I’m writing this in the middle of the night during a business trip to the US, so it feels appropriate that the line “miles to go before I sleep” by American poet Robert Frost is ringing in my ears – a line that captures not just my late-night writing, but also the fatigue induced by yet another baffling intervention by the British state into markets it insists are working perfectly well. A shorter version of this post appeared in UnHerd on Sunday.

Government takes a little stake in big software company

Last week, the Government announced it was taking an equity stake in Kraken Technologies, the software platform being spun out of Octopus Energy. £25 million of public money, we are told, will “help the company scale up and become a UK champion”. Yet the same press release tells us that Kraken already serves 70 million customers accounts across four continents and is a “powerhouse”, which rather begs the question of why it needs public money at all.

At the end of December it was announced that Octopus Energy raised US$ 1 billion in Kraken’s first standalone funding round, valuing the business at US$ 8.65 billion. Interestingly the Kraken company press release quotes all the figures in US dollars – curious for a UK based business that reports in sterling. The round was led by D1 Capital Partners, alongside other new investors such as Fidelity International, Durable Capital Partners and Ontario Teachers’ Pension Plan Board.

The valuation already looks stretched – according to the Financial Times, Kraken has been priced at “17 times contracted annual revenue of $500mn, many knots ahead of its peer group”, and notes that software-as-a-service (“SaaS”) companies have performed poorly recently.

The Kraken 2025 accounts (covering the 9 months to 31 January 2025) also show a marked shift versus the prior year…revenue was up (c £164 million for 9 months vs £143 million for the prior year), but administrative expenses jumped significantly as Kraken went from a healthy prior-year operating profit to roughly break-even operating profit, and then into a pre-tax loss (the finance expense was material). The net loss for the 9 months to 31 January 2025 was £2.7 million versus a profit of £17.4 million in the 12 months to 30 April 2024.

In other words Kraken delivered revenue growth but at the cost of margin compression. Much of the public commentary still treats Kraken as a highly profitable, high-margin SaaS business throwing off cash. The accounts show something closer to an enterprise platform business investing heavily and carrying real cost of growth.

The British Business Bank appears to have invested after this round so will have had to go in at the same or higher valuation.

Governments usually nationalise or invest for one of two reasons: to bail out failing firms whose collapse would be catastrophic – the banks in 2008 – or to fund projects that cannot otherwise attract capital, either because they are so capital-intensive that private markets cannot bear the risk, or because they are highly speculative but potentially transformative, such as early-stage nuclear fusion.

Kraken fits neither category. It’s already scaled, already global, and already profitable (despite the loss in the most recent reporting period). If it genuinely needed growth capital, private investors would be queueing up, particularly given the current appetite for energy-adjacent technology. So what, exactly, is the taxpayer buying?

The Government’s announcement is conspicuously vague…we’re not told the valuation at which the stake is being taken, nor whether the Government’s stake is being taken before or after the December funding round or ahead the mooted IPO (“initial public offering” or first listing of shares on a stock exchange) which may come in the next few months. We are told only that Kraken “may” list in London, a market struggling to attract new listings, implying that the Government’s involvement may somehow influence that choice.

That seems fanciful – £25 million is not serious money at Kraken’s scale, with an implied valuation of over £6 billion. On those numbers, the Government’s stake would amount to 0.04%, nowhere near enough to force strategic outcomes. If the objective is to secure a London listing rather than New York, this is an odd way to go about it.

Kraken announced its December funding round in USD and speaks increasingly of growth in the US, operating in a sector where US markets typically deliver higher valuations and deeper liquidity. This would tend to make a US listing more likely, and a tiny bit of cash from the UK Government isn’t going to change the decision either way.

More baffling still is the claim that Kraken needs help to “scale”. Kraken is already large enough to introduce concentration risk into the UK’s energy retail and flexibility ecosystem, increasingly sitting at the centre of billing, demand response, time-of-use pricing and consumer data flows. This is not a plucky start-up; it’s established market infrastructure.

Trying to understand the Kraken and Octopus capital structures

Kraken was 100% owned by Octopus Energy Group Limited (“OEGL”) prior to the December transaction. As a result, in all of the accounts we currently have for either company, Kraken is fully consolidated into Octopus. Media reports following the funding round state that “Octopus Energy will retain a 13.7% stake in Kraken following the spin-out, while Origin’s interest in Kraken remains at 22.7%”.

We also know from the Kraken press release that: “This round sees new and existing investors acquiring c. $1bn of Kraken equity to fund both Octopus and Kraken. Investors led by Octopus Capital are also injecting a further $320m into Octopus for innovation and growth. Collectively, these almost double Octopus Energy Group’s already strong balance sheet. After the split, Octopus will retain a 13.7% stake in Kraken.”

This is difficult to reconcile with the current Companies House filings, which still show OEGL owning more than 75% of Kraken Technologies Limited. It is possible that the relevant documents have been filed but are sitting in a Companies House processing queue and have not yet appeared on the public register. However, if OEGL genuinely still owns more than 75% of Kraken, then this cannot really be described as a de-merger in any legal or accounting sense. In theory, Octopus’s economic interest in Kraken could have been diluted through the issuance of preference shares or similar instruments while retaining legal control, but that would be an odd structure given the clear intention to pursue an IPO: any such economic-legal mismatch would need to be unwound ahead of listing in any case.

