Following on from my post about the need to secure critical minerals for the energy transition, in this post I look at copper and aluminium, two metals essential for the delivery of the huge increase in grid infrastructure that will be needed to deliver net zero targets.

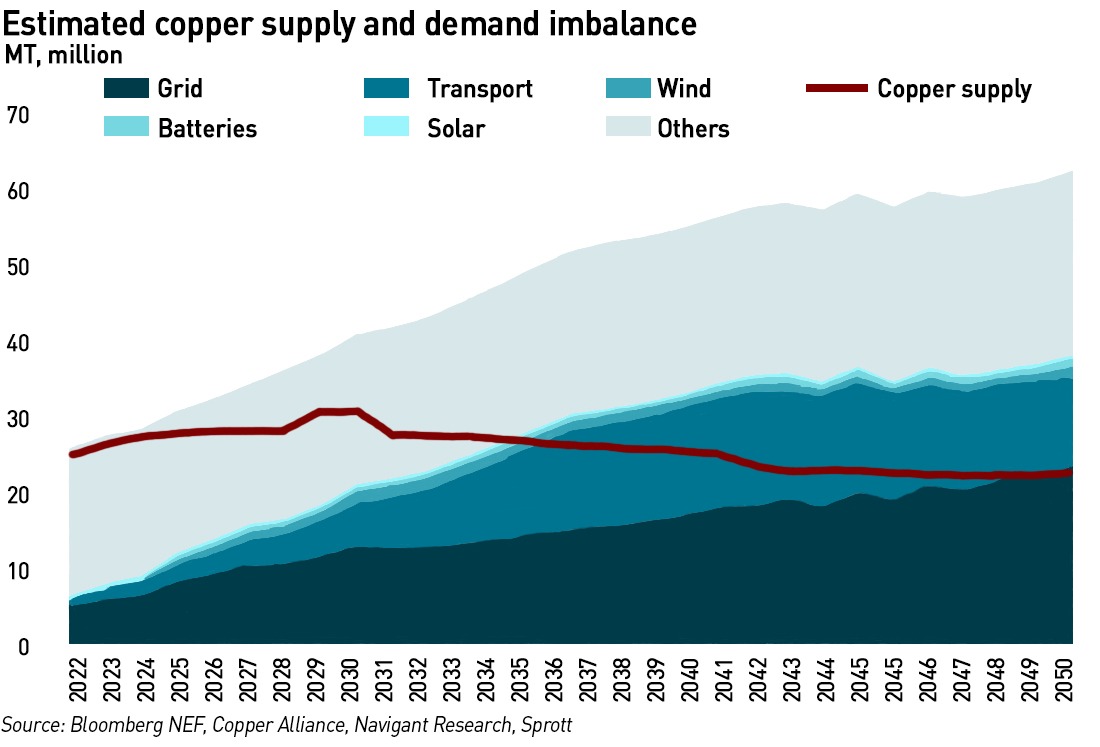

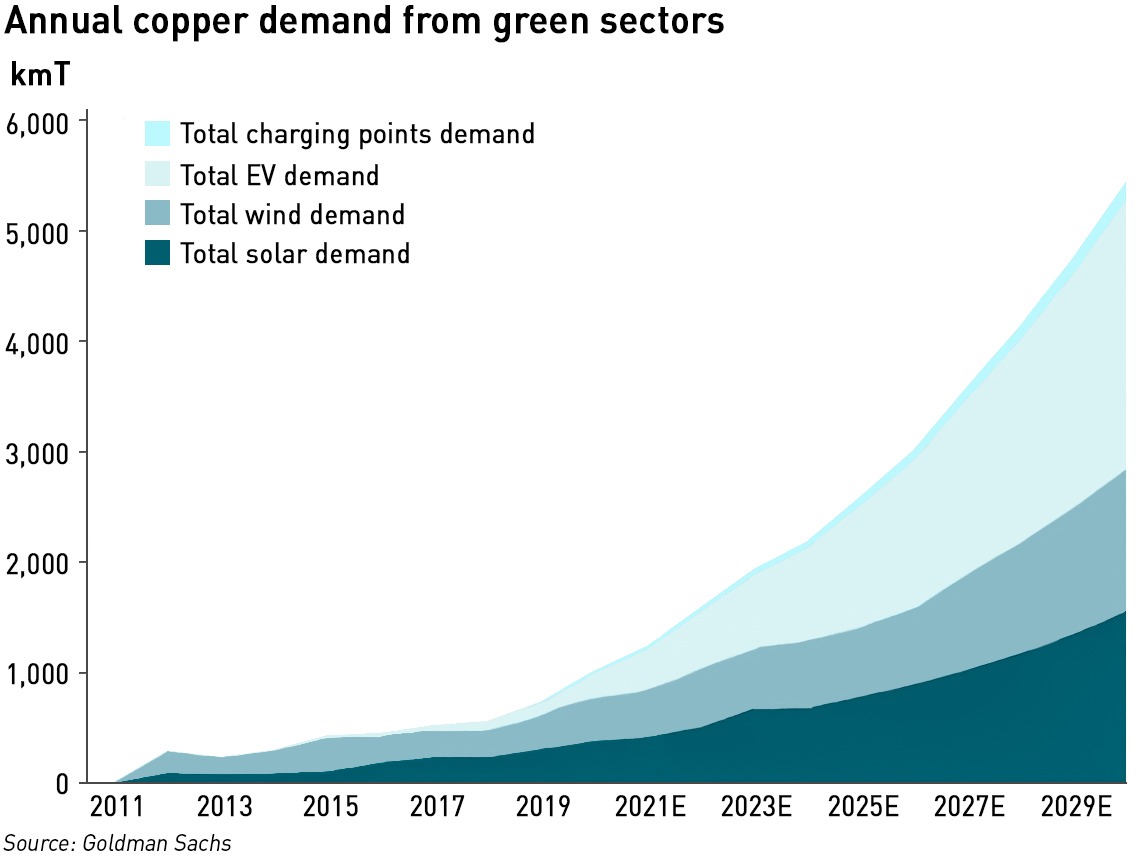

According to McKinsey, electrification is expected to increase annual copper demand from about 25 million MT in 2022 to 36.6 million MT by 2031, with supply then forecast to be just over 30 million MT, creating a 6.5 million MT shortfall at the start of the next decade. The International Energy Agency (“IEA”) expects copper demand for wind turbines will reache 600,ooo MT per year in 2040, driven by offshore wind requiring greater cabling.

