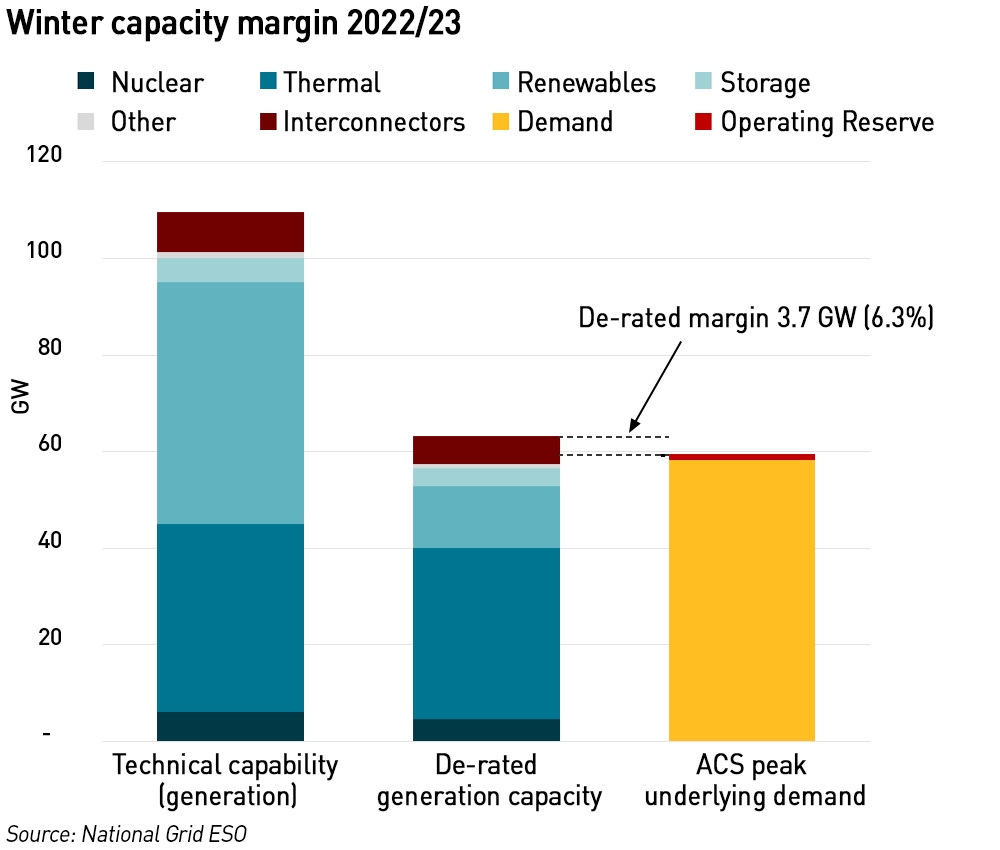

Today, National Grid ESO published its Winter Outlook for 2022/23, updating its position since the early outlook issued in July, which was widely seen as unrealistic. The position in July was that a capacity margin of 4.0 GW was expected, a small increase on 3.9 GW last year. While the final outlook does revise the figure downwards slightly, at 3.7 GW (6.3%) it still looks very optimistic. The Average Cold Spell (“ACS”) demand is assessed a little lower than in the early outlook at 58.3 GW versus 59.5 GW.

Unlike the early outlook which relied on interconnectors, NG ESO appears to now be relying on new tools it has developed to manage risk capacity risks – the coal contingency contracts and, in particular, demand reduction including the new Demand Flexibility Service though which businesses and households can be paid to move their demand out of peak hours.

NG ESO claims to have secured three contracts with coal generators “to keep 5 coal units open and on standby this winter to generate up to approximately 2 GW of additional power” – this is misleading…I asked EDF outright about the situation at West Burton A, and it confirmed that it has only agreed to make 1 unit available at any time, and then only at 80% of capacity. It would be more accurate to say that these contracts deliver 4 units at 1.9 GW (one 500 MW unit at Ratcliffe, two 500 MW units at Drax and one 500 MW unit at West Burton A operating at 80% capacity ie 400 MW).

