National Grid has published its latest future energy scenarios going out to 2050. The scenarios are based on the (in)famous energy trilemma: security of supply, de-carbonisation and affordability, and provide what National Grid says are “credible pathways for the future of energy for Great Britain”. In this post I will explore what these scenarios mean for the GB electricity system.

Scenarios describe various levels of economic prosperity and de-carbonisation

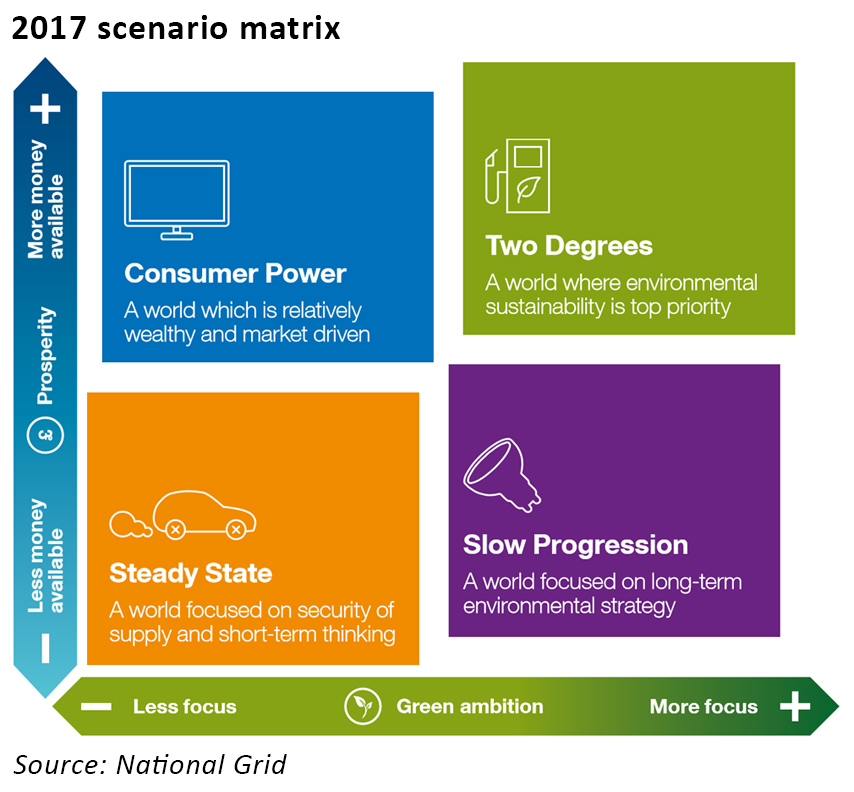

National Grid is presenting four scenarios: Two Degrees, Slow Progression, Steady State and Consumer Power, based on a 2×2 matrix with the axes “Prosperity” and “Green Ambition”.

Prosperity refers to the amount of money available in the economy for government expenditure, businesses investment and consumer spending, while Green Ambition reflects the level at which society as a whole and government policies engage reducing carbon emissions and increasing sustainability (my reading is that National Grid assumes equivalence between “sustainability” and de-carbonisation – the term “sustainability” only appears three times in the whole document, and “sustainable” twice).

Two Degrees has the highest level of economic prosperity combined with the strongest green ambition, with increased investment ensuring delivery of high levels of low carbon energy. Consumers choose to be greener and can afford technology to support it, while effective policy interventions make this is the only scenario where all UK carbon reduction targets are achieved. High taxes are levied on continued use of carbon intensive options, such as conventional gas for heating.

Slow Progression has the second highest level of green ambition but far lower prosperity. Conditions for growth are slow and gas prices rise significantly as a result of additional taxes. Incentives are in place to grow renewable and low carbon technologies, however a lack of money reduces the pace of their adoption. Consumers are environmentally conscious, but are limited by having less disposable income.

Steady State is the business as usual scenario, where the focus is on affordable security of supply. This is the least affluent of the scenarios and the least green. There is little ambition to de-carbonise, with policies focusing on energy affordability and there are no taxes on the use of gas. Electricity prices are relatively low as subsidies for alternate low carbon sources are limited. Businesses and consumers take a low risk, short-term value approach.

