A year ago I set out my key themes for 2017, and as predictions go it was definitely a mixed bag! In this post I review the key themes of 2017 and look forward to the current year.

What didn’t really happen in 2017…

# Creation of an Independent System Operator

In January, Ofgem and the Government announced plans to create greater separation between the system operator role part of National Grid and the rest of the group. In August, following an industry-wide consultation, the plans were confirmed, with National Grid being required to separate its system operator function with a separate Board, licence, staff and offices. The new entity will be called National Grid Electricity System Operator and should be up and running by April 2019.

Ofgem received 39 responses to its consultation, and found widespread support for the proposed separation measures, although a number of respondents believed the proposals did not go far enough and called for a full ‘hard’ separation of the SO function.

“There was general support amongst the Big Six and the suppliers that responded, for the proposed separation measures, with a small number of these calling for even harder separation measures than proposed. Similarly, DNOs and companies operating across generation and transmission all supported greater separation measures….

However, views on which aspects of separation should be harder varied amongst respondents. Some stakeholders felt that a separate office location, rather than physical separation on the same site, was important. Others felt that there should be minimal or no shared services and some expressed support for separate branding between the ESO and the rest of NG. There was a general recognition that harder separation would ultimately increase costs for consumers, although this was viewed by some as justified to ensure the ESO’s independence,”

– Ofgem decision paper

This topic has attracted some strong feelings. It may go quiet for a while, but I would not be at all surprised if the question of full independence for the SO does not appear again at some point.

# Capacity market

2017 was in fact a quiet year for the capacity market. The early capacity auction held in February to replace the Supplemental Balancing Reserve for 2017/18 cleared below expectations. The T-4 auctions due to be held in December were delayed until February, while the next T-1 auction will begin on 18 January.

# Investment landscape

The year opened with fairly negative investment news that saw clean energy investments in Q1 17 17% down on the previous year, although some of this reflected falling costs rather than sentiment. Later in the year there was considerable interest in US transmission assets, indicating some preference by investors for the regulated end of the sector. Renewables are still seen as having investment potential, but so far, returns have been modest, and the risk of regulatory change makes picking winners challenging. This didn’t emerge as a particular theme in 2017, and that probably won’t change this year.

…on the other hand I was right about…

# New rules for battery storage

A range of regulatory changes is in the pipeline for battery storage, including the introduction of a clear regulatory definition for storage, the removal of double-counting of final consumption levies, restrictions on DNOs operating storage, changes in capacity market de-rating factors, and changes to the RO regime where storage is co-located with renewable generation. Impending changes to balancing and ancillary services markets will also impact battery storage, and the environment for batteries may well become more challenging in the coming year.

