When people think about energy storage, their minds tend to leap to electricity storage technologies like batteries or pumped hydro, however energy is also stored in raw material form…piles of coal by a power station or as gas.

In July Centrica announced the closure of its 2.7 Bcm Rough gas storage facility until Spring 2017 due to the extension of a well testing programme. Winter-summer price spreads and gas price volatility have steadily fallen in recent years, making it increasingly difficult for traders to profit from using the facility, impacting the value of the storage units Centrica was able to sell.

Falling profitability inevitably leads to under-investment in maintenance as well as a wider reluctance to invest in new sites, leading to the current situation with the UK’s gas storage capacity being cut by 78% in the wake of this closure.

Subsequently, in August, Centrica announced that 20 of the 30 wells would be available for withdrawal of gas from 1 November, so that gas already in the reservoir could be delivered during the winter. The volumes in question are small compared with the usual available withdrawal volumes for the winter.

So what’s next for the UK gas market and what if any impact will this development have on the coming winter?

Background

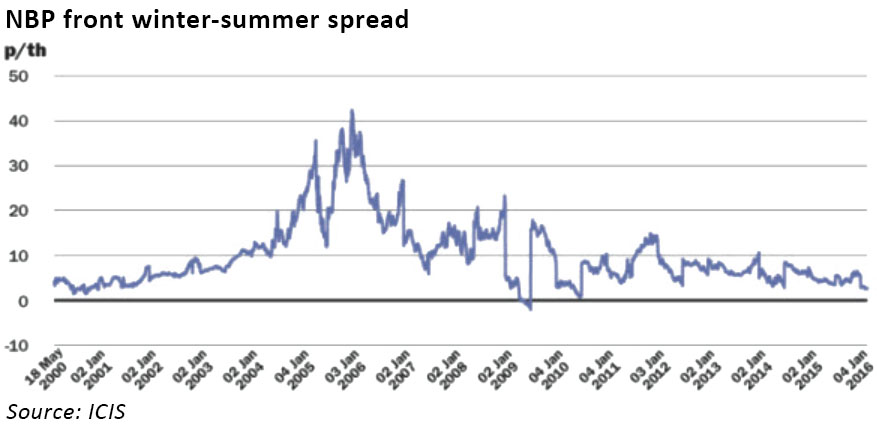

The value of seasonal gas storage strategies derives primarily from the difference between winter and summer gas prices. Traders and utilities typically buy gas in the cheaper summer months for injection into the facility, and then withdraw it in the winter to take advantage of higher market prices. Additional value can be derived by fine-tuning the seasonal strategy, re-hedging the winter position into individual months as the forward instruments become liquid to trade, and by churning some volumes throughout the storage cycle to capture short-term arbitrage opportunities.

Since the highs of 2006, seasonal spreads have fallen as shown in the chart below. This decline, and a decision in 2013 by the UK government not to subsidise the construction of new facilities, has led to the cancellation of around 17 Bcm of storage projects in the UK.

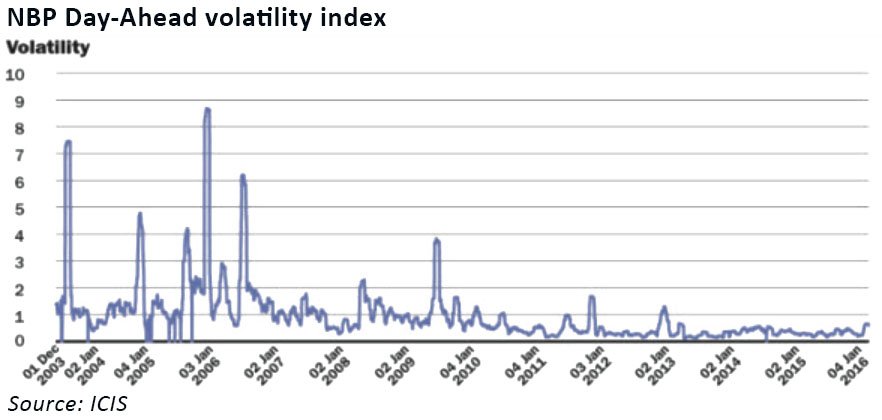

In addition to falling spreads, the UK gas market has also seen price volatility decline, reducing the profitability of storage-related trading strategies. Essentially low volatility reduces the real option value of a storage position.

Does gas storage matter?

The closure of Rough which accounts for 78% of the UK’s gas storage capacity means we will enter the coming winter with both very narrow supply margins on the power side and significantly reduced flexibility on the gas side. The question is whether this matters.

The past few winters have been unusually benign, with the most recent severe weather occurring in 2011, when the country experienced a prolonged cold snap that spanned the end of the winter season and the first weeks of the following summer.

This timing meant that Rough was already fairly empty in line with its traditional injection and withdrawal cycle, so the additional demand could not be met from storage. Market prices therefore rose, and the UK relied on increasing its imports from the Continent via the interconnector, and from increased production from those gas fields capable of swinging their output. Although prices were higher than normal during this period, the increase was not particularly dramatic, except during a brief outage on the interconnector, which saw within day prices rise to 150 p/th. A couple of pre-planned LNG deliveries further reduced the pressure on the system, which coped well with the unexpected surge in demand at the lowest point of the storage cycle.

