On 14 June, the National Audit Office (“NAO”) published an updated review into the smart meter rollout, finding that while progress has been made since its previous review, the scheme is significantly behind target and the Government is not keeping track of the overall costs and benefits in a way that will allow it to make optimal decisions for consumers. In particular, data about the benefits continue to be based on the behaviour of early adopters who may not be representative of the population at large.

On 14 June, the National Audit Office (“NAO”) published an updated review into the smart meter rollout, finding that while progress has been made since its previous review, the scheme is significantly behind target and the Government is not keeping track of the overall costs and benefits in a way that will allow it to make optimal decisions for consumers. In particular, data about the benefits continue to be based on the behaviour of early adopters who may not be representative of the population at large.

When the Government originally devised its smart meter plan for homes and business in Britain back in 2011, it expected the rollout to be materially complete by 2019. This target has not been adjusted on three separate occasions, and last year the Government introduced a new four-year regulatory framework with binding targets for suppliers.

The new Energy Act which is currently progressing through Parliament will extend the Government’s powers in relation to the rollout from the current expiry date of 1 November 2023 by a further five years. The Government is proposing new targets for suppliers to install smart meters in at least 80% of the homes, and 73% of small businesses, by the end of 2025. The Government believes it is now technically possible for smart meters to function in 96.5% of homes and small businesses.

The NAO says that the current installed base of smart meters is beginning to deliver benefits, however it says that the rollout is at a crucial point, with decisions taken now likely to determine the extent to which the Government can maximise value for money from the remainder of the programme. It says DESNZ should “ensure it has robust information on both the total costs and benefits of smart meters to make these decisions from an informed position, particularly on the merits of different approaches to the rollout after 2025, including considering at what point the programme can end”.

The NAO recommends that the Government should collect more information on actual and forecast costs and benefits to inform decisions on how to maximise value for money over the remainder of the rollout and that these should be reported annually to Parliament. It says that by the end of this year, DESNZ should determine whether more programme-wide evaluation would help to inform decisions on the remainder of the programme, for example how to maximise the benefits to consumers, suppliers and the wider system. It also says DESNZ should “work collaboratively with suppliers to address the reasons why installation rates have been slower than planned” taking into account differences between suppliers, and considering whether to introduce additional measures to encourage or require consumers to take up smart meters.

It should also work with industry on how to manage upcoming challenges in the rollout, including consumers’ continued use of traditional meters, and the replacement of communications hubs ahead of the 2G and 3G switch-off. This should consider how hub replacements will be financed.