The Demand Flexibility Service is projected by NG ESO to reduce demand by up to 2 GW, however, I have heard from industry sources that there is unlikely to be much take-up from the domestic sector since the prices offered are considered to be too low. It is also a day-ahead service that can only be accessed by households which have a functioning smart meter and act through their supplier or an aggregator. I do, however, believe that the public would respond well to voluntary demand reductions / load shifting requests should a system stress event occur, providing the required actions are appropriately communicated.

Winter outlook ignores the risks of low wind and is over-optimistic about imports

Another problem with NG ESO’s base case is that it assumes capacity across all providers (generation, storage, interconnection etc.) is available in line with Capacity Market commitments. This is likely to be optimistic for two reasons: not de-rating wind capacity enough and over-estimating imports.

The winter outlook models the capacity available to meet ACS demand. It would therefore make sense to consider the generation that is likely to be available during cold weather rather than the generation that is available on average through the year. There can be a high correlation between cold weather and still weather, so the de-rating factors used for wind in the Capacity Market which considers annual averages may be too high.

The Capacity Market de-rating factors for wind are 16.1% for both on-shore and off-shore wind (compared with 17.4% last year). However reducing this to 5% would cut de-rated capacity by just under 3 GW, and a reduction to 1% would be a reduction of more than 4 GW. On still days, wind output can be as low as 1% of installed capacity, so this is not an unrealistic scenario – low wind conditions can easily destroy the capacity margin.

In addition, the Capacity Market rules only require interconnectors to be available, they do not require them to be importing. An interconnector could meet its Capacity Market obligations whilst in export mode.