Analysis I carried out at the time showed that the duration and amount of the raised prices was not sufficient to attract LNG away from Asian markets, which were then the highest priced markets for gas in the wake of the Fukushima disaster. This confirmed the prevailing view that the European market was significantly long gas and that additional investment in gas storage was not justified.

Since then, the global gas market has re-balanced. Asian prices have fallen significantly, and new supply, notably from the US has come on stream. The European market continues to be very well supplied, and there does not appear to be any prospect of tightening in the near future. Indeed, the past year has seen record exports of gas into Europe by Gazprom, which has further capacity to deliver more in case of need. Gas prices have been bumping along at fairly low levels as a result and volatility remains subdued.

What history tells us

There is some precedent to inform what the impact of Rough’s closure might be. In 2006 a compressor fire caused Rough to be out of action for 9 months. A 2011 study by the Universities of Nottingham, Vernona and Warwick found that “the major impact on activity was through an increased sensitivity of supply to prices and an increased variance in this sensitivity, not through physical shortages of gas.”

The paper describes a gas market where short-term changes in demand are driven solely by temperature and not price, and that overall system demand was not measurably affected by the fire. Gas prices and gas price volatility both rose significantly, and it was the increase in volatility that the authors felt was more relevant in the security of supply question: had the impact been solely on price, changes in price due to higher demand could be managed through hedging without the need for physical storage.

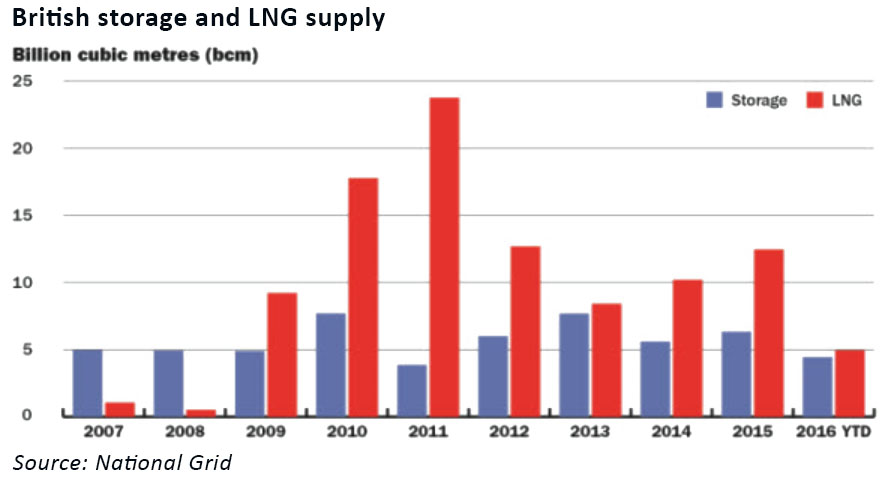

Since the 2006 fire significant sources of flexibility have been added to the UK market, including new LNG capacity with 0.2 Bcm of storage space, new fast-cycle storage, and the commissioning of the Langeled pipeline bringing gas from the large Norwegian fields. These all serve to reduce the importance of Rough to the market.

