Today the Business Secretary, Kwasi Kwarteng, has raised the prospect of nationalising parts of the electricity industry. Of course, it isn’t couched in those terms, but the Government has announced that it will appoint a Special Administrator to run any supplier that fails if Ofgem is unable to appoint a Supplier of Last Resort (“SOLR”). This would be the case should one of the larger suppliers fail.

“If the appointment of a Supplier of Last Resort is not possible, Ofgem and the Government have agreed processes in place to appoint a special administrator to temporarily run the business until such time as a new supplier can be found for the customers.”

In practice, this would mean that the state would take control of the business and finance it until such time as it could be either wound-up or sold. In other words, a bailout.

This comes on the same day that the FT reported the seventh largest supplier, Bulb Energy has engaged investment bank Lazard to help it to secure new sources of funding. The company, which supplies 1.7 million customers, has been consistently loss-making, and is reportedly exploring options including a potential joint venture or merger. A rival supplier has apparently described the company as “too big to fail” leading to speculation that the Government’s bailout moves potentially relate to Bulb.

Avro Energy, Symbio and Green Energy have also been identified as potentially being in difficulties.

Are the requirements of the price cap being met?

Section 1.6 of the Domestic Gas and Electricity (Tariff Cap) Act 2018 states that:

The Authority (Ofgem) must exercise its functions under this section with a view to protecting existing and future domestic customers who pay standard variable and default rates, and in so doing it must have regard to the following matters

- the need to create incentives for holders of supply licences to improve their efficiency;

- the need to set the cap at a level that enables holders of supply licences to compete effectively for domestic supply contracts;

- the need to maintain incentives for domestic customers to switch to different domestic supply contracts;

- the need to ensure that holders of supply licences who operate efficiently are able to finance activities authorised by the licence.

