Last week, National Grid outlined its plans for it system operator business, following the decision by Ofgem last year that greater separation of this activity was needed from the rest of the National Grid business in order to better manage conflicts of interest.

“Our long-term vision is for an Electricity System Operator (ESO) that thinks across networks, plays a more active part in the energy system and helps to shape frameworks for markets,”

– National Grid

National Grid describes its main ESO roles as:

- Managing system balancing and operability

- Facilitating competitive markets

- Facilitating whole system outcomes

- Supporting competition in networks

“Our aim is to join up network design and operation processes across transmission and distribution to ensure the most efficient decisions are made across all networks, accelerating connection timescales and reducing the investment needed in networks counterparties.”

National Grid’s ESO roadmap sets out its plans to achieve this based on a set of 7 principles (see below). The main elements in practice are around improving information provided to the market, improving access to the transmission system, and improving system security planning processes.

Providing better quality market information is at the heart of the new plan

As the electricity system is de-carbonised through the introduction of increasing amounts of intermittent generation, the costs of balancing the transmission system are rising. National Grid intends to improve the accuracy of its Day Ahead transmission demand forecasts to allow market participants to better adjust their generation/consumption positions ahead of real time. This would reduce the need for balancing actions by the control centre – National Grid estimates that a sustained reduction in the daily demand forecasting error of 10 MW could result in a £20 million reduction in the annual cost of balancing the system.

National Grid also intends to improve its BSUoS (Balancing Services Use of System) charges, moving from monthly to half-hourly resolution, published at the Day Ahead. This will be challenging, since half-hourly BSUoS is impacted by many external factors such as weather conditions, network and plant availability, as well as the complex interplay between the forecast and market behaviour.

Once the model is in production, National Grid will analyse the drivers of the change in BSUoS, and, since the accuracy of the forecast will be affected by changes in the behaviour of market participants in response to the forecast, there will be no accuracy performance measures.

National Grid will publish other market indicators, such as the carbon intensity of GB electricity generation, to allow the market to react to information on the progress being made towards clean growth targets. More information will be provided on National Grid’s procurement decisions, as well as performance metrics relating to balancing costs. This metric will incorporate a forward view of significant cost drivers, and the likely cost range.

The benchmark for expected balancing costs will be derived from 5-year moving averages of historic balancing costs (excluding black start and Supplemental Balancing Reserve), beginning with the rolling mean for 2010/11-2014/15. The forecast baseline balancing cost for 2017/18 would be £960.2 million on this measure. National Grid expects the 2018/19 baseline benchmark to be £998.6 million, but this will be recalculated after the end of the current electricity year.

The foreseeable cost drivers for 2018/19 are expected to be primarily:

- The full commissioning of the Western Link high voltage DC transmission project, which should have a downward effect on costs.

- Managing summer minimum demand periods where high renewable output creates additional costs for managing system inertia. This is likely to have an upward effect on costs.

- Impact on balancing costs where higher renewable penetration impacts the revenues of thermal or contestable plant. National Grid expects to see an increase in some elements of service pricing if revenues become increasingly constrained.

The over-arching theme points to a desire to increase engagement with market participants with a view to holding down costs by enabling more targeted decision-making.

Transmission system development under pressure

National Grid’s system operator plan came a couple of weeks after Ofgem’s announcement that it was minded to use a “competition proxy” approach for delivering the upgraded high-voltage transmission system link for Hinkley Point C, known as the Hinkley-Seabank project (“HSB”). In March last year, National Grid submitted its economic case for the £840 million project, however, Ofgem is challenging around 20% of the proposed costs, particularly in relation to the treatment of how severe weather could delay construction of the grid upgrades, and believes potential benefits will be driven primarily by lower costs of financing for HSB than under the status quo RIIO arrangements.

“We are still of the view that it is not appropriate for high impact low probability risks such as extreme weather to be funded in full up-front, particularly where we consider the methodology for estimating probability and cost could be more robust. As set out in our minded-to consultation on the delivery model for HSB, we propose that if delivery of HSB is funded through a Competition Proxy model, contingency funding for this sort of risk will not be included in the up-front allowance.

Efficient costs will instead be determined via a post-construction review. As such, we do not expect to provide upfront funding to mitigate extreme weather risk. If extreme weather does occur, at the end of construction we will review the impact it has had on construction, the efficiency of NGET’s mitigations and response, and the efficiency of the resulting costs. From this assessment, we would adjust NGET’s revenue allowance accordingly.”

Under the Competition Proxy model, National Grid would deliver the project, with Ofgem setting revenue terms intended to reflect the outcome of an efficient competitive process for the financing, construction and operation of the project. The project would attract a lower rate of return than is generally available under RIIO, reflecting the savings seem on offshore wind connections where competitive tenders have driven down costs.

National Grid has responded that Ofgem’s approach does not reflect the costs of financing and its estimate of £100 million in savings to consumers was too high.