Suppliers struggling with installation targets

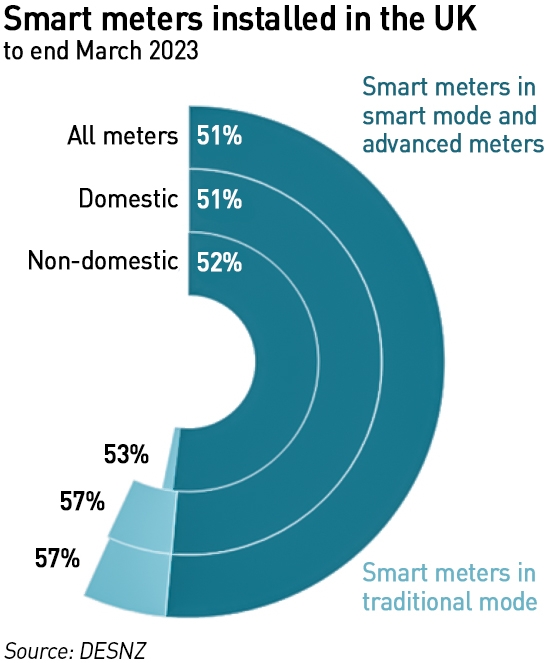

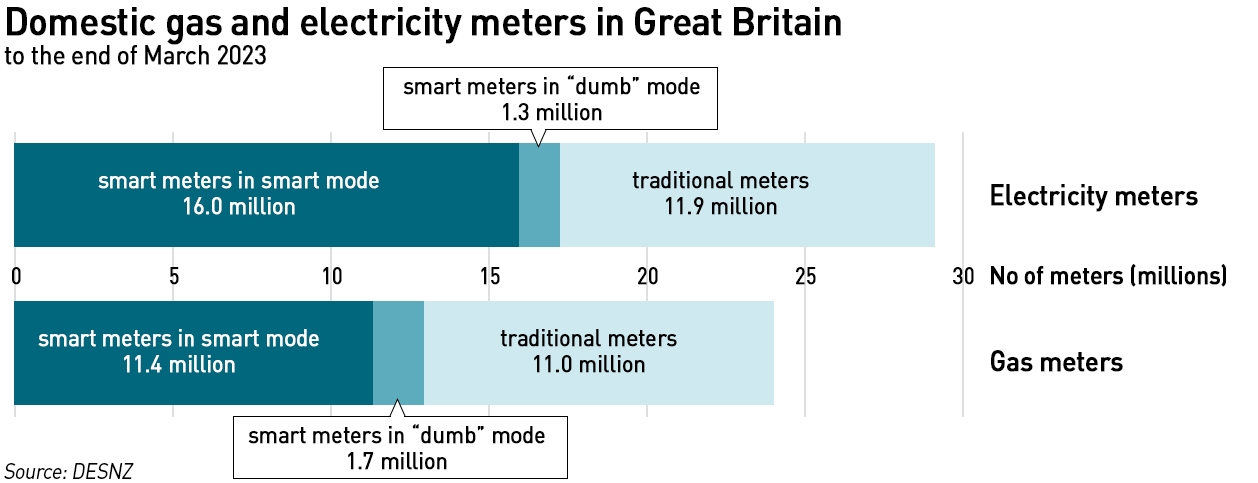

Suppliers have now installed smart meters in just over half of homes and small businesses, approaching the 60% coverage that the Government estimated would be needed for electricity networks to begin securing benefits from smart meters. At the end of March 2023, 57% of all meters were smart (32.4 million out of 57.1 million).

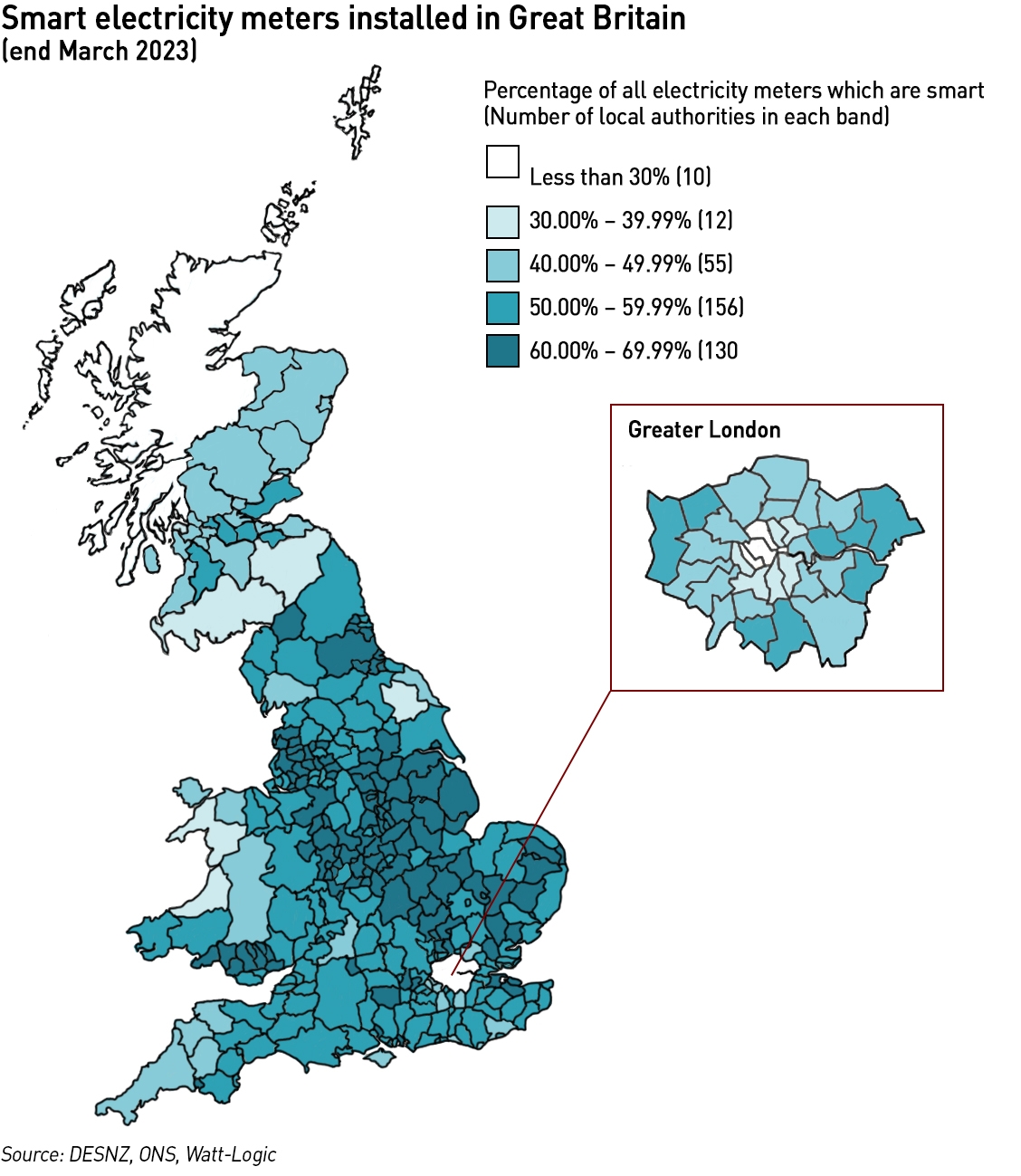

Survey data show that people aged 18 to 24, people in private rented accommodation, and those who pay their energy bills quarterly are less likely to have smart meters installed.