# Curtailment of embedded benefits

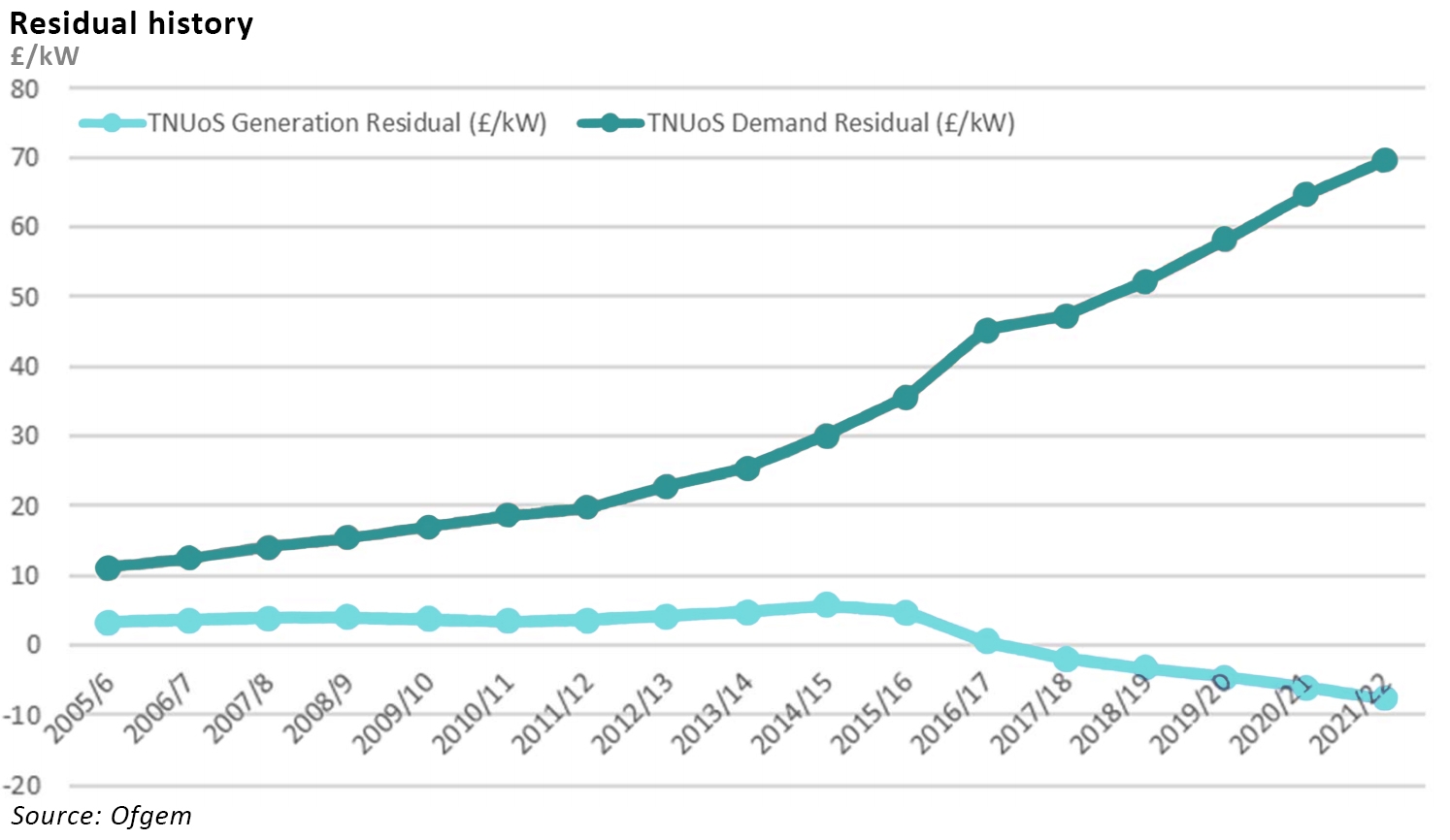

The anticipated changes to the embedded benefits regime did indeed materialise in June, meaning that the method by which the demand residual component (“TDR”) of Transmission Network Use of System charges will be based on gross rather than net demand. As a result, the value of embedded generation which reduces net demand on the transmission system, will be reduced, with the changes due to be phased in from this April.

However Ofgem’s decision is subject to a judicial review, on the basis that the applicants believe the decision breaches the directly applicable EU law principle of non-discrimination by treating embedded generators like large transmission-connected generators and differently from demand-side response providers and “behind-the-meter” generators; the decision is legally flawed by reason of failure to take account of material considerations/facts; and the decision is irrational. Ofgem intends to defend its decision in the court case which is expected to be heard early in 2018.

While arguments may be made that there were flaws in Ofgem’s decision-making process, Ofgem’s conclusions that the charging regime was distorting the markets were sound. Embedded generation does not reduce the historic costs of the transmission system that are recovered through TDR, and therefore it is not economically sound for net demand to be used as the basis for the recovery of this particular cost. However, as the legal arguments may well focus on technicalities, it cannot be assumed that Ofgem will win its case – in that event though it would not be surprising to see further reforms being proposed, as these benefits do not have a sound economic basis.

# Nuclear developments

The picture for nuclear in the GB market did change quite a bit in 2017. The failure of Westinghouse in March put the Moorside project into jeopardy, while the Advanced Boiling Water Reactor planned for Wylfa Newydd passed the Generic Design Assessment stage in December, increasing the chances it will come online in 2025.

