On 1 January 2021, the UK left the EU’s internal energy market (“IEM”), meaning that trading over the interconnectors between GB and the EU us no longer be managed through market coupling (except for Northern Ireland which remains part of the Single Electricity Market with the Republic of Ireland). The UK is also no longer be part of the EU’s joint action against climate change and has left the EU Emissions Trading Scheme (“EU ETS”), replacing it with a new UK version, and the UK has also left the European Atomic Energy Community (“Euratom”).

The agreement reached between the UK and the EU includes:

- provisions guaranteeing non-discriminatory access to energy transport infrastructure with predictable and efficient use of electricity and gas interconnectors;

- a new framework for co-operation between UK and EU Transmission System Operators (“TSOs”) and energy regulators;

- provisions regulating subsidies to the energy sector to ensure they will not be used to distort competition;

- provisions relating to security of supply, particularly relevant for Ireland, which will remain isolated from the EU internal energy market until new interconnections are established.

What is market coupling?

The European internal energy market was the result of extending the Single Market into energy, and involved the unbundling of networks from generation and supply with regulated rather than negotiated access to those networks. The ultimate goal is the creation of a single pan-European energy market, connected through the implicit allocation of capacity on interconnectors between the electricity grids of neighbouring countries.

Prior to the introduction of market coupling, transmission capacity on Europe’s interconnectors was allocated through explicit auctions. This was not always efficient, for example when electricity flowed from the higher-priced market to the lower-priced market, against the economic logic for interconnector use. Under market coupling, long-term interconnector capacity continues to be allocated through explicit auctions where market participants trade electricity and transmission capacity separately, however, at the day-ahead level, implicit auctions were introduced.

In implicit auctions, the relevant TSOs inform the power exchanges of the available capacity on their interconnectors (ie, the physical capability less capacity already nominated by long-term capacity holders). Market participants place orders in their local markets, with a pan-European algorithm called “Euphemia” determining the amount of electricity that will flow along each interconnector in every hour of the day ahead. The algorithm is designed to maximise social welfare, by matching surplus supply in one market with excess demand in another, and allowing customers to access the cheapest sources of energy, while pooling risk, exploiting geographic diversity, and reducing the need for new generation capacity.

What does the end of market coupling mean?

Since the beginning of the year, the UK’s day-ahead market has been de-coupled from the European market and is now outside the Euphemia interconnector determination. UK power will continue to be traded on the N2EX and EPEX exchanges, but these will now be separate auction processes with separate order books. Interconnector capacity for the interconnectors between the UK and the EU will also be traded in explicit day-ahead auctions. Nord Pool is staggering these auctions throughout the morning, with the BritNed auction first, followed by IFA 1 and 2, and then finally Nemo.