There is lower smart meter coverage in remote areas and London where there are particular challenges with hiring installers, having parking spaces for installers near homes, a high proportion of consumers in the private rented sector, and a higher number of people living in flats, which have technical challenges particularly with the in-home display and communications hubs being too far apart, although this is expected to be addressed by the Alt HAN Company Limited’s solution.

Government data on regional installations are incomplete: they only include electricity meters, and not gas meters, and the data do not differentiate between smart meters in smart mode, or those working in traditional mode.

This means the Government does not have an overall view on where all meters have been installed, and whether there are areas which are seeing more technical issues than others.

Only one out of 13 large suppliers achieved both its 2022 electricity and gas smart meter installation targets. In total, these 13 suppliers installed 3.7 million meters against their combined target of nearly five million, and most suppliers have not improved installation rates enough to meet their targets. Suppliers’ performance ranged from 48%-110% of their electricity target and 32%-138% of their gas target. Ofgem is currently progressing enforcement discussions with the majority of large suppliers that missed their targets in last year, however, suppliers told the NAO that the targets are too challenging and provide perverse incentives. Reasons given for missed targets in 2022 included:

- Reduced demand for smart meters – the November 2022 Smart Energy GB Outlook Tracker showed 41% of the 4,655 respondents who claimed to not have a smart meter had concerns about them. Suppliers say they have exhausted the “low hanging fruit” of households that actively wanted a smart meter, and it is becoming increasingly challenging to encourage take-up;

- Shortage of installers – there has been a steady decline in the number of meter installers across the industry since 2022, with a reduction of around 1,000 (as of September 2022, large suppliers were reporting there were fewer than 6,000 installers, a reduction of more than 1,000 – about 14% – since March 2020.

- Targets prioritise quantity of installations over quality – and do not include fixing issues with previously installed meters; and

- Varying supplier business models – suppliers vary by characteristics and face different challenges to each other, for example, they serve different areas and customer bases making direct comparisons between them difficult.

Chris O’Shea, chief executive of British Gas owner Centrica, complained in The Times that the company is in a “very odd” situation where smart meters are voluntary, but suppliers face penalties for missing installation targets, saying: “the regulator can fine us for not installing enough smart meters last year and does not seem to be open to the possibility that some customers don’t want smart meters”.

Both Ofgem and DESNZ believe suppliers are not meeting existing demand for smart meters and that there is scope for suppliers to improve their performance. In November 2022, 37% of Tracker respondents who did not already have a smart meter said they would seek or accept a one in the next six months. According to DESNZ, this group has not been dwindling over time, as more people become interested in having a smart meter – I was able to find the Trackers to validate that claim.

“As an industry we have installed the easier meters in the first phases, in the early days of installations. Now what’s left are more medium to difficult installations which will take more time and therefore more people to maintain the installation rate. Installations may start to speed up as we ramp up the training of staff and engineers in the near term, but the reality is it’ll be slowed down as we come to the end of the rollout with more difficult properties such as tall blocks of flats and farmhouses. Yes, we need to double installations now to get to 2025, but even if we double, that will still not get us to 100% by the deadline,”

– Matthew Roderick, founder and chief executive of digital services company n3rgy

Analysis by Utility Week suggests the rate of smart meter installations will have to more than double to have any chance of completing the rollout by the 2025 deadline. Based on the pace of installations over the past year, around 13.4 million homes and small businesses will still not have a smart or advanced meter at the end of 2025… to meet the target, suppliers would have to fit 700,000 devices per month, compared to the current level of just under 300,000. Even the Government’s backstop minimum target of 80% coverage in domestic properties by 2025 is set to be missed.

The work of the NAO shows that the Government and suppliers disagree on the best way to achieve the remainder of the rollout. Suppliers say their 2022 targets were too challenging as the remaining consumers with traditional meters are less interested in getting a smart meter, and a shortage of installers is hampering efforts to meet the demand that does exist. They say that introducing new regulations to require new-build homes to have a smart meter installed by default would help – it’s surprising that such regulations do not exist already.

DESNZ and Ofgem believe the fact some suppliers achieved their 2022 targets means missed targets are due to supplier underperformance and that suppliers have a commercial interest to argue for lower targets. However, this fails to address the differences across supplier customer bases as highlighted in the NAO report. The Government believes there is still demand for smart meters and that suppliers need to invest more in the rollout and improve their installation performance before it will consider introducing additional policy levers, but accepts that additional levers may be required at some point.

There are some premises which may never be suitable for a smart meter. However, manufacturers have largely stopped manufacturing traditional meters and stocks are gradually running down. Consideration needs to be made for metering these properties in the future.