Across the Channel, French nuclear regulator the ASN finally reached a decision on the compromised steel in the Flamanville reactor vessel – the bottom section of the pressure vessel has been deemed acceptable for use, albeit with additional monitoring, and the containment lid may enter service in 2018 as planned, but must be replaced no later than the end of 2024 (as the manufacturing process for a containment lid is around seven years).

There has been widespread criticism of Hinkley Point C, and in particular the Government’s decision-making processes which have been deemed to be flawed in respect of value for money considerations. Questions continue to be asked about the chosen EPR technology, with some experts being recently quoted as doubting whether it will ever be successful:

“It’s three times over cost and three times over time where it’s been built in Finland and France. This is a failed and failing reactor,”

– Paul Dorfman, UCL Energy Institute

2018 may see the start of Taishan 1 – which would be the first EPR to enter service. Neither Flamanville nor Olkiluoto are expected to open before 2019.

# Prices and volatility

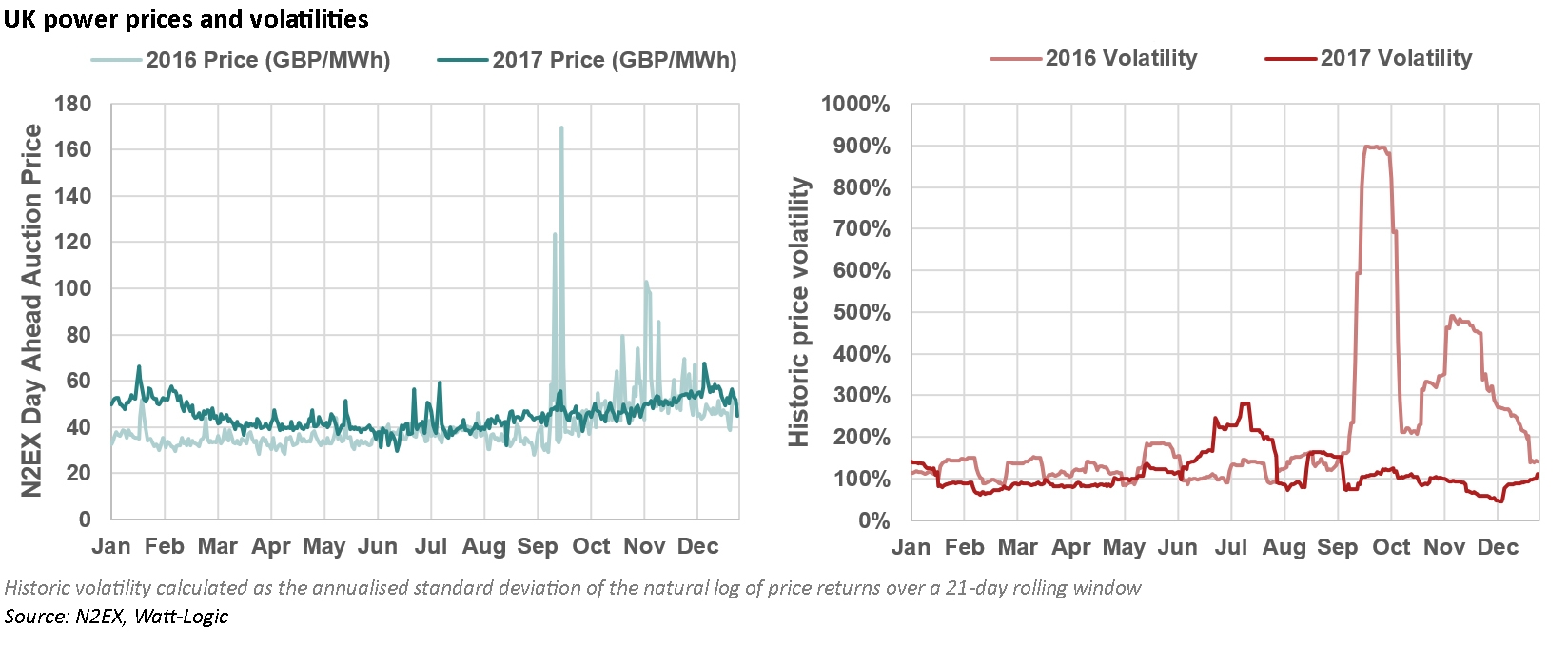

On the back of the collapse of GB Energy in November 2016, I anticipated ongoing volatility to stress smaller retail players. In the event although prices in 2017 were higher in general than in 2016, they were less spiky and less volatile.