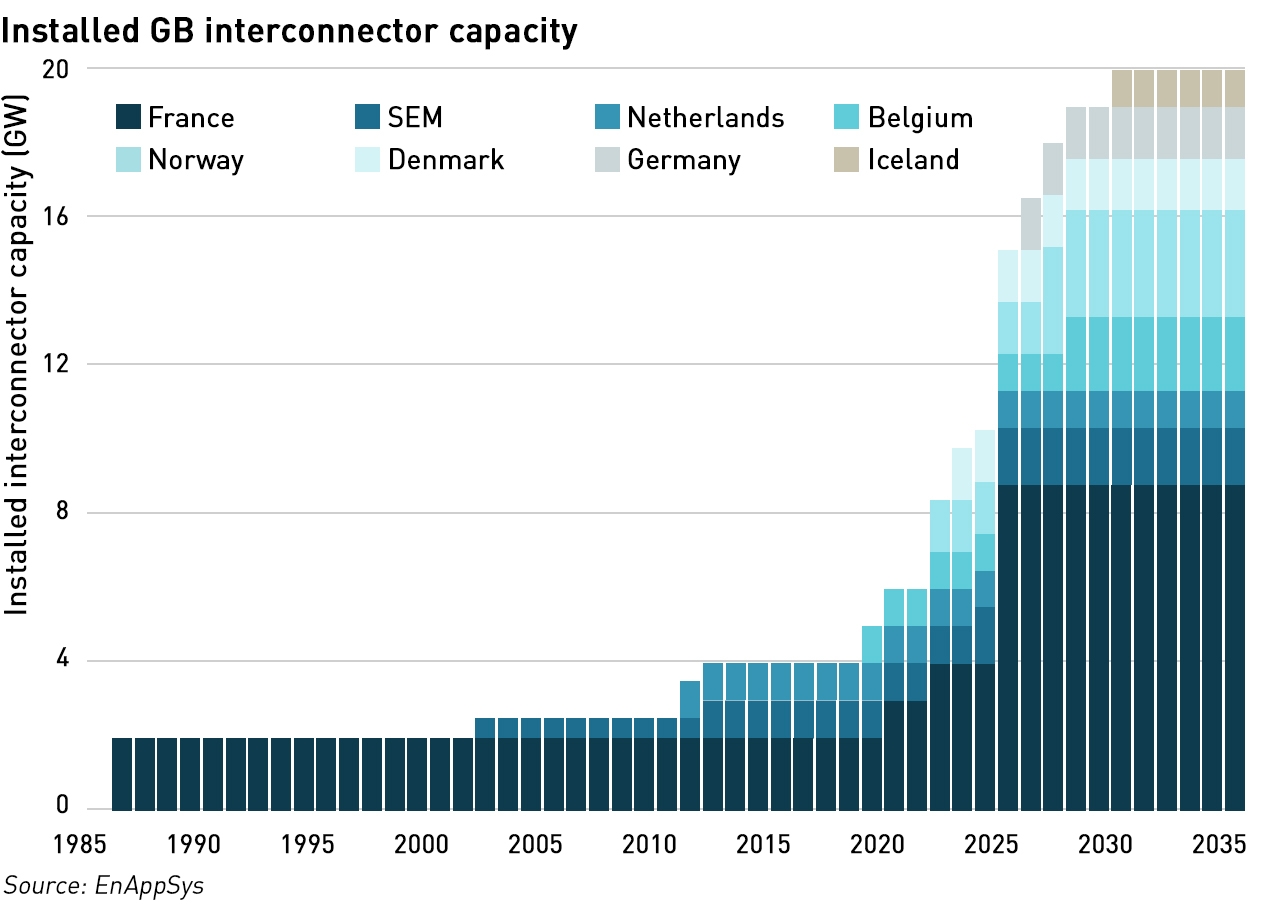

New day-ahead power market coupling rules are expected to be agreed between the UK and the EU, are should be in place by the end of March 2022. The plan is to introduce multi-region loose volume coupling to enable implicit capacity allocation on UK-EU interconnectors, based on day-ahead bids and offers in the UK and the EU bidding zones directly connected to the UK (currently Belgium, France, the Netherlands, and the Irish single electricity market). According to the Brexit agreement between the UK and the EU, the algorithm for the new coupling regime must be distinct from Euphemia.

The affected TSOs will develop a cost benefit analysis and proposal outline for the new procedures by the end of March, with full proposals due by the end of October.