Consumer Power describes a world with high economic growth but low interest in de-carbonisation. Consumer appetite for the latest drives innovation and spending is focused on sources of smaller generation that produce short- to medium-term financial returns. Government policies focus on indigenous energy supplies with support for North Sea gas and the development of shale gas, leading to low gas prices and no dis-incentives to use for heating. There is high uptake of electric and hybrid vehicles as desire increases for new and prestigious products, and a higher degree of interest in local energy solutions.

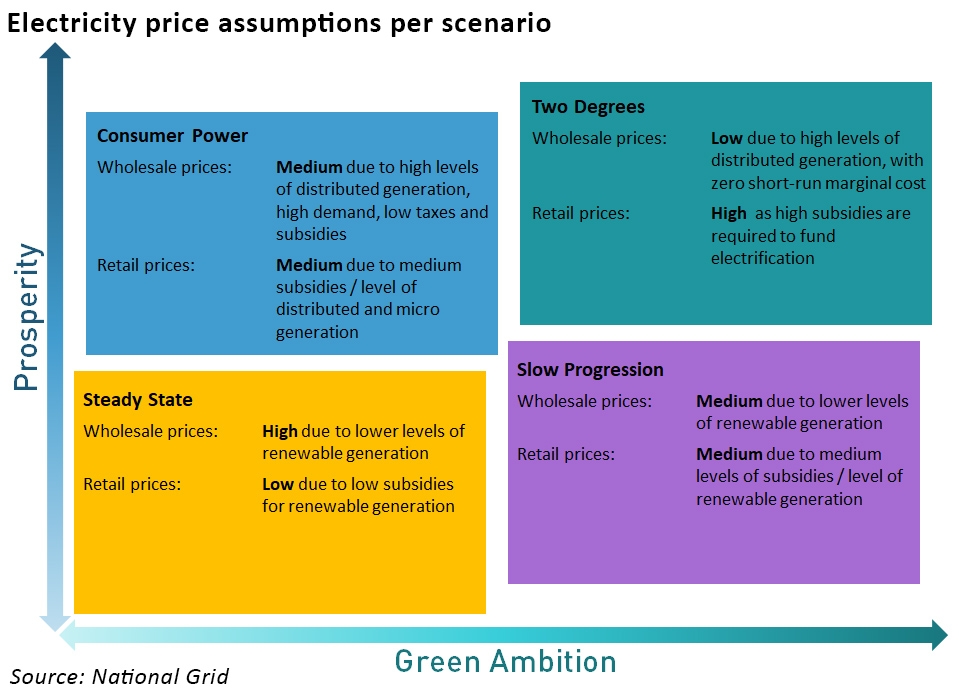

National Grid has not provided price projections by scenario, other than to say whether they are “high, medium or low”, so it may be inferred that Steady State follows the high path in this chart of projected wholesale prices, Two Degrees follows the low path and the remaining scenarios follow the base path.

Key messages

“An energy system with high levels of distributed and renewable generation has become a reality. This growth is set to continue, increasing the complexity of operating a secure and cost-effective energy system.”