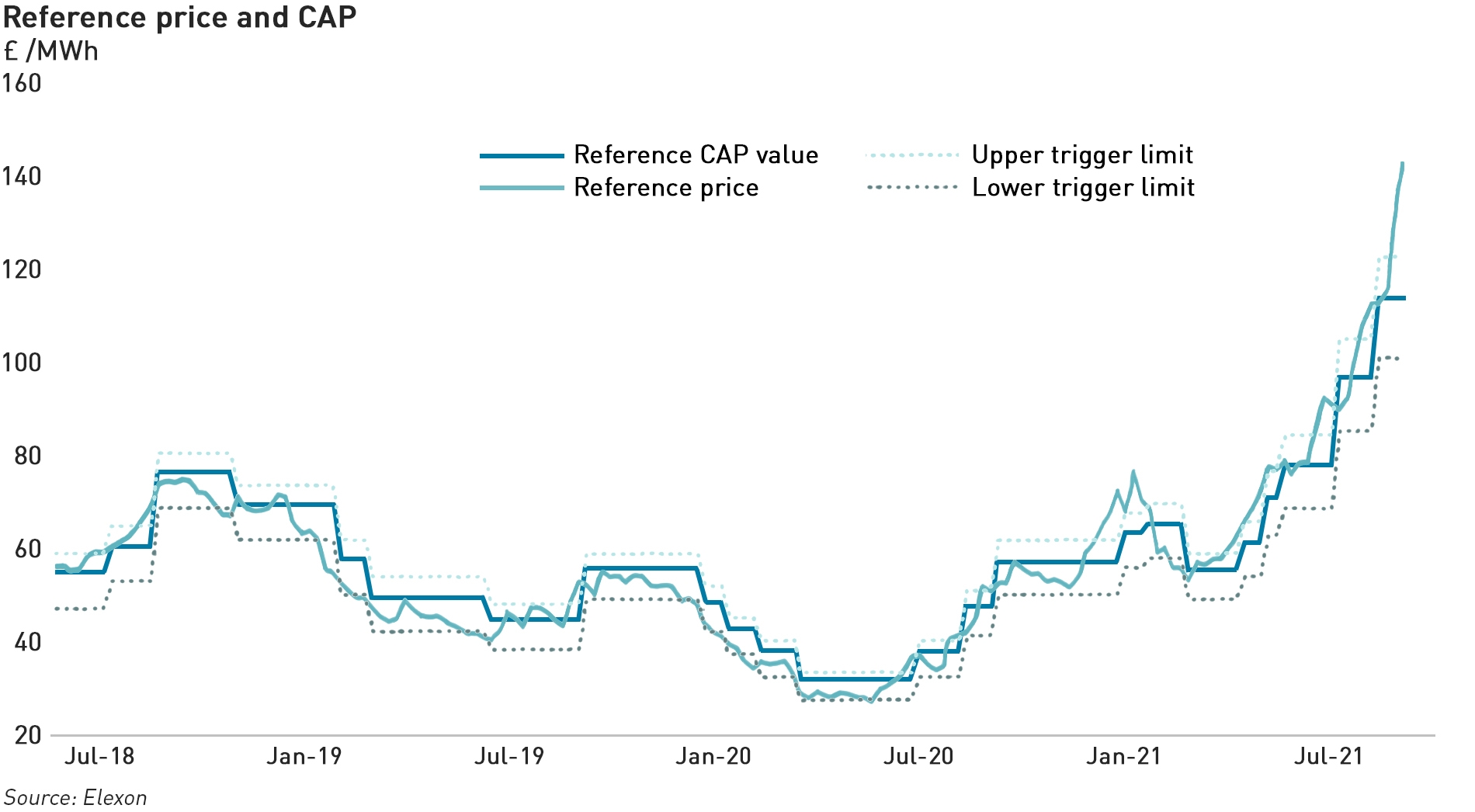

Ofgem is required to give at least 28 days’ notice of any change. The Act requires the cap to be reviewed at least twice a year, but doesn’t limit Ofgem to this, so in theory the cap could be re-set again, but the notice period set out in law limits Ofgem’s ability to respond quickly to market changes. It also means that suppliers have to wait two months before any increase can be put into effect since they must give 30 days’ notice to their customers.

Arguably the current price cap is failing to meet the statutory requirements set out in the Act. It is clearly not set “a level that enables holders of supply licences to compete effectively for domestic supply contracts” or ensuring “that holders of supply licences who operate efficiently are able to finance activities authorised by the licence.” The current problems facing suppliers are not linked to lack of operational efficiency and being in financial distress makes it difficult to attract finance.

It’s clear that the Act did not anticipate such rapid changes in market conditions as have emerged in the past few weeks, and there is simply no mechanism for Ofgem to respond quickly. The Government needs to give Ofgem emergency powers to suspend the cap and allow suppliers to reduce the notice period to consumers.

Longer-term the price cap should be removed, and the lessons from other markets learned, such as California in the 2000s when a similar price cap lead to multiple large-scale blackouts, the collapse of one of the state’s largest energy companies, bailouts and mass-redundancies.

So how exactly did it come to this?

Other than a widely ignored proposal from the Labour party to re-nationalise energy networks in 2019, there has been no meaningful discussion of state-ownership of energy markets in decades, so today’s announcement which opens the door to bailouts reflects the severity of the current situation.