The comment about Origin Energy’s stake is particularly interesting. Back in 2023, I tried to establish who ultimately owns Octopus Energy, and the trail quickly runs cold at Companies House. OEGL is 25–50% owned by Octopus Energy HoldCo Limited, which is itself more than 75% owned by Oe Holdco Limited, an entity with no person with significant control.

This is what I wrote in 2023: “According to data held at Companies House, Octopus Energy Limited has one “person” with significant control: Octopus Energy Group Limited which owns more than 75% of the company. Octopus Energy Group Limited in turn has one person with control, holding between 25% and 50% of the shares: Octopus Energy HoldCo Limited. In the past, this entity listed Keith Jackson and James Edison as having between 25-50% of the shares. Octopus Energy HoldCo Limited has one entity with more than 75% of its shares: Oe Holdings Limited, a company which was only incorporated in March 2022, which filed two different sets of governance documents (Memorandum and Articles of Association) during 2022. Oe Holdings Limited has no person with significant control.” So this is essentially unchanged since then.

At the time, Greg Jackson said that the ultimate shareholders remained unchanged following the corporate restructuring. According to the OEGL accounts, shareholders at 30 April 2022 were:

- Octopus Energy HoldCo Ltd (39.07%)

- Octopus Capital Ltd (0.58%)

- Origin Energy International Holding Pty Ltd (16.49%)

- Tokyo Gas UK Ltd (7.48%)

- GIM Willow (Scotland) LP (8.97%)

- CPP Investment Board (2.99%)

- and management and employees via Octopus Nominees Ltd (24.4%)

However the notes to the 2025 accounts tell us:

- Octopus Energy HoldCo Ltd (30.07%)

- OE Holdco Ltd (0.16%)

- Origin Energy International Holding Pty Ltd (22.18%)

- Tokyo Gas UK Ltd (10.02%)

- GIM Willow (Scotland) LP (12.78%)

- CPP Investment Board (12.31%)

- Galvanize Innovation & Expansion Fund I LP (0.25%)

- Lightrock Climate Impact Fund SCSP (0.41%)

- and management and employees via Octopus Nominees Ltd (9.82%)

In 2023 the management and employees sold more than half of their holdings. The press report that Origin has 22.7% in Kraken is not entirely consistent with this. It was perfectly consistent with the 19.28% OEGL stake it had in 2023 (19.28% held directly plus 19.28% of the OEGL share of 13.7%) so perhaps the press report referenced an out of date figure. My guess is that Kraken has been economically de-merged from OEGL, with shares allocated between OEGL and its shareholders, on a broadly pro-rata basis reflecting their economic interests in OEGL, and that the relevant filings are simply not yet available on Companies House.

I have asked both Kraken and Octopus to clarify, and I will continue to monitor the Companies House filings. The current picture is more ambiguous than one would normally expect for a transaction of this scale, unless this is simply a case of filing and publication delays.

Owner Octopus Energy needs the Kraken proceeds to meet regulatory capital requirements

For years, Octopus was loss-making, surviving only because its shareholders repeatedly provided fresh capital. The obvious question was always why those shareholders tolerated persistent losses, and the answer was Kraken, the jewel in the Octopus crown. The energy supply arm absorbed losses while the software platform quietly embedded itself across the market.

Several developments now bring this into sharper focus. In March, Ofgem announced tougher capital requirements to ensure suppliers do not collapse and leave consumers to pick up the bill. The requirement is to hold £115 of Adjusted Net Assets per dual-fuel customer where Adjusted Net Assets are defined as net assets excluding intangibles and permitted alternative capital.

So “Net assets” in the statutory accounts are not the same thing as Ofgem capital – if a supplier’s balance sheet is meaningfully composed of goodwill, customer acquisition intangibles, capitalised software and right-of-use assets then statutory equity can look strong while Ofgem capital is tight. Also, growth can worsen the capital position even if the business is operationally fine, because the requirement scales with customer numbers – a supplier that is “short” can get more short by adding customers.

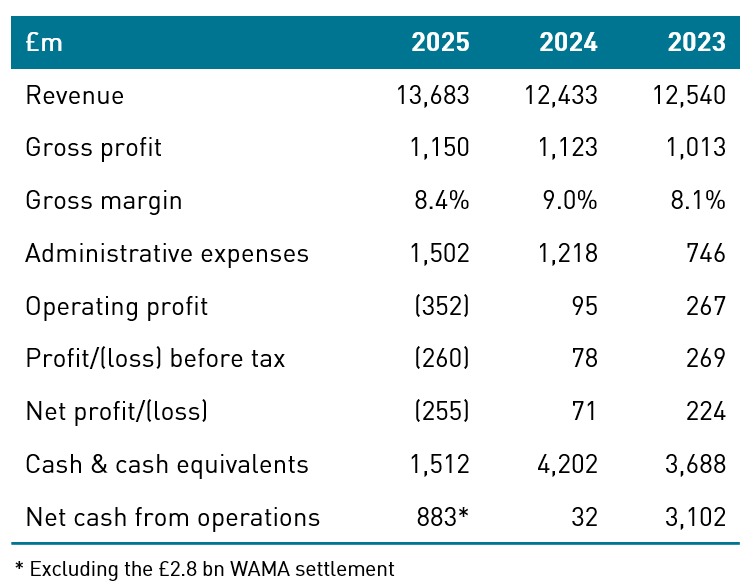

Based on its customer numbers at the end of April 2025, Octopus was required to hold around £875 million in net assets excluding intangibles – almost exactly the amount it reported in its 2025 accounts published earlier this month. It is one of three suppliers failing to comply with the new regulatory capital requirement.