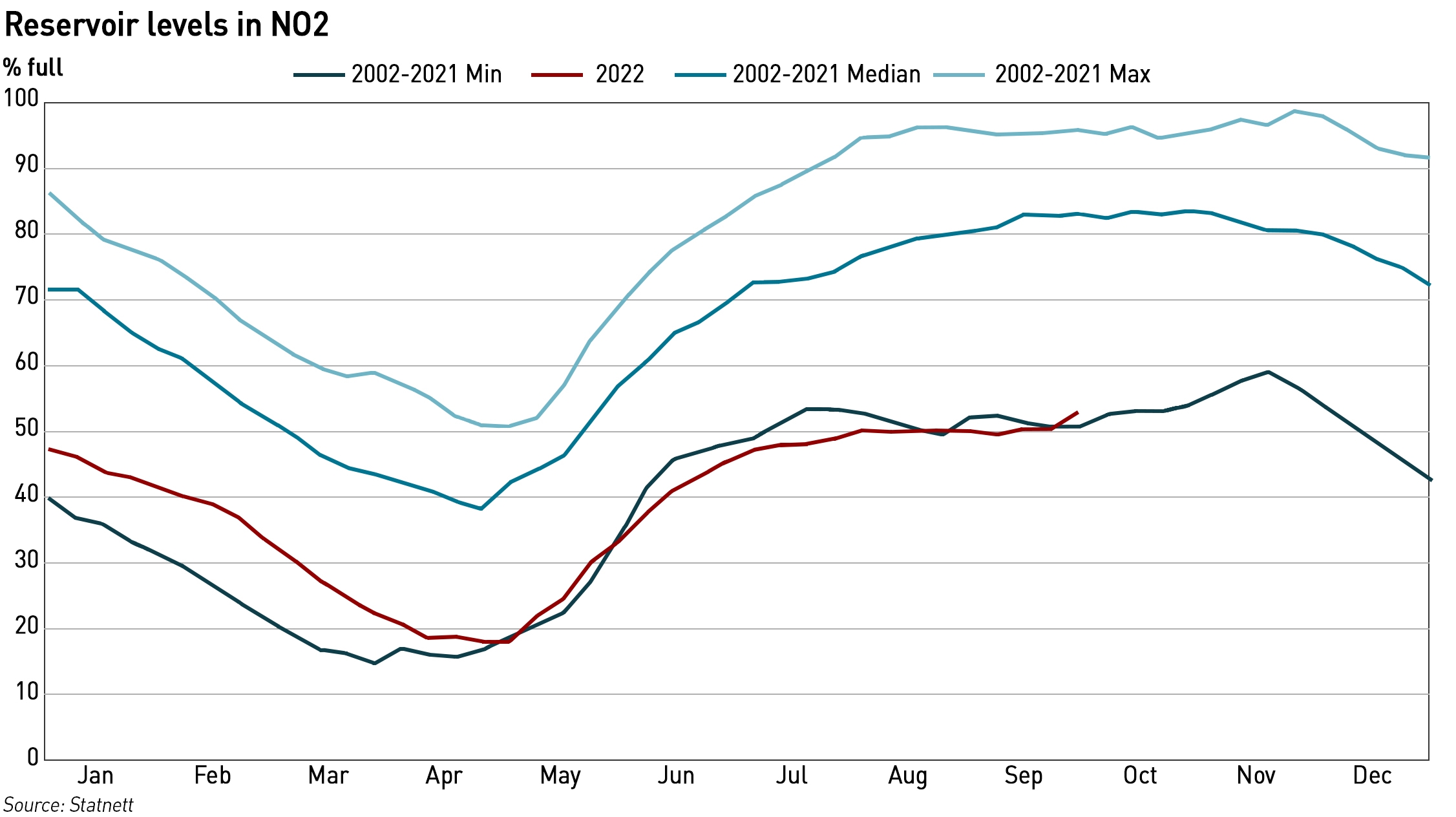

The risk of exports is high, since France has been consistently importing from GB since April when the corrosion problems with its reactors was first identified, and French grid operator RTE expects imports to continue through the winter (see below). In Norway, the Government is developing a mechanism whereby electricity exports would be restricted if reservoir levels are too low (see below), so there is no guarantee imports to GB would be available when needed.

NG ESO has considered a more pessimistic scenario which reflects lower import potential (no imports from France, the Netherlands or Belgium; but the full 1.4 GW of imports possible from Norway; and 0.4 GW exports to Northern Ireland & Ireland). It says that in this “hypothetical alternative scenario” it would deploy the reserved coal units and activate the Demand Flexibility Service. It believes the 4.0 GW available by these means would cover any import shortfall, with a spare margin of 3.3 GW. I would argue that imports from Norway are more at risk than those from the Netherlands and Belgium.

The Demand Flexibility Service will launch on 1 November – NG ESO sees particular potential from commercial organisations who can load shift, and says it has had positive feedback from businesses on the service.

“Without the deployment of the additional coal generation units or the new Demand Flexibility Service, the ESO would expect to see a reduction in margins. In this scenario on days when it was cold (therefore likely high demand), with low levels of wind (reduced available generation), there may be the potential to need to interrupt supply to some customers for limited periods of time in a managed and controlled manner. However, the ESO expects the mitigations outlined above to be effective,”

– National Grid ESO

NG ESO also recognises that an escalation of the situation in Europe affecting gas supplies to GB – a situation it considers unlikely – would further erode supply margins, potentially leading to supply interruptions for short periods. This has caught the media’s attention today and I have done multiple interviews on the subject of whether rolling blackouts are likely this winter. In my opinion, they are not, before we would encounter blackouts, there are various measures that would be taken:

- Voluntary, compensated, demand reductions by businesses and households

- Mandatory demand reductions by businesses

- Appeals for unpaid voluntary demand reductions from households

This last measure could be very effective if properly communicated. However, this is not a desirable way to run the electricity system – it is important to recognise the risks and manage them proactively, ahead of time, rather than relying on short-term demand reduction to avoid blackouts.

Norwegian government developing measures to link electricity exports to reservoir levels

NG ESO appears to believe there are no risks to imports from Norway. However, the Norwegian government has announced measures that would restrict exports if reservoir levels were too low. The details of the scheme are yet to be announced, but the intent is clear.

On the 19 September, the Norwegian Parliament was recalled from its summer recess to debate the energy crisis. The Energy and Petroleum Minister Terje Aasland gave a speech in which he outlined various measures the Government is implementing to address the current energy crisis in the country where prices have soared over the past year. These include:

- A reduction in the electricity tax for 2022

- An increase in the electricity subsidy scheme for households to provide up to 90% relief on bills from 1 September (up from 80% last year). A typical family in southern Norway will now receive an electricity subsidy of around NOK 45,600 (£3,830) this year

- A mandatory reporting scheme for large hydropower producers to support security of supply, with producers being asked to hold back the water

- A new management mechanism to ensure more water is saved when reservoir levels are low and that the export of power in such cases is limited