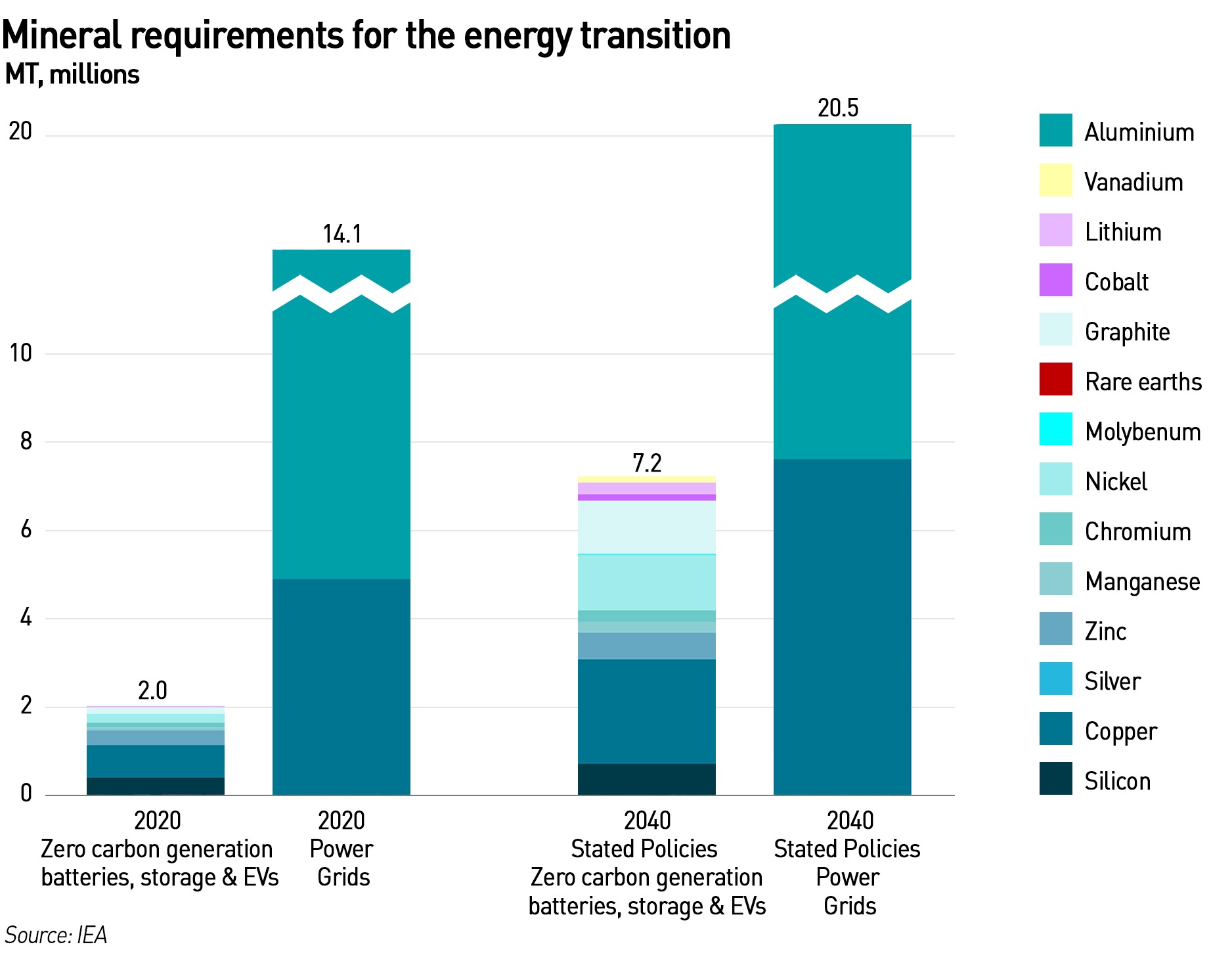

Annual copper demand for electricity grids is forecast by the IEA to grow from 5 million MT in 2020 to 7.5 million MT by 2040 in its Stated Policies Scenario and to nearly 10 million MT in its Sustainable Development Scenario . Aluminium demand is set to increase at a similar annual pace, from 9 million MT in 2020 to 12.8 million MT in its Stated Policies Scenario and 16 million MT in its Sustainable Development Scenario by 2040.

Copper is the most critical mineral for the transition, yet its availability is in severe doubt

Access to adequate supplies of copper will be essential for the energy transition – per MW electricity produced, solar and wind rely heavily on copper. Copper is widely used in power grids, and is a key input to electric cars. Solar farms require around 5 MT of copper /MW; on-shore wind requires 4.3 MT and off-shore wind requires more than 9.5 MT of copper (MT = metric tonnes).

Hybrid vehicles utilise almost twice the copper than a conventional vehicle, while fully electric vehicles use almost four times more copper. Then there is the additional copper needed to expand electricity networks globally as the demand for electricity continues to rise. All told, to reach net zero, demand for this critical mineral may increase by 142% by 2050, relative to 2022.