In July, the Government announced it was abandoning plans for zonal pricing, something Octopus chief executive Greg Jackson had lobbied hard to achieve. That same month, Centrica chief executive Chris O’Shea said Octopus was more than £1 billion short of its regulatory capital requirement and should be prevented from taking on new customers. Since then, Octopus’s capital requirement has risen again, to almost £1.5 billion, driven by rapid customer growth.

In September, the de-merger of Kraken was announced.

The Octopus Energy accounts published in January, covering the year to April 2025, make sobering reading. After earning profits of £203 million in 2023 and £83 million in 2024, Octopus swung firmly back into the red, recording a loss of £255 million. Net assets stood at £1.4 billion, but included £600 million of intangibles which do not count towards regulatory capital, much of it attributable to Kraken, leaving Octopus hundreds of millions of pounds short of the capital it is required to hold.

Selling Kraken converts those intangibles into cash that can be counted as regulatory capital but only once Kraken is genuinely separated and the proceeds are not themselves encumbered, and because the sale price will almost certainly exceed book value, it neatly solves the capital problem. What happens to the remaining proceeds will be revealing. If they are paid out to shareholders as dividends, serious questions will arise about their long-term commitment to the supply business once the valuable software arm has been sold.

Although Ofgem’s capital requirement applies at the supply company level, Octopus Energy Ltd has always relied on group support from OEGL in the same way British Gas relies on Centrica, making the group balance sheet the economically relevant unit of analysis.

Octopus Energy doesn’t look that great, even with Kraken on its books

Doing a deep dive into the information published about Octopus Energy and Kraken on Companies House tells an interesting story. Despite the hype, Octopus is not a consistently profitable business nor is it generating large amounts of cash. The past year has been particularly difficult, with a significant amount of financial engineering to boost liquidity, changes in accounting principles to improve the numbers, and going concern disclosures that smack of protesting too much.

What stands out is that the accounts are full of items that change the apparent economics without changing the underlying cash reality: classification tweaks, settlement-related items, and “underlying” definitions that can move the goalposts. If a business is genuinely comfortably capitalised and liquid, it doesn’t need to spend so much narrative effort on reconciling away from the statutory result.

Taken together, the OEGL accounts for 2023, 2024 and 2025 describe a group that has grown extremely quickly, but whose financial profile is still dominated by volatility, working-capital effects and accounting judgement rather than stable, repeatable profitability. Revenue growth is strong, but margins remain thin and costs have risen faster than profit. Administrative expenses went from around 5.9% of revenue in 2023 to around 11.0% in 2025. That’s a big jump.

2025 included a one-off £2.8 billion payment of the “WAMA” in relation to the Bulb transaction. Amusingly, a Google search of “Octopus” and “WAMA” yields lots of results about a ban on octopus farming in Washington State. This WAMA is much more mundane: it’s a Wholesale Adjustment Mechanism that arose from the Bulb Special Administration and transfer to Octopus.

When Bulb collapsed, its wholesale hedging position, price-cap assumptions and actual realised wholesale costs did not align, so rather than crystallising everything at the point of transfer, the Government and the Special Administrator put in place post-transfer reconciliation mechanisms. These ensured that Octopus was not taking on open-ended wholesale risk it did not create, while taxpayers and consumers ultimately bore the difference in a controlled way. I’m sure they also care a lot about cephalopod welfare!

One notable feature period is the growing importance of working capital and timing effects. Customer credit balances, regulatory cashflows and hedging collateral all move materially year to year, which means headline profitability is a poor guide to underlying cash generation. The group has also made changes to accounting policies and presentation over time, which generally have the effect of smoothing volatility and improving comparability, but also make it harder to tell whether losses are genuinely “one-off” or structural. While management commentary frequently points to weather or temporary factors, the persistence of losses and balance-sheet pressure suggests this is more about the business model than isolated events.

OEGL 2025 gross profit was £1,149.9 million, while Kraken’s 9-month gross profit to 31 January 2025 was £116.3 million, roughly 10% of OEGL’s full-year gross profit, even before estimating the missing 3 months. So Kraken is not the whole group story by any means, but it’s also not trivial, and is a meaningful contributor to gross profit quality.

OEGL’s 2025 operating loss was £352.1 million while Kraken made an operating profit of £0.6 million for 9 months so Kraken isn’t what’s driving the group loss. And in terms of net cash flows from operations, OEGL was £883 million (excluding the one-off WAMA settlement) while Kraken was positive £52.5 million over the 9 months. However, OEGL’s operating cash flows were entirely due to movements in working capital: trade and other payables increased by £724.9 million and provisions and accruals increased by £370.3 million, ie £1,095.2 million in total. The negative working-capital contributors were an increase in trade and other receivables of £127.1 million and an increase in inventory of £159.3 million, together negative £286.4 million giving a net working capital effect of £808.8 million.