- Market reforms to facilitate a simpler end-user market for electricity with better fixed price agreements that can provide greater predictability

- Increased measures to support households in reducing energy use or producing their own energy, and the government will make it easier for commercial buildings and housing associations to install rooftop solar panels

- Up to NOK 10 billion (£0.84 billion) of Statnett’s additional income will be used to prevent a significant increase network costs in southern Norway

- A business support package worth NOK 3 billion (£ billion) to help power-intensive companies, and contribute to reductions in energy consumption through energy management systems, insulation and installation of solar panels. Businesses are also being encouraged to switch to fixed price contracts. (Interestingly, unlike the business support package in the UK, the Norwegian scheme prevents recipients from paying dividends next year.)

The details of the hydro management mechanism are due to be published this autumn. Low hydro levels in the south of the country continue to be a cause for concern – in NO2 levels continue to hover around the 20-year minimum, and so far, the autumn is proving to be dry. At this time of year, both higher rainfall and snow in the mountains which quickly melts can boost reservoir levels by around 10% before snow begins to settle in mid-November, but so far this is not happening at the usual rate.

“Rationing has also been mentioned as a possibility in Norway. It is nevertheless important to say that our energy authorities consider the probability to be low, but that underlines the seriousness…In the long term, there are only three measures that can really improve the situation in the Norwegian power supply – more power, more networks and more efficient use of our energy.

These are measures that prepare the ground for a green reindustrialisation of Norway and are leading the way for the government’s energy policy. In the short term, the government’s priority is to continue the work to protect and relieve people, organizations and businesses in the demanding situation. In 2022, we will spend around NOK 44 billion. on targeted measures to help cover the high electricity costs,”

– Terje Aasland, Norwegian Energy and Petroleum Minister

There have only been two years in the past three decades in which there has been less rainfall than this year: 2003 and 1996 in southern Norway, and 1996 and 1991 in eastern Norway. There has been unusually low rainfall since the autumn of 2021, which has led to very low groundwater and water levels.

At the same time, hydro levels in the north of the country are at record high levels, with low prices and abundant water making it difficult to optimise hydro plant operation. But the lack of north-south transmission capacity means that this surplus cannot be used in the more densely populated south of the country. With plans for electrification, it is expected that these surpluses will be eliminated in the coming years without the need for additional transmission infrastructure.

It was interesting that Aasland referred to decisions in other countries that are harming Norwegian interests such as the closure (or potential closure) of nuclear power plants in certain EU countries. Although Germany has now decided to keep two of its three remaining nuclear power stations open beyond the year-end closure date, the other will still close, as will the Doel 3 reactor in Belgium which is closing as part of that country’s nuclear exit plan (an action which has attracted local protests due to the energy crisis).