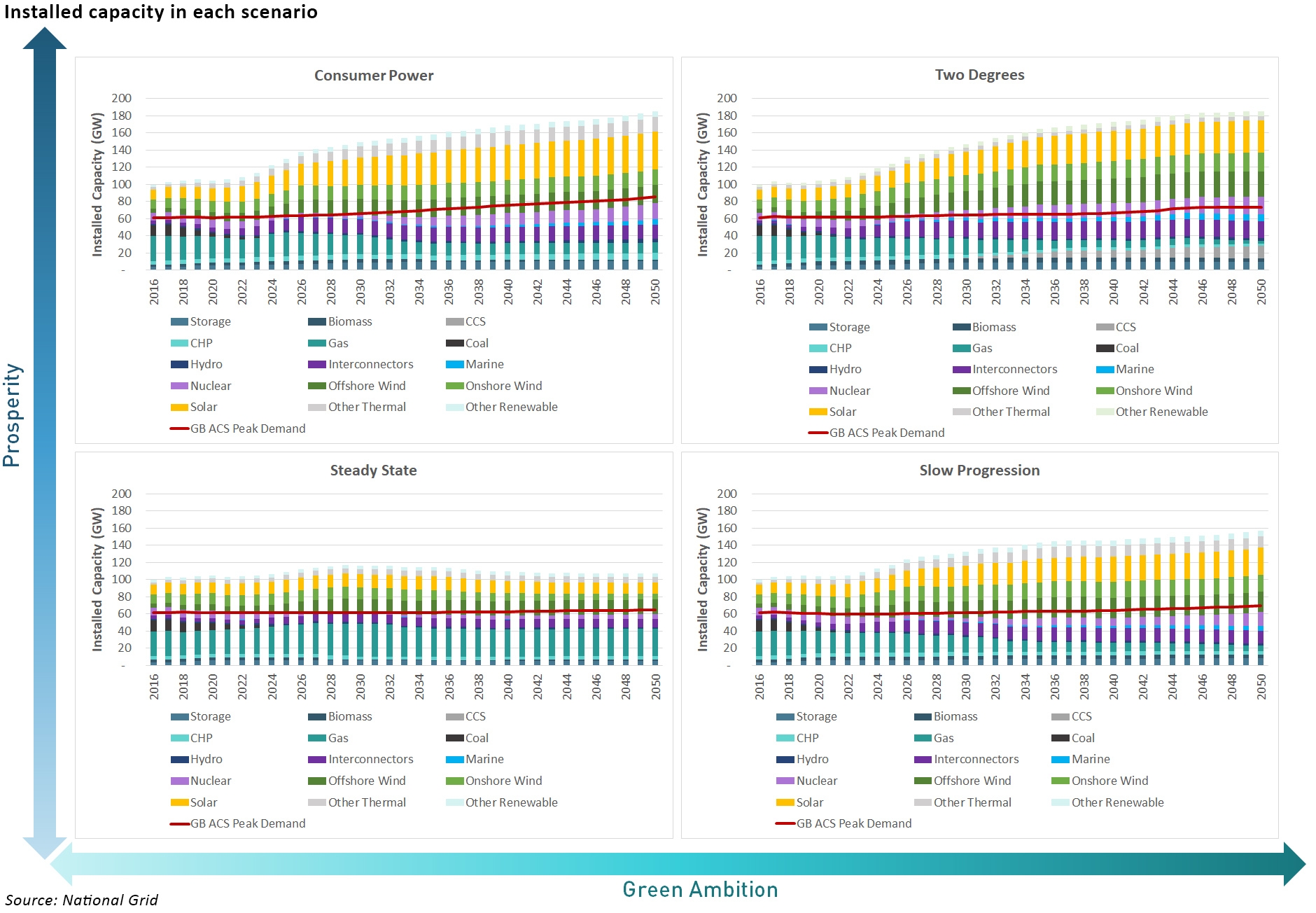

- The total amount of renewable generating capacity was 34 GW in 2016, or 34% of total installed capacity. In Two Degrees this could increase to as much as 110 GW / 60% 2050.

- In 2016, installed capacity from distributed generation reached 26 GW / 27% of total installed capacity. Looking forward to 2050, this could increase to a total of 93 GW or 50% in Consumer Power.

- As traditional sources of energy supply are replaced by new ones, and demand becomes more dynamic, the energy system will be more complex to manage. Responsive balancing products and services will be needed to deliver flexibility across both the electricity and gas systems.

“New technologies and evolving business models are rapidly transforming the energy sector. Market and regulatory arrangements need to adapt swiftly to support a flexible energy system with an increasing number of participants.”

- Electricity storage capacity totalled 4 GW in 2016 which could grow to almost 6 GW by 2020.

- Electricity demand has the potential to increase significantly and the shape of demand will also change. This is driven initially by electric vehicles and later on by heat demand.

- Electricity peak demand could be as high as 85 GW in 2050, compared to around 60 GW today.

- Electric vehicles are projected to reach around one million by the early 2020s, and there could be as many as nine million by 2030 – without smart charging, this could add 8 GW to peak demand. Heat pump demand may also add to this, and air conditioning could see peak summer demand matching peak winter demand if weather patterns continue to change.

- Outside peak periods, the increase in distributed generation could lead to periods of very low demand on the transmission system.

