Last week I was invited to speak at the Westminster Energy, Environment & Transport Forum on the subject of smart energy markets. The transcript of my speech is below:

Developing smart energy markets for suppliers and consumers – modernising entry rules, delivering smart tariffs and increased competition, and enabling households to benefit from new preferences and energy management options

Good morning.

Since privatisation successive Governments have prioritised competition in the energy market, believing that the more suppliers there are, the better value there is for consumers.

Since privatisation successive Governments have prioritised competition in the energy market, believing that the more suppliers there are, the better value there is for consumers.

But despite there now being more than 40 electricity suppliers, bills continue to rise and customer satisfaction to fall. At the same time, increasing numbers of suppliers are exiting the market, due to financial difficulties.

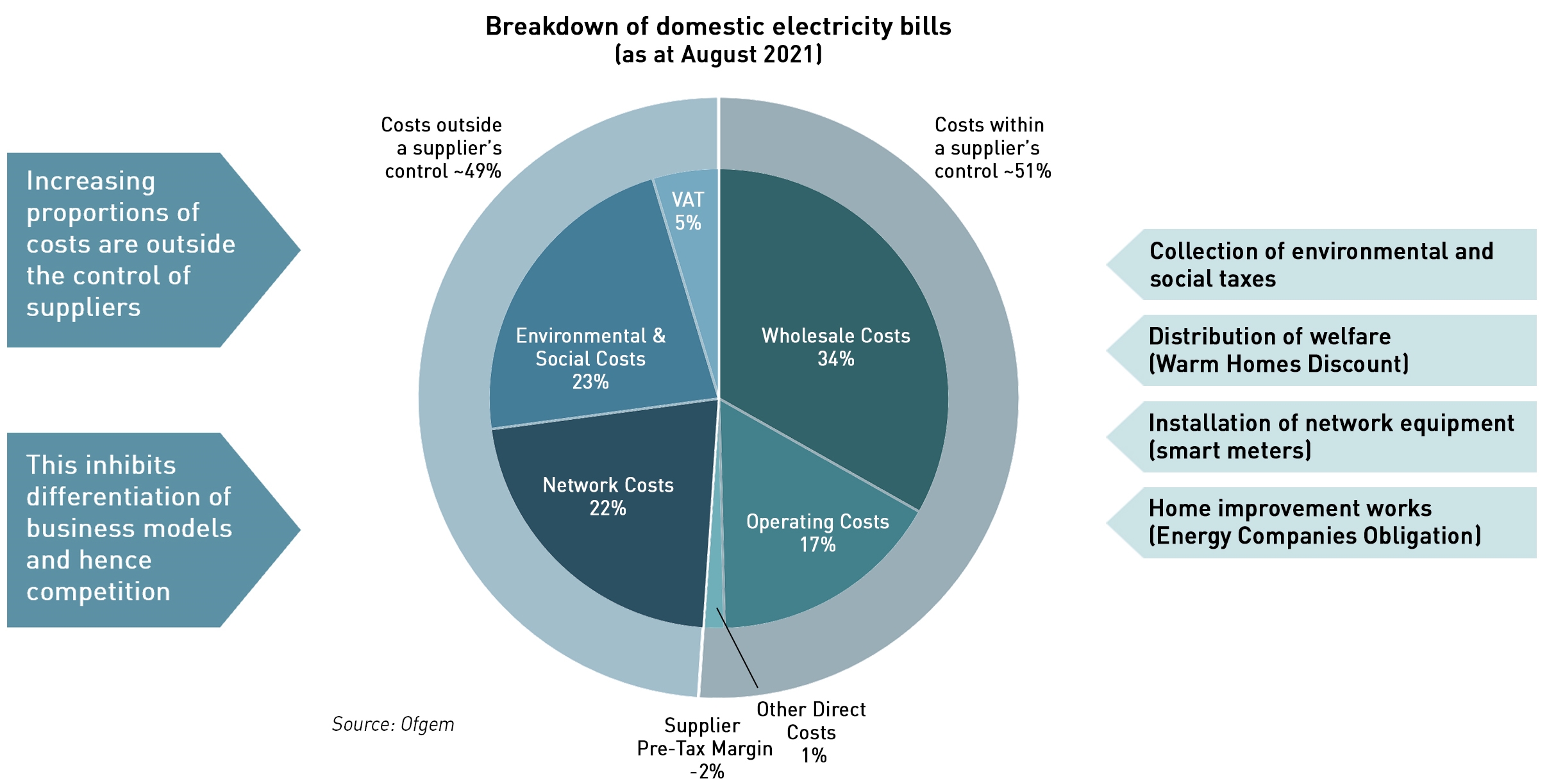

A big reason for the market failure is its high degree of complexity. In addition to supplying energy, suppliers are expected to collect taxes, distribute welfare, install network equipment and deliver home improvements.

