Back in February I wrote an analysis of energy supplier OVO, concluding that it faced a real risk of ceasing to trade in the coming 12 months. This week, after being for sale for some time, OVO, the 4th largest supplier by market share announced that it had sold its retail supply business to larger rival E.On (3rd largest). This marks a major consolidation of a sector that was supposed to be transformed by challenger entrants. In effect, yet another challenger supplier is biting the dust.

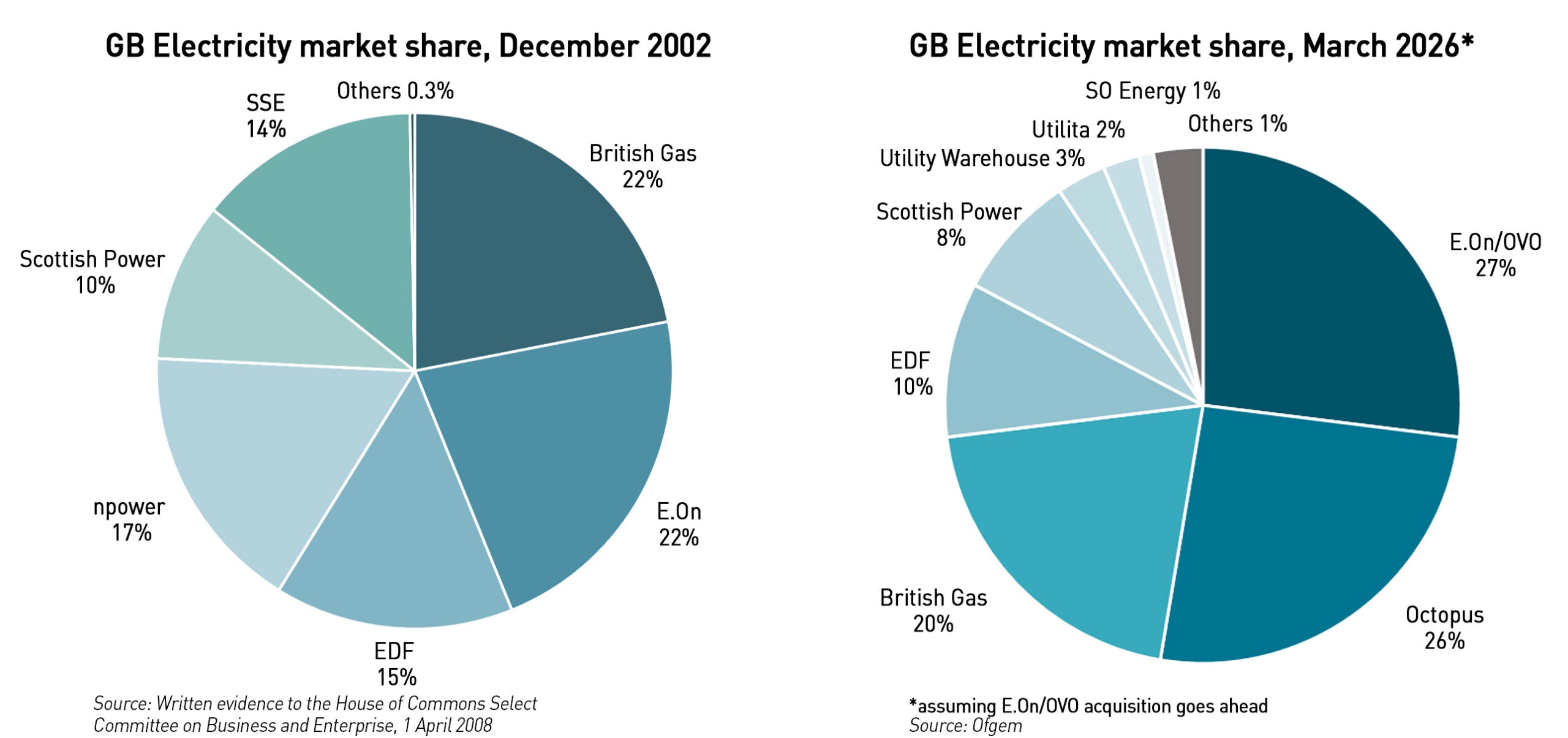

The reported sale price sets a very modest valuation for the business of around £600 million with the combined business overtaking Octopus as the largest UK supplier with 9.6 million customers.

