On Monday, Ofgem issued yet another set of consultations into the retail price cap. The key proposals are to review the price cap every three months rather than the current six months, and make a small reduction in the notice given to suppliers of changes to the cap level. There is also a proposal to update the wholesale allowance to ensure that suppliers can recover costs associated with backwardation in forward prices over a reasonable time frame, as well as adjustments to the parameters of the Market Stabilisation Charge. Ofgem intends to implement these changes, if confirmed, from October.

“Our top priority is to protect consumers by ensuring a fair and resilient energy market that works for everyone. Our retail reforms will ensure that consumers are paying a fair price for their energy while ensuring resilience across the sector. Today’s proposed change would mean the price cap is more reflective of current market prices and any price falls would be delivered more quickly to consumers. It would also help energy suppliers better predict how much energy they need to purchase for their customers, reducing the risk of further supplier failures, which ultimately pushes up costs for consumers. The last year has shown that we need to make changes to the price cap so that suppliers are better able to manage risks in these unprecedented market conditions,”

– Jonathan Brearley, CEO of Ofgem

However, while some of these changes are welcome, they do not address the real issue which is the distortive effect of the price cap itself.

Updates to the wholesale price methodology

Ofgem’s minded-to decision on updates to the price cap methodology is now out for consultation and covers three main areas:

- More frequent adjustments to the cap;

- A reduction in the notice periods; and

- Changes to the recovery of backwardation costs.

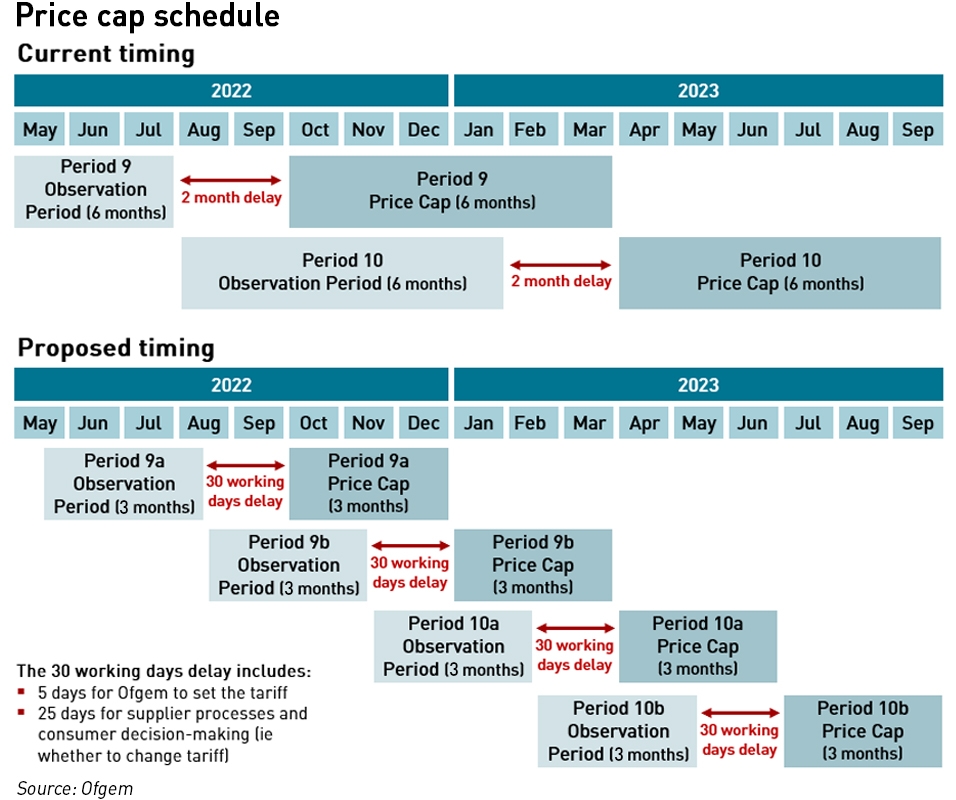

The reason Ofgem is having to make so many changes to the cap is because the cap methodology assumed market price volatility would remain low – there was no consideration of what might happen should a bull run occur in the markets. This was a significant oversight – gas and electricity are commodities, and bull runs are more likely in commodities markets due to the physical dynamics around the way in which supply and demand relate to each other, the need for transportation and storage, and the time taken to bring new sources of supply online, which are not relevant in other markets such as currencies, equities and interest rates (although they can also experience bull runs). As a result, the cap was implemented with reviews only every six months (a limit Ofgem imposed on itself since the legislation only required Ofgem to assess the cap level “at least” every six months).