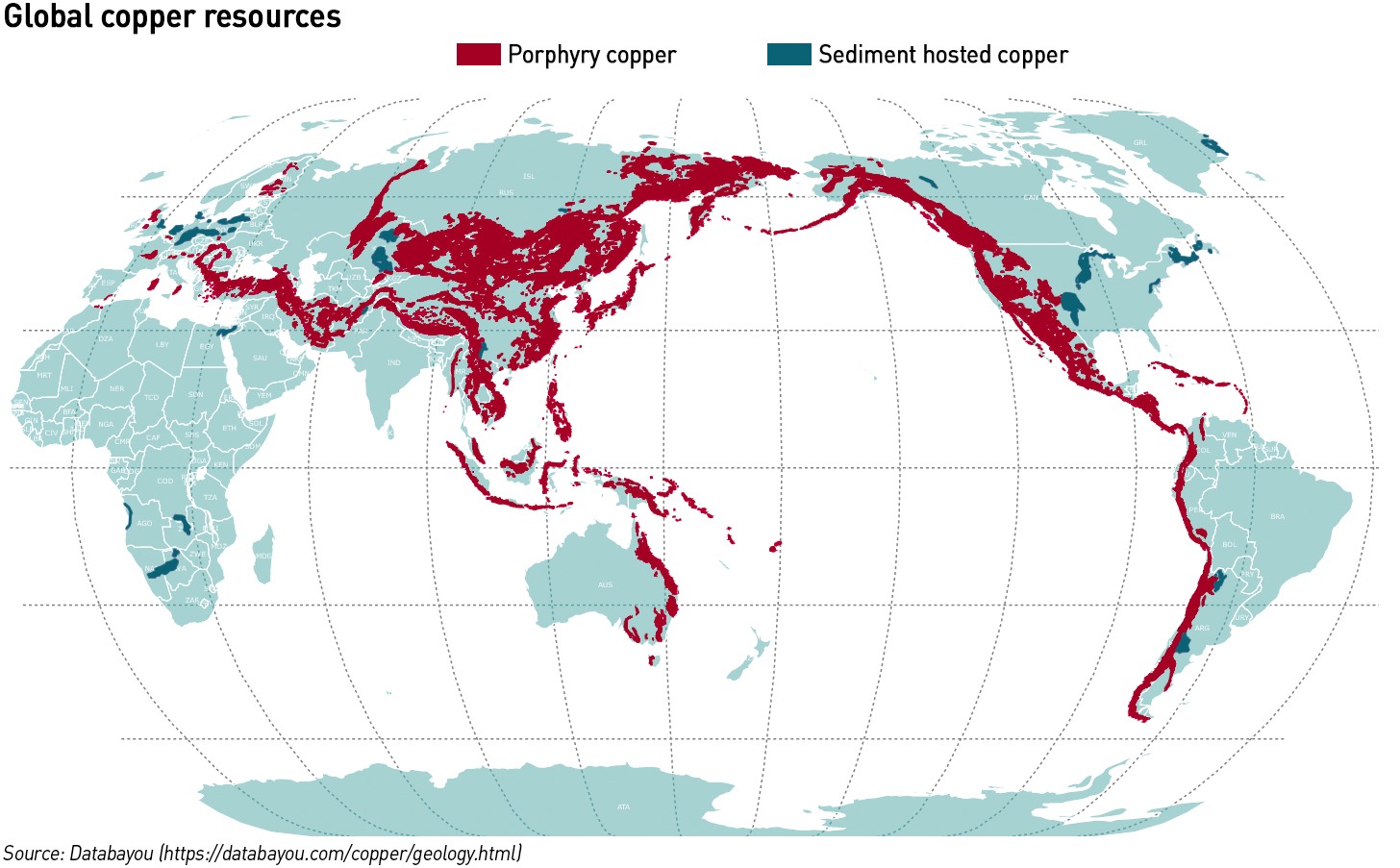

While copper is abundant in the earths crust, it is hard to mine an economically viable amount quickly enough. There are only so many copper mines and reserves and ore grades are rapidly depleting. The majority of porphyry coppers are associated with younger (250-300 million years ago) volcanic belts around the Pacific plate boundaries. The larges mines are in Chile, Utah, and Indonesia. Chile and Peru both face problems with labour relations, strikes and protests, while Russia, the seventh largest producer, is expected to see production fall as the war in Ukraine continues.

According to BloombergNEF, demand for copper could exceed primary supply within the next four years and lead to copper prices surging 20% by 2027. At the same time investors have been shying away from mining over ESG concerns. It is also difficult to attract people into mining careers. These are the most pressing concerns. Either more copper must be found, or alternative metals must be found, but only silver has similar (in fact better) electrical conductivity, and it is very much more expensive.