National Grid’s changing role presents risks both to its investors and the wider market

Although these two stories relate to two different, and now formally separate parts of National Grid’s business they are indicative of a new direction for networks in the GB market, and a more robust regulatory environment. The RIIO framework has been criticised for being overly generous, with network companies earning double-digit returns, and the next price control period is expected to be significantly tighter.

The tightening trend is reflected in Ofgem’s position on the HSB project. Transmission costs have been falling for the connection of offshore wind facilities, and Ofgem sees an opportunity to secure similar savings onshore. At the same time, Ofgem is enforcing a separation of National Grid’s system operation activities from the rest of its business, to limit the effect of conflicts of interest.

The tightening trend is reflected in Ofgem’s position on the HSB project. Transmission costs have been falling for the connection of offshore wind facilities, and Ofgem sees an opportunity to secure similar savings onshore. At the same time, Ofgem is enforcing a separation of National Grid’s system operation activities from the rest of its business, to limit the effect of conflicts of interest.

National Grid’s role is becoming significantly harder technically, and it is facing pressure to do more with less, which should come as no surprise, with the growing political pressures around rising bills. The vision it sets out in its ESO plan to play a more active role in the system and help “shape frameworks for the market” is a move in the right direction, but it will take bold thinking and ambition to translate this sentiment into real leadership on the ground…something not typically seen in regulated utilities.

Arguably, as a private company, it should not fall to National Grid to take on the role of redesigning the operation and function of the transmission system. The regulated utility model works best in stable, predictable markets, with innovations being directed towards improved delivery.

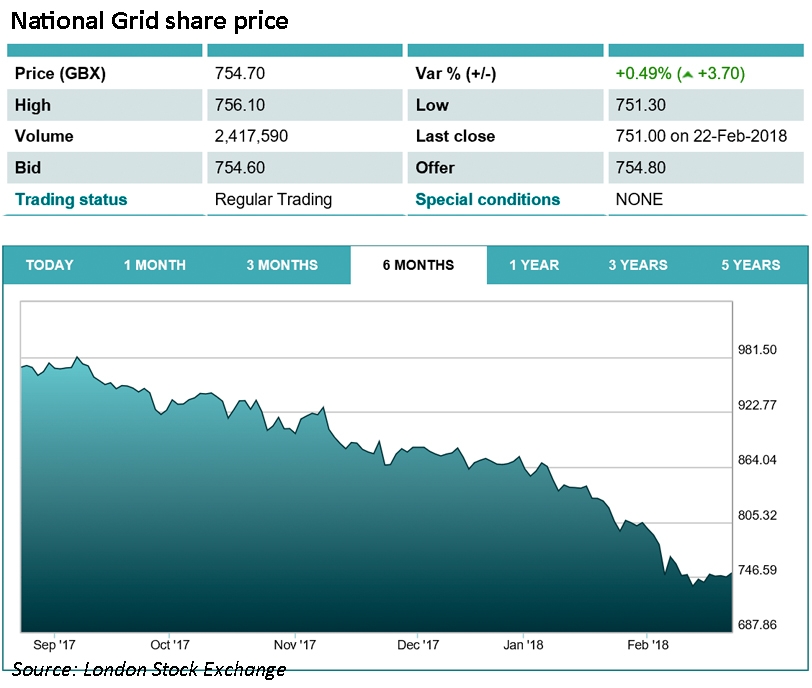

National Grid is being expected to lead fundamental structural changes in the electricity sector, in the context of growing unease over the costs of the transition, whilst balancing the legitimate interests of its shareholders against the demands imposed by policy changes. It is no wonder that its share price is suffering, and further headwinds are to be expected – the risks are high, while the rewards are diminishing.

“As the electricity system is de-carbonised through the introduction of increasing amounts of intermittent generation,”

Of course the $64,000 question is how much intermittent renewable generation IS decarbonising generation and how much the intermittency is actually leading to an INCREASE in carbon emissions as gas sets ramp up and down madly, and coal sets are kept on hot standby, ready to cover for the shortfalls in ‘renewable’ energy production.

The only real metric is to look for overall reductions in fossil fuel burnt per unit electricity generated globally, as renewable energy usage rises.

To date the data suggest that the impact is simply one of increased cost: specific global emissions by the electricity sector remain broadly unchanged, whilst the energy and emissions costs of building renewable energy solutions have risen with its adoption.

That’s the first question. I have a couple more:

Even if we de-carbonise locally there is a global impact? Even if there is, will it make any difference to climate change!

We’re spending ££££ on a big series of IFs.

“The only real metric is to look for overall reductions in fossil fuel burnt per unit electricity generated globally, as renewable energy usage rises.”

Leo,

I’ve told you before… stop using sense & logic in engineering, it only spoils the dream.

Now I must go & help the fairies feed the unicorns