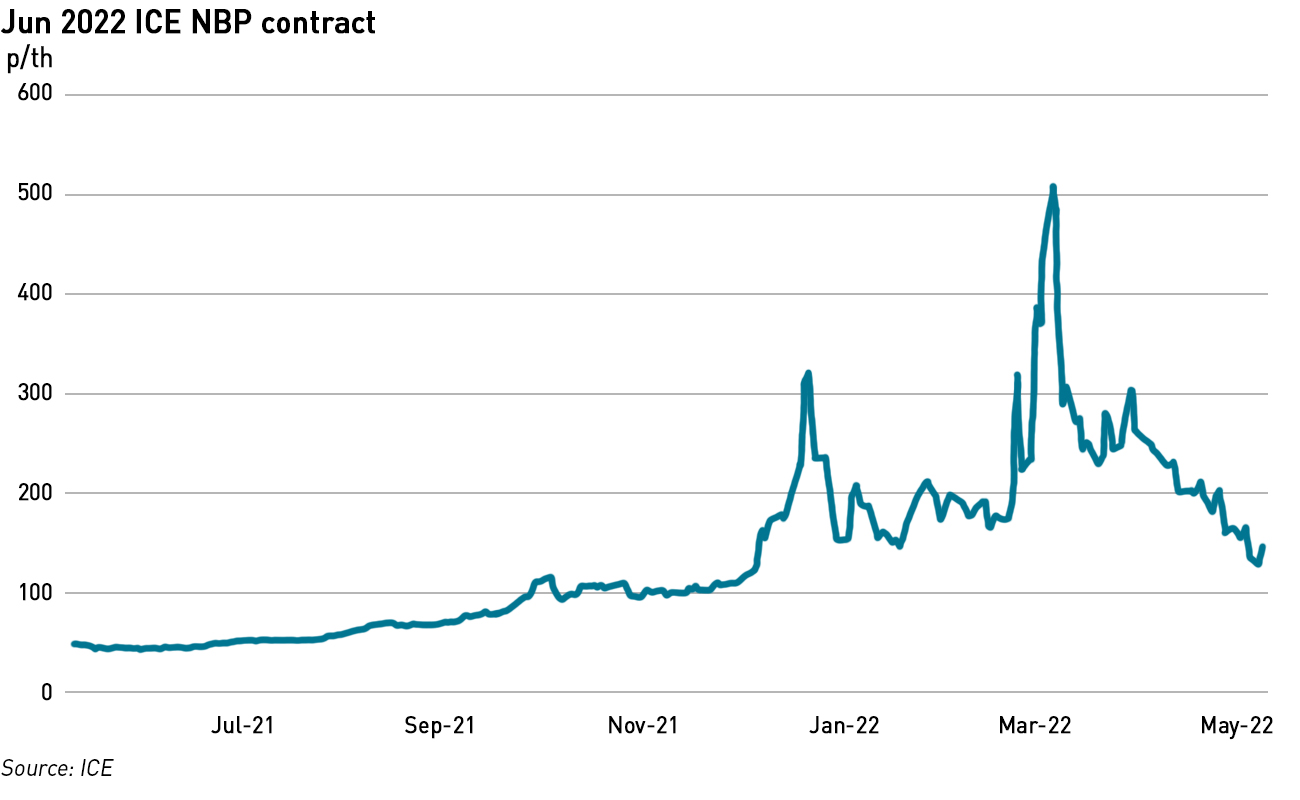

Gas prices have been continuing on their volatile journey as they respond to the global imbalances resulting from the pandemic, as well as the developments around the war in Ukraine. As the chart shows, UK gas prices have been extremely variable in recent months.

Gas prices driven by market imbalances and the impact of war

The fundamental driver of the price increases last autumn was a mis-match between the speeds with which demand and supply recovered from covid. Before the pandemic, global gas production and consumption both increased at a compound rate of roughly 3% a year for around a decade. However, in 2020, demand fell by 2.1% – the largest fall since the financial crisis in 2009 – resulting in a sharp reduction in drilling and capital investment across the industry, leading to an unprecedented decline in worldwide output. Production fell by 3.1%, the largest decline since at least the 1970s.