Ofgem also measures the wholesale component of the cap by looking at average prices over a six month window that ends two months before the start of each new cap period. This means that there is a significant gap between the time at which prices are set and the time when consumers actually pay for their energy. Ofgem assumed that suppliers would buy their gas and electricity in the forward markets over the same time period as the observation window, to minimise the basis risk between the price observation and their actual costs.

“The cap was intended to reflect a fair price for supplying energy for customers less able or willing to engage in the market. It was not intended to become the cheapest tariff in the market and attractive for normally active customers,”

– Ofgem

However, the rapid changes in wholesale prices meant that the capped variable tariff became cheaper than any of the fixed price deals available in the market, so customers stayed on the variable tariff when their fixed price deals expired, rather than moving to other fixed price deals. Suppliers then had to buy gas and electricity for these consumers are much higher prices, and above the amount they were allowed to charge under the cap, the predictable outcome was the failure of a large number of suppliers. According to Ofgem, 23 million out of the total 28 million households in the UK are now on the capped default tariff, with the costs of these consumers moving to the capped tariff costing suppliers £900 million during cap period seven (October 2021 – April 2022). Suppliers face similar risks when prices fall: consumers move onto cheaper fixed price deals and suppliers are left long gas and electricity they bought forward at higher prices that they then have to sell at a loss (since, unlike fixed price deals, there are no exit fees for the default tariff).

To limit suppliers’ exposure to these costs, Ofgem intends to reduce the time between changes to the cap level, thereby reducing the risk that large disparities build up between the prices observed historically in the cap fixing, and prevailing prices at any time which may drive consumers onto different tariffs. The notice periods are being reduced to fit better with the new schedule.