Consumers continue to experience technical issues with their smart meters

The Government has previously been criticised for rushing its smart meter rollout before the technology was ready. As a result, millions of homes were fitted with first generation SMETS1 technology which lost its smart functionality when the consumer changed supplier. While this issue has been fixed by the development of SMETS2 meters, and the adoption of SMETS1 meters onto the Smart DCC network, this enrolment process is incomplete and does not work in all cases.

At the end of March 2023, around three million smart meters (9%) were not operating in smart mode. As noted above, stakeholders say that targets incentivise the installation of new smart meters above addressing issues with previously installed devices.

As at 5 May 2023, around 11 million SMETS 1 meters had been migrated onto the Smart DCC platform, but four million had not, despite Government’s requirement that this be completed by the end of 2022. In September 2022, the DCC told the Government that technical limitations mean it may not ever be possible to migrate more than 500,000 of the remaining four million SMETS1 meters.

In August 2022, a survey of 1,580 adults for Smart Energy GB found 37% of respondents with smart meters claimed to have had an issue with their meter at some point following its installation, including no automatic readings, inaccurate bills and the smart meter or in‑home display not showing information. The Government believes this overstates the true number of consumers who have experienced issues as the data were collected at a time of increased concerns in the energy market, although I’m not sure how legitimate that belief really is – people either had a problem or they didn’t.

Stakeholders have also identified reliability issues with the Smart DCC platform which is intended to maintain and improve a secure network for smart meter data allowing the industry to develop future services, saying that they were not able to achieve their expected benefits from the system. The platform met most of its service level obligations between October 2022 and March 2023.

The disconnect between smart meters being voluntary for consumers, but suppliers facing penalties for failing to meet installation targets is leading some suppliers to call for powers to force households into having a smart meter if their traditional meter breaks down. Consumer advocates unsurprisingly oppose this idea, fearing abuses by suppliers who have already been criticised for hard-sell tactics to get households to accept smart meters. They also note complaints from consumers whose smart meters don’t work and have never worked due to mobile connectivity problems. Some devices have also displayed incorrect data leading to unexpectedly high bills, with consumers complaining that faulty devices are not repaired or replaced in a timely manner.

For example, 84-year old Doug Bruce, says he was pressurised into getting a smart meter in his home near Braemar, Scotland, but when it was fitted in August 2021 it failed to connect his supplier’s system, leaving him with inaccurate meter readings. He has since changed supplier, but the problems persist. Another consumer, 57-year old Patricia Worby, from Southampton was forced to change supplier after her previous supplier refused to fix her broken smart meter. She says her smart meter failed to function for more than two years after it was installed – it does not communicate with her in-home display (“IHD”) or send readings to her supplier, meaning she has to send reading to the supplier herself. Her main reason for accepting a smart meter in the first place was to avoid having to submit her own readings.

According to the Ombudsman Service, complaints relating to faulty and inoperative smart meters are rising. While Ofgem told The Sun Newspaper that suppliers must follow certain “licence conditions”, which include taking reasonable steps to operate smart meters, it provides little guidance on whether suppliers should bear the cost of replacing faulty smart meters and in-home displays if they’re over 12 months old.

The newspaper reviewed the main suppliers’ policies around faulty devices and found that larger suppliers will generally attempt to fix problems remotely and if that fails send an engineer for a site visit, replacing any meter that cannot be repaired. However, IHDs will generally only be repaired for free within the first 12 months and after that only vulnerable customers would receive a free replacement. Octopus Energy, Ovo Energy, Utilita and Shell Energy said that they will never charge customers for replacing a faulty smart meter or in-home display even if it is more than a year since installation, although Ovo excludes IHDs that have been damaged by the consumer.

As I have noted previously, a looming problem with even SMETS2 smart meters relates to their reliance on 2G and 3G mobile phone networks which will be switched off in 2033. This applies to devices in the central and southern regions (the northern region uses a different technology, although I’m told by industry insiders that it has reliability issues). More than 15 million SMETS1 meters and almost 14.8 million SMETS2 meters will be affected. However, the technology to connect SMETS2 meters to 4G will not become available until at least 2025, according to the DCC.

There has been no updated analysis of the costs and benefits of the smart meter rollout since 2019

The NAO report says that based on the assumptions in its 2019 cost-benefit analysis, DESNZ estimates that as of March 2023, a typical household with a smart meter is saving £56 per year on energy bill through reduced energy use. For context, a typical household was paying £2,500 per year for energy at that time.