Winter 2020-21 saw prolonged cold weather across Europe and North America, particularly towards the end of the winter, causing storage levels to fall significantly. In a normal year, gas inventories would re-fill over the summer when heating demand is low, but this did not happen last year for a number of reasons.

Winter 2020-21 saw prolonged cold weather across Europe and North America, particularly towards the end of the winter, causing storage levels to fall significantly. In a normal year, gas inventories would re-fill over the summer when heating demand is low, but this did not happen last year for a number of reasons.

Heat waves across the northern hemisphere (except in the UK which largely escaped the hot weather), and in China, boosted demand, as did coal shortages in India and a lack of hydro-electric generation due to drought in Brazil.

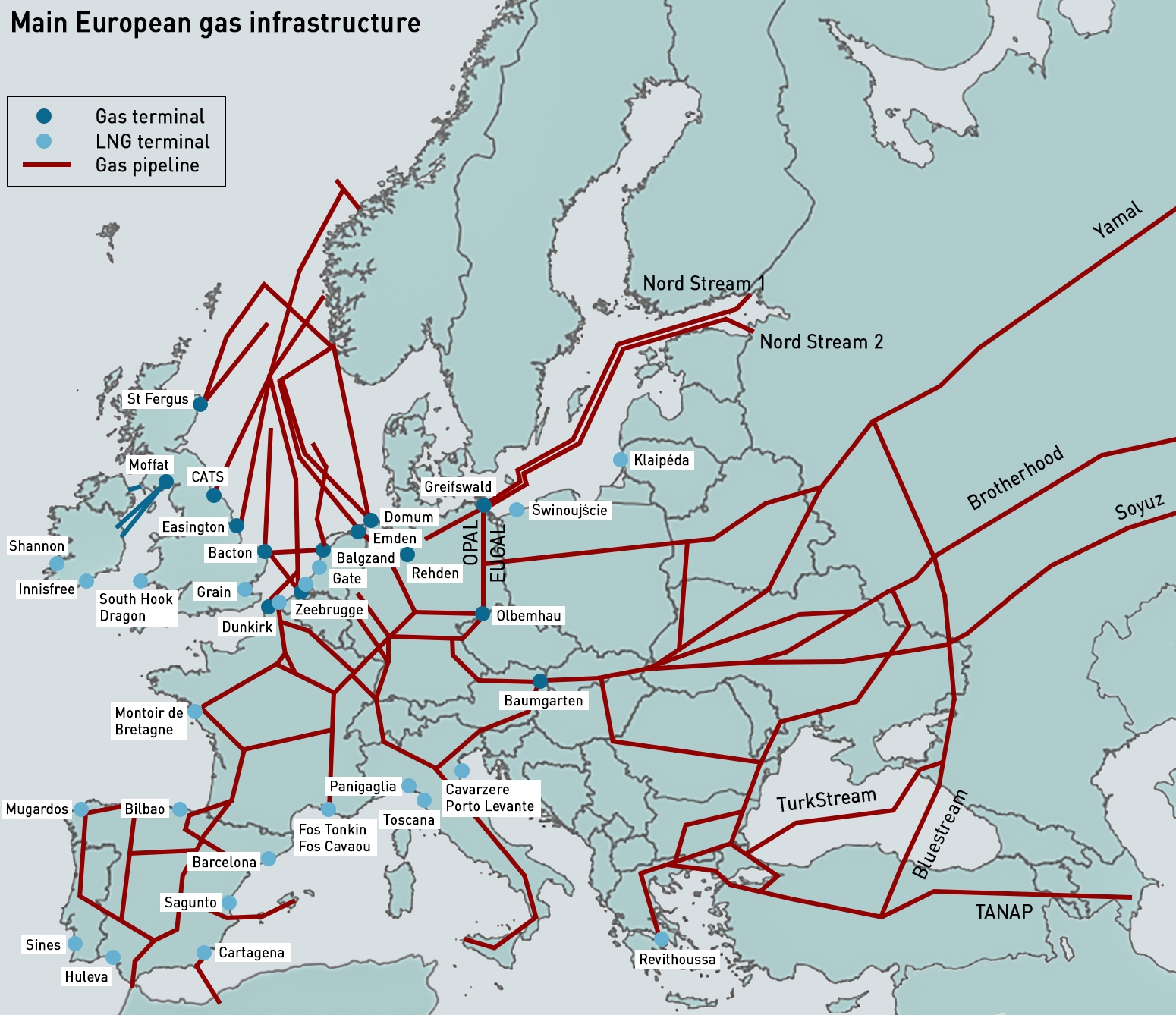

Extended field maintenance in Norway after maintenance work was delayed in 2020 due to the pandemic, restricted supplies. There were also reduced flows from Russia during the summer, which some attributed to a desire to exert political pressure in relation to Nord Stream 2 but there was also a fire at condensate treatment plant in Western Siberia in August which didn’t help.

