There are signs of squeezed power market supply and demand margins. Last week saw National Grid ESO issue two Electricity Margin Notices (the new name for the Notice of Inadequate System Margin, or “NISM”), warning of a potential shortfall in electricity generation in the GB market, and encouraging more generation onto the system. The last time such an alert was sent out was in May 2016, but September saw the first Capacity Market Notice since late 2016.

Both of these instances saw low wind generation – not an unusual situation during cold winter high pressure weather systems – think of all those clear, cold and above all still, frosty days. They were also characterised by the use of coal to meet demand.

What happened?

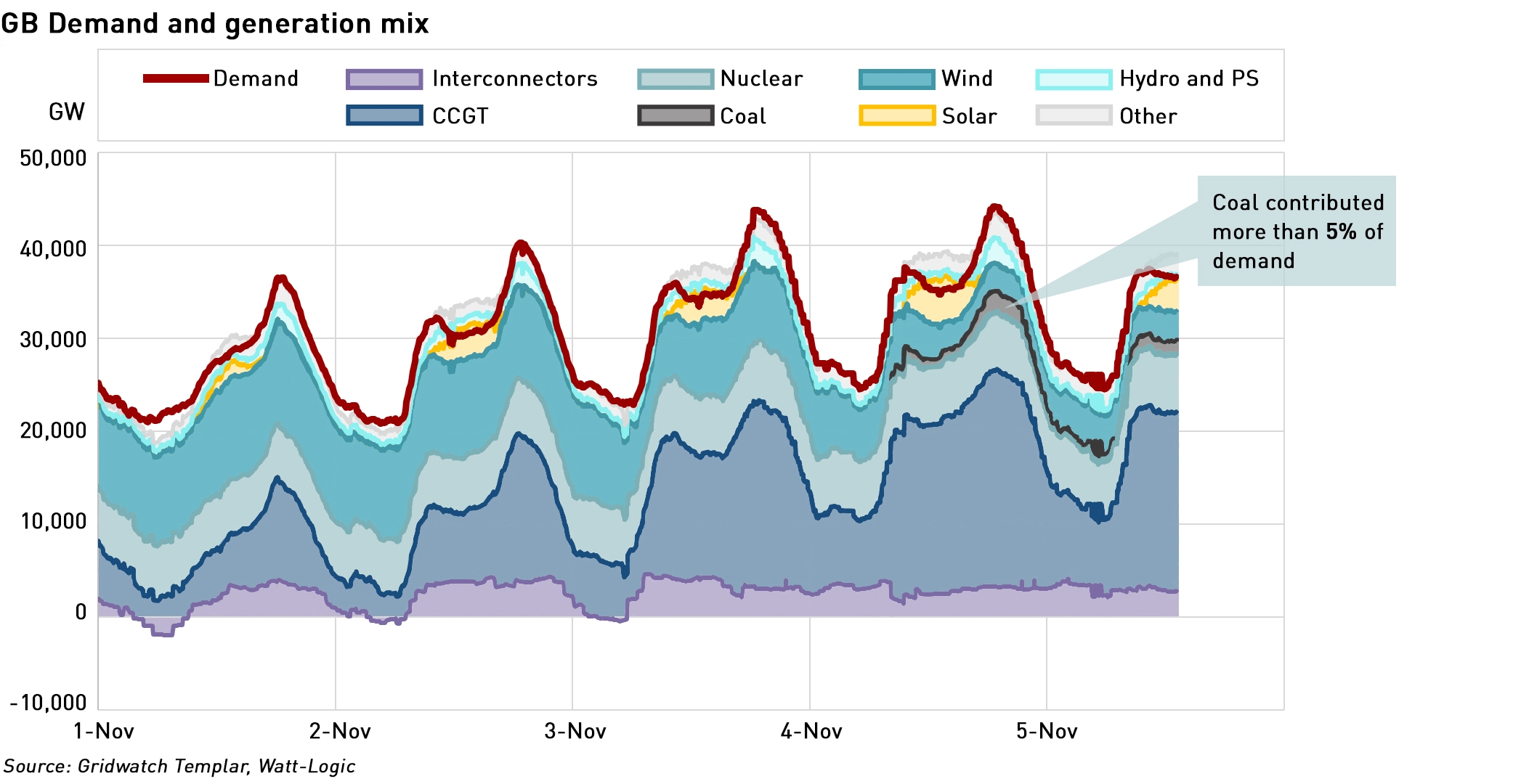

The first Electricity Margin Notice was issued just after 8pm on Tuesday last week (3 November), when a 740 MW shortfall was predicted between 4.30-6.30pm on Wednesday. An update was released at 10am on Wednesday stating that the shortfall had dropped to 477 MW and shortly after 1pm the alert was withdrawn, indicating that sufficient new generation had been attracted into the market.