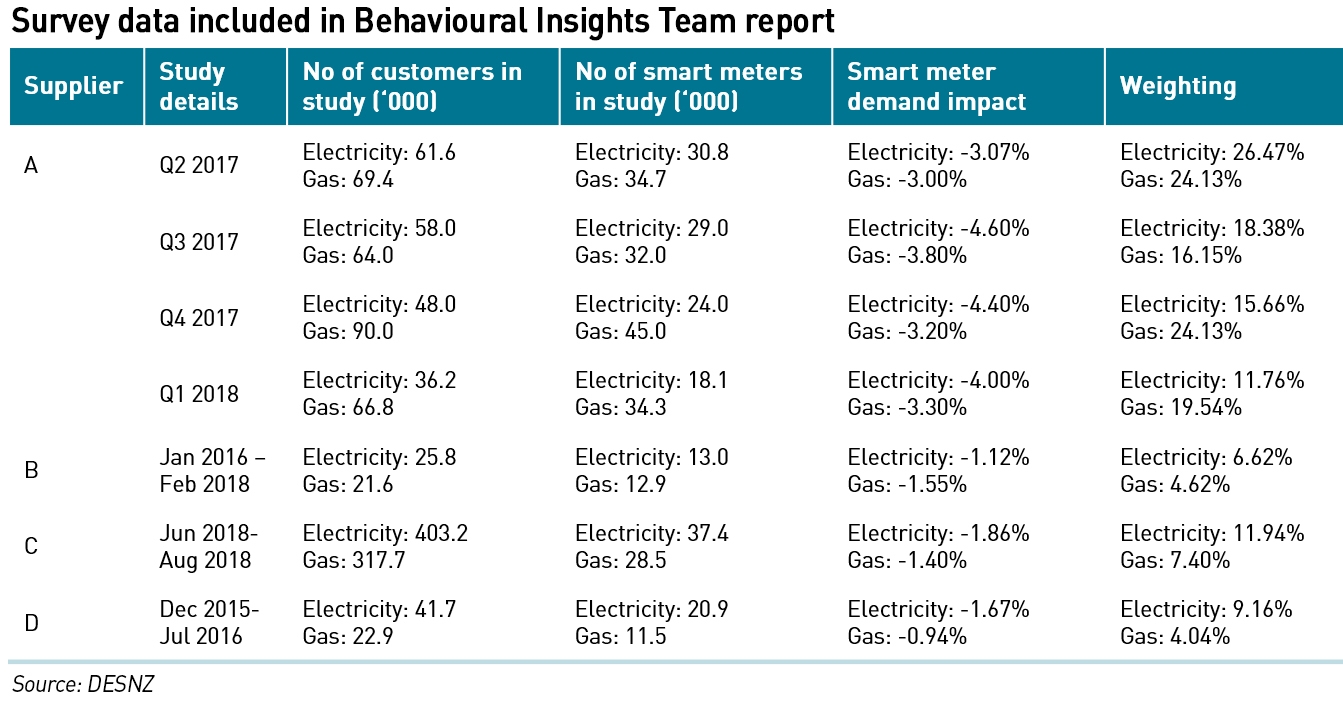

In 2022 the Government asked its Behavioural Insights Team to conduct a review of internal supplier studies to determine the benefits of smart meters in terms of demand reduction. It found that smart meters save an average of 3.4% of electricity consumption and 3.0% for gas, with narrow confidence intervals. However, the NAO criticised the study saying it was dominated by a single supplier and that the conclusions were based on early adopters which may not be representative of consumers more broadly.

The supplier studies included in the review are outlined below, together with the weighting they were assigned in the study (I was not able to determine the basis for the weightings). It is clear that the studies all use old data – the most recent being August 2018, and the highest weighting was assigned to studies using data from Q2 2017. The NAO criticised the data selection saying: “the study was also based on data from people who had a smart meter installed earlier in the rollout, who may have different energy use behaviours to those accepting a smart meter later in the programme and the wider population.” The sample sizes are also small.

The Government previously had a Cost Control and Benefits Realisation Group that identified, scrutinised and recommended actions to contain costs and maximise benefits of the rollout; however, it has not met since 2019.

In its 2019 cost-benefit analysis, the Government estimated that suppliers would save almost £8.1 billion between 2013 and 2034 (at 2011 prices). Suppliers have reported some cost savings, including from avoided site visits and fewer inbound consumer calls. The Government also expected to see network-related benefits worth £370 million, although network operators told the NAO they were only just beginning to see these benefits although there is potential for more when a higher proportion of properties have smart meters and when they can more reliably access data from the DCC.

Smart meters are starting to provide some wider system benefits, for example the Demand Flexibility Service launched by National Grid Electricity ESO last winter which enabled consumers to be paid for shifting their consumption to help reduce peak demand. Flexibility services and time-of-use tariffs are likely to become more widespread after April 2025, when Ofgem expects the industry to have started to implement half-hourly settlement across the retail electricity market. The NAO notes that “further system benefits are likely to rely on the financial stability of suppliers” as the development of flexibility services and time‑of‑use tariffs could depend on suppliers having enough capital to invest in new technologies and business models.