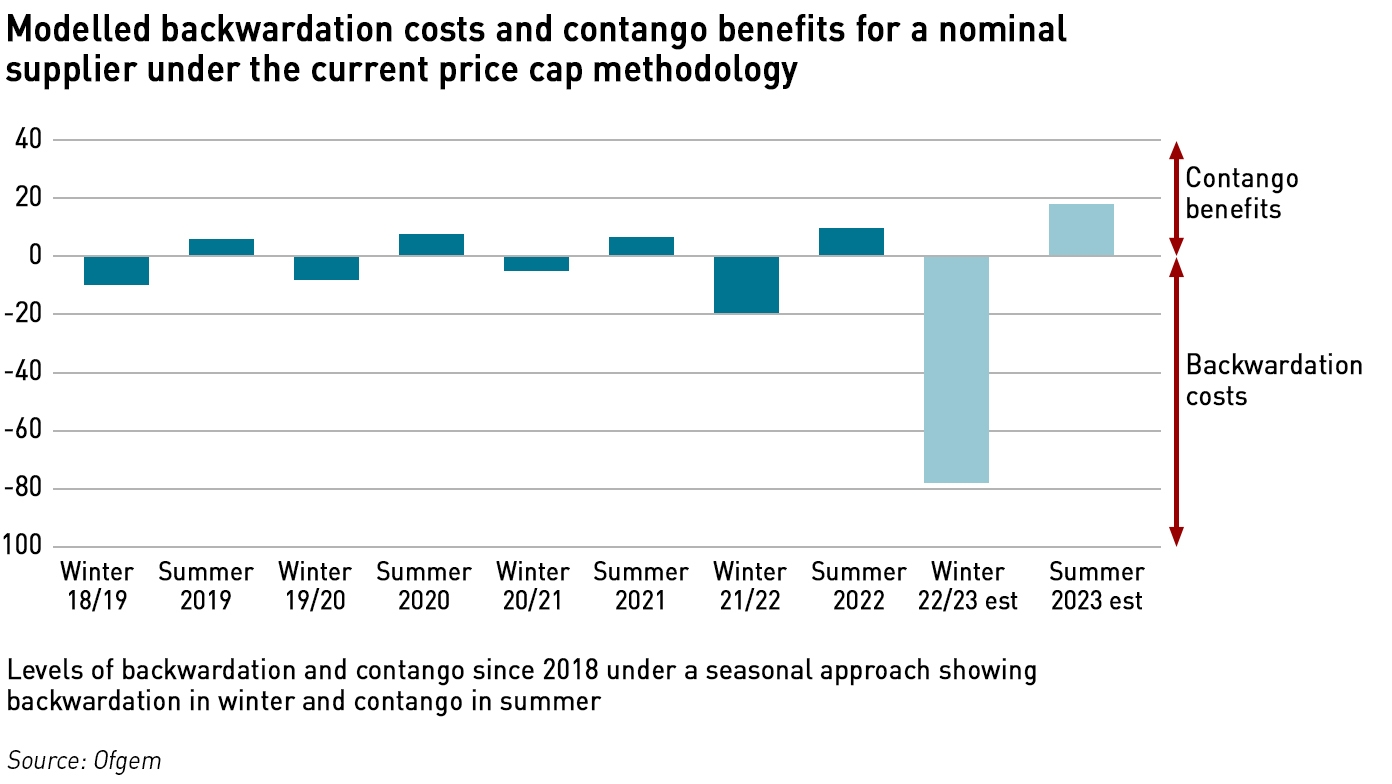

Ofgem is also intending to introduce an allowance into the cap to cover the costs of backwardation. While prices were less volatile, there was evidence that the effects of backwardation would be offset by periods of contango over a relatively short timeframe, and therefore there was no need to make any specific allowance for these costs in the cap. These costs arise again through the cap methodology: although prices are observed over a six month window, these are the specific products are forward contracts going out twelve months giving an annualised price level that is intended to insulate consumers from seasonal differences in market prices. Based on current market prices, there is no chance that the backwardation costs seen in the past few months will be recovered by any future periods of contango in a reasonable timeframe (ie, suppliers should not be expected to wait for years to see these costs covered).

Ofgem is therefore proposing to allow suppliers to recover backwardation costs over a 12-month period with a “deadband” that ensures that the approach only captures costs arising when the market is more volatile than it was in the first six cap periods. The initial deadband is proposed at £9 – £4 for electricity and £5 for gas.

Adjustments to the Market Stabilisation Charge

Back in February, Ofgem announced a set of new short-term interventions to address risks to consumers from market volatility: a requirement for suppliers to make all tariffs available to new and existing customers, and a requirement for suppliers to pay a Market Stabilisation Charge (“MSC”) when acquiring new customers. Both measures were intended to be temporary (expiring on 30 September 2022 but with a six month extension possible), although there are good arguments to make the non-discrimination requirement permanent, reflecting similar rules in the insurance market.

The MSC is a good deal more controversial since this requires suppliers that acquire a new customer to make a payment, under certain circumstances, to the customer’s former supplier. At first glance such a policy sounds preposterous, and Martin Lewis famously lost his temper with Ofgem this week when learning of the lowering of the thresholds for these payments to be made. However, the policy actually makes sense and without it, Ofgem could be at risk of legal action by suppliers when wholesale prices begin to fall.

The reasons are as follows:

Ofgem has been very clear that it expects suppliers to hedge broadly in line with the price cap methodology, and has been very critical of suppliers that have not done this. It is now introducing stress testing that will restrict the ability of suppliers to deviate from this unless they have sufficient capital resources to cover any losses. However, when market prices fall, new entrants may enter the market offering lower tariffs to consumers since they will not have hedged their customer demand at high prices. This would leave the previous suppliers long hedges they no longer need, but being forced to sell their positions at lower market prices, thereby incurring losses.