That is an astonishingly low valuation in the context of the pricing narratives surrounding the business only a few years ago, and it is difficult to avoid the conclusion that the concerns raised in my original blog about OVO’s financial situation were justified and that concluding that without additional capital or a buyer it faced a real risk of being unable to continue independently.

Back in 2019, Mitsubishi acquired a 20% stake in OVO at a valuation reportedly close to £1 billion – the Japanese company paid £216 million for a 20% stake, at a time when OVO had 1.5 million customers versus 4 million today. On a £ per customer basis this implies the valuation has fallen from £720 to £150 – a decline of almost 80%. Despite a huge growth in customer numbers since 2019, the business is only worth around 60% of what it was then. A dramatic fall by any standards.

When Mitsubishi bought in, OVO was widely portrayed as one of the great success stories of the UK retail energy market being a fast-growing digital challenger supposedly disrupting the legacy “Big Six” suppliers with superior technology and customer engagement. The following year OVO acquired SSE’s retail business for roughly £500 million, transforming itself overnight into one of the UK’s largest domestic suppliers and further reinforcing the narrative that it was building a major independent energy platform with substantial long-term strategic value.

But only a few years later, the core retail business has been sold back to one of the very incumbents it was supposedly disrupting, and at a valuation that suggests the market is assigning surprisingly little value to the underlying supply operation.

Like Octopus, a key part of OVO’s value has been in its software arm, Kaluza. This was sold by OVO Energy (the entity being bought by E.On), to OVO Holdings Ltd, the parent of its parent (OVO Finance Ltd), for £185 million. Of course, this may have under-valued the business which may explain some of the apparent reduction in valuation since 2019, although minority shareholders and lenders may object if they thought that was the case.

E.On is not buying Kaluza but will continue to use it for the OVO customers, for now at least – E.On uses Kraken, recently spun off by Octopus, for its existing customers.

Historically customer books in the energy sector often attracted materially higher implied valuations, particularly where recurring profitability, strong retention and cross-selling opportunities existed. But the economics of retail supply have changed fundamentally since the supplier collapse crisis of 2021–22, with Ofgem imposing much stricter capital adequacy requirements while simultaneously maintaining a price cap regime that compresses margins and leaves suppliers carrying substantial operational, hedging and working capital risks.

That deterioration was visible in OVO’s accounts, as I discussed in my previous blog. The company had disclosed “material uncertainty” relating to the business after failing Ofgem’s financial resilience stress tests, which is not routine language found in company accounts, reflecting genuine concerns around liquidity, funding or covenant resilience. In the past year, OVO has cut hundreds of jobs, with Sky News reporting in November that OVO had been trying to raise roughly £300 million of new equity “for months”. This along with the previously described high interest debt it had taken out strongly reinforced the impression that the business was under considerable financial pressure.

The accounts also revealed the extent to which the retail supply model had become dependent on external financing and balance sheet strength rather than simply customer growth. Retail energy supply is a working-capital intensive business since suppliers must effectively finance customer consumption, collateral requirements, hedging and regulatory obligations, and this becomes particularly difficult when margins are thin and volatility is high. As a result, net debt levels, shareholder funds and liquidity buffers are important but often obscured in the more excitable “tech disruptor” narratives around some of the challenger suppliers.

This is important because much of the valuation narrative surrounding OVO in previous years seemed to rest on the assumption that customer scale itself automatically translated into strategic value and long-term profitability. But customer accounts are only valuable if they can generate sustainable returns after accounting for hedging costs, bad debt risk, capital requirements, regulatory compliance and customer acquisition costs, and this was broadly the opposite of the story told by the OVO accounts.

The comments made by Stephen Fitzpatrick accompanying the sale are themselves revealing. He stated that energy retail is now “more regulated, more capital intensive and increasingly dependent on long-term investment and scale”, which is effectively an acknowledgement that the economics of independent retail supply have become extremely challenging under the current regulatory regime and that OVO no longer believed it could compete independently at the required scale, despite being the 4th largest supplier with 11% of the domestic electricity market. Prior to this deal, E.ON had 15%, British Gas 20% and Octopus 25%.

More broadly, the transaction indicates that the “challenger supplier” era is effectively over, and after the collapse of dozens of suppliers during the energy crisis the market is consolidating back towards a handful of very large, heavily capitalised players with sufficiently strong balance sheets to absorb volatility, regulatory change and working capital stress. Ironically, one of the companies that spent years presenting itself as the technologically superior disruptor to the incumbent utilities has now been absorbed by one of them.

