Over the last couple of years, Britain’s ongoing reliance on coal has been the subject of a few of my posts. Despite the “coal-free” days hype in the summer, the continued use of coal in winter goes unremarked. But the year-round economics for thermal generation are under-pressure, and, having failed to secure a contract in the T-1 capacity market auctions earlier this year, EDF has announced the early closure of its West Burton A coal power station. With the end of commercial coal generation at the remaining two coal units at Drax at the end of March, this leaves Uniper’s 2 GW Ratcliffe-on-Soar as the last remaining coal power station in the market.

EDF’s decision came after none of its four 500 MW coal units managed to win contracts in the T-1 Capacity Market auction for delivery in 2021/22, however EDF said two of the units will still be available over the next 18 months to fulfil Capacity Market commitments, suggesting they may have secured agreements for next winter through secondary trading. De-commissioning is expected to begin by 30 September 2022.

So what does this mean for the GB electricity market?

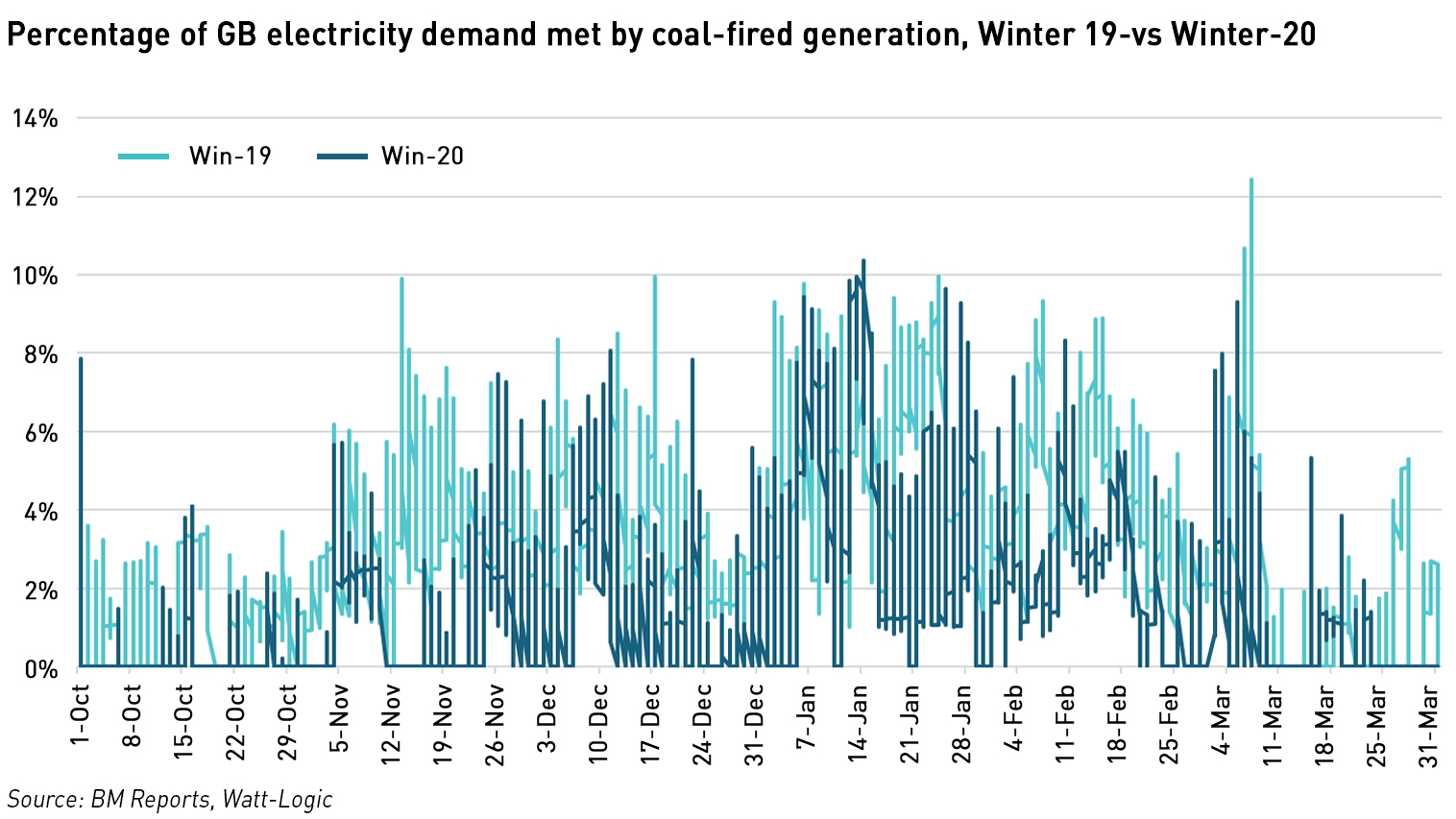

The use of coal has been gradually declining in recent years. Running hours were limited by environmental regulations, in particular the EU’s Large Combustion Plant Directive, and the UK Government has set a target date of October 2024 for the full exit of coal from the British generation mix. Despite this trend, coal still contributed as much as 10% of all generation last winter:

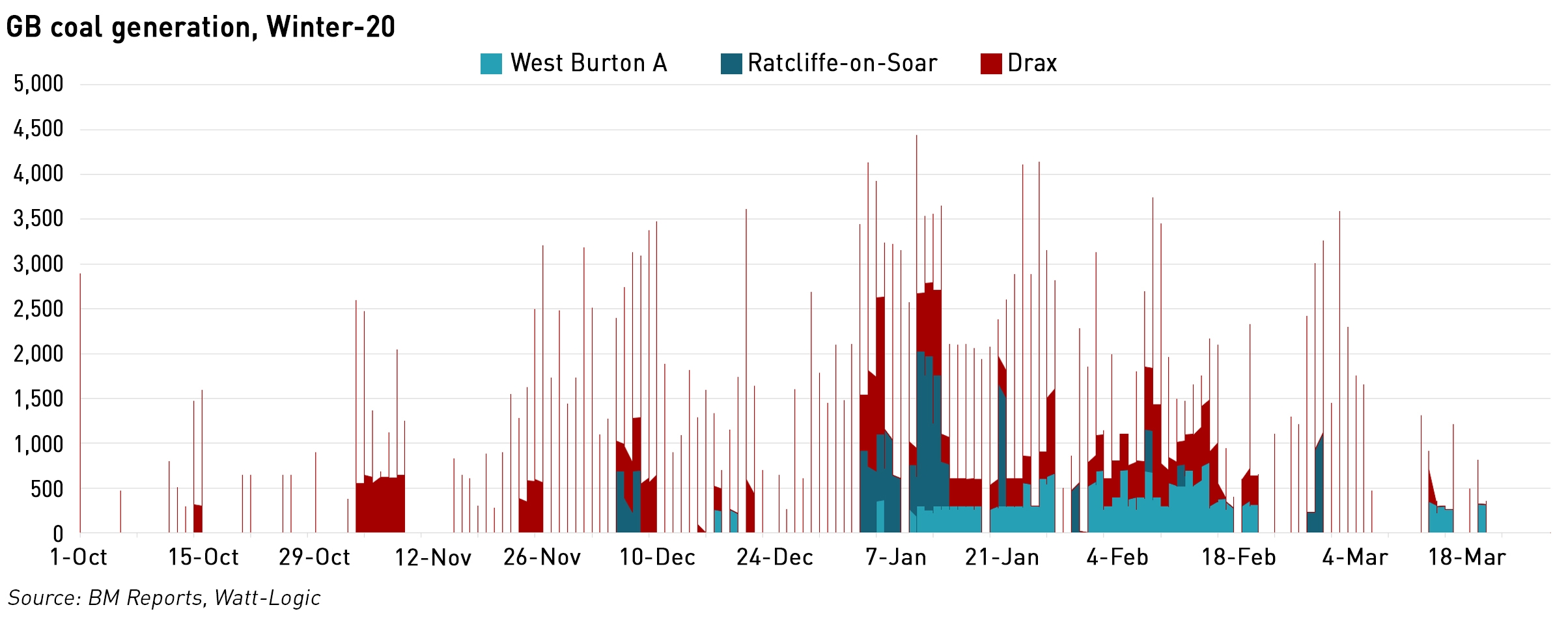

Coal was used most heavily during January and February when the weather turned cold and still, and wind generation was low. High demand was reflected in high prices. Drax in particular saw a lot of activity, as it ran down its coal stocks ahead of its closure at the end of the winter.

