The market has been waiting with bated breath for Ofgem’s decision on its proposed changes to the embedded benefit regime, since its statement in March that it was “minded to” implement a change to the CUSC that would limit the demand residual (“TDR”) component of Transmission Network Use of System (“TNUoS”) payments to embedded generators to around £2 /kW, down from current levels of £45 /kW.

TNUoS charges for both demand and generation consist of two elements:

- The locational element – a forward-looking locational signal that should broadly reflect the costs and benefits to the transmission system of embedded generation and transmission-connected generation in different locations; and

- The residual element – used to recover the remaining costs of the transmission network, which are largely fixed and sunk costs, as well as some additional costs such as network innovation funding.

Ofgem believes that the current level of rewards paid to embedded generators on the basis that they reduce the requirement for transmission infrastructure is beyond what is justified by the value they bring, particularly in the context of the backward-looking residual component.

“We consider that the current methodology results in a payments to smaller EG of around £370m/year from consumers to smaller EG, a figure that without reform, is forecast to rise to around £700m/year by 2020/21. Further, there is evidence that TDR payments to smaller EG are distorting markets, including the Capacity Market (CM), wholesale and ancillary services markets.”

Ofgem has rejected proposals for grandfathering arrangements on the basis that it would create a significant new distortion between existing and new capacity as well as preventing further changes to the charging arrangements for those network users for 10-15 years. However, Ofgem has agreed that the changes should be phased in over the three years from 2018-2020, allowing time for investors and generators to adapt their despatch and business models, and giving time for Ofgem to carry out its planned Targeted Charging Review, which will take a wider look at transmission charging.

Distorting effects of the current charging model

Historically, total transmission charges were lower and there were fewer embedded generators, however as the energy transition progresses, both the amount of transmission costs to be recovered through the TDR as increased as well as the amount of embedded generation. As a result, significant payments are now available to smaller embedded generation which is not available either to transmission-connected plant or embedded generators which are larger than 100 MW.

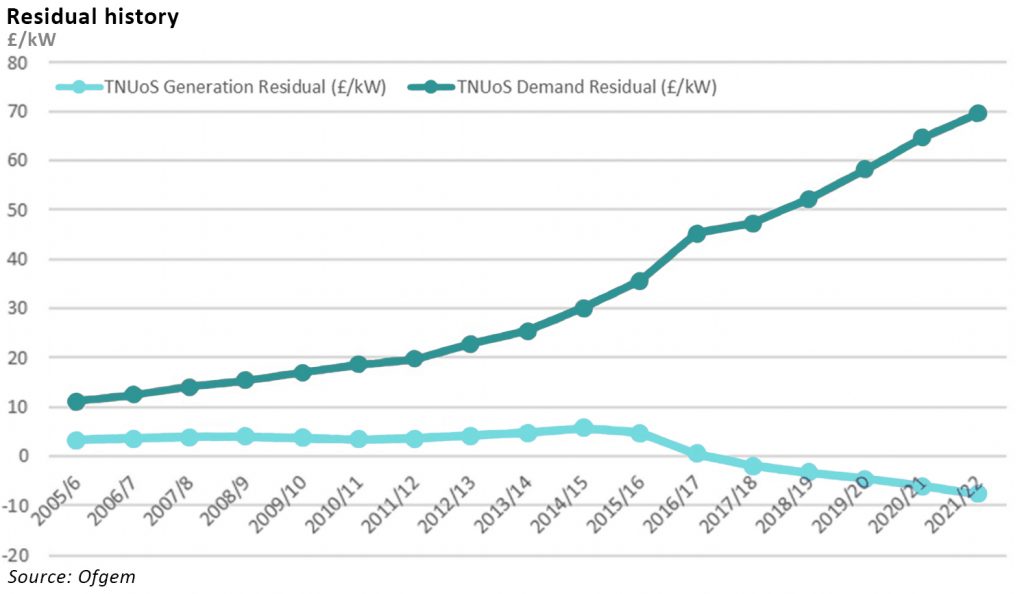

The TDR payment is currently around £47.30 /kW and is predicted to rise to £69.59 /kW in 2021/22. This compares with Capacity Market payments which are in the region of £20 /kW. These payments provide a strong incentive for smaller generators to connect to distribution networks rather than the transmission system, and mean that transmission costs must be recovered over a smaller charging base, which in turn increases the level of the TDR charge. It also increases costs to consumers as suppliers pass on the cost of these benefits to their customers.