It’s going to be interesting to watch what happens with Octopus. At the end of last year, Kraken announced that it had been sold with Octopus retaining just 13.7% of the business. I’m somewhat confused by this since according to Companies House, Octopus Energy still owns more than 75% of both the voting rights and the shares. To have failed to update this after 5 months would be a pretty long delay, particularly since Octopus took charges over the Kraken assets that were perfected almost immediately after the transaction.

The proceeds of the Kraken sale would strengthen Octopus’s capital position and probably bring it into full compliance with Ofgem’s financial resilience rules, but for how long? The Kraken announcement implies that Octopus shareholders have been restructured into owning Kraken directly rather than through Octopus (although in the absence of Companies House filings this is unconfirmed). If so, the rationale for injecting new capital into Octopus Energy becomes far lower, indeed in 2025 no new capital was received from shareholders despite investors pumping in more pretty much every year previously.

As I noted in my previous blog:

“Between 2021 and 2024, OEGL absorbed £1.56 billion of shareholder capital, while remaining loss-making for much of that period, including losses of £64.7 million in 2021 and £141.0 million in 2022. The scale and persistence of these injections suggest that shareholder funding has been structural rather than exceptional, raising legitimate questions about the sustainability of the business model once investor appetite or tolerance changes.”

It will be very interesting to see the 2026 and 2027 results (Octopus has an April year end) to understand whether the supply business can become self-sustaining, and whether it adopts a more conventional business model, imitating the incumbents it was built to challenge. If not, we may see Octopus joining OVO in seeking a better capitalised buyer, and then the “challenger supplier” model will truly be dead.

Either way, in a few short years, we have gone from a “Big 6” dominated market, to a fragmented one, and now to one dominated by a “Big 3” with 73% of the market – more than the 57% held by the top 3 in the very early years of the market. (Suppliers were created by the Utility Act 2000 – before that consumers were forced to buy electricity from their local network operator.)

More fundamentally, the trajectory of the market may suggest that the entire policy objective of creating a highly dynamic retail energy market characterised by constant new entry, disruption and innovation was somewhat futile. Electricity supply is not a normal consumer market – the underlying product is largely homogeneous, margins are structurally thin, working capital requirements are enormous and the risks associated with hedging, collateral and regulation are substantial.

Under those conditions, the natural equilibrium may simply be a relatively small number of very large, conservatively managed firms with strong balance sheets and utility-like or retail bank-like economics. In that sense, the repeated cycle of new entrants, aggressive growth, capital injections and eventual consolidation may not represent a temporary market failure at all, but rather evidence that policymakers were trying to force a fundamentally unsuited market structure onto the sector.

Years of obsession with switching and the model of competition pushed for so long by successive governments and Ofgem is largely in tatters. And that might not be a bad thing, Utilities should be boring. A sensible next step would be to recognise that these dull businesses have more in common with banks (holding customer money and doing accounting) than with energy generators or network operators, and should be regulated as such. By the banking regulators.

It’s not a market since the government introduced a price cap. Octopus are cash strapped I reckon. They keep trying to increase my direct debit despite me being in credit at the start of the low usage summer period.

With a market of this shape, with a government price cap, how long before a left-leaning party simply decides to take the lot back into public ownership, at least in the domestic sector, and what would be lost if that happened?

Very logical blog

A physics joke: Kaluza was made Klein and the charge disappeared into the 5th dimension as an Ovoid. The danger now is there will be calls to nationalise energy retail altogether. A monopsony buyer and monopoly provider would remove the last vestiges of competition from the supply chain, leaving it to the whims of Ed Miliband (Prop.), who already controls NESO as its Sole Member. Not a desirable outcome. We need alternatives to that, and the restoration of competition in the suppply chain – better, cheaper grid design, more rational markets for technologies of supply, removing obstructions to nuclear (see properly implementing Fingleton Review), and domestic development and use of gas oil and even coal, and an end to artificial supports for renewables.

The latter includes the huge bung they get via the allocation of network charges, with most of these being socialised across demand. Those are set to escalate alarmingly under the OFGEM programme for More Grid, as recently revealved by NESO in their estimates for TNUoS charges. If power generators were charged on the basis of delivery to a notional balancing point, including full capacity entry costs, then distant, intermittent wind farms would be completely uneconomic, and would become uninvestible – even with the other subsidies still in place. Replacing the nuclear netork we used to have would be immediately much more attractive.