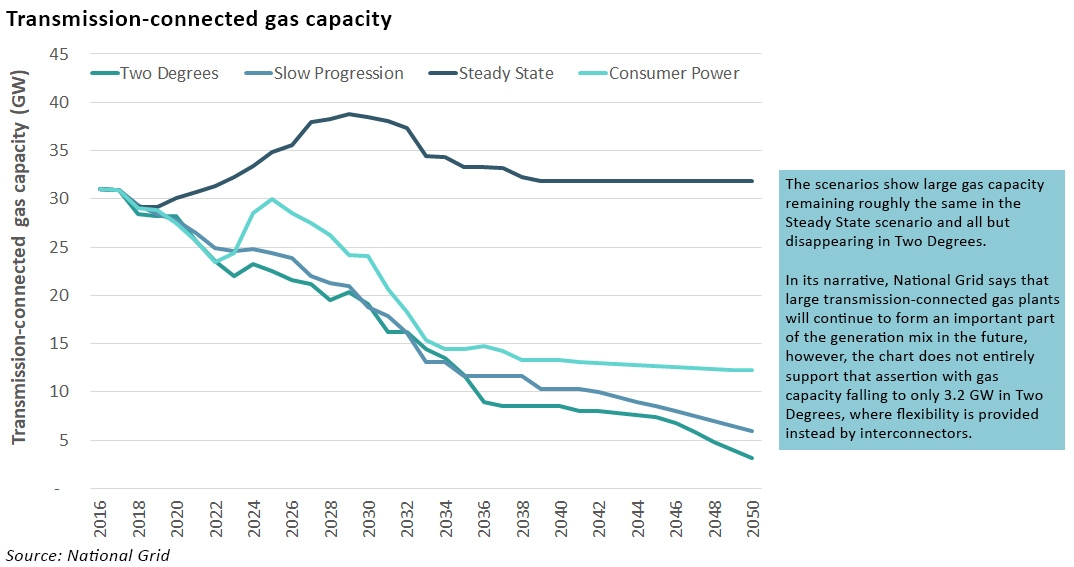

“Gas is critical to security of supply now and as Britain continues the transition to a low carbon future. It will have a long-term role as a flexible, reliable and cost-effective energy source favoured by many consumers.”

- Gas supplies more than twice as much energy as electricity today and could still provide more energy than electricity in 2050.

- Gas infrastructure is ageing and the demands on it are also changing, requiring a more flexible system.

- Gas will continue to play an important role in this transition and beyond with new technologies and the potential use of hydrogen.

About flexibility

Thermal generation

Large thermal plants are the traditional sources of flexibility in the electricity system, however they continue to face challenging economic conditions, due to a combination of energy and environmental policy, and increasing competition from zero marginal-cost generation.

Despite the first coal-free day in April, slightly fewer large coal plants have closed this year than predicted in the FES 2016 scenarios, as some plants have received Capacity Market or ancillary services contracts (the latter awarded by National Grid itself!). However in all scenarios, unabated coal plants all close by 2025 with the timing of closures differing according to scenario due to variations in the relative profitability of coal and gas generation.

National Grid believes that small-scale thermal generation, whether distribution-connected or behind the meter, can make an important contribution to system flexibility as intermittency grows. Consumer Power sees the highest penetration of small thermal plant, driven by local energy initiatives and innovation. Slow Progression also has high level of installed small thermal plant, primarily peaking plants that run infrequently. Two Degrees has the lowest growth of smaller thermal plants and the least small-scale generation overall.

Interconnectors

Interconnection capacity increases in all scenarios, although the modelled outcomes are lower than last year.

All scenarios show net imports at daily peak times (defined as 5-8pm on weekday evenings, November to February) until 2050, with large increases in peak imports to the early 2020s for all scenarios except Steady State. In these scenarios, interconnectors can provide a lower cost source of flexibility while old thermal plants are replaced with new intermittent and nuclear generation. The is particularly pronounced in Two Degrees as coal closes earlier than other scenarios, and a number of new interconnector projects are built.

The other wholesale scenarios show interconnectors flexing in response to changes in demand and supply over the period. For example in Consumer Power there is a dip in peak imports in the 2020s as more generation is built in GB. Later, imports increase again as GB demand increases.

Storage

National Grid expects storage growth to continue at a high rate to the early 2020s in all scenarios, driven by a fall in the cost of relevant technologies, ICT advances allowing better communication and control of assets, the growth in EVs, and the emergence of commercial opportunities.