The increase in payables and accruals indicates that OEGL has successfully pushed cash outflows forward, but the size is significant. Cash generation in 2025 was driven almost entirely by deferral of cash outflows rather than underlying profitability. This represents working-capital dependence rather than self-funding operations.

In terms of funding, the accounts do not show a steady accumulation of retained earnings. Instead, balance-sheet strength has depended on periodic injections of new capital and the use of financing structures rather than organic cash generation. That context matters when interpreting later claims about balance-sheet resilience.

One final point from the OEGL accounts is worth highlighting. The group issued substantial new equity in the years when it reported profits – £297.7 million in 2023 and £615.5 million in 2024 – but no new equity at all in 2025, the year in which OEGL reported a £255 million loss. Perhaps shareholder support was forthcoming when the group could still plausibly present itself as profitable and scaling, but not when losses widened materially.

This does not prove that shareholders have “drawn a line”, but it does indicate that fresh equity is not being injected automatically to offset losses, as it had been in the past, and that balance-sheet resilience increasingly depends on structural actions (such as asset separation, secured financing and working-capital management) rather than open-ended shareholder funding.

Between 2021 and 2024, OEGL absorbed £1.56 billion of shareholder capital, while remaining loss-making for much of that period, including losses of £64.7 million in 2021 and £141.0 million in 2022. The scale and persistence of these injections suggest that shareholder funding has been structural rather than exceptional, raising legitimate questions about the sustainability of the business model once investor appetite or tolerance changes.

Taken together with the apparent economic de-merger of Kraken, this strengthens the interpretation that risk is being consciously separated: Kraken is being positioned as a growth platform with its own capital base and investor constituency, while OEGL is left to stand on the economics of retail supply, its residual 13.7% stake in Kraken, and whatever additional support its shareholders are willing – or unwilling – to provide going forward.

Charges over assets throw some big red flags

There are multiple charges over both OEGL’s and Kraken’s assets registered with Companies House. These include for OEGL:

- Shell Energy Europe Ltd (created 20/07/2023): fixed charge and negative pledge

- HSBC Bank plc (created 29/06/2023): explicitly “security over cash deposits”

- BNP Paribas London Branch (created 06/02/2024): fixed charge and negative pledge

- Shell Energy Europe Ltd (created 30/09/2024): fixed charge and negative pledge

- GLAS SAS (created 07/11/2024): fixed charge and negative pledge

- Uniper Global Commodities SE (created 11/12/2025): fixed charge and negative pledge

- NatWest as Security Trustee x2 (created 09/01/2026): fixed charge and negative pledge. The security is over OEGL’s shares in Kraken Technologies Ltd with Kraken as the Collateral Company and Guarantor. These support letter of credit and revolving credit facilities and explicitly use Kraken to back OEGL liquidity

Kraken Technologies Ltd:

- NatWest as Security Trustee (created 09/01/2026): fixed and floating charge over “all the property or undertaking”, plus negative pledge

On their own, these can be framed as normal treasury operations, securing cash deposits, posting collateral to major counterparties, and setting up security trustee structures for facilities. But the sequencing and the counterparties (Shell/Uniper with security over cash deposits and later security-trustee structures) reads like an organisation actively widening its access to liquidity, which is consistent with a retail supply /trading profile where collateral, margining and credit support can swing significantly. In the context of the 2025 accounts, with its large loss and heavy working capital management, this looks less like optimisation and more like pulling every available lever to keep liquidity and credit lines open.

The NatWest charges are particularly interesting. Kraken is now providing collateral and acting as guarantor for OEGL’s liquidity facilities – like a Parent Company Guarantee in reverse because OEGL is the “parent” (albeit with a greatly reduce stake in Kraken). This is something of a red flag since OEGL’s credit providers clearly view the Kraken subsidiary as being economically stronger and require it to underwrite the weaker parent’s debt. While not unprecedented, this is an unusual configuration and typically signals that lenders view the operating group as materially dependent on the subsidiary’s credit strength.

OEGL now owns only 13.7% of Kraken, but effectively all of Kraken’s equity and assets are being put at risk to support OEGL’s liquidity facilities, and this was required immediately after the demerger – the demerger documents have yet to be filed but here we have the lender insisting that its credit support is perfected on credit lines that were not drawn or only lightly drawn at the last Balance Sheet date (of course they may have been drawn in the meantime).

This is not a durable situation because it means that the new majority shareholders in Kraken after the demerger and December financing round are bearing risk for a company they do not control, ie OEGL, and OEGL is relying on an asset it mostly no longer owns to remain bankable. This is tolerable only as a temporary transitional structure, or a bridge pending full separation, noting that Kraken and OEGL still share many shareholders in common, but presumably not all, since new investors entered the Kraken capital in December.

Before Kraken can list, all upstream guarantees must be terminated, as no listed company can credibly guarantee the debts of a former parent / affiliate retail supplier, and all share pledges must be released. It is not possible to IPO a company whose shares are encumbered to support third-party debt. Kraken lenders must be structurally senior to OEGL lenders as any residual intercreditor contamination would be fatal to the equity story. Any prospectus would have to disclose this history in detail, which is another reason this structure cannot persist.