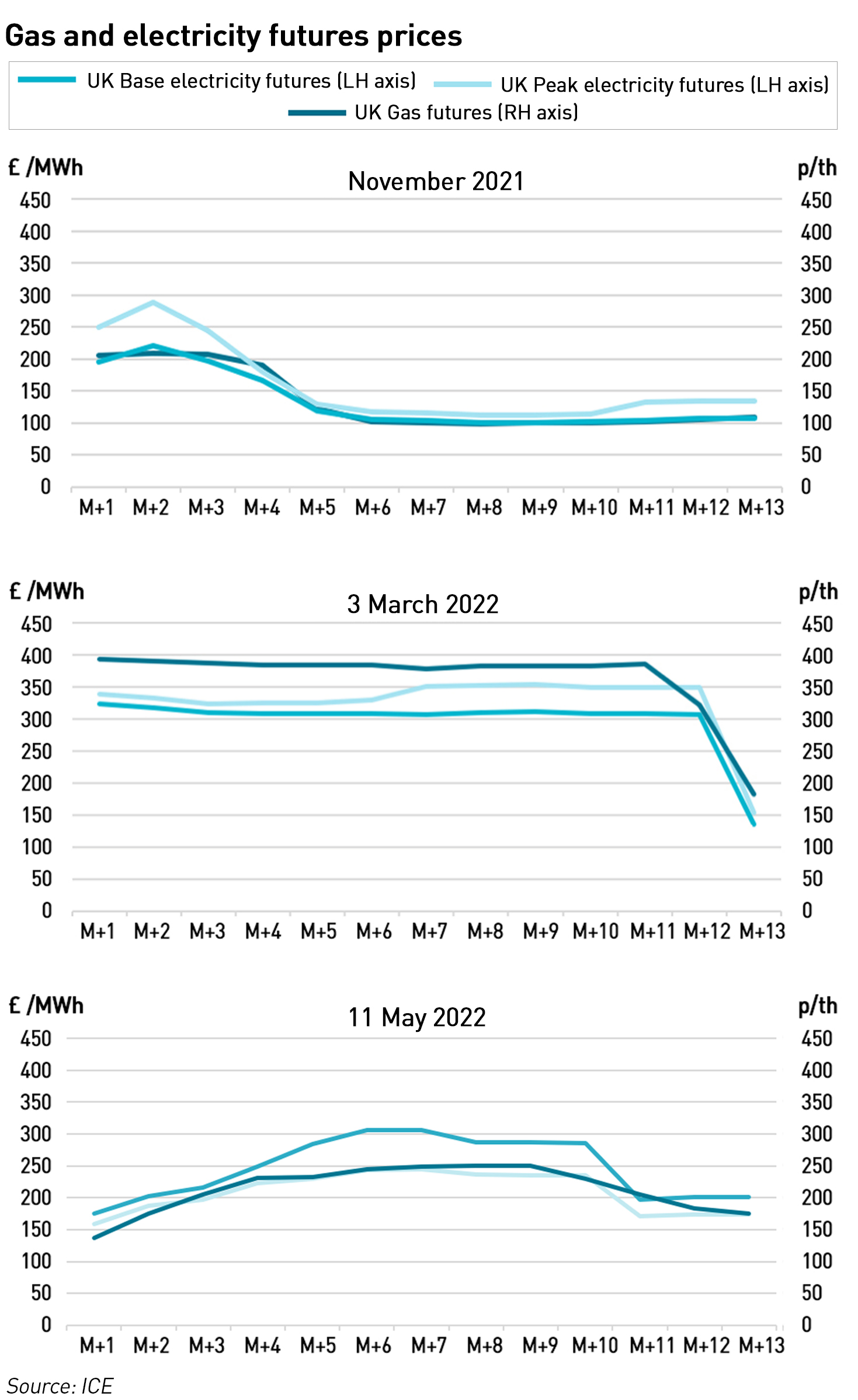

Late last year the markets were expecting that supply and demand would re-balance sometime in 2022, possibly after the summer, and this was broadly reflected in forward prices.

The next few months saw significant changes. At the beginning of 2022, Europe attracted significant LNG supplies from the US. Then the Russian invasion of Ukraine changed market dynamics significantly, as European countries sought to reduce their reliance on Russian gas.

More or less the entire liquid portion of the forward curve shot up to essentially the same level in response to the invasion. The dip out to a year shown in the charts was probably more a reflection of low liquidity than anything else. However, within days, the contracts beyond the prompt began to fall in price.

Now we can see that the middle portion of the curve has fallen slightly but the front has fallen significantly, as LNG deliveries into the UK boost supply.