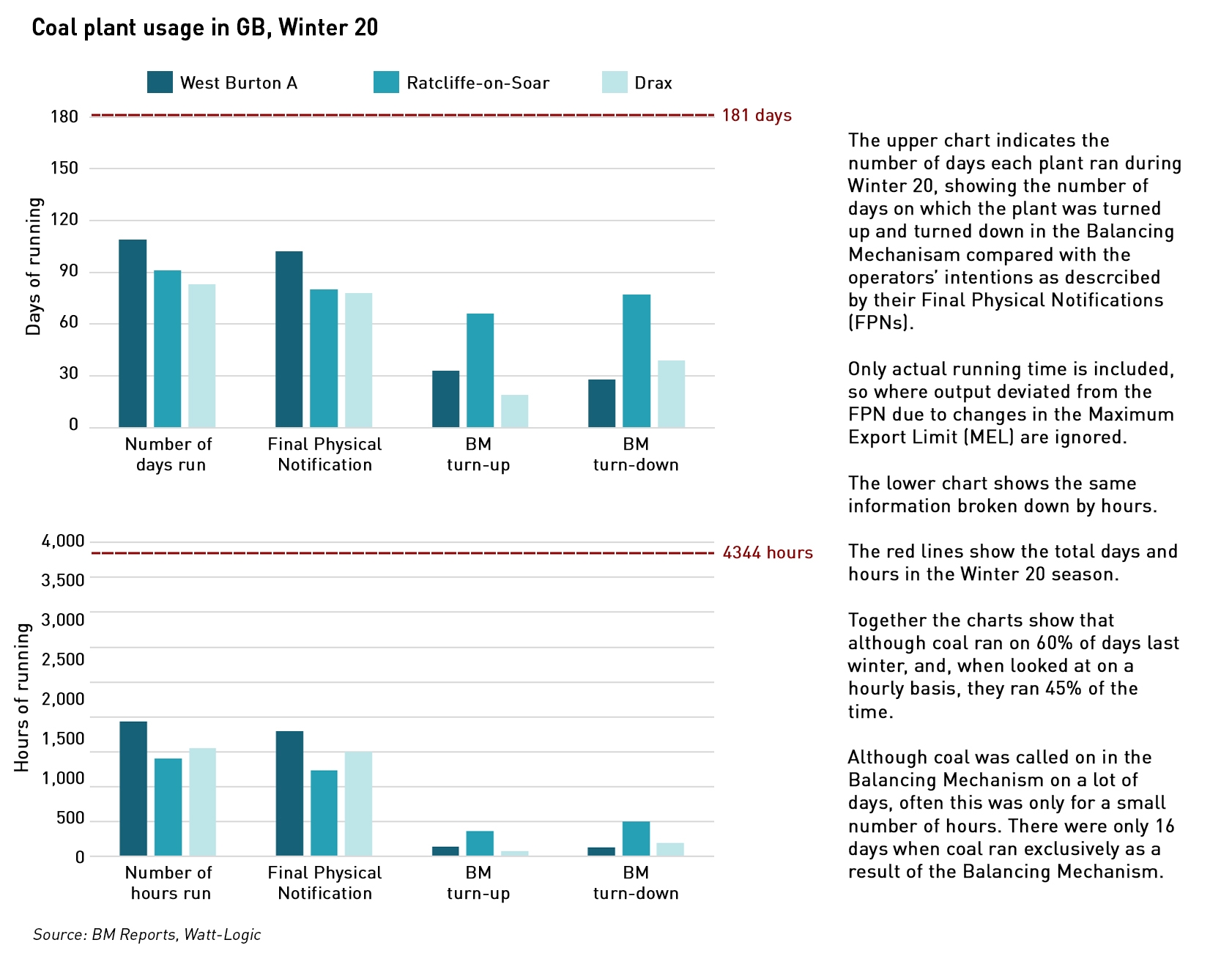

Most of the time, coal plant ran in line with the operator’s intentions, as reflected in the Final Physical Notifications (“FPNs”), and while there were a lot of small adjustments to the running profiles in the Balancing Mechanism (“BM”), there were only 16 days over the winter when coal ran solely as a result of being called in the BM, however, some of those were highly valuable to the operators:

Last winter saw high and spiky prices, with several Electricity Market Notices and Capacity Market Notices, a trend which is likely to continue in coming winters as capacity margins fall: as coal exits and older nuclear see declining reliability, there is a growing market tightness, particularly with yet more delays to the opening of Hinkley Point C and rising demand due to the electrification of transport and heating. Last winter saw higher balancing costs as CCGTs were called to fill the gaps, earning up to £4,000 /MWh in the BM. The market is likely to miss its coal once its gone.

Supply chain emissions threaten net-zero ambitions

One of the concerns raised in relation to net-zero ambitions is the issue of off-shoring of emissions, that is the manufacture of goods in countries with weaker environmental controls. The main country of concern is China, with its extensive and growing coal fleet. In 2019 the UK imported £49 billion (equivalent to 2.3% of GDP) of goods from China.

In 2020, China was the only G20 country to see a significant increase in coal production, generating more than 53% of the world’s total coal-fired power, despite adding record amounts of renewables with the country having 71.7 GW of wind capacity and 48.2 GW of solar. The country added 38.4 GW of new coal-fired capacity in 2020, more than three times the amount built elsewhere around the world, with another 36.9 GW of coal plant being approved last year. China now has 88.1 GW coal plant under construction and a total of 247 GW of coal power under development, enough to supply the whole of Germany. The current amount of coal capacity in operation is 1,050 GW, half of the global total.

Last year, China announced a plan to become carbon neutral by 2060, and earlier this year it promised to reduce its dependence on coal and bring emissions of greenhouse gases to a peak by 2030. However, despite a rapid growth in renewable energy, renewables met only half of China’s growth in electricity demand last year, and although coal’s share of consumption has fallen from around 70% a decade ago, it still amounted to 56.8% last year, with outright coal generation increasing by 19% between 2016 and 2020.

Research by the China Electricity Council shows China’s coal fleet has an average operating life to date of just 12 years and only 1.1% of its units have operated for more than three decades, the typical lifespan of a coal plant. This means that the Chinese coal fleet is much younger than those in Europe and the US, making closures more difficult to justify. Electricity demand is continuing to grow, so there are pressures to ensure security of supply during its energy transition.

The closure of coal-fired generation in Britain has wide-spread public support, and with only one plant left, it is essentially a done deal. But the dynamics elsewhere in Europe are very different, with lignite generation in Germany and Poland being an important part of the economic landscape. The appetite for closing local coal generation with the associated loss of jobs, while importing goods from China, manufactured using coal power is both politically challenging and environmentally unsound.

Leave A Comment