A forecast surplus of copper going into 2024 has suddenly all but disappeared – additional supplies had been expected due to new mining projects, leading to a widespread industry expectation for a comfortable surplus before the market tightens again later this decade, when increased demand collides with a lack of new mines. However, in November one of the world’s largest copper mines was ordered to close due to fierce public protests, and a range of operational setbacks forced one of the leading miners to slash its production forecasts.

The Supreme Court of Panama voted to overturn a contract for a Canadian company to operate the US$10 billion Cobre Panamá mine, forcing its closure. The mine produced around 400,000 MT per year, accounting for more than 1% of global copper production and 5% of Panama’s GDP. At the same time, workers at the Las Bambas mine in Peru, which produces about 2% of global copper supply began an indefinite strike over a profit-sharing dispute – the strike is ongoing. Between those two mines, the copper industry has lost nearly 600,000 MT of production.

As the market was digesting the news that one of the biggest mines was closing (at least for now), Anglo American said it has reduced its copper production target from its flagship copper business in South America for next year by about 200,000 tons, essentially removing the equivalent of a large copper mine from global supply. Production will fall even further in 2025. The company’s biggest problem is its Los Bronces mine in Chile, which, like many of the industry’s biggest copper mines, is over 100 years old and its ore now produces a much lower grade of metal. Rather than mine this expensive-to-process ore, the company has decided to wait until it can blend it with higher grade material, but this may take several years.

As mines age, miners must dig deeper to access ores, increasing excavation costs. Several large copper mines have mined out all the ore in open pits and are heading underground for higher-grade material, but thus us more expensive to extract.

The mining industry in Latin America is experiencing significant public resistance, with public anger over issues ranging from environmental damage to perceived corruption. Resource nationalism in Panama has become a major problem for both existing and potential mines – on 18 December it was reported that the Panamanian Ministry of Commerce and Industry has cancelled Orla Mining’s requests to extend three mining concessions at its Cerro Quema project.

Meanwhile Chile, the world’s largest copper producer, accounting for 27% of global supply, recorded a year-on-year production decline of 7% in November. Goldman Sachs expects Chile to produce less copper from 2023 to 2025 – the country’s production has been hit by a long-running drought in the north, where most of the copper mines are located.

One of the biggest problems is a lack of new mines. Over the past decade, greenfield additions to copper reserves have slowed dramatically, with tonnage from new discoveries falling 80% since 2010. Realistically, the current copper price is too low to incentivise new mines – prices would need to be in the region of US$ 15,000 /MT — much higher than the current level of around US$ 8,200 /MT. The capital cost of new mines runs into $ billions, and risks are rising, particularly in Latin America.

IMining magnate Robert Friedland believes copper prices could increase ten-fold if supply can’t keep up with demand, which is entirely possible, and cause volatility in the copper supply chain to spike. He also warns of a copper “train wreck” if supply can’t keep up, stating that prices could jump 10-fold, and cause volatility in the copper supply chain to spike. He says that a combination of factors suggests this may happen, including the fact that deposits are becoming more expensive and difficult to find, that funding is scarce, and societies have yet to grasp mining’s role in the shift to fossil fuels.

In the short term, the impact of production cuts has been muted due to depressed Chinese demand – while Chinese demand has benefited from energy transition sectors such as electric vehicles and power grids, this has only partly offset lower demand from more traditional sectors such as household appliances. However, some analysts believe that China is quietly building inventories, either commercial or strategic or possibly a combination of the two.

80% of the foreseeable copper supply is from just five mines, of which four have off-take agreements with non-Western buyers. That supply is locked up. The west has almost no off-take agreements for 80% of the world’s future copper supply. Mined copper that is locked up by off-take agreements should not really be considered part of global supply, because it will never western markets. Instead, it will go to smelters in China, South Korea and Japan.