According to Ofgem, large suppliers are now losing money on both the gas and electricity supplied to homes. While smaller suppliers can avoid some non-supply activities, they find it harder to hedge their wholesale price risk.

Indeed, Ofgem has been sufficiently concerned by supplier failures – and with good reason since some of the costs of failure are socialised – that it has raised the barriers to entry, which impedes competition

Since electricity supply attracts very low margins, suppliers struggle to manage the operational complexity of their business models, leading to poor customer satisfaction.

However, the Government is now re-considering its approach to the recovery of environmental and social policy costs through electricity bills since the resulting disparity in electricity and gas prices dis-incentivises the electrification of heating.

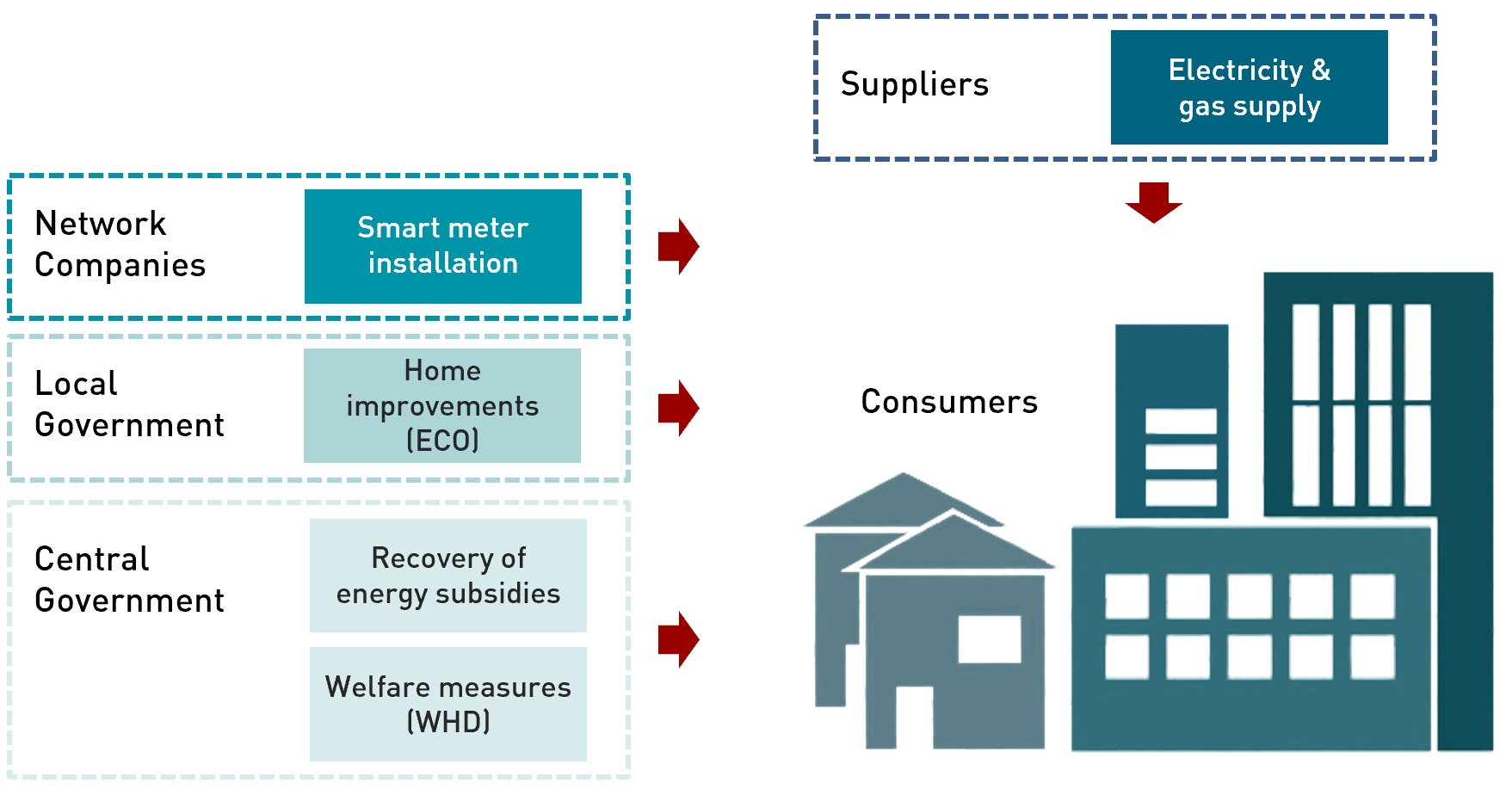

As a first step, supplier business models should be simplified, and non-supply activities re-assigned to more appropriate bodies:

- network companies for smart metering,

- local authorities for the Energy Company Obligation,

- and central government for recovery of subsidies and distribution of the Warm Homes Discount.

There is also a recognition that net zero ambitions will be difficult to achieve without changing the WAY that energy is used in homes.

Smart meters were supposed to help consumers to monitor and reduce consumption, although there is little evidence this has been achieved, yet policymakers remain confident that consumers will take up time-of-use tariffs and use them to optimise new flexible assets such as EVs, solar panels, batteries, and flexible heating technologies.

In reality, few will attempt to do this – they already find bills difficult to understand and have little interest in kWhs and standing charges and unit costs. They are unlikely to have the time or inclination to self-optimise.