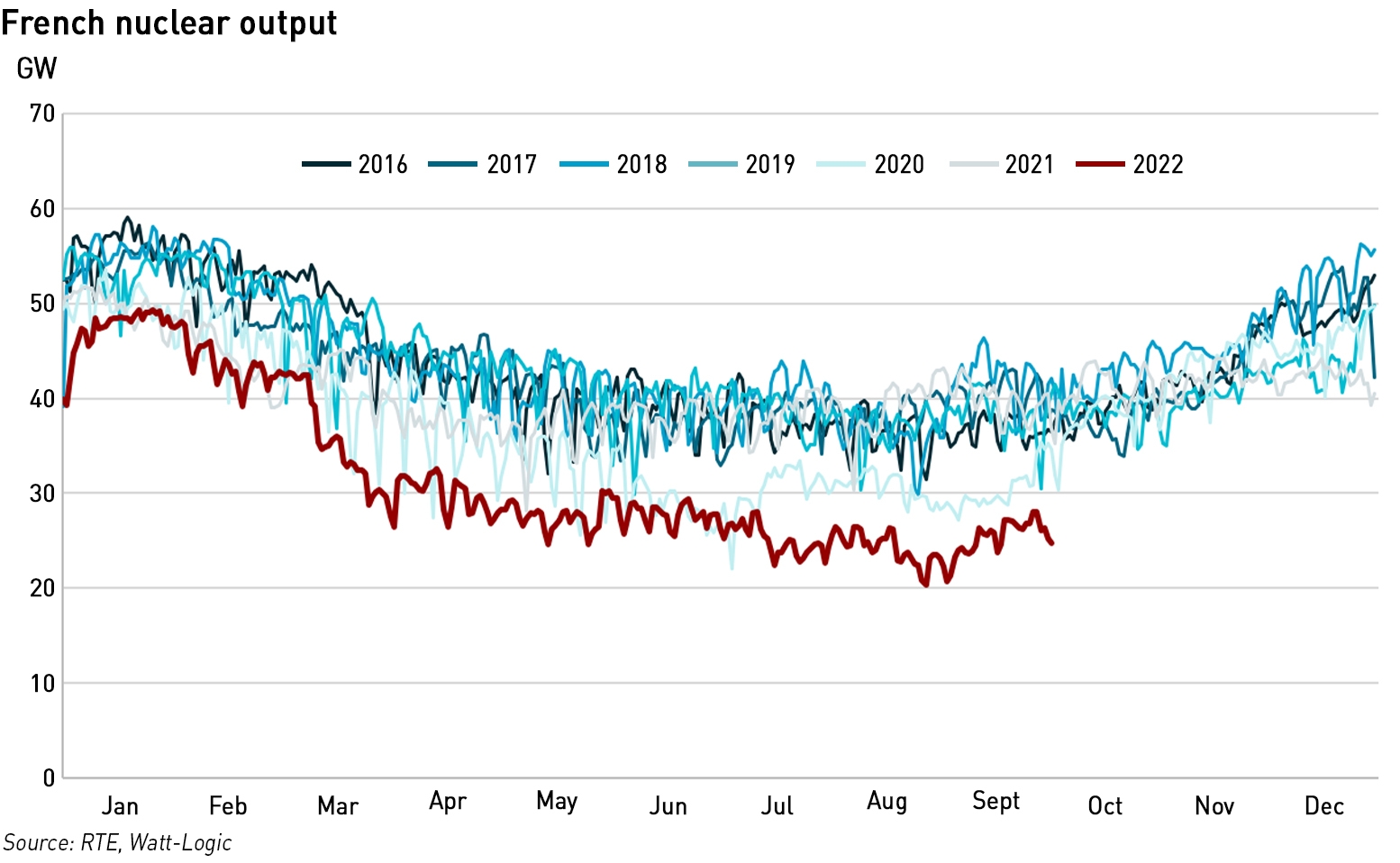

French grid operator expects to rely on imports this winter

Back in April EDF discovered corrosion problems in the cooling circuits of its P4 and N4 reactors, and was required by the French nuclear regulator, Autorité de Sûreté Nucléaire (“ASN”) to take them offline for inspection and repair. Since then, France has switched from being a net exporter to net importer of electricity, including from GB.

EDF has identified the pipework being most susceptible to the cracking – in the N4 reactors, these are in the safety injection circuit located in the “cold leg” (the pipes of the main primary circuit which go from the motor pump units to the reactor vessel) and in the pump lines of the shutdown reactor cooling circuit. In the P4 reactors, it is the pipelines of just the injection circuit located in the cold leg. In late July, ASN approved a three-year programme presented by EDF for rectifying the problems.

“As you know, 32 reactors are shut down, some for stress corrosion and others for routine maintenance. EDF has undertaken to restart all the reactors this winter. We are monitoring the situation closely with weekly updates and we are being especially vigilant to ensure that this schedule is kept,”

– Agnès Pannier-Runacher, Minister of Energy Transition

EDF has committed to re-starting all of its reactors this winter, with the French government pressurising it to maintain its timetable. According to EDF’s projected schedule, 27 reactors will restart by the end of December, with a further 5 starting between early January and mid-February 2023. This will return all 32 of the currently closed reactors to service, however the ultimate decisions rest with ASN.

Industry insiders question the company’s ability to meet these targets, particularly for the 12 reactors closed due to the corrosion problems. Repairing them requires long and complex processes, and the President of ASN, Bernard Doroszczuk, has warned that other problems may be detected, leading to the further closures. Some contractors working on the repairs have apparently agreed to relax their rules on radiation exposure limits to allow workers to spend more time on the job, although these times will still be well within legal standards.