If Ofgem didn’t act to mitigate this risk, then there would be a significant dis-incentive to hedging, which would be at odds with Ofgem’s preferred risk management approach. But if Ofgem forced suppliers into loss-making actions (by penalising them through the stress testing regime for not undertaking such hedging) that would be manifestly unfair and would leave the regulator open to legal challenges from suppliers who could legitimately argue that following the rules caused them significant losses.

In the extreme, these losses may lead to further supplier failures, which is another reason that Ofgem needs to act: some of the losses incurred when a supplier fails are socialised across all consumers, so consumers pay a cost when a supplier fails. The final reason that Ofgem needs to address this is that by allowing new entrants to undercut existing suppliers in this way, a subset of active and engaged consumers might benefit from lower tariffs, but dis-engaged consumers would not benefit and would face a risk of additional costs. Since dis-engaged consumers also tend to be disadvantaged in other ways, this would be effectively an economic transfer from less well off to more well off consumers, which is also unfair.

“We do not consider that we should prioritise the lowest possible prices for consumers at the present time over the need to enable efficient suppliers to finance their businesses. Doing so would mean that pricing would not cover efficient costs, which would risk severe detriments,”

– Ofgem

So while Martin Lewis was angry that he thought the MSC would reduce the availability of cheap tariffs in the market – which is correct – these cheaper tariffs would come with risks that would harm the most vulnerable consumers, and that is an important reason for Ofgem to act. The MSC was introduced as an alternative to allowing exit fees on some standard variable tariffs.

Under the original proposal, payments under the MSC are only triggered when wholesale gas and/or electricity prices fall below a defined trigger level of 30% below (ie at 70% of) the implied price cap wholesale element for the relevant period (ie summer 2022). When such a threshold is met, Ofgem will publish the charge each week on a volumetric basis (eg in £/kWh). A de-rating factor is used to determine the percentage of the incremental supplier hedging losses which are covered by the MSC, and this was set at 75%.

Ofgem has now decided, subject to this final consultation, to adjust these parameters to a threshold of 10% and a derating factor of 85%. Ofgem believes these levels can still deliver some benefits to consumers of falling prices, and ensuring that suppliers manage some of the risks of price volatility themselves, without the risk of undue financial stress to suppliers as a result of falling prices. Ofgem intends to launch further price cap consultations in June, including on an extension of the MSC to the end of March 2023.

Time to ditch a bad policy rather than tinkering with the rules

In its consultation, Ofgem is explicit that the price cap is going beyond its intended purpose in a way that is damaging to suppliers and exposes consumers to the risks of the costs associated with supplier failure.

“The default tariff cap (‘the cap’) was established to protect customers who did not engage in the retail market and was designed for much more stable market dynamics. The structure of the cap has played a significant role in how this market volatility has been passed through to suppliers and customers. The cap’s methodology has meant it has protected an increasing number of customers – around an extra 7 million since its introduction – from the full extent of the price increases and the costs suppliers face. But this has placed a strain on suppliers – exposing them to hard to manage risks and costs not specifically accounted for in the cap. This pressure will continue unless changes are made to the methodology and suppliers are able to recover the efficient costs they face in providing this tariff to customers,”

– Ofgem

In other words the price cap is being used as a means to force suppliers to subsidise consumers. This is far beyond the scope of its intended purpose, and makes me wonder whether Ofgem, in recognising this so explicitly, is opening itself to legal risk: it is not the job of the regulator to determine a distribution of wealth from businesses to consumers. That this has happened, as Ofgem states, as a result of the methodology Ofgem itself determined, appears to be significant regulatory over-reach. To correct this, not only should Ofgem make cap adjustments more frequent, it should write a public letter to ministers highlighting this unintended consequence of the cap.

While supporting consumers at the expense of suppliers may be politically appealing, this is one of the reasons for the sclerotic nature of the market – MPs recently complained about a lack of innovation in the sector, but is it any wonder that suppliers are reluctant to put capital at risk when they operate in a structurally loss-making, over-regulated market where any returns they manage make are immediately sucked away. Ministers are expressing squeamishness over the proposals for windfall taxes on oil and gas producers (and for good reason) but seem oblivious to the greater harms they have created in the retail gas and electricity markets.