So one of two things must occur before IPO: OEGL refinances on a standalone basis, without Kraken support, or OEGL downsizes, de-levers, or receives explicit shareholder support to replace Kraken.

Putting the pieces together, OEGL has persistent losses, heavy reliance on working-capital deferral, no new equity in 2025 for the first time in years, and now only a minority stake in its most valuable asset, with banks unwilling to rely on OEGL alone.

Going concern statements fail to reassure

Which brings me on to the going concern statements in the OEGL 2025 accounts. The way Octopus addresses the issue of being a going concern is interesting. If we look at Centrica plc, previously the largest energy supplier in Britain, it makes the following concern disclosures in the annual report…

“Accounting standards require that Directors satisfy themselves that it is reasonable for them to conclude whether it is appropriate to prepare the financial statements on a going concern basis. The Group’s business activities, together with factors that are likely to affect its future development and position, are set out in the Group Chief Executive’s Statement on pages 7 to 10 and the Business Reviews on pages 33 to 37. After making enquiries, the Board has a reasonable expectation that Centrica and the Group as a whole have adequate resources to continue in operational existence and meet their liabilities as they fall due, for the foreseeable future.

For this reason, the Board continues to adopt the going concern basis in preparing the financial statements.

Additionally, the Directors’ Viability Disclosure, which assesses the prospects for the Group over a longer period than the 12 months required for the going concern assessment, is set out on pages 52 to 53. Further details of the Group’s liquidity position are provided in notes 25 and S3 to the financial statements on pages 225 to 228 and 244 to 250.”

All very standard stuff – there’s a requirement for company directors to satisfy themselves that the company is a going concern (ie likely to be able to meet all its financial obligations and remain in business for at least the next 12 months), so Centrica’s directors simply say they looked into it and are satisfied.

Octopus however says the following, and it repeats this entire section twice in its annual report:

“The financial statements have been prepared on a going concern basis which the Directors consider to be appropriate for the following reasons.

The Directors have assessed the liquidity of the business through a detailed going concern forecast and in particular considered the associated hedge position required, which in the UK is procured through a third party without collateral requirements, with a similar arrangement introduced for the European operations. This also includes consideration of commitments by Octopus Energy Group to fund international operations and committed acquisitions when applicable, together with any actions required to ensure compliance with the capital floor requirements of Ofgem’s financial resilience requirements for UK suppliers.

The Group held cash of £1,512m at 30 April 2025. There are significant peaks and troughs through the year with April generally the low point of the cash flow cycle. On the basis of existing funding previously received from shareholders, along with ongoing available facilities and trading lines, the forecast cash flows show headroom through the going concern period even under stressed conditions reflecting reasonable sensitivities identified including cold winter scenarios as noted below.

The general approach to hedging expected supply requirements is set out on page 22, along with consideration of the Group’s principal risks and uncertainties including increased risks from ongoing cost of living challenges. The Group assembles a set of sophisticated financial forecasting models from key divisions which it tracks and calibrates carefully based on actual performance. The largest cash flow movements are driven by the energy supply business and this forecasting includes consideration of changes in both the hedge book and forward wholesale market prices.

Existing and new regulatory requirements arising over the period have been considered, and assumptions of increased customer gains and losses (together with increased numbers of fixed price contracts) included. The Directors have also actively considered downside sensitivities of cash flows from operations including that which would arise from a cold winter and some associated higher pricing. The Directors have evaluated risks based on historical weather data, which is used to model a range of increased consumption that could arise from an unusual, sustained cold winter during a winter month over the forecast period.

The Group has previously received equity injections as well as access to financing through committed loans from banks, trading counterparties and cash generated by other Group businesses. The business also continues to actively consider further investments and regularly reviews options for additional working capital or other facilities or equity injections although the going concern position does not assume these additional sources of capital in the forecasts. Corporate investment across the Group and acquisition activity is continually monitored to reflect the economic and regulatory environment.

Following the detailed process above the Directors have a reasonable expectation that the Group will have sufficient funds to continue to meet its liabilities as they fall due for at least 12 months from the date of approval of the financial statements and consequently have prepared the financial statements on a going concern basis.”

So we have Centrica essentially saying: “We have to do this assessment because the standards say we must. We looked. We’re fine. If you’re curious, here are three places with more detail.” It is short, boring and confident to the point of being almost dismissive, which is exactly what a genuinely robust going-concern statement looks like.

Octopus, by contrast, says something very different. Its directors emphasise that they have modelled everything: cold winter scenarios, hedging arrangements, reliance on third-party counterparties, trading lines, shareholder support, European operations, regulatory capital floors, stress scenarios, sensitivities, forecasts and liquidity models. That is not reassurance, it’s defensive over-explanation. And to anyone who regularly reads accounts, it immediately raises the question of whether the business is closer to its constraints than the directors would like to admit.