Both India and China are expected to import more copper, both refined and ores, making it unavailable for estern usage. China is building its network of copper smelters, just as it did for iron ore, cobalt, rare earths, lithium, and other. Richard Mills, Editor of commodities newsletter Ahead of the Herd believes that China plans to become the swing copper producer and world’s largest copper exporter, giving it the strongest influence on the copper market. It would become a price maker, not a price taker.

All of this means that access to the copper required for the energy transition in the west will be both harder to obtain and more expensive.

Aluminium is essential for the energy transition, but requires a lot of energy to produce

Aluminium is the most abundant metal in the earth’s crust, with proven, economically viable reserves of bauxite are sufficient to supply at least another 100 years at current demand. Aluminium-containing bauxite ores gibbsite, böhmite and diaspore are the basic raw material for primary aluminium production. Gibbsite is an aluminium hydroxide, while böhmite and diaspore are both aluminium-oxide-hydroxides. The main difference between the latter two is that diaspore has a different crystalline structure to böhmite. Differences in ore composition and presence of iron, silicon and titanium impurities influence their subsequent processing.

90% of the world’s bauxite reserves are concentrated in tropical and sub-tropical regions. Large blanket deposits are found in West Africa, Australia, South America and India as flat layers situated close to the surface, and extending over areas that can cover many square kilometres. Layer thickness varies from less than a metre to 40 metres in exceptional cases, although 4 – 6 metres is the average. In the Caribbean and Southern Europe, bauxite is found in smaller pocket deposits, while interlayered deposits occur in the United States, Suriname, Brazil, Guyana, Russia, China, Hungary and the Mediterranean.

As it is almost always found near the surface, bauxite is typically extracted by open cast mining. Unlike the base metal ores, bauxite does not require complex processing because most of the bauxite mined is of an acceptable grade. Ore quality can be improved by relatively simple and inexpensive processes for removing clay, known as “beneficiation”, which include washing, wet screening and mechanical or manual sorting. Beneficiating ore also reduces the amount of material that needs to be transported and processed at the refinery. However, the benefits of beneficiating need to be weighed against the amount of energy and water used in the process and the management of the fine wastes produced.

Aluminium is critical for the energy transition, powering many low-carbon technologies such as wind turbines, batteries, electrolysers, transmission lines, and hydroelectric plants. It is also essential for solar PV, accounting for over 85% of most solar PV components. The World Bank estimates that demand for aluminium will more than double in a 2-degree climate scenario. Ironically, aluminium production is a significant source of CO2, emitting nearly 270 Mt of direct CO2 emissions in 2022 (about 3% of the world’s direct industrial CO2 emissions).

Alumina refining can also cause severe environmental damage: for roughly every tonne of alumina, two to three tonnes of waste, known as “red mud”, is created. This is very difficult to control and prevent from contaminating nearby bodies of water.

About 120 million MT of this highly alkaline red sludge, containing iron, titanium and silicon oxides, is produced worldwide each year. It is typically stored in dams, which require prior care of the disposal area, and needs ongoing monitoring and maintenance.

The global consumption of aluminium semi-finished products is expected to grow by 33.3 million MT from 86.2 million MT in 2020 to 119.5 MT million in 2030, and to 179 million MT per year by 2050 according to CRU Consulting.

Semi-finished products are intermediate goods which have undergone a first industrial process but require additional processing to define their final use. Around 37% of this growth is expected to come from China, followed by 26% from Asia (excluding China), 15% from North America and 14% from Europe. The highest growth in terms of absolute demand is expected to come from the transportation sector, driven by growth in EVs – according to Volkswagen, aluminium makes up 126 kg of a typical 400 kg electric car battery, more by far than any other metal.