It is also interesting to note another policy contradiction: the price cap was designed to protect consumers who failed to seek out cheaper tariffs which were assumed to be in their best interests, and yet at the same time the Government expects consumers to respond to price signals in order to reduce consumption to meet environmental goals. The rationale behind recovering the costs of renewables subsidies from bills was that if the “polluter pays” then there will be an incentive to reduce demand (and hence pollution and hence costs). So consumers are on the one hand being protected from not responding in one way (switching) to price signals while being penalised for not responding in a different way (demand reduction) to those same price signals.

It is more important than ever that the price cap is abolished. The cap and its poor implementation by Ofgem was responsible for the failure of a large number of suppliers last year; it contributes to lack of innovation and effective competition in the market (with tariffs clustering around the cap level) and it has created a manifestly unfair subsidy of consumers by suppliers.

It would therefore make sense to remove the price cap and replace it with a social tariff for energy, targeted at the fuel poor, and funded (at least in the short term) by taxpayers. This would have the benefit of being targeted at those most in need, and could be used to correct the current situation where the poorest consumers – those on pre-payment meters – pay the highest rates for their energy. Of course, the devil would be in the detail – the actual costs to suppliers of providing this tariff would need to be determined, and the difference between these costs and the amount received from customers entitled to receive the social tariff paid promptly. These calculations could involve similar assumptions to the price cap methodology, unless the suppliers’ actual costs were used, but then there would be a risk that suppliers would not manage these costs efficiently, or that they might create some cross subsidies to other customer groups.

These are difficult challenges to resolve, but it is no-one’s interests to maintain the status quo. The Government should seize the initiative and use the cost-of-living crisis as an opportunity for radical reform with benefits targeted at those in most need. The energy retail segment should be further de-regulated with many of the non-supply obligations removed (there are more suitable agencies for the ECO, WHD, collection of green levies and installation of smart meters), and banking-style regulation should be introduced (alongside an energy equivalent of the FCA Principles) to ensure customer money is protected.

Replacing the price cap with a social energy tariff would not only help consumers it would also remove a major source of distortion from the market. Then we might see high quality entrants with genuinely innovative business models entering the market, offering a wider value proposition to consumers.

Every time I hear of OFGEM or politicians decreeing what optimal hedging strategy should be it gives me conniptions. Ed Miliband famously called for his price freeze right at the top of the market, which then fell for at least 2 years afterwards and only regained the levels he wanted to freeze at when the present crisis erupted last summer. Perhaps that experience lies behind OFGEM’s current thinking. At least they are beginning to get away from trying to promote unhedgeable bases to some extent.

A look at the forward open interest structure, and volume of trading data on the futures markets gives some idea of relative market liquidity. TTF shows more market depth than NBP, and shows some seasonal pattern of open interest, whereas NBP does not. However they are small beer relative to the volumes actually delivered. Any serious hedging takes place in OTC markets.

As you have previously demonstrated, there is a huge amount of shape risk from settlement period to settlement period particularly in the light of highly volatile balancing markets , whereas OFGEM are worrying about converting seasons into quarters. Being hit for £4,000/MWh over 100MWh is the same as being hit for £4/MWh over 100GWh. I have proposed before that smaller suppliers should be required to sign up to intra month balancing services where they would pay an average charge, leaving them free to hedge in the fungible markets. OFGEM need to address this issue as part of a general topic on hedging.

From the consumer point of view there is a cashflow issue that arises from higher demand in winter months. At the moment it seems that suppliers are in fact on average taking advantage of consumers by forcing them to build a credit balance over the summer to finance the winter. There should be transparency on this, with positive balances earning interest and negative ones paying it, with rates set at levels to dissuade suppliers from seeing it as easy financing. Obviously there have to be safeguards against negative balances become defaulting customers. It’s really a banking product though.