However, 7 hours later, a second notice was issued for the same time period on Thursday evening, this time predicting a 466 MW shortfall. This was revised down to 316 MW by Thursday morning, and withdrawn at 2pm that afternoon.

According to the Energy and Climate Intelligence Unit, the predicted deficit for Wednesday was partly the result of the series of outages: three nuclear power stations were offline (Hinkley Point B, Heysham 1, and Dungeness B), as well as five CCGTs (Carrington, Fawley, Pembroke, Kings Lynn and Coryton) and the Drax biomass plant. There was also a partial outage at the East Anglia One offshore windfarm, while imports via interconnectors were expected to be low due to reduced nuclear output in France. Coal plant fired up to meet the shortfalls.

Although National Grid ESO emphasised that the expected shortfalls did not take account of its reserves – meaning blackouts were unlikely – various market observers suggested otherwise.

“The actual impact of those very high winds earlier on in the week was that we saw something which we very rarely see in the UK power market – negative pricing. You’re in that position then all of a sudden you had this drop off in wind, and wind power output was less than forecast. And then temperatures dropped. We had a mini anti-cyclone over the UK so that’s when you get stone cold temperatures and no wind at all, which is when we always see these big price spikes. And the fact that wind power had been asked to switch off just a day before or so would have meant there wasn’t as much generation which was ready and running as you would normally expect,”

– Jamie Stewart, managing editor for energy at ICIS

The situation was compounded by uncertainty over the levels of demand as the UK began its second national lockdown – unlike in the first lockdown in the Spring, the new lockdown began as the country experienced its first proper cold spell of the winter with most parts of the country seeing night-time frosts, meaning people working from home would be using more heating. And with sunset in the South of England now at 4:30pm, much more lighting is also needed.

Will it happen again?

The excess wind power at the start of the week pushed power prices into negative territory, creating a dis-incentive for generators to begin ramping ahead of the predicted demand uptick. Jonathan Marshall, of the Energy and Climate Intelligence Unit told The Times newspaper that the warnings showed that “the rapid transition in Britain’s electricity system is outpacing the changes in governance and regulation needed” to encourage the emergence of more flexible technologies such as batteries which would have allowed the excess wind power available from the storms earlier in the week to have been stored for later use when wind levels and temperatures both fell.

While National Grid ESO emphasised that low wind output was only one factor causing the alerts, it acknowledged that balancing the grid is becoming increasingly complex as more intermittent generation is brought online. More than 10,000 wind turbines now operate in the GB market with a theoretical maximum output of 24 GW. Over a typical year, their output averages about third of that level, equivalent to the annual energy needs of 18 million homes. However, there have been times this winter when wind has produced barely a tenth of its potential output, below the 16% assumed in NG ESO’s winter planning, and once again, coal is ramping up to fill the gap.

Of course, in a net zero carbon world, there will be no coal around – the UK is committed to closing its remaining coal plant by October 2024. The Capacity Market was designed to incentivise new generation to replace exiting coal and aging gas and nuclear plant, but so far the most successful technologies in the Capacity Market have been small-scale gas and diesel engines, which are also incompatible with a zero-carbon world.

While system margins now look better with the warmer weather, more shortages are likely through the winter, particularly with two large CCGTS, Severn (850 MW) and Sutton Bridge (850 MW), being essentially mothballed last summer when their operator, Calon Energy, went into administration. The Severn plant was only commissioned in 2010, indicating that even relatively new and efficient gas plant is struggling to remain economic

“This doesn’t seem to be a one-off. These shortage events look increasingly common in the market and should be expected to continue throughout the winter. The loss of Calon in such a manner – during a period when the market is seeing these tight margins – raises the question of whether the capacity mechanism has sufficiently ensured that plants will be able to make up the ‘missing money’ that results from plants having to meet the proportion of demand that is not met by renewables and other subsidised generation, whilst stepping aside during periods when renewable output levels are strong.”