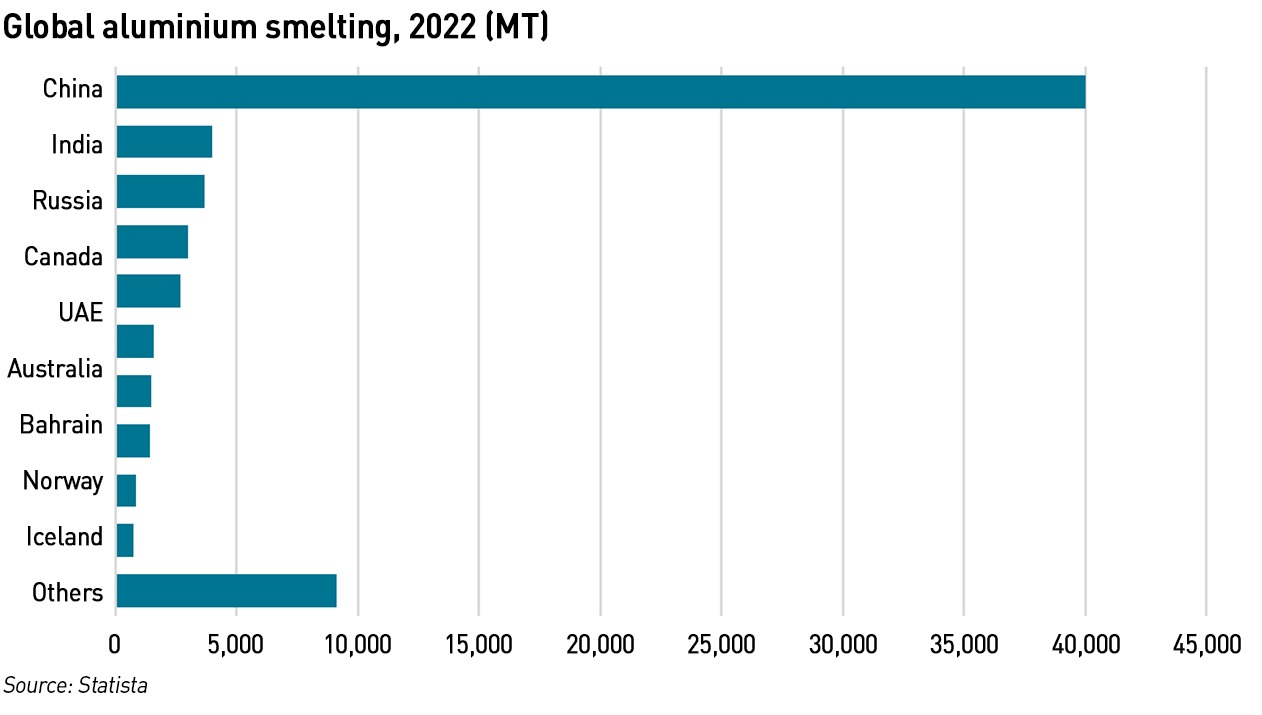

While ores containing aluminium may be abundant, smelting capacity is not. Aluminium production is highly energy intensive – energy costs account for 40% of total primary aluminium production costs according to industry body European Aluminium. Aluminium production requires around 40% more energy than copper. Recent high energy prices have forced aluminium production offline, particularly in Europe where around 1.4 million MT – amounting to 50% of the EU’s aluminium production capacity and about 2% of the global total – was forced offline in 2022, taking European aluminium production to its lowest level since the 1970s.

In October 2021, the Dutch aluminium producer Delfzijl Aluminium (also known as Aldel), stopped annual production capacity of 110,000 tonnes due to high electricity prices. In late 2022, Norsk Hydro closed a smelter in Slovakia and Aluminium Dunkerque Industries France, Europe’s largest aluminum smelter, reduced production by 22%. There was also a 33% curtailment at Alcoa’s Lista smelter in Norway, a 59% production cut at Speira’s Rheinwerk smelter in Germany which was later fully closed in 2023, and reduced output at Alcoa’s San Ciprian alumina refinery in Spain. Norsk Hydro also decided to keep smelting pots at its Husnes and Karmoey plants in Norway offline after normal maintenance and Alro’s alumina facility in Romania was shut down.

Aluminium production in the US has also fallen in recent years. In 2000 the country was the largest producer of primary aluminium in the world, but now its six remaining smelters account for just 2% of global output, forcing it to rely on imports. While both the US and EU count aluminium as a critical mineral, neither region is seeing this translate into meaningful action to secure supplies.

