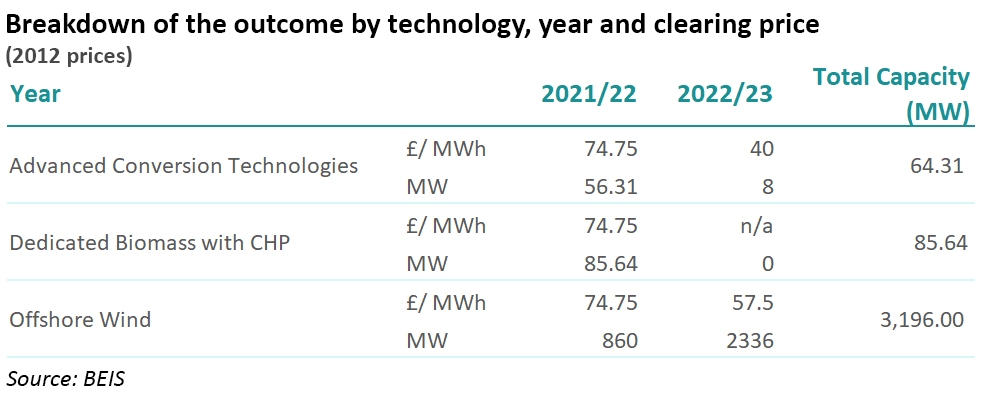

Earlier this week, the Government published the results of the second round of CfD auctions, which saw offshore wind secure contracts at lower than expected levels.

CfDs were introduced as part of the Energy Market Reform, largely to replace the Renewables Obligation regime which closed this year. The strike price represents a guaranteed return the generator will receive: if the wholesale power price is lower than the strike price the difference is made up by the Government; of the wholesale price is higher the generator pays the difference back. The net cost to the Government is passed on to consumers in their bills.

In the first round, in 2014, 15-year CfDs were awarded to five offshore windfarms with a strike price of £140-150 /MWh, a process which was criticised by the National Audit Office, which found that competitive auctions could have achieved lower costs. In 2015, the first CfD auction saw offshore wind secure strike prices of £120 /MWh. This time, 3.2 GW of offshore wind secured contracts at £57.50 /MWh, significantly below even the most aggressive pre-auction forecasts.

The prices for offshore wind are now lower than both the levelised cost of nuclear, and the estimated cost of CCGTs, which according to a November 2016 estimate by BEIS would need £66 /MWh to be economic. In its analysis, Cornwall Insight asserted that the results hailed a new epoch of renewable power:

“The conclusion from today is this: the epoch of renewables as the most cost competitive technology has arrived. Even without the added and essential benefit of its zero-carbon footprint, policymakers would – at these prices – be hard pushed not to press ahead with bigger growth in renewables on cost grounds alone, even if there was not a legally binding carbon budget to achieve. There could be no greater accolade than that. A new paradigm has arrived.”

Not everyone agrees. In June, the International Renewable Energy Agency published a report into global renewable auctions over 2016, and sounded a note of caution:

“There is, however, a risk associated with the fierce competition in the market and it is important to consider whether the drop in prices is sustainable from an industry point of view. A sustainable price decrease indicates that prices are falling owing to increasing market maturity while businesses remain profitable, whereas an unsustainable price decrease could lead to bankruptcies. This is due to the pressure that can be exerted on developers to stretch their input assumptions too far. Therefore, auctions can be associated with weaknesses that pertain to the “winner’s curse” and to underbidding that can result in projects coming online late or not at all.”

Offshore wind auctions in Denmark and Germany clearing with zero subsidy

Offshore wind auctions and tenders elsewhere in Europe have been clearing lower than estimated levelised costs for some time, with some German auctions clearing close to the expected wholesale power price, without subsidy.

According to Danish wind energy developer, Dong Energy, five cost drivers enabled their zero-subsidy bid in the German auctions:

- Platform change: significantly larger turbines will be on the market by 2024, which means fewer turbines will have to be installed and maintained;

- Scale: two “zero bid” parks will be combined into one large-scale project;

- Location: wind speeds at the locations are particularly high;

- Extended lifetime: the lifetime can be extended from 25 to 30 years;

- Scope: the auction did not cover grid connections, which will be provided by the grid operator.