The method by which the residual transmission costs are recovered is based on the net amount of power drawn from the transmission network by suppliers during the triad periods (see the box below). The contribution of embedded generation counts as negative demand, reducing the supplier’s share of this TDR charge, however as the triad periods cannot be forecast with complete certainty, embedded generators are often incentivised to generate in 25 or more periods in order to hit the triads. Furthermore, the use or otherwise of embedded generation has no impact on the amount of cost that National Grid must recover through the TDR charge, so the cost of incentivising embedded generation to run during triad periods is entirely additive.

Ofgem believes this process has the following distorting effects, leading to higher consumer costs overall, as TDR payments are additional costs and these incentives might push more efficient generators out of the market, as well as creating conditions for sub-optimal investments in generation and network capacity:

- Wholesale price: by running out of merit during peak times due to the TDR payments, smaller generators cause demand to be artificially dampened at peak times, hence distorting wholesale market prices;

- The Capacity Market: smaller embedded generators have a competitive advantage when bidding into the Capacity Market since their ability to earn TDR revenues allows them to reducing their possible bid prices;

- Dispatch: increasing amounts of smaller embedded generators run out of merit to ensure they hit the triad periods;

- Inefficient investment in generation capacity: the TDR represents a financial incentive to build generation that may not have otherwise been economically viable, and to locate generation on the distribution system even when this would not otherwise be the most efficient place to locate;

- Ancillary Services: smaller embedded generators may be at a competitive advantage in the ancillary services market, as the TDR allows them to price more competitively.

Impact of the cut

There is currently around 30 GW of generation connected at the distribution level, with diesel and small gas plant primarily benefiting from the TDR payments, which together account for about a third of all embedded generation. However some renewable generators believe they will be impacted by the cuts to the TDR benefit. Ecotricity said its 24 distribution-connected wind farms would lose 11-12% of their annual profits following the move and Vattenfall has estimated the benefit accounts for around 5% of its revenues.

Ofgem believes that while some embedded generation projects may now be cancelled, security of supply will not be impacted, however there are some developers who are considering giving up their capacity contracts given the loss of TDR income. Agora Energy Research estimates that up to half of the 2.2 GW of peaking plants that won new-build contracts in the first two auctions could give up their 15-year agreements. This capacity may need to be replaced in the 1-year capacity auctions.

“I know that a lot of these projects are being touted around the industry for sale. The investors I’ve spoken to have said that most of them ‘just don’t work’ – in other words, you can’t get a positive internal rate of return with any sensible assumptions. There is a strong risk the owners of these ‘options’ – they are not yet projects – just pay the penalty [for non-delivery] and move on,”

– Dan Roberts, energy director at Frontier Economics.

Consultancy firms Frontier Economics and LCP predict the reduction of the TDR benefit will signal a change in market economics to favour new CCGTs – of the 25 GW of new-build capacity contracts they expect to see between 2022 and 2034, the majority will go to CCGTs, with reciprocating engines securing less than 1 GW of the total.

Aurora Energy Research sees things differently, predicting that there is only about 3-5 GW of capacity that could be filled by CCGTs in the late 2020s, because much of the capacity that will be contracted through the Capacity Market will have load factors below 15%, at which level CCGTs are uncompetitive against small peaking units. Tom Edwards, a senior consultant at Cornwall Energy agrees:

“Why would you invest in a big power station … when you could invest in a smaller plant which is more efficient when running at low load factors, …can react quicker and can stack revenues. They’ve more flexibility to either earn money from ancillary services, the wholesale market or embedded benefits. Reciprocating engines aren’t going to go away, even after this change.”

The government continues to have a preference for CCGTs, so it will be interesting to see if in a post-Brexit world, changes to state-aid rules would lead to direct subsidies to CCGTs to guarantee their economics against other forms of generation. The government is also still considering other actions to deter dirtier forms of embedded generation, in particular diesel engines, so the outcomes are far from clear at this point.