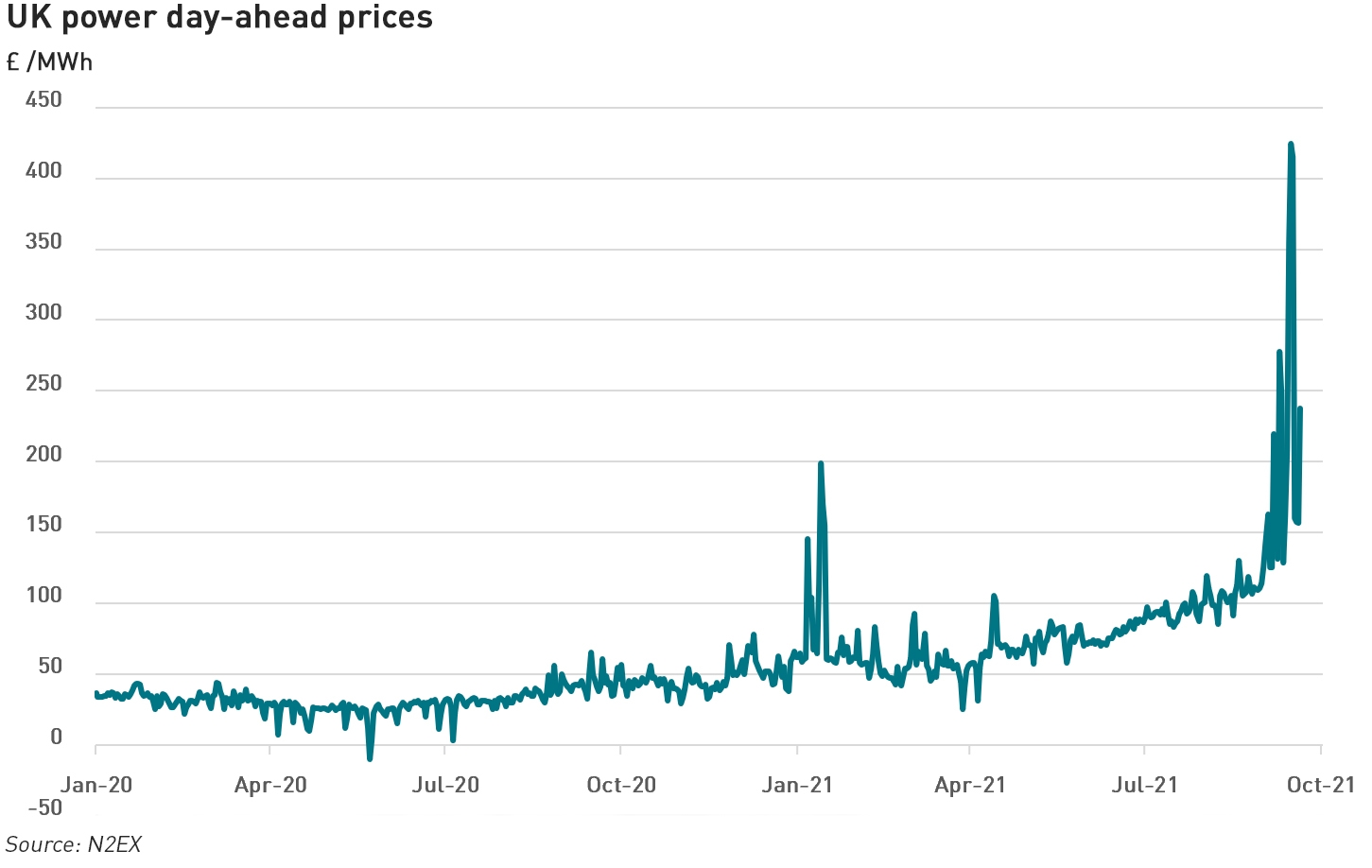

Over the past few weeks we have seen a sharp increase in gas and electricity prices on top of the steady doubling that had happened over the previous year. This has led to the swift exit of five suppliers in recent weeks. There are several reasons for this sudden supplier stress.

Firstly, smaller suppliers struggle to access the hedging they need due to a combination of unaffordable credit requirements and the volumes they need to hedge shape risk being too small for the market.

Secondly, prices rises are out-stripping increases in the price cap which in pratice is only re-set twice a year. The only way to circumvent this is to either become exempt from the cap by getting a “green” derogation (the rules are strict and it takes time), or to switch consumers to higher-priced fixed tariffs which can be above the level of the cap. However there are two challenges with offering fixed price tariffs – if they are not hedged then the supplier is very exposed to any price rises, and suppliers are required to give their customers 30 days’ notice of any tariff increases.