Chinese output continued to grow, and together with reduced economic activity resulted in a global surplus in 2023. ING expects this surplus to continue into 2024 as China continues to drive growth over the next two years. European re-starts are not expected until 2025 despite the easing of power prices in recent months. Re-starting a smelter is a long and expensive process, meaning some of the production halts seen since 2021 could become permanent. Rival bank Goldman Sachs believes the market will be in deficit in 2024 due to the effects of winter power shortages in China restricting production.

After more than 20 years of rapid growth, China’s aluminium sector recently reached its domestic capacity limit when the government imposed a ceiling on new smelter construction to cut pollution and energy consumption. Chinese companies expect to produce up to 10 million tons of aluminium per year, with new production being across southeast Asia, centred in Indonesia in a move expected to emulate Chinese nickel smelting and processing in the region. In addition to its world leading position in smelting, China also owns or controls bauxite mines around the world.

Indonesia also continues to develop its own aluminium industry, leveraging the country’s substantial reserves of bauxite, nickel, and copper. Indonesia recently banned the export of unprocessed bauxite, with the intention of encouraging foreign investors to build smelters in the country.

There are also pressures to reduce the carbon intensity of aluminium smelting, in part to mitigate the impact of the EU carbon border adjustment mechanism, which is due to come into full force in 2026. According to the World Bank, while carbon pricing may play an important role in de-carbonising the aluminium sector, a balance must be struck to ensure sufficient capacity to meet the demand driven by the energy transition.

When carbon prices are applied, the opportunities for new and existing aluminium smelters are limited, which means that production will be restricted to countries such as China and India or that the price of aluminium will have to rise above historical levels to justify investments in new smelters in new countries. In both scenarios, this will mean higher production costs for low-carbon technologies such as solar panels, EVs, and transmission lines.

.

The energy transition comes at a time when western power grids are aging, requiring updated equipment. $ billions of grid investment backlogs exist just in the US, but exist across most of the developed world, meaning that in addition to supporting grid expansions for the energy transition, grid operators also need to replace aging and obsolete equipment that is already in place. This is going to be a huge challenge, not just in terms of finding the money, but also finding the materials and the facilities to process them. A combination of resource nationalism and Chinese efforts to effectively corner these markets is going to make things very tough in the coming decade – western buyers need to develop much better buying strategies and partnerships if the necessary supplies are to be secured.

Critical minerals series

Following on from my post about the need to secure critical minerals for the energy transition, in this post I look at copper and aluminium…

Continuing my series on critical minerals, in this post I will look at some of the main metals required for lithium-ion batteries: lithium, cobalt and nickel…

In this next post in my series on the critical minerals required for the energy transition, I look at graphite and manganese….

In this final post in my series on minerals critical to the energy transition I look at rare earth metals.

Simon Michaux of the Finnish Geological Survey has published a lot of good information on this issue.

https://www.simonmichaux.com/

Thank you for an interesting article.

I think another interesting question that seems to be largely unexplored is whether the world is doing anything like enough manufacturing of turbines, solar panels and batteries (grid scale, dwelling scale and vehicle) for countries to meet the commitments they have made (assuming manufacturers can get the minerals).

Finally another question I find interesting is the impact on the world workforce of a wind and solar energy world. Net Zero Australia identified an increase in the workforce in the energy sector in Australia. This did not include

increased mining of lithium, copper, whatever and Australia does no real manufacturing. If the energy industry will require a markedly increased workforce, I wonder where that leaves other infrastructure.

Aluminium is a very good substitute for copper for almost everything discussed – and ends up being cheaper when used as a conductor in these applications.

And there is plenty of scope for Australia to dramatically increase both bauxite mining and processing of ores into raw aluminium, as it is blessed with huge solar resources which can provide very cheap power.

See https://pubs.usgs.gov/periodicals/mcs2022/mcs2022-aluminum.pdf. There are around 1,000 years of bauxite resources available, based on current aluminium production.

So there is no serious issue here, though many users of copper might find it much more economical to move to mainly aluminium in the next decade.