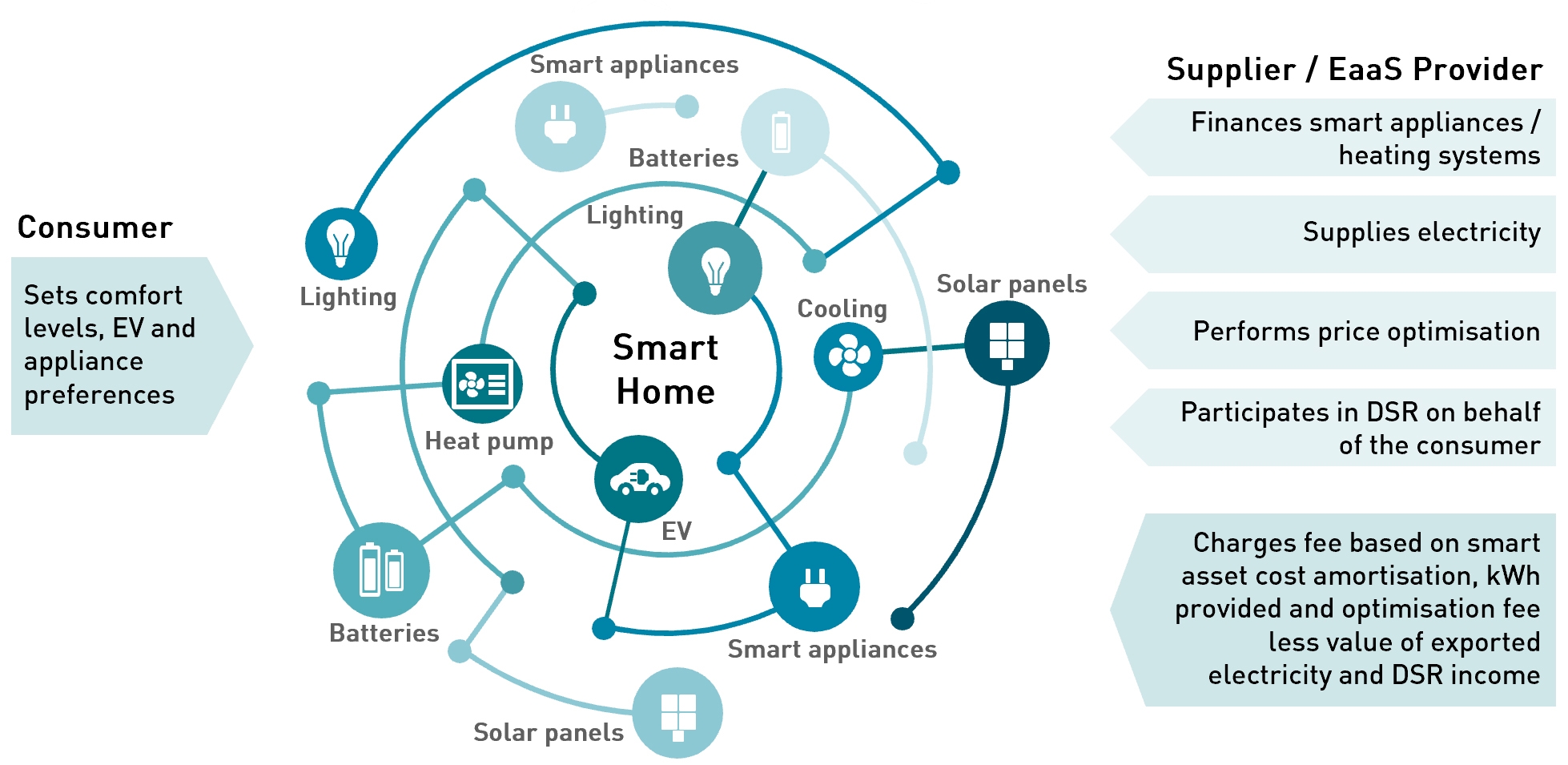

So as a second step, the Government should incentivise new supplier business models where electricity supply is bundled with optimisation.

Consumers could be offered flexible energy assets as part of the bundle, with the capital costs amortised over a pre-agreed period, possibly structured like mortgages which can be ported to other providers.

In these “energy-as-a-service” models, consumers would define comfort levels and other outcomes such as their EV charging preferences, and the provider would deliver based on market prices, and the needs of any demand-side response services it is providing to network operators.

Simplifying supplier business models by removing non-supply activities will provide a stronger basis for competition since suppliers will have greater control over their costs.

And making the offerings available to consumers easier to understand and more convenient, will increase consumer engagement and with it the likelihood of success in de-carbonising homes.

But any discussion of new business models in critical industries must include consideration of vulnerable consumers. As with water and finance, consumers have little choice other than to participate in energy markets.

Many consumers face real barriers to engagement that go beyond simple dis-interest:

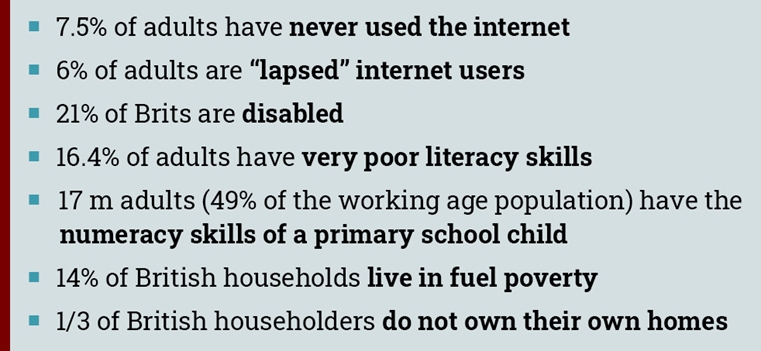

5% of adults have never used the internet and a further 6% are “lapsed” users meaning they have not been online in the past year

5% of adults have never used the internet and a further 6% are “lapsed” users meaning they have not been online in the past year- 21% of Brits live with a disability

- 16% of adults have very poor literacy skills

- 17 million adults – representing 49% of the working age population – have the numeracy skills expected of a primary school child

- 14% of British households live in fuel poverty and a third do not own their own homes

Households living in fuel poverty already face choices between heating and eating, and it’s important that in a world of time-of-use tariffs, they are not discouraged from cooking a hot dinner.

Similarly, fire services consistently advise against running appliances such as washing machines at night, yet there is an assumption with time-of-use tariffs that consumers will do exactly that.

Since low income households are overwhelmingly more likely to use older, cheaper and less safe appliances, care must be taken not to encourage them into harmful actions.

Smart energy markets offer a significant opportunity to both advance the de-carbonisation of homes and improve consumer outcomes, but there is a risk that if business models do not change, it will be impossible to fully capture these benefits.

Making supplier business models work for suppliers and consumers

The more I think about the retail market, the more I want to see radical reform. The large amount of non-supply activities suppliers are required to perform is ruining the market: business models are far too complex, but with low margins, suppliers struggle to deliver the systems and processes necessary to undertake all of these activities well, meaning mistakes are made and customer service is worse than it would otherwise be.