“The current situation of rising energy bills is nothing to do with the effectiveness or competitiveness of the energy retail market, we are already in a challenging position since the advent of the price cap on suppliers and the industry in aggregate has been loss-making. The price cap on suppliers doesn’t affect global commodity prices or the price paid to generators and that’s where the current price pressures are coming from,”

Michael Lewis, Chief Executive, E.On UK

Thirdly, there are behind-the-scenes costs that require suppliers to post collateral with various parties to cover the risks of non-payment. The most important one of these is the credit cover they must place with Elexon, but collateral must also be provided to the bodies administering the CFD scheme and Capacity Market, among others.

Elexon increased the Credit Assessment Price on which the amount of collateral is based from 8 September (£96 /MWh to £113 /MWh) and has announced another increase from 5 October (£113 /MWh to £137 /MWh). This means that in the space of a month, suppliers will have to increase the amount of collateral they provide to Elexon by 43%. For suppliers living hand-to-mouth, this is a lot of additional cash to find.

Then there is the looming late payment deadline for the Renewables Obligation. Many smaller suppliers fall into the trap of using their RO receipts as working capital and then struggle to make payments into the buyout fund. The interest rate on late payments (for the two months between the initial deadline on 31 August and the late payment deadline on 31 October) is only 5% over the Bank of England base rate, which many consider to be effectively a cheap form of finance, so they strategically delay payment.

Unfortunately, there are so many higher priority stresses just now, the logical decision for suppliers would be to simply default on the RO and hope they can survive the consequences – ultimately they can lose their licences but Ofgem might prefer to negotiate than see a large number of suppliers all pushed out of the market at once.

Consolidation now the most likely outcome

The consequences of all of this are interesting. Utility Week reported that on 17 September Compare the Market informed consumers that its price comparison services had been halted since suppliers were limiting the tariffs on offer, and that there were few available tariffs on other price comparison sites. One thing suppliers are not required to do is to provide a market in new tariffs. Some are now predicting a return to the market concentrations seen in the early years of privatisation.

Since the start of 2018, 37 small electricity suppliers have left the market, and there have been significant business re-organisations among the larger suppliers:

- Centrica, trading under the British Gas brand, has sold most of its generation assets and is no longer vertically integrated, although it still retains a large share of the retail market, now at just under 18%;

- E.On continues to have a large retail presence and owns a significant renewable generation portfolio, however it divested its conventional generation to Uniper in 2018. It has just over 17% of the retail market;

- npower was absorbed into E.On following an asset swap between E.On and npower’s parent company RWE. The brand was subsequently discontinued with customers being transferred into E.On UK;

- Scottish Power sold its generation assets to Drax in 2019 and is no longer vertically integrated. It has a 9% retail market share;

- SSE sold its customer business to challenger supplier Ovo Energy and now focuses on renewable power generation and networks businesses;

- EDF Energy is the only one of the Big 6 that continues to operate as a vertically integrated supplier owning both conventional and renewable electricity generation in addition to supplying both business and retail consumers, and has an 11% share of the domestic market.

According to Ofgem data, the Big 6 had over 99% of the retail energy market in 2004, and retained a more than 90% share until 2015 when challenger suppliers began to make inroads. In March 2021 there were 44 companies selling electricity to domestic customers, down from a high of 63 in early 2018. Four companies, only three of whom were part of the Big 6, held 60% of the market: British Gas, E.On. EDF and now Ovo Energy which has 14%. A further three companies have a 22% share: Scottish Power (9%), Octopus (7%) and Bulb (6%). The remaining 17% of the market was shared between 37 smaller suppliers.

Obviously, since those data were published in July for the period up to 31 March there have been further changes, but this gives a sense of the levels of market concentration – so far this year, EDF, E.On and British Gas have shared most of the SOLR duties. The effect of failures since that date is to increase concentration since the SOLRs are typically taken from among the group of top seven suppliers – People’s Energy and Utility Point, left well over half a million customers to be acquired by a SOLR.

