much tighter than usual.

BritNed has been in operation since 2012, and has had something of a chequered past. In 2018, the High Court awarded the company, a joint venture between National Grid and TenneT, the Dutch grid operator, £13 million in compensation after finding it had suffered damages as a result of a cartel that existed between cable manufacturers. The cartel was in operation between 1999 and 2009, and included ABB, the supplier of the BritNed cables.

The cartel had come about when the cable manufacturers perceived there to be a global surplus of capacity in the market, and therefore sought to support prices, by agreeing certain limitations to competition. European and Asian manufacturers agreed not to compete in the other’s regions, and within each region projects were allocated between manufacturers, with the rest agreeing to submit uncompetitive or non-compliant bids to ensure contracts were awarded to the right manufacturer. This affected the tender process for BritNed, where ABB provided the only compliant bid and was therefore awarded the contract.

The damages awarded were significantly lower than BritNed’s claim, since the judge found that ABB had priced the contract based on its actual costs, but he also found that ABB’s costs were higher than its competitors since it used more copper in its cables. This was borne out by the fact that after the cartel was disbanded, ABB consistently lost out in competitive tenders. The judge also found that although BritNed’s losses were limited by its cap-and-trade regulatory model which limited its ability to earn profits, ABB was not entitled to retain the benefits of its participation in the cartel.

The need for new regulatory models for offshore electricity infrastructure

The importance of cable reliability goes beyond the economics of individual interconnectors and even the risk of capacity market penalties. With the growth of offshore wind has come the growth of a whole new set of interconnection: asset to market rather than market to market.

Offshore electricity infrastructure is typically developed on a point-to-point basis, rather than as part of a network, and as such has much less ability to use alternative routes than onshore equivalents. Cable failures are also much harder to find and resolve offshore, being less accessible due to water depth and weather conditions.

The ownership models are also different: where network operators in GB have regulated income and risks under the RIIO (Revenue = Incentives + Innovation + Outputs) model, interconnector owners face either full merchant risk or operation under a cap-and-floor regime (BritNed is a little different having capped but not floored returns), while offshore wind connections are subject to the OTFO (Offshore Transmission Owners) regime which enforces the separation of ownership between offshore generation and transmission assets, and provides a regulated rate of return.

The UK Government has set out a major ambition to deliver another 40 GW of offshore wind by 2030, which inevitably will require larger projects, further offshore. It also means that the current point-to-point model for offshore transmission infrastructure will almost certainly need reform for a number of reasons:

- Physical space onshore is limited, so landing electricity from different projects separately will become increasingly untenable;

- Operational efficiencies could be secured by combining infrastructure across projects for example by booking scarce installation vessels for multiple offshore substations would reduce scheduling delays, but this is difficult to do under current regulations which tie cost recovery to specific qualifying projects when the different phases of large projects tend to be submitted as separate qualifying projects in OFTO tender rounds;

- The current offshore regime does not allow for over-sizing infrastructure since such costs cannot easily be recovered, but such over-sizing could be a more efficient approach when additional projects or phases of the same project may be developed nearby, or where batteries, hydrogen electrolysers or other technologies might subsequently be co-located;

- The scale and complexity of new projects is increasing the capital requirements to a level where new investors need to be encouraged into the market;

- Most links are developed by generators who are legally required to divest the connections within 18 months of commissioning under tenders run by Ofgem, but multiple extensions have had to be granted since projects are increasingly complex meaning tenders must be staggered to allow proper time for bidder evaluation.

BEIS is currently carrying out a review of the offshore transmission regime, to identify how increased integration of offshore electricity assets can increase efficiency and prevent the 2030 goals from being undermined by the limitations of the current regime.

This is a complex undertaking given the large number of stakeholders involved – as well as the usual suspects (National Grid ESO, Ofgem and offshore wind developers) it also involves the Crown Estate (and Crown Estate Scotland) who typically award seabed rights, Defra which is responsible for the natural environment, the Marine Management Organisation and Marine Scotland which deal with the sustainability of marine activities, and the Ministry of Housing, Communities and Local Government which is responsible for local issues in relation to the impact of onshore infrastructure.