It may seem surprising to see wind projects relying solely on wholesale market prices, since they will need to be confident both in the price level achievable and that they will run for sufficient hours to cover their costs.

“Our plans [for the German auction] were based on comprehensive market analyses and intensive discussions with the supplier industry, which is working on numerous new technological developments and is fully focussed on achieving cost efficient solutions. The assumptions regarding electricity prices that were used as the basis for our bid were thus set at a moderate level. The anticipated returns are considerably above our capital costs and thus remain attractive,”

– according to Dirk Güsewell, the manager responsible for the expansion of renewable energies at EnBW.

However, there are some features of the auction design in Germany that may tempt developers to treat bids as cheap options that will allow them to wait to see how both technology and the markets develop before making a final investment decision.

The German Offshore Wind Energy Act requires bidders to post a bid bond equivalent to €100/kW prior to auction. After that, the planning approval – a relatively inexpensive step – must be started within 12 months, and then the next milestone is not until 24 months before the expected completion of the project, which in some cases may be as late as the end of 2023. If this milestone is not met, the contract award is cancelled and a financial penalty in imposed which may be as little as 30% of the initial bond.

This article from the Offshore Wind Journal explains that developers on the Continent take less risk than those in the UK, with governments bearing some of the costs of site scoping and design, as well as taking responsibility for grid connection costs, which must be covered by developers in the UK.

Other differences between the UK and German systems include earlier delivery dates for UK projects meaning there is less time for cost reductions to materialise, and the fact that in the UK the CfD has a two-way payout: developers do not keep returns above the strike price. For these reasons, UK bids could not be expected to be as low as those on the Continent, and in particular the zero-subsidy bids in Germany should be viewed with caution.

The impact on system costs should not be ignored

While the reduction in the cost of renewables is positive, this should not be taken in isolation as a signal to build ever increasing amounts of intermittent generation. The non-energy component of bills is rising, with network costs being a major component of cost inflation, as National Grid spends increasing amounts on balancing an electricity with higher amount of intermittency and lower inertia.

A report by UKERC forecasts that the system costs associated with renewable generation are very sensitive to the flexibility of the system as a whole, but can generally be categorised as “modest” (although the data for high levels of penetration seem to be lacking).

A report by UKERC forecasts that the system costs associated with renewable generation are very sensitive to the flexibility of the system as a whole, but can generally be categorised as “modest” (although the data for high levels of penetration seem to be lacking).

The report analysed the different cost impacts of renewable generation from a number of studies:

- Reserve requirements and costs for high levels of intermittent generation, such as 50% penetration, could be between £15 and £45 /MW;

- Capacity credit (a measure of how much conventional plant can be replaced by variable renewable generation whilst maintaining overall reliability at peak demand), and capacity costs could be between £4 and £8/MWh at an assumed 20% capacity credit, between £9 and £11/MWh at 10%, and reaching a peak of less than £15/MWh even if the capacity credit is zero;

- Curtailment of renewable generation could also start to become significant at 50% penetration levels, meaning that generators would be paid for not producing electricity;

- Transmission and network costs could lie between £5-£20/ MWh at 30% penetration levels. Very few data were available for higher penetrations;

- Thermal plant efficiency and emissions are expected to be modest regardless of the level of renewable penetration, but could be quite sensitive to system flexibility;

- System inertia is likely to only become significant at high (>50%) penetrations of variable renewables.

Taken together, these costs seem to be more than “modest” and illustrate the wider consequences of high levels of renewable penetration.

The falling cost of renewable technologies evidenced by the CfD auction will help to mitigate the impact of de-carbonisation on consumer bills, however this should not be taken as a signal to accelerate their deployment. System costs are still rising, and National Grid’s consultation on balancing services illustrates the growing challenges it faces as system inertia falls.

The danger is that policymakers will be seduced by the prospect of lower subsidies, and in particular prices that are comparable with thermal and nuclear technologies, to implement “technology neutral” auctions. As long as developers are isolated from the system costs of their projects, such an auction would further distort already highly distorted markets.

Leave A Comment