There are concerns in the market that no-one wants to take on SOLR responsibilities. Not only are all suppliers losing money on energy supply, but the SOLR is required by law to honour customer credit balances, and while the amounts funded can be recovered through an industry levy, this process can take up to two years during which time the SOLR is required to fund the amounts in question. Where suppliers are under stress there is a temptation to increase customer direct debit payments in order to boost short-term working capital, and seasonally credit balances tend to be higher at the end of the summer since summer demand is lower, so it could be that SOLRs are looking at higher credit balances that would usually be the case.

Meanwhile the BBC is reporting that four suppliers are currently soliciting bids from other suppliers for their customer books, effectively seeking to exit the market, while others are speaking publicly about the challenges they are facing, and noted that crisis talks held by the Government this weekend had failed to include smaller suppliers.

“Where once there were 70 suppliers, we could soon be down to 10 or 15. We’ve seen £60 million added to our bills because of the collapse of companies, and the figure could triple yet. The drive for more competition in the market left many consumers worse off. Cheap deals for savvy, tech-literate and time-rich consumers were effectively subsidised by higher prices for more vulnerable households…The lesson is that cheaper does not mean better.,”

– James Coney, Money Editor, The Times

Many of us have been saying this for years (Retail energy market: does size matter?). Competition in the market has not worked for a long time (if ever), and market rules have been based on the false premise that energy retail is highly profitable. It isn’t and hasn’t been at least in the past decade. Customers are encouraged to shop around for “the best deal” but “cheapest” and “best” are not synonymous – in order to achieve cheap prices, suppliers cut costs in back-office functions which leads to high levels of customer dis-satisfaction due to billing errors and long call-centre waiting times.

In these markets, scale is crucial, as is a degree of vertical integration. When we experience periods of low wind generation, the only real hedge is gas-fired generation (or the last remaining coal plant) but while EDF as the only true vertically integrated player should feel more comfortable, its assets are aging and lacking in reliability, particularly in the nuclear fleet.

So what next?

Suspending the price cap and notice periods for tariff increases might prevent some supplier failures, but it means consumers will see rapid increases in their bills. Unfortunately consumers need to accept this – energy is not, and should not be free, and it is not the job of suppliers to provide welfare to the public in the form of absorbing increases in wholesale energy prices.

Suspending the price cap and notice periods for tariff increases might prevent some supplier failures, but it means consumers will see rapid increases in their bills. Unfortunately consumers need to accept this – energy is not, and should not be free, and it is not the job of suppliers to provide welfare to the public in the form of absorbing increases in wholesale energy prices.

If the Government wants to soften the blow for customers it could consider reducing the rate of VAT – now the UK has left the EU it has discretion to set its own VAT rates and this would be a quick adjustment that could be made, for example for this winter.

Encouragingly, Alok Sharma implied this morning that a suspension of the price cap is under consideration, although it was apparently unclear as to whether he was referring to the price cap or subsidy costs (although their removal would also be very positive). Unfortunately a Government spokeman later denied the claim, telling The Independent:

“Our energy price cap will remain in place this winter and exists to protect millions of customers from sudden increases in global gas prices.”

This statement is, unfortunately, nonsense – consumers will not benefit if suppliers go bankrupt, and the logical conclusion of a price cap set below the level of cost recovery is a collapse of the entire industry, exactly as happened in California.