– Paul Verrill, director of EnAppSys

The four-year ahead nature of the Capacity Market auctions means that operators must estimate years in advance what additional income they require from the Capacity Market in order to be economic, but four years is a long time in a rapidly changing market. While there are penalties for non-delivery, if an operator falls into insolvency, or even if they pay the penalty, the market will still be short and need to find the missing capacity from elsewhere, which may well be at higher prices.

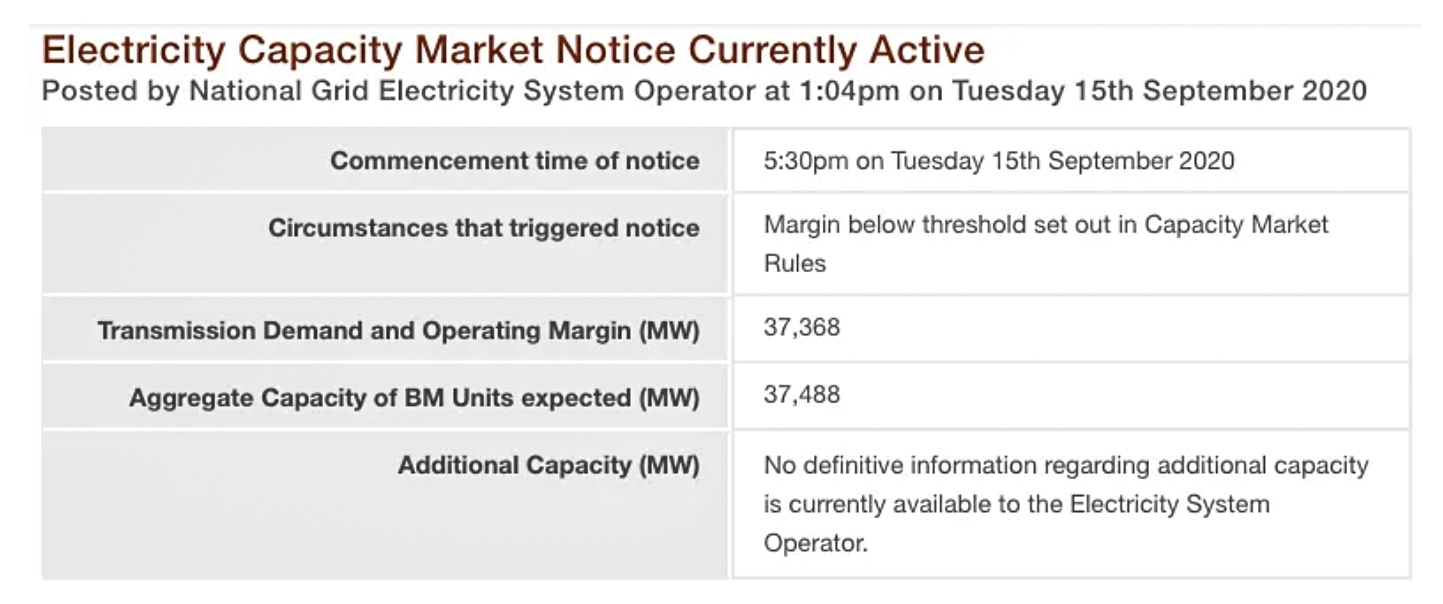

Capacity Market Notice issued in September

September also saw some tight capacity margins, spiking prices and the first Capacity Market Notice since Q4 2016 issued on 15 September.

A capacity market notice can be issued for one of three reasons:

- The System Operator gives a Demand Reduction Instruction or an Emergency Manual Disconnection Instruction to one or more DNOs

- An Inadequate System Margin is forecast (at least 4 hours in the future)

- Automatic Low Frequency Demand Disconnection takes place

In this case rule 2 was satisfied.