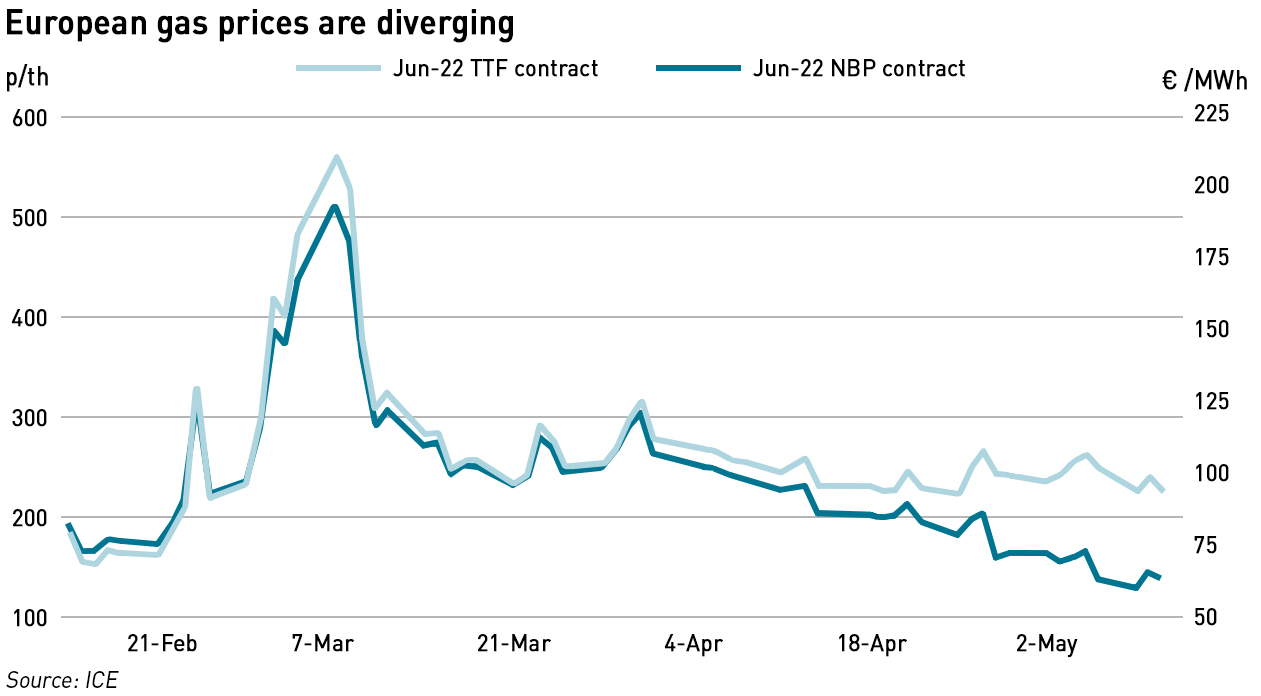

UK and European gas prices diverging

However, the past month has seen gas prices in the UK and Europe have begun to diverge. NBP and TTF usually trade within a tight range, but the spread between them has now grown to more than €30 /MWh. This price divergence from TTF is not limited to the UK – French and Spanish prices are also trading at a discount to the main European hub price. This is driving similar electricity price divergences.

The main reason for this growing difference is access to LNG. France, Spain and the UK all have significantly more LNG regasification capacity than the Netherlands. Indeed, there are reports that National Grid is limiting LNG imports into the UK due to storage constraints. There