Overall, do I think Octopus will fail within the next 12 months? No, and on that narrow basis it can reasonably be considered a going concern. But do I think this is a robust business with a secure long-term financial footing? Much less so, particularly given the clear lack of confidence its lenders have in it. And that matters because Octopus is now the UK’s largest energy supplier. If it were to fail, the consequences would dwarf those of Bulb, whose collapse required an expensive and disruptive Special Administration regime. When a company reaches this scale, “probably fine for the next year” is not a sufficient standard. Which is why Ofgem now requires regulatory capital and why Octopus’s failure to have it is all the more worrying.

Bad optics makes the BBB stake even more baffling

As a final kicker, there are also unresolved governance questions around the Government stake in Kraken. Greg Jackson sits on the Cabinet Office board and on the Industrial Strategy Advisory Council, both of which provide strategic input to the Government. While this does not imply impropriety, the optics are uncomfortable: the state is taking an equity stake in a business being sold by a government adviser, whose other business appears to be struggling to meet regulatory obligations.

Jackson has strong ties to the governing Labour Party, and was once head of the LabourList, which describes itself as “leading dedicated forum for authoritative news, insightful analysis and robust debate about the Labour Party across the UK”. Jackson appears to have the ear of Ed Miliband, unlike Ineos CEO, Jim Ratcliffe, who has complained about a lack of access despite operating vital energy infrastructure including the important Forties pipeline.

Business Secretary, Peter Kyle insisted to the Financial Times that the investment is “not a bung” but acknowledged it was part of efforts to keep the company in the UK. The very use of such language indicates that the Government is aware that this looks bad. How much worse will it look if the company lists in the US after all?

Public money is supposed to address market failure, but the only market failure here is Octopus’s regulatory capital position, a problem it can solve perfectly well by selling Kraken, and its shaky credit profile. So why is the Government buying a stake in an already successful software business, and what exactly is it getting for our money?

.

There are still miles to go before I sleep, because this whole can of worms is keeping me awake – and it should keep everyone else awake too.

Thank you for this, I hope managed to get some decent rest!

As an Octopus customer, this does explain their recent message informing me that they would increase my direct debit by £20. I’m well in credit for at least February. Octopus does ‘bill’ monthly unlike British Gas which is quarterly and very confusing. Despite trying to reduce my consumption, there was a deeper cold spell in December in the Midlands which continued in January. However usage should peak in January and normally drops to three quarters in February. They didn’t get more money from me, but I assume other customers are more malleable. It’s odd when their practice of monthly billing keeps their accounts more clear that their monetary obligations are worse.

Interesting- what is the government buying with their (our!) £25M? I was until recently a customer of Octopus, not by choice but due to being shovelled in with them after the collapse of Avro. As a chartered chemical engineer I know how many beans make five. I had repeated battles with Octopus, who kept trying to increase my monthly charges by too much. After a particularly egregious case I had had enough & moved to another supplier. This was not for better rates, as there is no working market any more in utilities, but to get away from their ‘customer service’. I think they are using inaccurate software tools to maximise their income, which require the intervention of a human to correct the issue. It is refreshing to see a deep, measured analysis such as this & most welcome.

This is a sorry tale and frankly one which I don’t fully understand. Worryingly, it paints a picture of what could be described as deliberate deceipt. I wonder whether this sort of thing is going on in other industries.

US markets value SaaS software companies significantly more highly than London does and there is a wider research community to provide coverage and position the company among a panel of “comps”. Not that much “tech” listed on London at least as a % of the market relative to NASDAQ and NYSE. Seems worthwhile for a small ticket (on which money will probably be made) to try and retain the listing business for London (which will have wider benefits in showing London as still a viable listing location for largish tech). However, whether one can compete with 15x revs, I doubt because London investors prefer earnings or EBITDA to revs multiples.

Chapeau! You are a forensic accountant and a power systems engineer rolled into one; I thought I was smart being just a one-time electrical engineer. Thanks for this – I’ve always thought Octopus was fishy and Labour’s donation confirms it.

Thank you for this detailed and worrying analysis, Kathryn.

Yes, I am an Octopus customer and had built up a large credit balance and their fabulous AI driven Kraken software was saying DD should stay at £90pm. I went through all the bills for the past 12 months, gas and electricity (import and export) and showed that £30pm would cover it, and a human agreed (when I could get a reply) and repaid my credit so I will be in debit for the next 3 months and clear it all over the summer.

I have had solar panels for 7 years now and a Tesla battery for almost 2. I fill that up every night at the cheap Flux rate and then sell it back at the peak rate. That’s in winter months – in the other 8 I only do that if there’s no sun forecast for the next day, so I make a profit of around £350pa on electricity which covers half of my gas bill (and then there’s £240 of FIT income too). This only works for us as a retired couple with no EV or heavy appliances who can do washing and dishwashing when sun shines and who live in a relatively small decently insulated house. YMMV. Yes I know I had a big capital outlay, but it will be repaid well within 10 years for each and I have the security of full home backup when we get the Millibandouts.

I have 35+ years of experience in IT and my estimate of their systems are, to use a technical term, crap. I assume this is the customer facing part of their vaunted Kraken system.