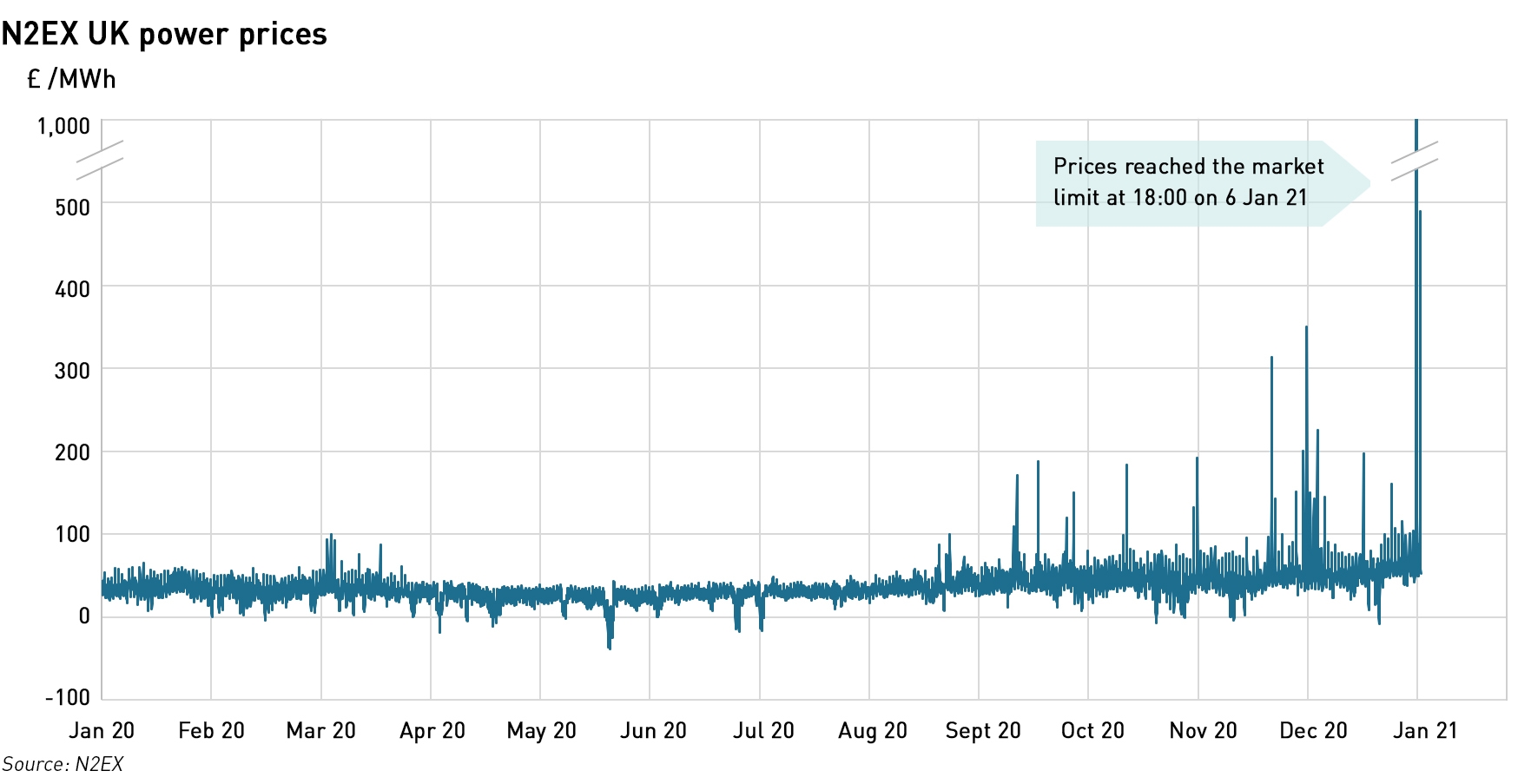

One aspect of the new trading arrangements is that since the electricity auctions on the two exchanges no longer have shared order books, and the auctions are blind, the two auctions can clear at different prices for the same delivery periods. There is a potential for the prices to diverge significantly meaning there is no unique day-ahead price of UK power.

Most of the time, any differences are likely to be small, but in times of system tightness, there is a greater potential for divergence. This has already happened – cold, still weather mid-week, combined with several nuclear plants being offline, meant National Grid ESO issued an Electricity Margin Notice (previously known as a Notice of Insufficient System Margin or “NISM”) for the fourth time this winter.

As with the previous notices, the issue resolved within hours when additional thermal plant ramped up to meet the gap, but not before market prices spiked, reaching exchange limits – auction prices reached a record £1,000 /MWh on N2EX for Wednesday evening, the same period for which a 584 MW capacity shortfall had been identified. Prices on EPEX reached £737.50 /MWh. The volume of power traded on N2EX was around 3 times that on EPEX – which has consistently seen lower volumes than that traded on Nord Pool.

In fact, the N2EX auction was run twice after the price in the initial auction exceeded the maximum threshold of £750 /MWh. When this happens, the order books are re-opened giving market members the opportunity to amend their bids and offers. The price threshold was reduced from £1,500 /MWh when the UK left the IEM to reduce the impact of potentially volatile prices during initial period post-Brexit.

Is leaving market coupling a bad thing?

Market coupling is not without its problems, primarily the ability of TSOs to limit the availability of cross-border capacity in order to protect their own markets. Some countries – such as Germany which is the EU’s largest power market – have made less than 20% of their potential transmission capacity available to neighbours in recent years.