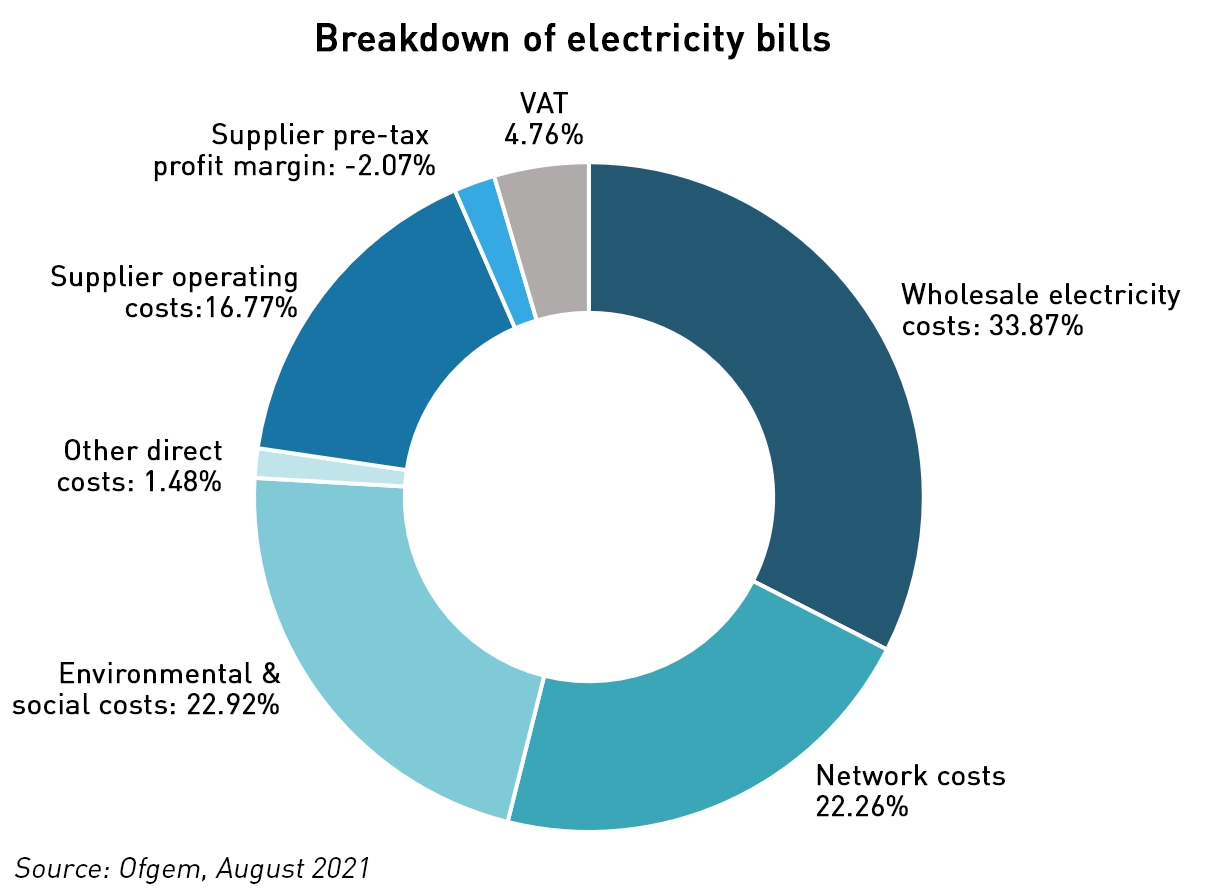

Emergency action is warranted, ideally to prevent the need for bailouts, but longer term the market must be reformed. Regular readers will know my views on this, and I have argued for retail reform for as long as I’ve been writing my blog, but recent events make this more pressing. Removal of non-supply activities from suppliers is essential – these make up 23% of electricity bills and hit the poorest consumers hardest.

If no action is taken, then by the end of the winter we may be left with fewer than a dozen suppliers in the market, and the Government’s experiment with competition will officially have failed.

The problem here is not which retailer sells the gas to the consumer and whether they may be nationalized or not. It seems of little consequence in the long run unless you are a stakeholder of one of the struggling retailers.

Surely the real problem here is understanding the real causes behind the spike in wholesale prices and whether we face serious blackouts this winter.

I’m not a stakeholder of any of them!