National Grid assumes that storage needs multiple sources of revenue to be viable, including balancing and ancillary services revenues, asset services for Distribution Network Operators and Transmission Owners, and wholesale arbitrage opportunities. Storage is expected to often be co-located with renewable generation, to minimise capital and network costs and reduce the need for buying from the grid for charging.

Market saturation is reached at different times in each scenario, beyond which cannibalisation occurs, meaning that projects are less likely to be economically viable.

Last year, National Grid was predicting storage levels of 18.3GW of storage by 2040 in its highest-storage scenario. Marcus Stewart, National Grid’s head of energy insights explained the reduction is down to improved modelling in this year’s analysis:

“Last year was the first year we included battery storage in the scenario modelling and we had a reasonably simplistic approach. This year we’ve built on that and improved the modelling in that area, so the values we’ve calculated this year are lower because we’ve looked at the arbitrage value and if you go to a theoretical maximum, you start to see the cannibalisation of revenues.”

Trying to make sense of the detail

National Grid assumes that installed capacity remains fairly flat in all scenarios until the early 2020s after which the scenarios diverge. A similar story can be seen with demand, although the divergence is smaller. What is very clear is the very large difference that emerges in all but the Steady State scenario between demand and installed capacity, indicating that in a high-renewables world, large amounts of capacity will see very low utilisation rates.

Interestingly, the Consumer Power scenario where de-carbonisation is not a priory still shows extremely high levels of renewable penetration – more than in the Slow Progression scenario – it would be interesting to understand why this is the case. Inspection of National Grid’s price assumptions (shown below) is not entirely what could be expected from the description of the scenarios.

In particular, the Consumer Power scenario which is described as a world where neither consumers nor policymakers wish to support de-carbonisation, shows both medium levels of subsidies supporting a high level of distributed renewable generation, and low levels of renewable subsidies overall.

It should be assumed as well that the price assumptions themselves are relative, since it is difficult to reconcile high wholesale prices with low retail prices in the Steady State scenario otherwise.

National Grid has also provided its expectations of generation output. The two “high green ambition” scenarios show gas generation featuring strongly until the late 2020s after which it declines, replaced by a combination of nuclear and interconnectors. Gas has high importance throughout the Steady State scenario, but is also replaced by nuclear in the Consumer Power scenario, albeit much later than in the “high green ambition” scenarios.

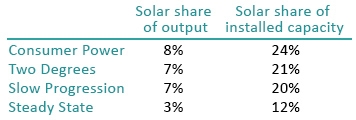

Wind generation is high in all scenarios, and solar is low (clearly solar’s possible hours of operation are limited) – comparing solar’s contribution to output compared with its share of the installed base tells us that:

It’s far from clear why a “low green ambition” scenario would have such high levels of renewable generation, particularly when the scenario suggests that this puts upward pressure on prices. A more realistic Consumer Power world might be one in which there is little growth in renewables as all subsidies are low, but where, unlike the Steady State scenario, there is meaningful investment in new nuclear.

Investments in interconnector capacity might also be lower than suggested in this case, as consumers and policymakers might be more sceptical and less willing to invest in capacity which may give more benefit to neighbouring countries. (See previous analysis showing the coincidence of high UK demand with high levels of electricity exports via the interconnectors.)

It is also interesting to note that none of the scenarios show any decline in wind generation, and the only scenario showing a fall in wind capacity is the Steady State scenario where onshore wind capacity declines after the late 2020s. Government figures suggest a typical lifespan of 20-25 years for a wind turbine, meaning that in the period to 2050, turbines currently in use would have to be replaced. In scenarios where renewable subsidies are low, it is unclear what would drive the replacement of these assets. Subsidies apparently continue to support growth in renewables in the “high green ambition” scenarios, so it is surprising not to see a reduction in all wind capacity and output in scenarios where subsidies are lower or absent.

Huge amounts of capacity needed to meet demand in a high-renewables world

Whatever one might think about the likelihood of the various scenarios, what is very clear from the details presented by National Grid is that in a world with high levels of renewables and strong commitment to de-carbonisation targets, a massive amount of additional generation capacity will be required. As demand will grow by significantly smaller levels, much of this capacity will have low utilisation, meaning that high levels of subsidies will be needed to support this capacity. Prices will be high and productivity low, as investments in capacity will be economically inefficient.