“With more than half of homes now having smart meters DESNZ has an opportunity to strengthen its evidence of whether the benefits it anticipated for consumers and suppliers are being achieved and how these compare with the costs incurred. DESNZ is planning a full evaluation of its approach once the rollout is complete. But having this information earlier, using the latest evidence from the meters installed to date, could help inform future decisions, including about the rollout after the current regulatory approach ends in 2025. In particular, this could consider the point where the Programme can cease because costs incurred would outweigh the additional benefits gained. In addition, DESNZ needs to consider the potential future costs, including the costs of additional home visits to replace communications hubs ahead of the closure of the 2G and 3G networks by 2033,”

– National Audit Office, Update on the rollout of smart meters, June 2023

The Government collates information on smart meter costs from suppliers and the DCC on an annual basis and uses this to support policy decisions. However, it does not calculate and report on total costs to date or estimate the lifetime costs of the rollout. DESNZ told the NAO that it is confident the costs of the rollout are under control, but it recognises that providing Parliament with an annual update on the costs and benefits of smart meters would increase transparency and accountability.

Suppliers told the NAO that the cost-benefit analysis did not include all the additional costs suppliers will need to incur to ensure smart meters continue to function during and after the rollout, such as additional home visits and communications hub replacements when the 2G and 3G networks are shut down. In addition, ongoing maintenance of smart meters is more complex than for traditional meters as they have three different and separate components at minimum, compared with just one traditional meter. This may lead to further technical issues and increased costs as, for example, they may need to have software updates. Citizens Advice says these costs may be very significant is concerned they will ultimately borne by consumers or taxpayers.

The Government counters this by claiming there will be ongoing costs and benefits associated with the enduring operation of the smart metering system beyond those considered in the 2019 appraisal of the core rollout, and that these should be considered part of suppliers’ business-as-usual costs in the future, although it does recognise there is a role for government in maintaining some oversight of these costs.

Smart meters should be and easy sell – why aren’t they?

That “smart meters save people money” is one of the energy market myths. Smart meters just measure consumption, they do not have the capability to save people money – only people can do that through behavioural change, and while that change can be informed by the information provided by smart meters, demonstrating that that is happening requires more than a handful of five-year old surveys of small numbers of early-adopters. Perhaps the reason for the lack of an updated cost-benefit analysis is a fear that the costs now outweigh the benefits, and if all the costs including those associated with the 2G/3G switch-off were included, then this becomes even more likely.

Misleading consumers is not a good look. The Government should be transparent on the outcomes of its programmes, and if they impose a net cost on consumers, they should explain why this is still a good thing. Perhaps the benefits will emerge later in the form of better optimisation of grid resources and a reduced chance of blackouts through load-shifting behaviours.

The Government also needs to better understand the reasons for the low uptake of smart meters – more than a decade on penetration has only just passed the 50% mark. Why are consumers reluctant? Lack of trust is likely to be a major factor, something to which both the Government and Ofgem contribute with their relentless anti-supplier rhetoric. DESNZ and Ofgem seem keen to “blame” suppliers, using the performance of some as a stick with which to beat others, but as the NAO points out, there are legitimate reasons why some suppliers will do better than others. It should be obvious that suppliers with a significant number of customers in remote areas, or in high density housing will face challenges others do not. Failing to take these differences into account, and in some cases failing to even gather the data that will allow these differences to be better understood, is a major failing.

Aside from concerns over data security and privacy, smart meters should be seen as a good idea, but it’s difficult to muster much enthusiasm for them. The rollout has not been managed well: it began before the technology was ready leading to millions of households facing technical problems, and the choice of suppliers rather than network companies to lead the installation was hampered by the poor reputation of suppliers and a failure by the Government and Ofgem to persuade consumers that the benefits outweigh any disadvantages. There are no signs of this changing any time soon.

Energy to make, energy to fix , energy to fully replace.

Aren’t we supposed to be making our lives less complex.

Interesting article thank you. However, it’s difficult to be sure whether there is any real evidence for consumer cost savings. So how is Government reaching it’s conclusions? I have a £13 “smart” meter which provides me with instantaneous electricity consumption, daily, weekly and monthly usage and cost. The meter can be calibrated against my mechanical meter so the readings are accurate. This meter tells me all I need. Regarding savings, surely the massive hike in utility prices will do more to reduce consumption than any smart meter?

Exactly – there are other consumption measurement devices people can use and high costs are a significant motivator.

As I fairly tech savvy electricity consumer who gets through 18000kWh on the night rate and 4500 0n the day rate, I recently had a “smart” meter installed. Many years ago I got used to switching as much consumption as I could to night rate including heating, hot water, car, washing machine etc. Having a smart meter has changed nothing.

It’s not even that smart. What I would like is a way of downloading my own half hourly data. I can’t see any benefit for customers who use fossil fuels for heating. What are they supposed to do?

Some people think complex time of use tariffs will somehow improve things for consumers. How? Most people don’t even understand Economy 7.

One suggestion I have is that the 7 hrs off peak rate is tied to the cost of gas and that the day rate can only vary closely around the night rate – say by a factor of 3:1. The current regime allows suppliers to operate in a way that seriously disadvantages off peak users. So, for me the cost of having a smart meter is balanced by, zero benefit.

