I recently wrote about the calls from the House of Lords for energy security to be prioritised over the other elements of the trilemma. With the end of Winter 16 almost upon us, and with it the end of the Supplementary Balancing Reserve (“SBR”), it’s reasonable to ask what is level of supply margin is required for the system to be considered “secure”.

The SBR was established in 2013 amid concerns of tight capacity margins and the prospect of blackouts as aging coal plants close. As it turns out, the £180 million scheme has never been used, which begs the question of whether it was needed in the first place, and whether its replacement by the Early Capacity Auction at three times the price is really value for money.

Year after year there are warnings, including on this blog, of the possibility of winter supply shortages or even blackouts, yet year after year the lights remain firmly on. So were the concerns overblown, or have we been enjoying an extra-ordinary lucky streak?

Winter 16 saw some tightness but in the end demand was comfortably met

On his Energy Matters blog, Euan Mearns describes how this winter unfolded, particularly in January, when a period of still weather led to thermal plants running flat out to meet demand. He concludes:

“Concern about the integrity of the UK grid is borne out of the closure of 17.7 GW of coal fired power between 2004 and 2016 and its replacement with 14.4 GW of wind and 10.7 GW of solar. But the UK still has about 49 GW of dispatchable capacity left – nuclear, ccgt, coal, biomass, and hydro – that was enough to see us comfortably through January 2017.

One lesson from this is that the UK carried very large surplus generating capacity before the closures began and there was no doubt a cost associated with that. Since the closures, spare capacity is now thin and we got through January with comfort only because all CCGT and coal stations were operational which is not always the case.”

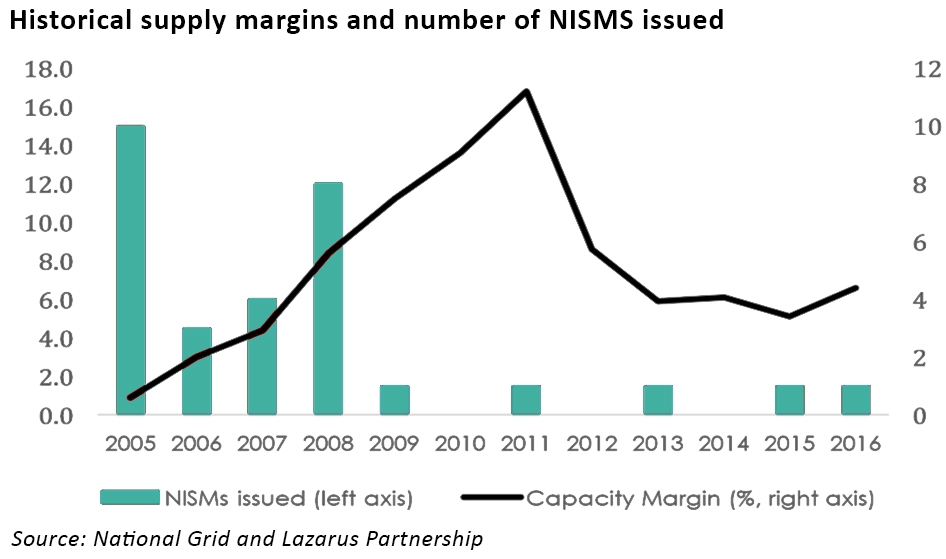

Was SBR an expensive and un-necessary insurance policy?

The Energy and Climate Intelligence Unit in its report Overpowered: has the UK paid over the odds for energy security? argues that although an insurance policy might seem prudent, it is not sensible if either it is not needed or is too expensive. The report highlights the high levels of grid reliability in the UK, and concludes:

“Looking ahead, we can also learn from the events of this winter, where the grid didn’t even blink during times of highest stress. Calls for an increased capacity margin have been shown, once again, to be unnecessary, with costs of boosting the margin to 10% calculated at anywhere from £800,000 to £12 billion – cash which could surely be spent better elsewhere.

In fact, as the system becomes more flexible, a greater margin will seem even less sensible. Building, operating and maintaining hugely expensive assets that will be used infrequently at best should be avoided, with any unneeded outlay likely to be recovered through higher bills.”

SBR is not the only source of back-up capacity

The SBR costs are only part of the overall cost of energy security – National Grid has made use of a number of other measures whose outcome has been to make capacity available which might otherwise not have been on the system. This report from the Institute for Energy Economics and Financial Analysis outlines the different measures available specifically aimed at security of supply, with Demand Side Balancing Reserve and the Short Term Operating Reserve providing additional capacity.

There are also in-direct sources of support, in particular the two Black Start contracts signed by National Grid last year, which avoided the mothballing of the plants in question at an additional cost of £113 million.

Interestingly this report has a somewhat different conclusion on overall security of supply, saying:

“Tight margins in supply and demand show that new reliable peaking generation is also needed, and it is far from certain that current capacity markets will provide it. While the goal of the capacity market was to drive investment in reliable new generation, the scheme—with £3.4 billion in awarded contracts to date—has yet to incentivise a single large new power plant.

This support for existing generation is distorting energy markets and has subsidised outdated investment, including more than £450 million for existing coal-fired power plants. Smaller, targeted capacity auctions solely for flexible, new-build generation, including gas peakers, demand-side response (DSR) and storage, should reduce this distortion. It should also reduce energy consumer bills.”

In other words, there is a need to incentivise some new capacity, but it is important that this capacity is flexible.

As SBR is replaced by the capacity market, what next?

It’s interesting to see arguments that SBR was un-necessary and expensive, when it is being replaced by an even more expensive scheme. The Early Capacity Auction for next Winter is set to cost three times as much as SBR as it rewards all available qualifying capacity and not just capacity which would otherwise have closed.

But there are increasing calls for energy policy to recognise that capacity alone is not sufficient to ensure security of supply, and the traditional view of supply margins may not be appropriate as the system transitions to a lower carbon, more decentralised model.

This article on the Clean Energy News blog suggests that the focus on capacity risks ignoring greater threats to security of supply, since blackouts can occur if the gird becomes unstable due to frequency deviations. As more renewables are added to the grid, so challenges of maintaining stability are increasing, and traditional solutions based on thermal generation may lack the response times needed.

As long as capacity is prioritised over flexibility, these problems will persist. An efficient energy system will place flexibility alongside capacity at its centre, taking full advantage of turndown DSR, storage and other measures to deliver security at the lowest reasonable cost and avoid either over-building new capacity or over-paying for old plant to stay online. Debating whether the supply margin should be 6%, 10% or some other amount, is rather missing the point.

Leave A Comment