It is likely though, that the value of the TDR payments will find its way back into wholesale market prices through the removal of the distortions mentioned above, and into higher Capacity Market prices as the absence of TDR income will mean embedded generators will need to bid at higher levels to recover their economics.

Industry reaction reveals spilt between “traditional” and “newer” generators

Ofgem’s “minded to” statement in March garnered negative reactions from the renewables lobby. The Renewable Energy Association reportedly claimed that the decision showed that renewable energy was once again “in the firing line”. The final decision by Ofgem has been greeted with similar levels of concern. According to Jonathan Marshall, energy analyst at the Energy and Climate Intelligence Unit:

“This backwards step from Ofgem will directly hit small and flexible power stations, exactly the sort needed in the UK to keep the grid balanced and ticking over as we generate more and more power from renewable sources. Rather than looking to the future where the electricity system is decentralised, democratised and decarbonised, this ruling will play into the hands of the Bix Six, who have long been lobbying against progressive changes.

By turning its back on the power system of the future, Ofgem’s decision is likely to add to energy bills and could force planned projects to be cancelled – undoing technological progress from recent years that has kept the lights on and ensured costs stay low. As the rest of the world moves away from large, centralised power stations, this decision will see us lose ground on rival nations, with ramifications spreading through the whole economy.”

This view however flies in the face of the facts: the UK does not have low electricity prices – it has very high electricity prices, and recent technological progress has only been enabled by the use of expensive subsidies. It’s also pretty unclear how this rivalry with other nations manifests itself in this context – although the negative impact on the whole economy of high prices due to a combination of subsidies and network expansion to accommodate renewables is all too clear.

Some commentators have levelled their criticism at the size of these growing network costs, suggesting they may be excessive. This is entirely possible – as I have noted previously, National Grid is incentivised to build and operate transmission capacity, some of which would not be required if there was a greater role played by turndown/turnup DSR. But even if the costs could be lower, it is unlikely they could be reduced to levels that removed the distorting effects of the TDR payments, and presumably if they did then the generators that currently rely on these payments would still find their economics challenged.

There was also significant criticism of the decision-making process, with many embedded generators feeling they were structurally cut out of a process designed around transmission-connected generation. Mark Draper, chairman of the Flexible Generation Group summed up the complaints:

“We have repeatedly raised our concerns that Ofgem’s current governance structures give large energy firms undue influence over the reform process and changes in regulation. The decision makers on the Connection and Use of System Code (CUSC) panel overwhelmingly represent companies, including EDF Energy, SSE, Scottish Power and Uniper, which will benefit from what is being proposed. It is their recommendations which Ofgem has endorsed in its ruling.

Small generators and new entrants have no representation on this panel, despite requests to have their voices heard and interests represented. This decision – and its timing – reinforces in the minds of many that the large power generators wield excessive and undue influence within Ofgem’s regulatory processes.”

On the other hand, owners of larger transmission-connected were positive about the move:

“We welcome the announcement from Ofgem as we believe that reducing embedded benefits in this way creates a more level playing field for all generators, reduces distortion in the market, and also delivers a good result for the consumer. The working group which looked at possible changes to embedded generation benefits reflected a wide range of industry views, with two thirds of the members representing small, embedded generation interests. The process took almost six months,”

– Felix Lerch, UK chairman, Uniper.

Clearly, there is some consensus among generators that the winners from Ofgem’s decision will be large transmission-connected generators, but this is likely to favour existing plant rather than provide an incentive for new CCGTs, absent other regulatory interventions. It seems unlikely, however, that consumers will see any great benefit, as both wholesale electricity prices and Capacity Market prices will adjust to the removal of the distorting effect of the TDR payments. For the required generation capacity to be present in the market, sufficient rates of return must be earned one way or another.

That being said, removal of some of the distorting influences in the market is a positive step, allowing investor behaviour to be better aligned with policy objectives, but the market is plagued with many other distorting factors. The challenge is that achieving the dual goals of de-carbonisation and security of supply is expensive, and economically inefficient, leading to the requirement for a complex set of direct and indirect subsidies. Therefore to the extent that de-carbonisation continues to dominate the energy agenda, affordability will be difficult to achieve and consumers will continue to suffer from high prices.

Usual toys out of the pram from the rent seeking renewable sector when someone threatens to take their sweeties away