I think the assumption is that a third party will do the optmisation on behalf of consumers – but that will require trust which is noticeably absent in the sector. Also, some studies have shown demand response making things worse because people are not very good at optimising. And then there’s the issue of how to stop too much response and putting the grid into the opposite problem…

We are with EDF. I selected to send data half hourly when we had the smart meter install so I can download this from the EDF website. Can also download daily data although not what you are after.

Not sure whether all suppliers provide this download. It appears yours doesn’t.

Ten years or so ago, I bought an attachment which gave a minute by minute readout of my electricity usage. For a few weeks I was a total nuisance to the family, turning things off to see how much I could save. After some months I was forced to realise realised that I was not reducing my bill by any significant amount- as a household we were already pretty good at turning off lights etc.

I am thus very sceptical of the benefits to me of a smart meter. The downside is ‘demand management’. I interpret that weaselly term as a) turning off my power whenever convenient to them, or b) varying the price to be more expensive at the times I actually want to use electricity.

The whole reason they need to impose these on us is that the grid has been totally destabilised by the race to net zero.

Back in the day, with coal, nuclear and gas, there was ample capacity for all needs, with a spinning reserve that could easily cope with half the country turning on a kettle during the Coronation Street commercials.

Most DSR participants only secured pennies of savings last winter despite the high prices. Also, if you have LED lights they don’t use much power so turning them off isn’t that important. In the absence of ToU tariffs there’s also little scope for saving – load shifting could make a difference eg don’t do laundy at peak times, but not doing laundry at all isn’t an option.

Of course the other reason for consumer reluctance to smart meters is the power it gives suppliers to change tariff to prepayment for instance, or remotely cut off customers.

I don’t understand why the meters don’t come with some sort of wifi connection. Most homes have wifi now that should give a more reliable connection in mobile not-spots.

Really the smart meter programme should be paused until there is resolution of the built in future obsolescence. Then we need to tackle the issue that few believe that smart meters will be passive, benign devices, but will in the fullness of time be used for cutting off supply. Indeed, they already are, with the scandal over switching customers to pre-payment remotely and with no notice or even explanation of how to obtain credit, leaving them disconnected.

DFS may be voluntary for now, but when we have REGEN on behalf of NGESO calling for 20-30GW of demand flexibility in the future you know that will not be quite so voluntary. Also, the DFS programme has been perhaps disappointing despite the false bravado hype from NG, with only a maximum of 294MW actually “delivered” (less after allowing for gaming the system), or about 0.6% of demand, despite nominally high bribes and bids of £6,000/MWh being accepted to organise the service and pay consumers.

I think that the Net Zero future is running into marketing difficulties, with smart meters at the fore of consumer conscience. Trying to make them compulsory will only raise suspicions much higher. Half hourly metering is also a privacy issue, revealing much about personal lives. I don’t think the implications of that have been thought through, unless the intention is to micro control our lives. Who would vote for that?

I agree.

Making smart meters mandatory will be difficult to justify and may well attract legal challenge since for many consumers they don’t work and for some they never will. Similarly making demand response mandatory will be fraught with difficulty…does that mean consumption will be rationed? I think this is a rabbit hole we need to avoid falling down…

I’ve long been obsessive about saving energy – there are no lights on in unoccupied rooms in my house! So, unless and until smart meters are smart enough both to identify real-time usage that is different from the normal pattern and give a readout of the energy consumption of individual appliances, they will be of no help to the consumer whatsoever.

I think the idea is to identify wasteful use, but this is of limited benefit: when prices are low people won’t care about waste (see the issues with water meters in Sussex where the affluence of the residents meant consumption increased once it was metered), and when prices are high they will be careful not to be wasteful. Meters aren’t much help in either scenario.

Another Quango inspired foul up, SMETS 1, SMETS 2 , 2G / 3G , and next gen linkage ( Which cannot operate near RAF bases ).. Still sorting out bills after 2.5 Years of foul ups , 5 visists by” experts” changing bits.. (In reality partially trained Joe Soaps who have to ring back to base for guidance ( From an area within poor mobile signal).. Yet to ask for help on IHD ( But expect to be told it does not work on time varaible tariffs. )

Elegant in concept , and expensive in delivery.. Business case now is in tatters . Do not even have traceability to failure areas ( theat is secret ..must not be traced or known!!) And now my off peak rate is increasing by 26% from July 1.

Are the peope for delivering this foul up still in place? Normal Government and Civil Service Performance ..Overrun on costs , Late delivery and not acheiving planned outcome.

Thank you Chris. There are a multitude of issues which will be needed to be sorted out before the move from fossil fuels for domestic heating to electricity. Not least the issues you mention but importantly the way that suppliers flex the off-peak/Economy 7/night rate tariff. If domestic gas prices fluctuated by similar percentages, there would be uproar.