After an instruction is issued, generators holding a Capacity Market contract must be ready to generate during the time the short fall is forecast to occur (assuming they are not performing any other ancillary services). Other market participants not holding capacity contracts can also react to the market conditions and capitalise on the high market prices and volatility that are likely to coincide with the shortfall.

The Notice was cancelled when National Grid ESO was able to reverse the scheduled flows on the interconnectors, primarily with France. After the Day Ahead auctions, GB was set to export electricity to the Continent, but NG ESO was able to secure imports, primarily from France but also from the Netherlands and Belgium, using bilateral contracts. This supplied an additional 2 GW to the system, easing pressure on margins. NG ESO’s trades were at prices of up to £607.57 /MWh with these high price levels filtering through into the cash-out price.

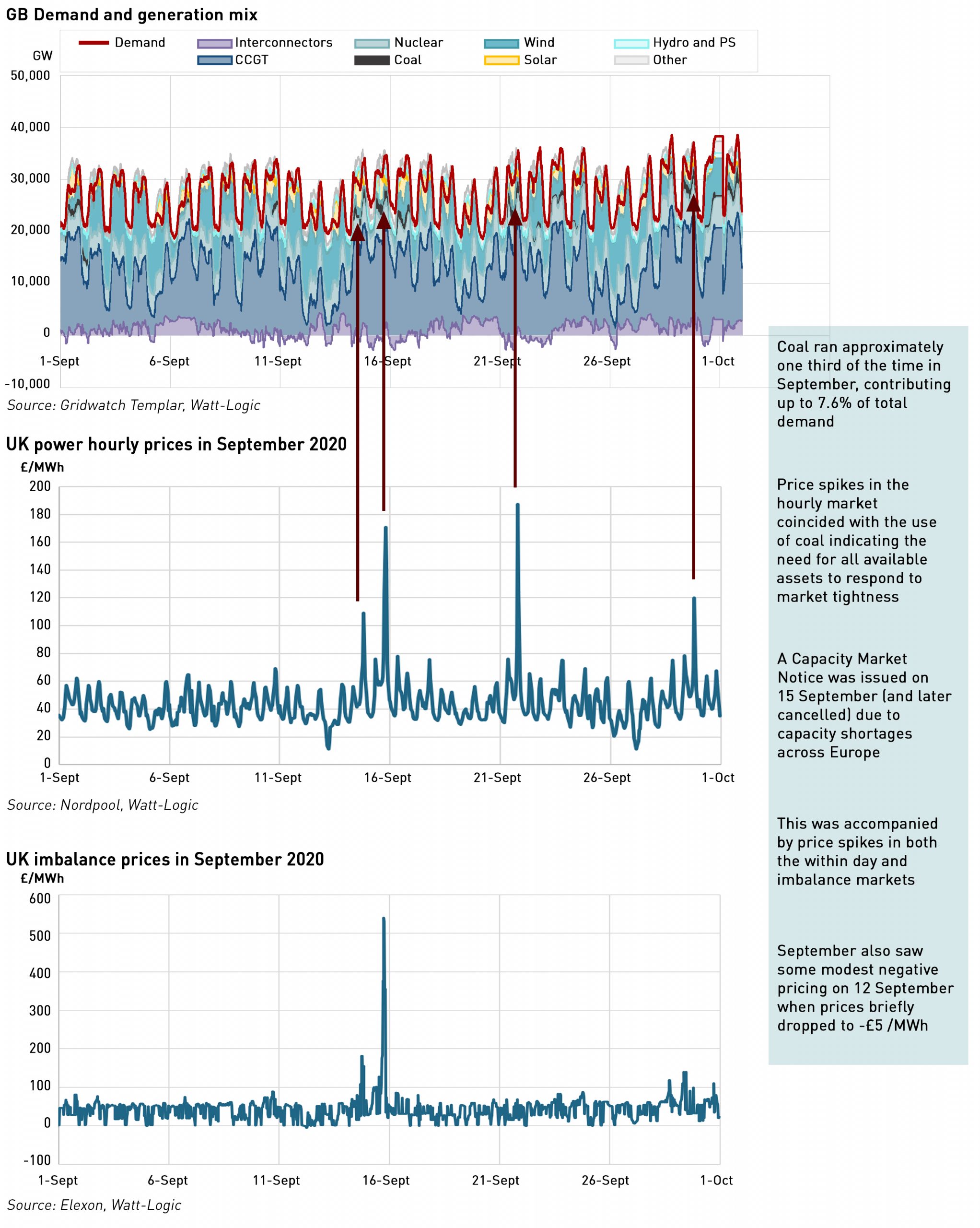

The charts below indicate the generation mix and demand during September, and the within day and cash-out prices for the month:

On the 15 September, prices spiked, with the system price reaching over £500 /MWh against a backdrop of high demand alongside low wind generation across northern Europe, which limited electricity available for import as well as creating a domestic shortfall. High prices were seen across Europe, with hourly prices of over €1,100 /MWh in Belgium and almost €4,000 /MWh in quarter-hourly trading in Germany.

“The biggest issue was that all of Western Europe had the same problem. This meant that, whereas countries would normally trade across the interconnectors to solve their issues, this was not really an option yesterday. This shows again how important it is to look at the European power market as an interconnected and interdependent system. The interconnectors can solve problems, but they also allow the problems of other markets to seep through to neighbours,”

– Jean-Peal Harreman, director of energy market data analyst EnAppSys BV

The chart also shows that coal ran multiple times during the month to meet rising demand, at times making up 7.6% of all generation.

A combination of never-ending subsidies and tight margins spell bad news for consumers

The failure of Calon and the ongoing difficulties of attracting new large gas plant into the Capacity Market indicate that the move away from market-based to subsidy-driven mechanisms is undermining both existing and new conventional generation.

Since the inception of the Energy Market Reform in 2013, successive governments have determined that consumers should subsidise specific renewable technologies in order to reduce the consumption of fossil fuels and hence reduce carbon emissions. However, in so doing, the economics for conventional generation were undermined, and so the Capacity Market was created in order to provide support, primarily to gas plant. Unfortunately, even with the Capacity Market, very little new large gas plant has been brought forward, and low utilisation rates mean the economics remain under pressure.

SSE’s 840 MW Keadby plant is one of the few new CCGTs being built in the UK and is on track for commissioning in 2022, with a gas turbine weighing as much as an Airbus A-380 arriving on-site from Germany in June. The plant secured a capacity contract in the 2023/24 capacity auction which took place in March this year.

“I don’t think it will be the last traditional gas plant we build but it will be the last one that doesn’t have carbon capture or hydrogen involved with it,”

– Alistair Phillips-Davies, chief executive officer of SSE

Now there are ambitions plans for new gas generation powered by hydrogen, but this will require even more subsidies both for the power stations and for the carbon capture that is likely to be required in the production of carbon-free hydrogen.

Consumers are getting the worst of both worlds, paying a high price for the subsidies that currently support almost every form of generation currently on the system, while periods of tight margins see spikes in wholesale prices. And at the other end of the spectrum, periods of low demand and high renewables output as were seen in the Spring lockdown – widely considered a sign of the future of the markets – saw balancing costs triple.

And all the while, despite the talk of de-carbonising not just the electricity system but the whole economy, we still turn to coal to keep the lights on.

I must admit to having had concerns that the “energy market” has a certain unreality about it; so that issues of continuity of power have been marginalised or neglected – and the benefits have been aimed at suppliers who can promise sufficient total energy for a years worth of consumption – but not when required.

Thus no value had been placed on continuity (or no apparent “market” mechanism exists for this). If continuity had been appreciated then one would expect that (thermal) battery plants might have been designed and developed of sufficient capacity to assist-or an appropriate premium for nuclear power (as the principal CO2 free reliable generation).

As you indicate by the high spot prices for energy the market is nearing that point at which there is not enough energy available to fulfil the contracts of supply – unless one uses fossil fuels and invest in gas powered generation.

I would like to ask if this is something that the regulator (OFGEN) should be doing about regulating the market?

Technically Ofgem already oversees this by setting the necessary parameters NG ESO must fulfil, in particular the SQSS. The problem is whether these measures are sufficient. I believe the are not for 2 reasons:

1. The SQSS ignores the fact that a significnt amount of embedded generation can be lost if there is a major outage caused by a local network fault (ie the thing that trips off the largest generator can also trip off lots of embedded generation nearby). This was the case in both the major blackouts of the past decade.