They regularly lose billing data – most notably in August 2024 which I only noticed in October in the Octopus Watch app (OW – highly recommended) which shows your Octopus usage, gas and elec. by day on your phone or smart watch. The developer sent me this:

“What happened in August is that an employee made a well-meaning but problematic change to the internal code. The intention was that “if there is no data, do not store it in the API”. That makes sense, of course. However, in some programming languages—and I know that Octopus Energy uses this language—there is sometimes no distinction between “missing” and 0. This created the whole situation: your import meter was using 0 kWh, so the code on their end assumed that the data was missing, so it wasn’t stored in the API. These kind of bugs can be hard to spot and many people were still on leave at that time so it took two weeks for Octopus Energy to finally spot the issue.

Octopus Energy has tried to fix the missing data a total of 3 times. Each time they believed it was fixed for everyone, and each time there were still users who complained that there was data missing. This situation is weird: how can Octopus Energy think it is fixed when users still notice missing data? I suspect—based on everyone I am helping with this issue—that the fix from Octopus Energy sometimes writes the data to the API, only for it to then be erased later again due to the original bug. This situation has been going on continuously.”

There have been other instances of missing data shown in OW that I managed to resolve by directly contacting the tech. expert I learned about in that first occurrence.

The most recent occurrence was Nov and Dec last year when they failed to collect smart meter data. I have an ongoing formal complaint with them about this. The person I am in touch with admitted:

“Unfortunately this feature is not computer automated yet in terms of one notifying us [that DCC is missing data] or two estimating a piece of half hourly data. The process at the moment is to bill around the missing data and if we cannot retrospectively draw the data, bill you to a standard variable tariff aka the Flexible Octopus Tariff.

We are actively working on creating a computer automated process for both of the aforementioned issues however this does unfortunately take time.”

As a result my bills for the last 2 months have been sent multiple times, with lots of credits and debits and recalculations which might be easy for an AI to understand, but are a nightmare for the average consumer.

What I really want is a bill for both gas and electricity (import and export) on the 1st of each month, but that hasn’t happened since July once they’d finally sorted out my Flux account properly (which took 3 months). The missing data maybe explains last month, but not the others. One of the comments was that “this software is still in Beta” ! Is that what Kraken customers are buying ?

They still have no explanation for the earlier month failures, or that the process when DCC don’t send data is the problem and have offered my a 2nd generation meter as the fix.

Apart from the software, they are totally understaffed in Customer Service. Their target for responses to problems is 2 working days, but they rarely meet that ime. Once you are in touch with someone they can usually resolve the problem, but they are all obviously overworked and hence slow to respond.

Words fail me.

A Kraken’ tale! They reported over £100m of losses because of the sunny spring. Having gone after customers with solar panels to be green they were caught out overhedging at the temporarily higher prices for spring delivery during the previous winter. Customer demand was sharply lower than expected because they were using their own solar. Moreover, export volumes under the generous Solar Export Guarantee tariff soared, but this and overhedged purchases faced resale in day ahead markets at prices that were low or negative, caused by solar surpluses.

The above was meant to be a reply to Julie Cutler.

Thanks Kathryn for your excellent but rather scary analyis, but for reasons outlined it does not surprise me.

I know this much:

• Kraken violates RFC5322 (the Internet standard defining email format) and §2.1.1 specifically (maximum line length). I wonder what other shortcuts lie hidden in Kraken’s code base.

• Emailing their Data Protection Officer (who appears not to be one single, named person, not in practice, at least) is routed through Kraken _and_ there are inadequate or possibly no access limitations over who can see those emails, so far as I am in a position to determine. I consider this unprofessional, at best, and negligent disregard for consumer privacy at worst.

• Octopus wants £250 even just to register a non-MCS export MPAN, whether or not they enrol you into an export tariff. They are, shall we say, economical with the truth about their reasons. They blame regulations but refuse to quote the relevant sections of the SLCs or other applicable codes, blame the DCC and so forth. The truth turns out to be “company policy”, ie a voluntary decision which, of course, they will not justify.

They are, or were, an otherwise good company let down by poor quality management.

Well done for this work. We are indebted to you for your knowledge and understanding. As an Octopus customer who assumed they were the best for my energy supplies I now consider whether to change to an alternative.

Thanks

If you are an Octopus customer, get in touch with customer service and ask them to switch you to a flexible direct debit and pay in arrears. I.e. pay for just what you use each month, after you have used it. You will no longer be subsidising them. Your bills will have more ups and downs, which you’ll need to budget for, but over a year you will be better off because you will be earning the interest if you have the spare cash rather than Octopus.

I helped a bit with the overnight unravel. It’s a very complex tale. Among the things I found was the establishment of a new entity, Kraken Holdco, which owns the beneficial interest in Kraken Technologies. It’s evidently a vehicle for the demerger that needs separate monitoring.

Also, I checked on the OFGEM regulated subsidiaries, which are Octopus Energy Ltd (not OEGL), and the companies that cover the business acquisitions of Bulb and Shell Energy Retail which are subsidiaries of OEL, and Octopus Energy Trading, which used to be an OEL subsidiary, but was transferred to direct ownership by OEGL in 2024. Removing the highly volatile, collateral intensive trading operation from OEL is financial engineering designed to evade OFGEM capital requirements. New accounts for the trading entity are due real soon now, and may be quite revealing.