If, and its a big If, there is to be a move to electricity for heating, there has to be a financial benefit for customers to move. How? More certainty about future rates – linking the off peak rate to gas – providing worked examples of potential savings (including lifecycle costs) – building regs – no separate domestic tou tariffs for electric cars. There needs to be some sophisticated (but not difficult modelling of how electricity demand will change over time, linked to how and when it is generated. Time of use data is essential for this to be done and I expect 50% uptake of smart meters is adequate for this, but in reality they do little or nothing for customers.

I do wonder about smart gas meters. Anecdotally it also seems they are more difficult to connect

Appears to little (or no) scope for consumers to move their usage.in response to high demand. With sufficiently punitive ToU tariffs one might turn the heating off, but that seems an undesirable outcome. We’ve got a NEST + HW cylinder so could potentially heat hot water ‘off-peak’, but it’s small usage compared to CH on cold days.

But surely a bigger point is that as we replace gas boilers, it may not be that long before number of gas meters is actually reducing. Smart meters being installed today may well have less than 10 year lifespan.

Does look like a huge amount of effort & cost that could more usefully employed elsewhere

There really is no point in intraday ToU tariffs for gas: the diurnal swings in demand are buffered by linepack (extra pressure in the pipelines effectively stores gas as a replacement for gasholders). The only substantive ways to reduce demand are to improve insulation (which may be hard to justify on cost grounds) or turn down the thermostat or fire up the woodburner or coal grate.

The industry operates with daily pricing which is sufficient to cope with incidents such as production upsets. LNG and other storage also help. Electricity has no storage, so supply must meet demand.

Perhaps I should add that if you want Norway to boost exports on Langeled you’ll need to give 3 days notice to allow for pipeline travel time. Propagation of supply ex LNG terminals and cavern storage will be a little quicker, but it won’t reach all corners of the system for a day or more. Hence the use of linepack as inherently more local storage.

“The Government believes it is now technically possible for smart meters to function in 96.5% of homes and small businesses.”

The Government believes anything (true or false) that reinforces it’s political agenda.

And in this bastion of democracy & free speech,… anyone who goes against the latest perceived ‘political wisdom’, is rapidly canceled as we’ve seen with – Brexit, Climate, Covid, Defense, Energy, Health, Policing, Transport ….

Brave new world !!!

A little off subject but relevant. BBC R4 Today 30 June interviewed Karl Arntzen, CEO Worcester Bosch discussed the roll out of ASHPs as part of the UK Government’s plan to reduce the dependance on gas to heat our homes. He made the inescapable point that so long as there is a 3-to-1 difference between the cost of electricity and gas, he called it ‘the spark gap’ then even with a COP of 3 of ASHPs then bills will be about the same. There is no insensitive to change.

typo mistake: insentive not insensitive!

I see they got you under their skin!

[link removed]

A load of slyly written lies and half truths in their attempt to smear. Quite how much a political writer knows about the real world is a nice question.

I hope you don’t mind but I’ve removed the link to avoid giving them clicks, particularly from my own website!

They gave me only a couple of hours to respond at a time I was organising some logistics for my father’s funeral. I didn’t give them permission to quote from my response becuase it was clearly a hit piece where they were trying very hard to demonstrate my “links” to big oil. They had planned to say I receive funding from oil companies which isn’t true – I have received no external funding other than fee income.

They also completely mis-represented what I said on the Today Programme and planned to twist it into something that was not only untrue but nonsensical. As it isn’t a very widely read blog I thought a public response was un-necessary and would just given it more attention than it deserved.

Apparently the upgrades from 2G/3G to 4G will cost £0.5 billion!

https://utilityweek.co.uk/smart-meter-comms-hub-swap-could-cost-500m/

the problem is that aiming at 4G today is way too late, that boat has sailed. It’ll have been turned off by the time you get there.

The downside with consumer technology, like mobiles, is that it advances rapidly. maybe even exponentially.

last thing you want to be doing for a long term thing like smart meters is to be chasing a version number like windows, or (worse) Chrome.

and for the application, even 2G is way overkill. What’s the requirement to chase 3G,4G,5G,6G etc when you only actually need to get a reading every few months? You don’t need to be able to transmit a 10 digit number in half a nanosecond, you do need to be able to transmit it reliably from the most akward or remote places, to survive all sorts of interference and to still work reliably in 50 years time with no changes

the money would be better spent on an appropriate technology that won’t be going obsolete in a heartbeat. I see little reason to get a ‘smart’ meter that I know is obsolete tech before it’s installed and know it’ll rapidly change back into a dumb meter at any excuse

We seem to live in a topsy-turvy world, where it’s more important to have everything ‘new & improved’ (even when it isn’t & is not);

‘alternative technology ‘ (that doesn’t work) to replace the appropriate technology that does work,

and basic laws of physics are ignored in favor of politically correct groupthink.

This is why we should be searching the cosmos for intelligent life … because there’s not much of it on Earth.!!