Further problems will arise since there will be times when there is a significant amount of surplus generation, particularly on sunny and windy summer days. In this case there will be three possible courses of action: export, storage or curtailment. Export would be limited by overseas demand, which may be similarly low if neighbouring countries follow similar energy policies; storage is likely to be limited by size and the unfeasible levels of storage that would need to be built (and indeed, the amount of storage predicted by National Grid is only 10.7 GW in 2050), leaving curtailment as a being highly likely.

In other words, consumers would be paying eye-wateringly high electricity prices in order to support the construction of vast quantities of under-utilised capacity, some of which may even be paid not to run. Perhaps it is no coincidence that National Grid has named the scenario under which economic prosperity is high and green ambition low “Consumer Power” – but even so, consumers would benefit more from an approach which avoided wasteful investments in assets with low expected utilisations.

…”that in a world with high levels of renewables and strong commitment to de-carbonisation targets, a massive amount of additional generation capacity will be required”….

…unless you build nuclear.

And there you have it. The primary assumptions in this whole exercise would seem to be that

– energy gets more expensive

– more and more renewables are imposed on the grid

– more and more embedded technology that can’t be controlled is imposed on the grid.

– more and more electricity is needed for electric cars etc.

And yet if we remove a single element – the carbon emissions element, NONE of this applies.

Frackable gas will keep energy prices more or less the same

There is no point in having any renewables on the grid

There is no point in having any more embedded generation.

There is no point in massive transition to electric vehicles in a huge rush.

Couple that with the opportunities that Brexit offers of removing the nation from EU ‘renewable obligations;’ unilaterally, an exit from Euratom and a chance to redraft regulatory frameworks for nuclear in the 2020s, and thereby reduce costs to at or approaching gas for baseload (high capacity factor) plant, and a totally different picture emerges.

– Energy costs stable or lower than today, in real terms

– No new renewable and a rapid reduction in subsidy for existing

– Gas used for summer peaking and winter baseload with

– existing hydro and pumped storage used for short term demand following.

– existing and new nuclear up to around 35GW to cover summer baseload with modest availability (scheduled maintenance for summer), and high winter capacity and availability factors.

To understand the justification for renewable energy requires that yiu accept ALL the following propositions are true.

1/. That man made global warming is a fact, and it is of a significantly alaraming level.

2/. That it is in the main caused by CO2 emissions.

3/. That reducing CO2 emissions will impact it significantly.

4/. That renewable energy ( so called ) is an effective way to achieve that reduction.

5/. That reducing emissions is more cost effective than e.g. slowly adapting to slowly rising sea levels and a slight change in the geographical distribution of food crops.

If just one of those propositions is false, the case for renewable energy falls away.

I suspect all 5 are false.

I agree, but I don’t have confidence that Brexit will stimulate the changes needed because the UK’s commitment to de-carbonisation pre-dates the relevant EU directives. Until politicians can accept that “sustainability” and “de-carbonisation” are not the same thing, and that the arguments for de-carbonisation don’t actually stand up, I can’t see things changing.

I never expected Brexit to stimulate changes, but it at least removes a major barrier to implementing them.

If the UK decides that by and large Climate Change™ is bunk, or Renewable Energy™ is largely ineffective as a remedy, then it should have the power to scrap renewable obligations.

The stimulus is coming from a growing number of people, perhaps you and I included, who are voicing extreme concerns over what we see as politically motivated knee jerk policy that is at odds with sober cost-benefit methodology for arriving at fact based decisions.

Thanks Kathryn and Leo.

I need to read through the document again and consider the detail of your comments Kathryn – I have little business experience or knowledge of the electricity market. So I am learning (and forgetting) all the time.

I appreciate your summary of the situation Leo and I agree. I see stigmatising CO2 as the root driver of many of our Gov. policies.

Elsewhere I have seen the multiplicity of the policies as a fragile pyramid of cards. I see the stack of cards has three dimensions and they are all balance precariously on a point, CO2.

Brexit just adds uncertainties. It may well be made a scapegoat for things going wrong with other power policies.

Nick.