There are two coinciding things happening with prices. The first is a doubling of gas prices over the past year due to the global supply and demand balance which has left European storage levels at about two thirds of the levels they should be at this time of year. There are a few reasons behind this including higher demand this summer in south America due to reduced hydro capcity, lower Norwegian output due to maintenance, some of which was held over from last year, and reduced flows from Russia, possibly to force an early decision on Nord Stream 2.

This, together with higher carbon prices has pushed up electricity prices, which have also doubled in the past year across Europe.

On top of that we’re in a period of low wind generation which is exposing how vulnerable our power grid has become. Low utilisation rates for thermal generation have acted as a dis-incentive for new CCGTs, with next to none coming through the capacity market, and the age of the fleet is leading to reliability issues.

I don’t know that we’re facing blackouts – I believe there is enough capacity in the system to cover demand absent a serious disruption in gas supplies – but I do expect price volatility to continue, both in gas and electricity markets. Having said that, there could be supply interruptions for industrial consumers, which we’re seeing in gas at the moment. This is having a knock-on effect on other industries, but domestic consumers will always be super-senior to use credit terminology when it comes to supply preference.

Apologies, my poor English – I meant stakeholders generally – not you personally. Given your knowledge of the industry I find your answer reassuring. I believe that 20% of our gas comes from LNG imports and I was concerned these may face serious disruption in a global market shortage. Given the UK has woeful storage capabilities then I was fearing the worst, particularly if its a cold winter. I would be very interested in your view of UK energy security, with North Sea gas on a downward slope and with Russian piped gas unlikely to make it as far as the UK. Perhaps a subject for a future blog post if you had time.

No problem – I didn’t think you necesarily meant me, but I’m genuinely independent with no links to any of these companies.

I’m about to publish a post about gas market dynamics. LNG is definitely tight at the moment because Asian markets are higher priced. The challenge we have is around short-term disruptions…when Rough closed the view (held by me and others) was that without a large storage facility we would be at risk of shortages until LNG could be diverted to us, and we would have to potentially pay a lot to get it. That is still the case – eventually if we really neeed the gas spot LNG cargoes are available but we’d have to outbid an Asian market that is seeing record JKM prices.

In terms of where our gas comes from – 48% from domestic production, 30% from pipeline imports and 22% from LNG. 96% of the pipeline gas imports come from Norway, and about 4% from Belgium and the Netherlands which probably originates from Russia.

I like the Alok Sharma quote, and your response. We really are in the post-truth world.

I’m old CEGB and when privatisation happened a lot of us thought it could never work. Well, we seemed to be wrong for nearly 30 years and the “market” now is so complicated that few of us have the time or energy to try to understand it. So it is really nice to read your well informed analysis pointing out some of the deficiencies.

My late sister worked for the old CEGB! So many political imperatives constrain the supply of electricity that its hard to see the space for a market at all. Some form of nationalisation looms

Very informative article, as they all, but hard reality is that we are using too much energy/capita anyhow and are now paying the price literally for its provision. More should have been done to reduce demand especially from improving the insulation of domestic properties but we are now entering a perfect storm with constraints across many aspects of modern society inhibiting a response. Furthermore its all very well Sharma harking on about the need for reduced fossil fuels but when half the world has barely had access to what we in the West have enjoyed for over a century its not going to wash. A day of reckoning is coming and small energy suppliers failing are just the early indicators of deeper problems ahead whilst this govt pursues such reckless policies. As i see it the remaining coal stations should be instructed to run as baseload now to reduce gas consumption in the run up to winter and those assets need to be mothballed, not demolished, as strategic reserves until there is more certainty. We also need to get on with building out more nukes and rekindle the abilities we had 60 years ago in this sector.

Absolutley – in the short term we need to keep the coal open and available, and in the medium-long term we need new nuclear (that works ie not EPR) and better energy efficiency. To do that the EPC need to be reformed so that actual heat losses are measured and addressed, rather than notional ones which may not even be the issue.

Painful as it might be, the only way to properly have competition within this market is to remove artificial modifiers like the price cap.

Price and offers will react accordingly and we will have true competition again.

Krs

Mark