As CEO of the most innovative challenger brand, a business that has withstood everything that the government and the market has thrown at us over the years, I beg to differ.

As the CEO of the most innovative challenger brand, a company that has withstood everything the government and the market has thrown at us over the years, and is still growing, I beg to differ.

Good article – a depressing outcome for this industry

which looks to be heading back to nationalisation

I hardly know how you find the time, if you want to get things done ask a busy person. That a government could have created a monster like Dale Vance and given over domestic energy supply to techno9logy companies with a passing interest in hydrocarbons. Perhaps if they were honest as to how they make their money they would be harangued by those of the Green Persuasion, Just Stop Octopus? It comes down to you against the world. Pity Miliband won’t stand up and debate you. Then again, that would be beneath you dignity. Stay well.

Are we going to go full circle and see only one supplier for electricity and one for gas or will we see State ownership?

Another excellent piece Katherine.

With Octopus and others using customer credit credit balances as working capital and the low point being April they might suffer extra strain as May so far has been particularly cold..

It would be interesting to get your take on the further NESO problems with balancing the grid. Apart from the well known early January peaks with non existent solar and and a possible northern Europe high pressure system meaning low wind , it seems that mid summer might also be a problem with rising solar farm generation, and domestic solar uploads being unquantifiable on the local grid networks leading to balancing problems.

One final thing. We also know that in times of petrol and diesel scarcity everybody fills the tank completely and keeps filling until the garages are empty. If winter power outages occur or worse a total blackout will the relaunched grid cope with EV owners charging to 100% whatever the time of day or night whatever the cost.

I am certainly no expert on the structure of UK electricity market. However, UK retailers suffer many of same issue as US. Specifically, with renewables being forced onto the system operator’s grid, the only way to profit is technology installed in the customer connection that allows automatic demand side management via network connection controls, the code word for forced user outage. Unfortunately, the customers that are on-board with the electrification of everything are among the least likely to contract for this type of service. The more renewables, especially behind the meter solar, will weaken the UK grid further without significant automated control of customer’s ability to consume electricity.

Sorry I posted this to a 2025 blog by mistake – it needs reading as relevant to our energy crisis as a whole

Kathryn – I’ve just used A.I to look at a proposed massive storage system called MESH. It’s planned to be able to store 20TWh of energy through mainly Hydrogen in salt caverns – produced through over production of renewable energy – it has a possible completeion date of 2038 – 2045. So with inefficiences of energy conversion this might mean 5 – 7 TWh back out. So given the UK’s winter usuage this could keep the generators running for 7 days.

So as many older Gas generatots can only accept a 20% blend we could need . I supposose Hinkley + Hinkley C will be up and running by then, but existing gas powered stgations will have been retired. So, with MESH, we would have to build a whole new fleet of Hydrogen powered stations – which would cost a fortune. Plus, of course the cost of the storage caverns plus a stoarge system of 7 days will not be enough if we have a very low wind winter.

The whole thing sounds ridiculous as you’d also need expensice electrolysers to convert the excess electricity into hydorgen plus hydorgen pipelines.

Does anyone else think Miliband is crazy – Kathryn I hope you have time to read this- and perhaps do you own more detailed analysis.

Yes he is crazy. Hydrogen is not coming to the rescue in any meaningful way. They are just hoping to cobble together a bunch of stuff that might, sort of, sustain the grid. No particular plan. Here in the US we are seeing a plateau in utility scale battery installs. They have been used to meet peak hour demand as solar fades. They have harvested all the peak hours and are running into poor economics when they are getting paid for off-peak power.

To me, nuclear and gas have always been the answer. Threr are just too many economic downsides to renewables.

There is currently no official UK proposal for MULTI-DAY energy storage.

The only proposal is for Long Duration Energy Storage LDES;. The scheme is organised by OFGEM which is assessing fewer than 100 projects. Track 1 scheme are sized at 0.1 GW power production 8 hours.

In 2024 and 2025 onshore and offshore wind averages 9-10 GW 24 hours a day. Thus a single Track 1 proposal will provide about 0.33% of the electricity produced each day by wind.