The real story on price in 2017 was the proposed retail price cap. This is now continuing its legislative path and will continue to be a theme over the coming year.

Looking back over the past year, the main themes were the thorny issue of retail price caps, the transition of DNOs to DSOs, the impact of falling costs for a range of technologies central to de-carbonisation (batteries, wind, and solar), development of new nuclear, and changes to transmission both in terms of charging and balancing services.

Looking ahead to 2018

Some of the key themes from last year will inevitably continue to hit the news in 2018, in particular retail price caps and the new nuclear projects. Other areas I think may well see some prominence in the coming year include further changes to the operation of and charging for the transmission system; the impact of new digital technologies on the sector, particularly blockchain; and a slowing of the development of new battery storage as revenue models face strain. 2018 could also be an interesting year for the gas markets, with recent news on hydrogen, as well as changes in global market structures.

# Retail price cap

The Draft Domestic Gas and Electricity (Tariff Cap) Bill was published on 12 October and is now undergoing pre-legislative scrutiny, with hearings before the BEIS House of Commons Committee.

The Government has been forced to admit that the proposal could damage retail competition, while the large energy companies argue that other initiatives such as the smart meter roll-out will suffer as a result. However, consumer groups and MPs remain in favour of a cap, to protect the public from perceived profiteering by large suppliers.

This whole policy is based on fundamental misconceptions about the levels of profit being earned by the large energy companies. Should a cap be implemented at the levels necessary to remove the claimed £1.4 billion of excess profits from the sector, the impact on suppliers will be dramatic and highly negative for consumers.

Eliminating the profit margins of the large energy suppliers is neither sensible or sustainable, and policy-makers would do well to remember that the listed energy companies are FTSE-100 members and widely held by pension funds. Destroying the value of these companies will do more than hurt a few “fat cats”.

This topic is definitely going to continue to make headlines in 2018.

# Nuclear developments

Another of 2017’s themes that will continue to make news in 2018 is around the development of next-generation nuclear technologies in the GB market. A spate of announcements in December seemed positive for the sector: the GDA approval for Wylfa Newydd, the emergence of South Korean utility KEPCO as preferred bidder for the Moorside project, and funding for a new competition for the development of advanced nuclear technologies, including Small Modular Reactors (“SMRs”).

The SMR news is not as positive as it first looks, since the Government announced that the previously launched SMR competition from March 2016 was now closed, and was essentially just an information-gathering exercise. The amounts available under the new competition are also very small, and a wide range of technologies is eligible to apply, leaving many in the sector feeling frustrated and essentially short-changed by the process.

At the same time the Government published its long-awaited Techno-Economic Assessment of SMRs, which included analysis from EY indicating SMRs would be 30% more expensive to build than traditional scale reactors. This goes some way to explaining the Government’s hesitation to commit more meaningful funding, and also the long delay in publishing this analysis (the EY report is dated March 2016!).

# Transmission system

In December, National Grid published its response to the System Needs and Product Strategy consultation it ran earlier in the year. The product roadmap covers frequency response, with a further roadmap for reactive power, black start and constraint management expected in Q1. The highlights of the roadmap include:

- standardising existing products (Firm Frequency Response, Short Term Operating Reserve, Fast Reserve) to deliver greater transparency;

- introducing a set of faster-acting response products;

- delivering a trial of closer to real-time procurement using a pay as clear mechanism; and

- reviewing balancing and ancillary services contracts and clauses to reduce barriers to entry.