have also been pipeline constraints between the UK and Continental Europe limiting the scope for price convergence.

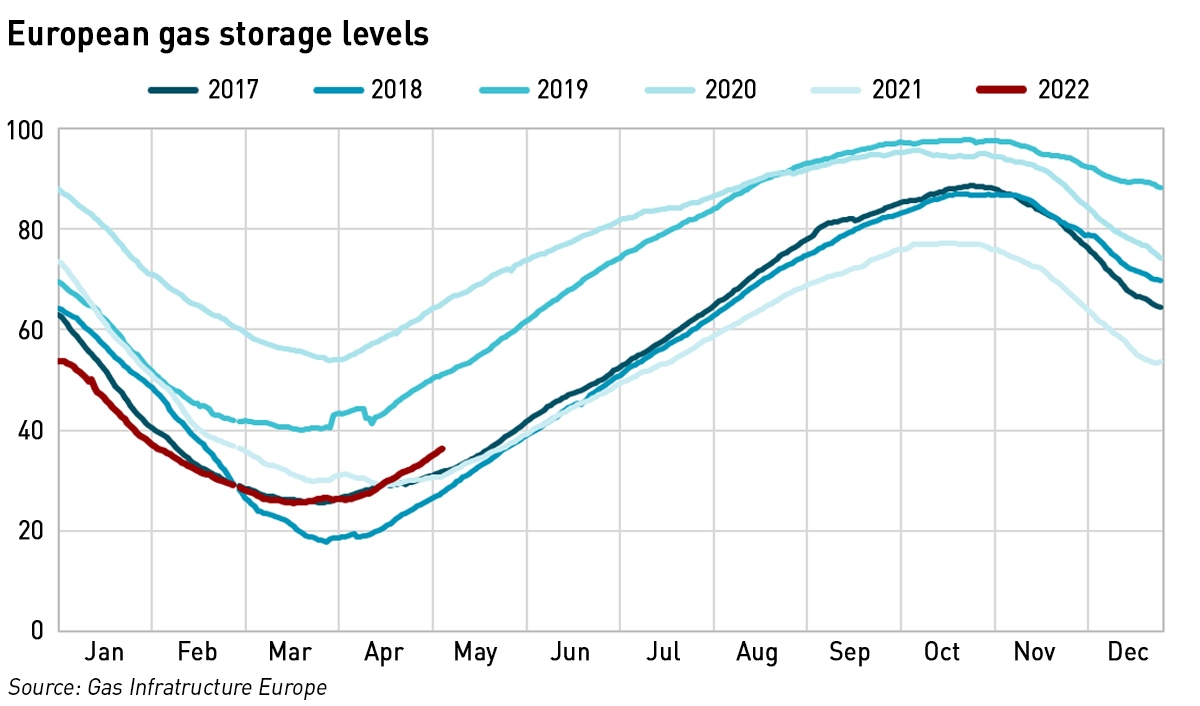

The pressure to divert gas into storage facilities on the Continent is also fuelling the price divergence: as the UK lacks significant storage capacity, the need to build inventories has a much more muted impact on demand. In response to the war in Ukraine, the European Commission outlined its intention to require underground gas storage across the EU to be filled to at least 90% of capacity by 1 October each year. To put this target in context, in only two of the past six years have inventory levels exceeded 90% (although in one year they were only very slightly under) at the beginning of winter.