“DA market coupling remains a crucial outstanding element in the integration of European electricity markets. The efficient use of interconnectors did not significantly increase in the last five years,”

– ACER Market Monitoring Report 2019

As a result, in 2019, the EU legislated to make it a requirement that from 1 January 2020, a minimum capacity margin of 70% must be made available for cross-zonal trade, the on all critical network elements. In its first report into compliance with this obligation, ACER found that while the target was largely being met on dc interconnectors, the position on ac lines is much more “diverse” with “significant room for improvement”.

More price volatility is expected this winter

Price volatility can be expected as the market settles into the new trading regimes, but even without this, the market has been prone to spikes due to lower-than-normal capacity margins this winter. Calon Energy’s administrator mothballed 2.3 GW of CCGT capacity when the company failed, while the Hinkley Point B (1 GW) and Dungeness B (1.1 GW) nuclear reactors are off-line on long-term shutdowns. The 1.2 GW Hesham 1 nuclear reactor has also been off-line since late September and will only begin its re-start later this week, returning to full capacity on 16 January.

At the same time, the 1 GW BritNed interconnector with the Netherlands tripped on 8 December and is not due to re-open until 1 February. Given tight system margins are also forecast in France and Belgium, there is no guarantee that Britain will be able to rely on its remaining interconnectors with the Continent to plug the gaps left by its missing domestic generation capacity.

With further cold weather expected over the coming days, more price volatility is likely. And of course, coal has had to fill the gap with coal-fired generation reaching 3.8 GW on 6 January.

The problem is that some countries – Germany being a notable example – have genuine internal transmission constraints which will make compliance with the 70% rule expensive. A potential solution is to split countries into separate bidding zones, with different prices – Germany could have a cheaper, wind-dominated northern zone and a more expensive, demand-dominated southern zone – but this is often politically difficult. Germany used to have a single pricing zone with Austria but was forced to separate in 2018 following complaints from neighbouring countries that their grids were being used as a substitute for internal transmission capacity in Germany, creating congestion to the detriment of local citizens. Instead, Germany intends to expand its internal electricity network.

While leaving the IEM may create some short-term market inefficiencies, market coupling is far from perfect, and so being outside the scheme for a year until an alternative method is agreed is unlikely to be a huge issue for most market participants. What will be interesting is how power trading evolves, and whether there is a migration of the existing, lower volumes on EPEX to the more liquid Nord Pool market, making the price divergence largely irrelevant.

Trips aside it seems that there is little change in the operation of the interconnectors in practice. Trips do seem to be rather more common than comfortable on these subsea cables. For example IFA suffered two trips in October, one to each bipole, losing 1GW on each occasion: the first produced a sharp RoCoF and a nadir at 49.59Hz, even if the second was more of an unscheduled ramp down. Followed by WesternLink HVDC on the 25th (I assume this is why constraint payments were so high in November and December – it is impossible to find out anything about the current status of WesternLink) – and finally our old trip friend Hornsea deloaded 1185MW on the 30th, causing a dip to 49.60Hz. IFA tripped again on 20th November – this time losing 1GW of exports and sending the frequency high to 50.40Hz. We await more recent news.

https://www.nationalgrideso.com/industry-information/industry-data-and-reports/system-incidents-report

Did you notice that National Grid had proposed setting a minimum inertia level of 140GVAs as a belated response to the inertia questions raised by the Aug 9th blackout?

Of course the big news on the Continent was the close shave with potentially quite a widespread blackout.

https://www.entsoe.eu/news/2021/01/15/system-separation-in-the-continental-europe-synchronous-area-on-8-january-2021-update/

Still, there was perhaps 500MW or more of involuntary blackout in Romania judging by the demand data on top of the 1.7GW of interrupted supply, and probably more that ENTSO-E aren’t owning up to.

Meanwhile AFAIK the UK seems very keen to go ahead with TERRE, (indeed it seems we participated in a small way by reducing imports during the Jan 8th incident)

https://www.entsoe.eu/news/2020/01/09/trans-european-replacement-reserves-exchange-terre-project-to-deliver-a-european-platform-for-the-exchange-of-balancing-energy-from-replacement-reserves-based-on-libra-solution-live-in-january-2020/

and ENTSO-E itself tacitly recognises that it will have to flange up with the UK in other ways:

https://www.entsoe.eu/news/2021/01/25/third-entso-e-position-paper-on-offshore-development-focuses-on-interoperability/