2. Away from dramatic blackouts it is becoming harder to maintain the supply and demand balance at a cost that is reasonable and acceptable to consumers. This year we have seen balancing costs increase dramatically, high price volatility with both positive and negative spikes, and increasing instances of intervention due to overly narrow capacity margins.

Ofgem is responsible for ensuring consumers get value for money, but this leg of the trilemma has been consistently subordinated in favour of de-carbonisation. Now that the security of supply leg is also under threat, more really should be done, since all of this means we keep having to run coal plant the is inconsistent with de-carbonisation (and more importantly, clean air) goals.

A plea… please don’t use the uncertain, unscientific unit of energy called a “home” – it is highly variable, changing with time (OFGEM redefines it annually for their typical bill calculation for example) and who uses it (wind farms often shoot low to maximise the number). Let’s just stick to kWh, MWh, GWh and TWh, which are constant. I wish they’d kept NISM, which sounds like a transformer buzzing just before it goes up in a puff of smoke!

I had already taken a look at the high wind event at the start of the month, and I noted that the Renewable Energy Foundation reported over 76GWh of wind curtailment for the 1st November at a cost of £5.95m – that is a constant flow of over 3GW for 24 hours: actual curtailment may have been somewhat higher, with metered wind forecast running at over 17GW for much of the time. I see no sign that we are going to invest in hundreds of GWh of batteries (let alone tens of TWh) to absorb such surpluses, even if we move towards 3GW of delivery capacity for dynamic system containment (but is the £17/MW/hour – equivalent to about £7.5m p.a. in continuous use for a typical 50MW/50MWh grid battery – paid for the service in recent auctions enough for battery capacity that isn’t called on a large chunk of the time?) – i.e. very short term balancing over seconds and minutes. Dinorwig and Cruachan did their best overnight, pumping at 1.6GW or so and adding useful inertia, but we were still left exporting up to 2.5GW at negative system prices to France, Belgium and the Netherlands, while consumer bills paid subsidies for e.g. Hornsea to run almost flat out at an average of 1,066MW, with no diminution in the £162.47/MWh price because CFD marker prices carefully avoided being set negative for any consecutive period of longer than 6 hours. Overall balancing costs were reported at £12.9m for the day.

The Grid Winter Outlook report

https://www.nationalgrideso.com/document/178126/download

has always looked very optimistic, with its assumptions on effective capacity available. Their forecast de-rated margin was some 4.8GW, of which 3GW comes from assuming net imports on interconnectors (recognising that we would likely export 750MW to Ireland). For wind generation, we assume an equivalent firm capacity (EFC) of 16 per cent. Which seems to be a tad optimistic given that metered wind output fell to around 2GW at the demand peak on the 5th, and as low as 900MW in the early hours of the 6th, taking us to little more than 5% of capacity. It also seems they underestimated system demand – partly because they overestimated embedded generation, rather than because it was exceptionally cold.

The thing is that if they are prepared to wear rose tinted specs for a forecast as short term as a few weeks, imagine the shade of rose (or is that Roisin Quin?) in preparing the Future Energy Scenarios that are driving government decisions at the moment.

We might have to agree to differ on “homes”! I know its unscientific, but not all of my readers are energy experts and it’s a useful way of measuring scale – 18 million homes out of a total of 27.6 million is significant, and provides a measure of context I agree about NISM though, it’s a much better acronym (and the new version doesn’t lend itself to being known by its intials…EMN!).

It’s a good point about the amount, and cost of curtailment, and I agree that batteries are not the way forward for large-scale energy storage. I’ve quoted Euan Mearn’s analysis on this before, highlighting that if nothing else, there would be insufficient land mass available to house the necessary Li-ion batteries. I suspect the thinking at the moment is to use these surpluses for hydrogen production rather than direct electricity storage, but I’m far from persuaded that a switch to hydrogen is either desirable or feasible.

The use of interconnectors is also contentious: we can’t necessarily import when we need to (or it forces NG ESO into off-market high price trades in order to secure flows), and then we can be importing at the same time as curtailing wind, or exporting while simulanously running coal. It’s what happens when you mix “free” market behaviours with high levels of policy intervention.