The government is currently proposing to expand wind and pay billions to bring the power to where it is needed. It is totally reliant on aging gas turbines to fill the gpa when there is little wind. Periods of sustained low wind can sometimes last for a month or more. Will these old turbines run continuously for 28 days and what happens if they start to fail?

The UK needs a credible plan B to either augment the current gas turbines or expand nuclear or a mixture of both.

Nuclear can be more than just baseload – the French have the expertise to modulate their nuclear output to reflect the average daily cycle – for the avoidance of doubt – the power output follows a planned cycle rather than respond to demand

Have a look at the below documents

# ✅ **What documents the information came from**

Your earlier answers about MESH were based on these specific sources:

1. **EnergyPathways official MESH project page**

– Describes the project concept, compressed‑air storage, hydrogen production, and salt‑cavern system.

[energypathways.uk](https://energypathways.uk/mesh)

2. **Tank Storage / EnergyPathways article (March 2026)**

– Confirms the licence application to the North Sea Transition Authority (NSTA) and the plan for up to 60 salt caverns.

[oilgasstoragenews.com](http://oilgasstoragenews.com/energypathways-hydrogen-gas-storage-licences-mesh-project/)

3. **FuelCellsWorks report (May 2026)**

– Confirms that EnergyPathways *has been awarded* a Gas Storage Licence (GSL) by the NSTA — a major milestone.

[Fuel Cells Works](https://fuelcellsworks.com/2026/05/06/energy-innovation/energypathways-secures-uk-gas-storage-license-for-mesh-hydrogen-ready-project)

4. **Offshore Engineer Magazine (Nov 2025)**

– Confirms expanded licence applications, government designation as a “nationally significant” project, and intention to submit a Development Consent Order (DCO).

[Offshore Engineer Magazine](https://www.oedigital.com/news/532795-energypathways-files-expanded-license-for-mesh-gas-and-hydrogen-storage-scheme)

These are the authoritative documents that underpin everything.

—

# ✅ **What stage the MESH project is currently at (as of mid‑2026)**

### **1. Gas Storage Licence AWARDED**

EnergyPathways has been awarded a **Gas Storage Licence** by the North Sea Transition Authority.

This is a major regulatory milestone and allows development of up to **60 offshore salt caverns** for hydrogen and natural gas storage.

[Fuel Cells Works](https://fuelcellsworks.com/2026/05/06/energy-innovation/energypathways-secures-uk-gas-storage-license-for-mesh-hydrogen-ready-project)

### **2. Expanded licence applications submitted**

EnergyPathways has applied for **additional hydrogen and gas storage licences**, expanding the project area nearly fourfold.

[Offshore Engineer Magazine](https://www.oedigital.com/news/532795-energypathways-files-expanded-license-for-mesh-gas-and-hydrogen-storage-scheme)

### **3. Recognised as a “nationally significant” project**

The UK Secretary of State for Energy Security and Net Zero has confirmed MESH is a **nationally significant infrastructure project**, which accelerates its regulatory pathway.

[Offshore Engineer Magazine](https://www.oedigital.com/news/532795-energypathways-files-expanded-license-for-mesh-gas-and-hydrogen-storage-scheme)

### **4. Development Consent Order (DCO) preparation**

EnergyPathways intends to submit a **DCO application** for the onshore and offshore elements.

This is the formal planning process for major UK infrastructure.

[Offshore Engineer Magazine](https://www.oedigital.com/news/532795-energypathways-files-expanded-license-for-mesh-gas-and-hydrogen-storage-scheme)

### **5. Pre‑FEED / early engineering stage**

The project is still in **pre‑construction**, with engineering design, environmental assessments, and regulatory approvals underway.

The official project description emphasises long‑duration energy storage, compressed‑air storage in salt caverns, and hydrogen/graphite production.

[energypathways.uk](https://energypathways.uk/mesh)

—

# ✅ **Simple summary of the current status**

– **Not yet under construction**

– **Gas Storage Licence awarded** (big milestone)

– **Expanded licence applications submitted**

– **Recognised as nationally significant**

– **Preparing Development Consent Order**

– **Still in pre‑FEED / planning and regulatory phase**

– **Targeting up to 60 salt caverns for hydrogen and gas storage**

– **Designed as Britain’s largest integrated energy‑storage hub**

—

Government involvement is regulatory, not ownership

The UK Government has designated the MESH project as “nationally significant”, but that is a planning status, not ownership.