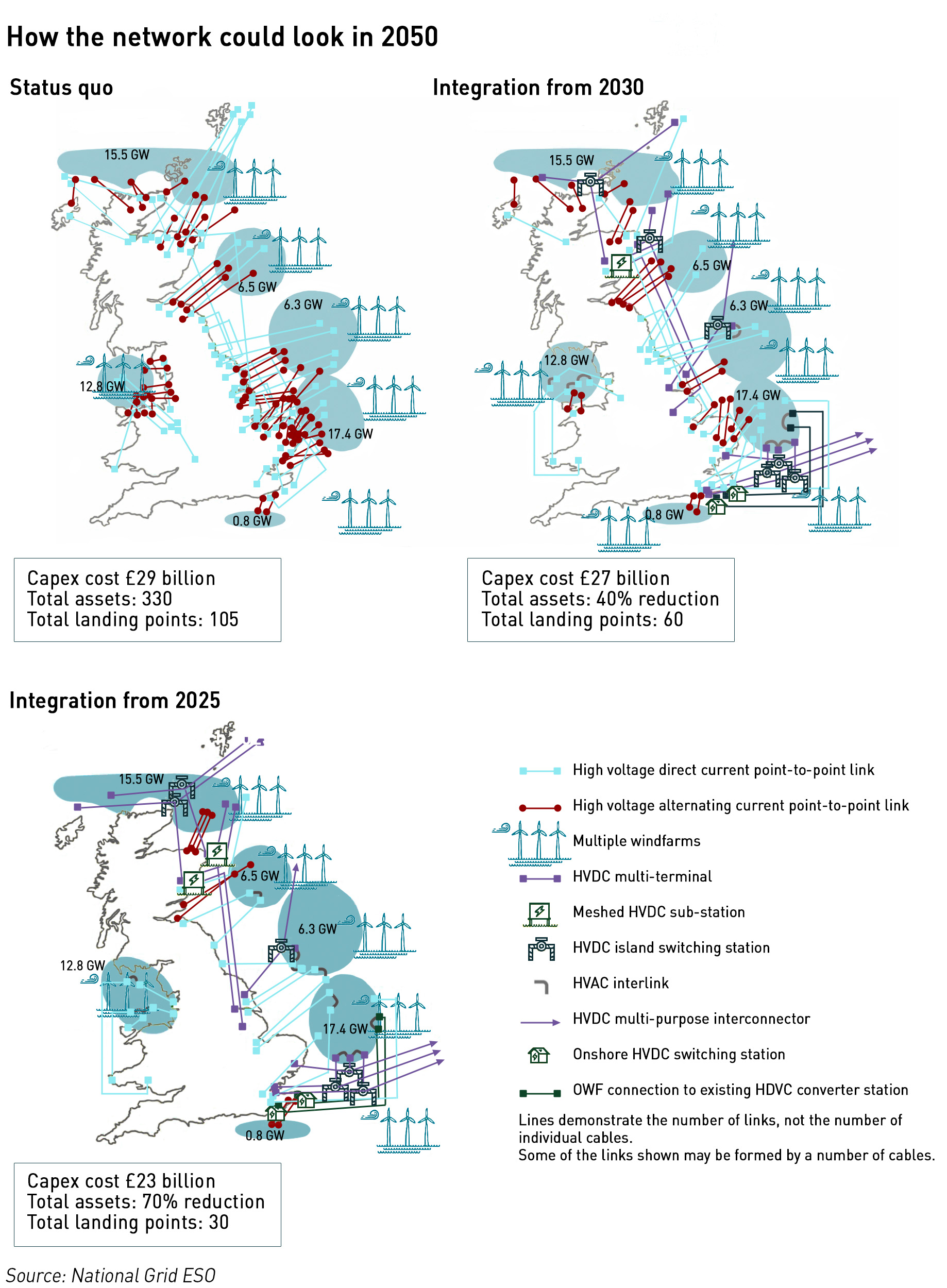

“Adopting an integrated approach for all offshore projects to be delivered from 2025 has the potential to save consumers approximately £6 billion, or 18 per cent, in capital and operating expenditure between now and 2050,”

– National Grid ESO

As the offshore energy environment becomes more developed, there are good arguments for moving away from the existing radial model, to the creation of offshore networks. The current regime is increasingly mired in inefficiencies, while the technical problems affecting the 9-year old BritNed link illustrate some of the challenges arising from point-to-point connections, particularly with sub-sea infrastructure.

The creation of a new regulatory model for Britain’s offshore electricity infrastructure is not a simple task, but without reform, it will become increasingly difficult to deliver the range of new offshore projects that are likely to be required in order to meet net-zero targets.

All this nonsense to eliminate Britain’s 0.0000002% of CO2 into the atmosphere.