The Warm Homes Discount is particularly egregious, since suppliers require information on consumer eligibility from the Department for Work and Pensions (“DWP”) before applying the discount, when the DWP could itself provide this welfare payment to those who are eligible in the form of an additional pension credit. The payment would be funded by taxpayers rather than bill-payers, which means that low-income households would no longer have to subsidise slightly lower-income households.

These spurious supplier activities also make energy much more expensive than it would be otherwise, so a combination of high prices and poor customer service significantly reduces consumer confidence and therefore engagement in the market. The fact that most of these costs are applied to electricity bills rather than gas bills is now creating a dis-incentive to gas-to-electricity switching in the domestic heating segment, which is prompting a re-think by the Government. I urge policymakers to take this opportunity to radically reform the market.

A simplified model for suppliers would then form an excellent basis for the emergence of new energy-as-a-service business models. The removal of spurious activities may also attract new players into the market, such as technology companies, since they have expertise in the enabling technologies that under-pin smart homes. If done well, energy-as-a-service models could drive both the de-carbonisation of homes, and a material increase in the contribution the domestic sector makes to flexibility markets.

But I cannot see how these new models can emerge for as long as suppliers are burdened with the current range of non-supply activities. Bold thinking is needed if the market is to deliver the significant levels of change that are needed if net-zero ambitions are to be achieved.

You are so right to rail againt the present system, and your suggestions seem to me plainly correct. Especuially to remove from energy companies any obligation to mitigate the effects of climate policy on poorer people. That is a government responsibility. But, underneath everything, is the brutal supply side fact that renewables + gas is not an adequate basis for a net zero world. Some people will suffer a lot before this is understood.

I agree – the impact of net zero policies on vulnerable consumers is a major concern. I really believe the 80% target was much more reasonable when you measure GB emissions against the rest of the world. Pushing more people into fuel poverty will have a huge impact on the and a near zero impact on global emissions.

This is a nice post. I agree that the three responsibilities highlighted should be taken away from energy suppliers.

But I feel, the replacement responsibility of becoming a ‘energy-as-a-service’ supplier and optimising energy usage for the consumer is unlikely.

Firstly, energy suppliers are not technology companies, they don’t have the culture to suddenly become engineering-orientated rather than the admin and market traders they currently are (I assume here).

Secondly, I can’t see how a low-margin company could finance large upgrades to a consumer’s home. For instance if a house battery or solar PV was installed, there would be some savings generated, but the return is long and low compared to the high risk of default or lower-than-expected return. Because of this investors will stay away and I assume these companies just don’t have raw cash.

Thirdly, there is an inherent conflict of interest in a company that makes a profit per unit of energy used, offering energy reduction services (e.g., optimisation as from the consumers point of view). A third-party (tech?) company is much better placed to offer energy reduction services than an ‘energy supplier’ itself.

Going back to the top, I agree that energy companies are not the best suited for the non-core responsibilities. But I don’t think they will ever become ‘energy-as-a-service’ companies.

I’m not saying energy suppliers must become energy-as-a-service providers, I’m saying the Government should create the conditions where these providers can emerge, attracting technology companies into the market which may currently be deterred by all the non-supply activities they would have to engage with if they entered the market.

My hope would be that suppliers would partner with technology companies and finance providers to deliver these services. I also don’t see suppliers funding energy assets for their consumers themselves – this would be in partnership with finance providers…there are well established markets in asset finance that are analogous such as car financing. So today’s energy suppliers could move into energy-as-a-service directly, or they would provide the energy used by a tech company that delivers the service to the consumer, with finance partners providing any capital and financial engineering needed. (Alternatively, the Government could create incentives for energy assets such as heat pumps and solar pv to be finance as an add-on to mortages.)

The retail energy market is struggling, with over 40 suppliers yet rising bills and declining customer satisfaction. ⚡️ Simplifying business models by removing non-supply activities could enable suppliers to focus on providing better services. The concept of “energy-as-a-service” allows consumers to bundle flexible energy assets while defining their comfort levels, promoting a more personalized experience. However, it’s essential to address barriers faced by vulnerable communities, such as limited internet access and fuel poverty, to ensure they aren’t left behind. By fostering an inclusive energy market, we can advance decarbonization and improve outcomes for all consumers.