OEGL reports capital injections of £500m to OEL and £387.5m to the trading entity, doubtless to try to satisfy the OFGEM capital requirements. The OEL one shows up in their balance sheet, comprising most of shareholders funds.

OEGL has over 3 pages of subsidiaries listed in note 12 to its accounts, some overseas. Guessing which are material, and which are being used to hide problems away reminds me of trying to disentangle Enron’s accounting structure looking for “cookie jars” before they went bankrupt. The realities of others observing Enron making loss making trades were more reliable. So I take Centrica’s comments seriously.

There are two areas that merit further investigation. Some of their investments in wind farms seem to have been less successful. Also, they have a rapidly expanding business in leasing out EVs, which appears to pass on residual value risk to a special purpose vehicle (not an EV!) which could blow up in their faces as another major source of loss.

Thanks for sharing your insight, Kathryn.

Very informative.

Where there’s smoke… This is one to watch and make sure it gets on the radar of opposition parties. Of course the regulator would see no conflict of interest.

OfGem is as unfit for purpose as Octopus is financially dubious and their customer service found wanting. It’s such a pity. Their customer service used to be pretty good, but no more.

To be fair, OfCom is little better. It’s just a reflection of general dysfunction across public- and private-sector institutions.

Very interesting analysis. It does beggar believe that the government is taking stakes in such companies. The figures for the % were out though, it is a 0.4% stake, not 0.04% but either is pretty immaterial. Great British Energy does seem to be predominantly a PR exercise rather than a serious investment fund.

Really appreciate the clarity and depth of analysis.

It will be very interesting to see these accounts for Octopus Energy Trading Ltd., filed at the last moment,when they are published

https://find-and-update.company-information.service.gov.uk/company/09263368/filing-history

These accounts are now published, and it turns out that this is only a small scale operation mainly involved in trading leased BESS capacity in short term markets with a turnover of only £15.7m. A minnow trying to learn through doing that made a £3m net loss: they made a gross profit from charging and discharging and perhaps ancillary services, but the lease payments overwhelmed it.

As someone who has used Kraken, and other similar systems, I can tell you that it’s not the game changer they make it out to be and there a lot off major problems – for instance, Octopus and other suppliers who use Kraken such as E.On Next and EDF currently have a major problem with double billing & Kraken don’t seem to be able to fix it. The only thing Octopus & Kraken are the best at is self promotion & congratulations

Excellent, thanks Kathryn.

Hi Kathryn

thanks for your analysis of the Octopus group

I agree their most recent accounts look pretty tricky – I would guess that this group would be a nightmare to audit

What struck me was that their Octopus Energy supplied customers increased by 25% and revenue only 10%; gross profit has barely moved in absolute terms and decreased from 9% to 8.4% spite of the increase in customer base; and admin costs have increased by 23%, perhaps partly the result of increased numbers of customers to integrate and manage; the combination of the small increase in gross profit and significant increase in admin costs has been the major cause of the move from break even to £254m loss

I have never seen an audit report that listed in detail the steps taken to verify the move of the accounting system from Aqilla to Netsuite; such moves are hardly unusual, but clearly Deloittes had sufficient concern about the transfer that they saw fit detail out the steps they took and the checks they made; they must have had major concerns about the accuracy of the transition

And as for the accounting policies – pages of it – and the section “Judgements in applying accounting policies and key sources of estimation uncertainty” – some interesting points here, including extending amortisation periods for customer acquisition costs and the life of internally generated software, which is unusual. I know little about the energy business, but I suspect accounting for it is not straightforward, given the volatility of the energy market and politically sensitive nature of energy supply and cost

What would concern me is the breadth and complexity of this group’s operations

Maybe Greg and Stuart Jackson are supermen, but are they really on top of everything that is going on (or not going on) in this group

All that said, my personal experience as a customer of Octopus has been fantastic; they have always been responsive and as a happy EV owner, with solar panels and batteries, their Intelligent Octopus Go and Outgoing Octopus tariffs are great for me

And their energy data is great as well, so easy to download and interrogate

To me they are light years ahead of other energy suppliers in the UK – admittedly a very low bar. And as the recent migration of customers to Octopus shows, many other people think the same

So I hope they survive

I am sure that Octopus will be hoping they aren’t caught in the downwind of the US tech stock selloff. It might knock back the value they can get for Kraken significantly. The worst would be no investor appetite for further exposure in the sector, leading to the float being pulled.

I follow your analysis of the capital structure and what stands out to me is how much the story depends on working-capital timing, intangible valuations, and intra-group guarantees rather than consistent operating cash flow. In my work at Taxplusaccountants, I usually treat situations like this as a reminder to focus on cash conversion, covenant exposure, and whether asset pledges or related-party support could distort the true solvency picture. Stress-testing liquidity without subsidiary backing and reconciling statutory profit to free cash flow often gives a clearer view of long-term financial resilience.

Thank you very much for sharing your valuable content.

Octopus seem to be planning to splash some of the cash in California as part of Miliband’s deal with Governor Newsome. Given Greg Jackson’s historic links to Labour it raises an eyebrow. Whether OFGEM would regard such investment as contributing to OEL capital ratios I somewhat doubt.

https://www.uktech.news/news/octopus-energy-pours-1bn-to-us-clean-tech-market-20260216