NG ESO is about to publish the FES costings, so there’s going to be a lot more to say about that in the next month or so….

I still think that “homes” is enormously misleading. I’ve seen it defined as anywhere between 2.5 and 4.2MWh p.a. IIRC (and that’s ignoring the much larger statistical range in consumption between parsimonious homes and profligate ones), and it ignores non domestic use of electricity anyway. There are good statistics you can use here:

https://www.gov.uk/government/statistics/electricity-section-5-energy-trends

the .ods spreadsheet has the virtue of having all the tables in one file, and it allows you to look at demand segments if you wish.

I agree with your conclusions about hydrogen: every time I look at it, intermittency, long storage periods for seasonal and inter year balancing and huge swings in output (do you provide electrolysis for the few hours when the system is generating close to capacity, or do you curtail anyway?) kill the economics even more stone dead. Even SMR and CCS seems a pointless expense, and far from guaranteed to be useable anyway.

I’ve done various bits of work looking at the possibilities for cross border balancing. This chart shows the high degree of correlation at the hourly level for wind generation between the countries at the heart of Europe:

https://datawrapper.dwcdn.net/tn541/1/

and this one shows daily totals of wind generation (so already some smoothing from shorter term storage is implied):

https://datawrapper.dwcdn.net/QcA5c/1/

As wind generation capacity increases, these shortages and surpluses will amplify, also creating significant problems for grid stability.

FES costings – now that will be interesting – and probably full of holes.

Ignoring the proposed link to Iceland, the only interconnector project that makes any sense when weather correlation is taken into account is the one with Norway. All the others share the issues that weather is highly correlated so many of the demand (and now generation output) drivers are the same. Although there is probably a second order effect due to the fact everyone else also wants to be interconnected with the Norwegian hydro system.

Connecting with France makes the least sense from a diversification perspective since the French electricity system is more highly temperature sensitive than ours due to the low penetration of gas heating. Proponents of the electrification of heating should take note of this, and we don’t have anything like the storage capacity the French market has in the form of its hydro resources.

The other big issue with cross-border balancing is the fact the TSOs game the system by discovering internal network constraints that limit cross-border capacity when they see domestic tightness, thereby making sure they’re not exporting at times of high domestic demand.

Timeta has an interesting blog outlining plans for subsidising electrolysis, although they don’t call it that of course. Rigged markets all the way, so the consumer pays: no-one would invest otherwise.

https://timera-energy.com/building-a-hydrogen-electrolyser-investment-case/

I’ll be interested to read their follow-up, but I can’t see that the overall system realities of intermittent and sometimes massive surpluses can possibly be avoided.

Of course, the electrolysers will need subsidising, as will the CCS for hydrogen from methane, as will new hydrogen-fired gas generation, and you can also expect domestic hydrogen appliances to require subsidies otherwise millions of consumers would be left without the means of heating and cooking overnight when (if) the switchover happens.

The idea that subsidised assets then get to play in balancing and ancillary services markets is also unfair, but is the case already, it’s just a question of level: when just about every energy asset is in receipt of some form of subsidy the idea of properly functioning markets is long gone. I do wonder whether Brexit will mean the pretence of running free energy markets will be dropped at some point.

I can’t help wondering where all the money for these subsidies is supposed to come from given the fact we’ve broken the bank on covid….

I was following up some technology and found that thermal energystorage is in favour for both nuclear (paper at mit.edu) and wind (Siemens Gamesa) . The latter has developed an electric heating variant used for driving a steam turbine. I suspect that the two technologies would use storage differently to gain commercial (power market) advantage. The nuclear thermal storage would be integral with the power station but the electric heating (wind) variant not necessarily.

The technology is immature only allowing for about 10hrs of storage and being focussed on lower temperature (steam) electricity generation.

However I am not sure how (relatively) long term storage is viewed by OFGEM and, more importantly how it is valued (and would fit into the market, if it is not integrated with the generator source). It should be notes that if Siemens raise the temperature of their storage then they could use it to drive a gas/steam combined cycle – with significantly improved conversion efficiencies (and energy storage capacity)