In the same way there needs to be transparency on other forms of hedging. Logically poorer customers probably need the protection of a cap in the form of an Asian call option (which has the advantage of being somewhat cheaper as it deals in averages). This would have the advantage that if prices fall they would be able to benefit, as well as benefiting from the price ceiling, but the option itself would have to be paid for, and its effective payout should be transparent in calculation. It could be a standard item for anyone on benefits, and potentially offered to all: the main issue might be what would be appropriate ceiling strike prices in the light of market conditions. Fixed price deals would be an alternative that comes with no benefit should prices subside. Either way, volatile markets make for volatile pricing. It should be up to government, not OFGEM to decide on any welfare support element. Of course, that would mean they might have to acquire some expertise, which would be no bad thing.

Hedging is insurance, and it can be expected to have a cost. It would probably be cheaper to have a separate hedging market where hedges of your choice could be bolted onto your bill. Some transparency about the cost of hedges would help: they are all complex derivatives that the average man or woman in the street is poorly equipped to evaluate, especially when they are wrapped up in an overall deal. An advantage of organising in this way is that hedges become independent of the actual supplier, or indeed, property – move and take your hedge with you, at least for a fixed volume you contract for. It might even be possible to split a hedge between divorcing couples. Another big advantage is that suppliers could all be left with simply targetting acquiring energy against a fairly prompt based benchmark (monthly, perhaps to tie in with futures markets and the proposal for intra month shaping services), with little need for longer term hedging, de-risking their businesses. The hedging would be done by properly financially sound entities, monitored by the FCA. If larger suppliers wished to establish their own well backed subsidiaries to compete in this area they would of course be free to do so. The prices on hedges would of course vary with market conditions, and early termination terms should also be clearly set out. All the issues about OFGEM calculating “backwardation allowances” (in reality a recognition that the OFGEM hedging basis is unrealistic) etc. disappear. Price comparison sites might get a new lease of life offering consumer advice about the available offers in the market and tailoring the choices to their needs and risk profiles. They would also need to be FCA regulated, with people who understand the underlying derivatives at the helm.

That leaves volume risks that come from variations in weather, demand variations due to price, and due to gain and loss of customers. Whatever the source of variation it could be handled by options, or even options on options. Many of these disappear if you remove longer term hedging as a responsibility of suppliers.

The real gains for consumers do not come from these financial toys, which are tinkering. They can only come from establishing a properly competitive market, aimed at lowering costs overall. That of course is a separate topic, and quite incompatible with attempts at net zero.

“It’s really a banking product though.” – exactly why this is a matter for financial regulation and not Ofgem!

Overall I agree with the idea that volumes are smoothed for consumers by having them pay more in summer and less in winter – most people do not earn more in winter so a pay-as-you-go model would create a lot of volume-based cost variability that would be hard for them to manage.

That being said, consumer credit balances should be ring-fenced. It’s interesting that only Centrica, a company subject to financial regulation due to its boiler insurance business, does this. I’m less sure about paying or charging interest on the balances though – that can get complicated, and consumers who join a supplier in winter wih annualised pricing could face quite a bit in initial interest costs if interest rates go up, which I think is now likely. In a world of 10% interest rates that could become very painful. On the whole I think the interest would net off, and since supply is such a low-margin business, I don’t see why suppliers can’t get some benefit from it given that mostly it would net off.

What I find very interesting about the market is the way in which it has dis-integrated in the past few years…by this I mean that many previously vertically-integrated companies have sold off parts of their businesses and now focus on only one part of the value-chain. Only EDF is still conventionally vertically integrated with thermal, nuclear and renewable generation as well as a supply business, although E.On has renewable generation alongside supply. Hardly any other supplier owns any other meaningful amount of generation.

Owning generation would be a natural hedge for suppliers, but the fact that hardly anyone is following this model illustrates how broken the market has become – it is not worth having so much capital tied up in generation when the economic models for generation are also very challenged. Nuclear has upfront costs that are beyond the reach of private companies, thermal generation has declining utilisation rates with policymakers actively trying to get rid of it, and renewables are largely uneconomic without subsidies.

The entire market needs complete reform, but unfortunately both BEIS and Ofgem are focusing on completely the wrong areas…