National Grid is implementing changes not only to rationalise its product suite, but also to make the procurement process more transparent. Contract terms and durations will be standardised, bundling of products will be avoided where possible, and exclusivity clauses reviewed to make revenue stacking easier.

These changes will not all happen at once, and further plans are due to be published in the coming months, meaning that system operation will continue to be an important theme over the coming year. In addition, Ofgem will soon launch a consultation on the new RIIO price control framework, while the outcome of the embedded benefits judicial review will also be keenly anticipated.

# Digital technologies

Big data is starting to change the shape of the energy sector, and this trend is set to continue, particularly in demand-side response (“DSR”), where granular usage data from individual components can be aggregated to inform companies about how they can flex their consumption to save money and benefit from DSR services.

Another “hot” technology area that may impact the energy sector in 2018 is blockchain. 2017 saw the technology behind bitcoin used in the financial services sector for a wide range of transaction types, particularly trade finance, and it also has a number of potential applications in energy. In the near term, blockchain could make supplier switching faster and cheaper for consumers, while longer-term, peer-to-peer trading platforms could emerge allowing even small consumers/”prosumers” (consumers who also have some production capability) to transact small volumes directly with each other. A pilot project for this purpose is currently underway in Australia.

BP and Shell are developing a blockchain based energy trading platform in conjunction with a group of banks and commodity traders, and trials for blockchain use in energy are underway around the world, so this may well be the year that blockchain makes its mark in the energy sector.

# Battery storage

2017 was a hot year for battery storage, with costs falling and project sizes growing, most notably with the “giant” 100 MW Tesla project in South Australia. As noted above, battery storage projects have faced regulatory change in a number of respects and this change is likely to continue in 2018, with possibly less favourable outcomes.

National Grid’s rationalisation of balancing and ancillary services will be positive in some respects, particularly if revenue stacking is made easier, but the market for these services is limited meaning a growing number of projects will be chasing a modest revenue pool. This is likely to depress prices, which will be good for consumers but challenging for developers. Alongside this, capacity market revenues are also set to fall after lower de-rating factors for batteries were announced in December.

# Evolution of gas markets

There has been a growing trend towards greater hub-indexation for gas pricing. Last year saw some movement in the long-running dispute between the EU and Russian gas producer Gazprom in relation to pricing. European buyers have argued in recent years that the traditional oil-indexed pricing basis in long-term gas supply agreements meant they were over-paying for gas, since hub prices were lower. Gas hubs have become more numerous and far more liquid since many of the Gazprom agreements were first agreed, and the rationale for oil-based pricing has significantly reduced. In 2017, Gazprom agreed to more hub-indexation.

Similar trends towards hub-based pricing are also emerging in LNG, particularly in the context of destination-flexible and shorter-term or spot contracts. China is expected to become a major LNG buyer in 2018, while Japanese demand will fall as its nuclear plants begin to come back online after a long shutdown due to concerns arising from the Fukushima disaster. Otherwise the LNG market is not expecting to see major changes in 2018.

There continues to be interest in hydrogen as a possible solution to the de-carbonisation of heating in the UK. Northern Gas Networks is exploring the feasibility of converting the entire gas network to hydrogen, starting with an initial pilot in Leeds but while an initial feasibility study was promising, the success of the scheme in de-carbonisation terms depends on a viable carbon capture and storage technology which is so far not available. However the scheme was awarded £9 million in funding by Ofgem in December. Across the Pennines, another trial in Manchester and Liverpool will look at supplying pure hydrogen for industrial users, and hydrogen blended with methane for domestic use.

Whether these trials come to anything remains to be seen, but it feels as if gas may be a hotter topic in 2018 than it was last year.

Finally, Brexit deserves a mention. Last year I suggested that Brexit would not be a key theme for 2017 in the energy markets, and I think that was broadly right. There were some discussions around Euratom, but overall, Brexit was not as important in the energy markets as other topics. This will change as the 2019 leaving date comes closer, and we may well start to see much more movement on the impact of Brexit on the sector in the second half of the year.

Whatever happens, my concluding comment from last year’s post still holds…. there will almost certainly be some surprises!

Leave A Comment