At the start of this year’s injection season on 1 April, EU gas storage facilities were 26.4% full, which is at the lower end of what is normal for the time of year, but a mild winter and an influx of LNG helped levels to recover.

Market prices jumped on the news of the storage mandate, forcing the Commission to modify its proposal for this year to a target of 80% full by 1 November, rising to 90% in future years. Storage levels are now just over 36% full but still towards the bottom of the five-year historic range.

In the past week there have been further changes. Gazprom indicated it will cut shipments to Europe the Yamal pipeline, after the Kremlin imposed sanctions on European gas companies. The sanctioned companies include some former Gazprom units as well as Europol Gaz, the pipeline’s owner. The sanctions prevent Russian entities from selling gas or transacting with Gazprom Germania, which was nationalised by the German government last month.

“A ban on transactions and payments to entities under sanctions has been implemented. For Gazprom this means a ban on the use of a gas pipeline owned by Europol Gaz to transport Russian gas through Poland,”

– Gazprom

Also last week, Ukraine’s pipeline operator shut down flows from one of the two major pipelines transiting the country, citing interference from Russian occupying forces, and saying it no longer controlled the relevant infrastructure enabling use of the Sokhranivka entry point. It maintains that Gazprom can ship gas through an alternative pipeline in Ukrainian-controlled territory using the Sudzha interconnection point.

“As a result of the Russian Federation’s military aggression against Ukraine, several GTS facilities are located in territory temporarily controlled by Russian troops and the occupation administration. Currently, GTSOU cannot carry out operational and technological control over the CS ‘Novopskov’ and other assets located in these territories. Moreover, the interference of the occupying forces in technical processes and changes in the modes of operation of GTS facilities, including unauthorized gas offtakes from the gas transit flows, endangered the stability and safety of the entire Ukrainian gas transportation system,”

– Gas TSO of Ukraine

Gazprom has claimed the alternative route is “technically impossible” although analysts have pointed out that the Russian military is targeting Ukrainian fuel depots and supplies. While this is not creating an immediate crisis in the European markets, it is a sign that both sides in the conflict are increasingly willing to use energy for leverage, and this may create further tensions in the markets when gas demand increases.

What all of this means for the gas markets over the next few months is anyone’s guess. It seems reasonable to expect UK and European prices to continue to diverge through the summer as any restrictions on Russian flows in addition to the storage mandate will support prices, while the UK’s more just-in-time market looks well supplied into the summer. However, come the winter, the UK’s lack of inventories may well see prices rise as demand ramps up, narrowing the gap. Europe is likely to trade at a premium through the winter if flows from Russia remain constrained, with the potential for prices to rise significantly if supplies are materially reduced.

There have certainly been a lot of LNG tanker arrivals into Milford Haven over the last couple of months but according NG gas operational data LNG storage this morning its still c2TWh below full capacity assuming no operational restrictions. Also with wind being below average output (again) we’ve been burning plenty of gas with coal barely being used (given we get most of our coal from Russia maybe wise but also several units were destined to close so maybe have no stocks on hand). Over last month r LNG has been providing 25-35% of total gas demand on some days with rest from N.Sea input but as I write this LNG is well down and the two i/c’s to Belgium and Netherlands are taking 40% of total demand. Like the leccy grid we’ve suddenly become a big exporter of energy which is fine through summer but not sure either system can support full export capacity as well as domestic demand on a really cold winters day. One hopes summer mtce of the energy infrastructure isn’t being deferred to gain income at the expense of reliability down the line.