Prospect for the coming winter

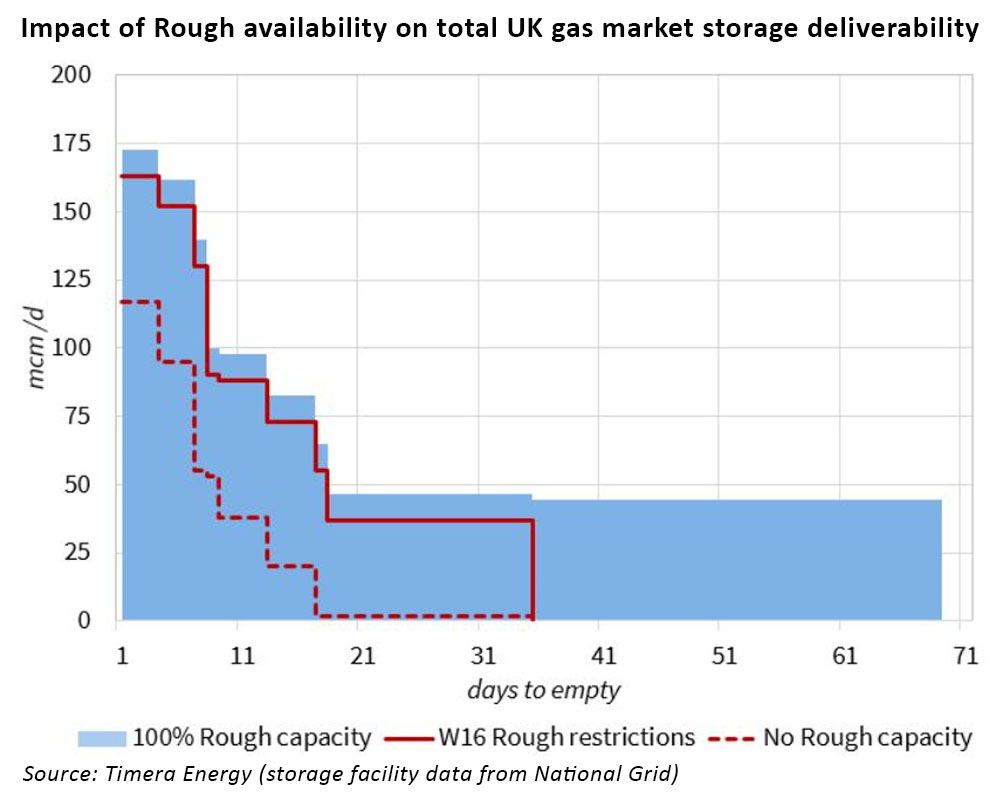

As Timera Energy argues in this blog post, the issue is less around the volume of available storage and more around the deliverablity of gas into the market. Without Rough, the UK would only have around 18 days’ of deliverability, resulting in greater price volatility and more spikes, making fast-cycle storage which is able to quickly respond to such signals, more valuable.

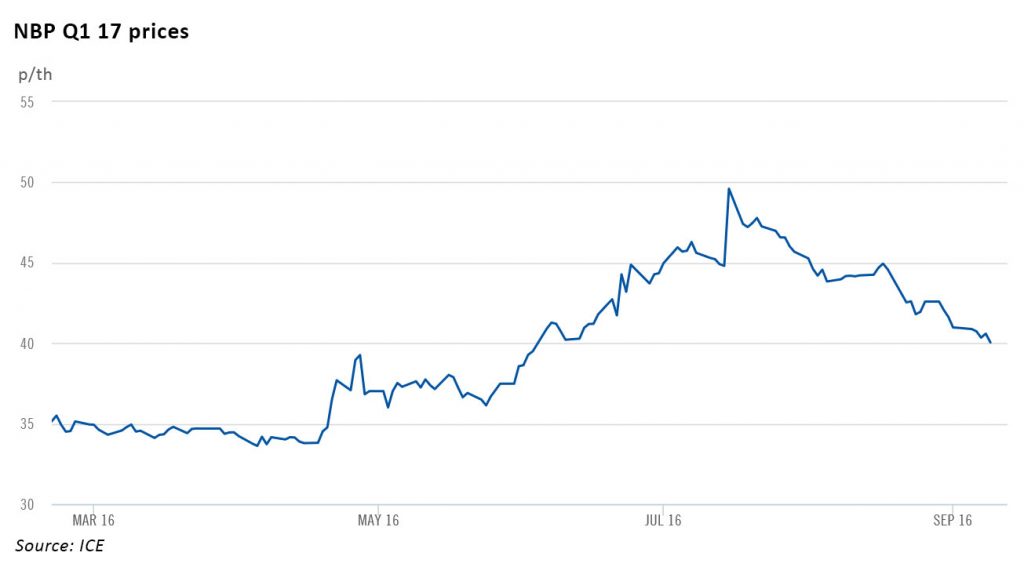

When Centrica originally announced the closure of Rough, NBP front winter prices moved up by 3.2 p/th to 46.65 p/th and the Q1 17 price rose by 3.675 p/th. The announcement in August of some deliverability through the winter prompted a fall in the Winter 16 price of 1.063 p/th to 40.758 p/th and a drop in the Q1 17 price of 1.525 p/th to 42.575 p/th.

Over the past weeks, the market has reacted with increased LNG deliveries and the system is currently long, putting significant downward pressure on the prompt. This highlights the fact that markets can and do respond to newsflows, and the timing of Centrica’s announcements has provided enough notice for suppliers to line up LNG deliveries through the winter in response to anticipated demand.

As a result, the likelihood is that the UK will cope quite well with the absence of Rough this winter.

Of course the real test would be a period of prolonged cold weather, but given the narrowing of the global LNG price differentials, prices would not need to rise by much to make the UK the market of choice for uncommitted cargoes. Clearly LNG diversions are not immediate and the market would face sustained higher prices while waiting for the additional LNG to arrive, but this would be measured in weeks rather than months.

In terms of pipeline gas, UK prices would need to rise above European prices to stimulate imports. European markets in general are well supplied, so while cold weather will result in higher prices across the board, the question is to what extent the lack of Rough will exacerbate the situation.

An extended period of increased demand due to cold weather would be the ultimate test of the Government’s decision not to subsidise additional gas storage, and would provide a real-life demonstration of whether the costs of investing in new facilities for security of supply reasons would be justified by the costs of an extended period of cold winter weather.

It seems unlikely that a single cold winter would be enough to support the necessary investment, even if Rough remained out of the market, but the increased volatility might make the economics of fast-cycle storage more interesting. Time, and weather, will tell.

Leave A Comment