In its winter outlook, French grid operator RTE said it expects to ask households, businesses and local governments to reduce energy consumption several times over the winter months, to avoid rotating power cuts although it does not expect any total blackouts. The risk of power cuts could be minimised by reducing electricity demand by 1% to 5% in most cases, but reductions of up to 15% could be needed in the worst weather situations, particularly between 8 am and 1 pm, and from 6 pm to 8 pm, on weekdays. There are also supply risks in the autumn due to the low availability of hydroelectric power – 33 TWh compared with an average of 43 TWh in previous years.

“If winter is mild, you probably won’t hear from us. If the winter is very cold, the likelihood is for about 10 red EcoWatt alerts,”

– Xavier Piechaczyk, Chairman, RTE

RTE presented three scenarios:

- In the best case scenario, nuclear reactors will quickly restart and reach 82% capacity by January 2023. This case also requires European gas markets to encounter little to no pressure, or for consumption to be strongly reduced;

- In the base and most likely scenario, about 75% of France’s nuclear capacity will be available in January, requiring significant electricity imports, with demand reductions also potentially needed, albeit in small amounts. In the event of very cold weather, temporary or localised cuts in electricity would need to be made;

- In the worst-case scenario, with both gas and nuclear shortages, power cuts would be “unavoidable if consumption does not decrease” even if the winter is mild.

To avoid full blackouts, RTE has said it can activate contracts allowing it to disconnect large electricity users, reduce voltage on the grid for a few hours, and implement rotating power cuts of up to two hours. The grid operator believes that the most extreme situations would require an unlikely combination of factors including very cold weather, a fuel shortage limiting the use of gas-fired plant and electricity imports, or very deteriorated nuclear output. In the worst-case scenario, the demand reduction alert known as “EcoWatt” could be used on 20 to 30 days during the winter.

RTE’s scenarios are closely linked to the availability of gas which is increasingly used for electricity generation in France. Gas use in the French power sector doubled in the first half of 2021 (to 24 TWh), and again in the second half of 2022 to reach about 39 TWh, according to gas network operators GRTGaz and Teréga who estimate that in a hard winter, the availability of gas could fall by 2.0% – 4.7%. A mild winter would be unlikely to affect gas supplies.

This has led the grid operators to urge consumers to save both gas and electricity produced by gas, to avoid depleting stored reserves too early in the winter, and for the throughput of LNG terminals to be optimised. GRTgaz is recommending that consumers reduce their heating by 1°C, saying this could lead to a 7% reduction in gas consumption. There are also voluntary paid cut-off schemes for industry, which have the potential to save 200 GWh per day, or about 5% of consumption on a very cold day. However, the gas operator has said that cuts will only be imposed on industrial consumers as a last resort.

Looking to the future, France is pressing ahead with its next generation EPR2 technology with plans to begin construction on the first reactor by May 2027.

“The goal is for the procedural part and authorisations to last less than five years and for construction work on the first EPR2 (rector) to start before the end of the presidential term, before May 2027…The latest timetable … sees commercial operations starting from 2035-36,”

– French government spokesperson

EDF plans to construct these reactors on three existing sites: two at Penly, in the Seine-Maritime region, two at Gravelines, in northern France, and two in either Bugey in eastern France, or Tricastin in southern France.

Suggestions that electricity may be rationed after all

Despite multiple assurances from Prime Minister Liz Truss that there will be no electricity rationing in GB (not something that politicians can control in any case), there are now indications that BEIS is working with NG ESO and industry on demand reduction and load-shifting measures, as fears grow over potential electricity shortages. According to the Guardian, households could be asked to turn down thermostats, and to use appliances at times when energy demand is lower. The system would make use of the alert service that NG ESO uses to notify consumers by text, phone call or email when there are power cuts.

A public information campaign could help consumers to ease pressure on energy supplies by providing advice on changes to consumption patterns. Until now, the Government has resisted calls to ask the public to cut energy use, unlike its counterparts in Europe, however, analysis carried out by BEIS suggests that Britain could experience power cuts for four days in January if there are gas shortages and the weather is particularly severe.

It is clear that despite all of its previous rhetoric, NG ESO is finally recognising that the system could be tight enough to require load shedding this winter. Hopefully this will be achieved purely through voluntary means, but there is a risk of mandatory supply disruptions, particularly for businesses. However, the system operator still seems to be in denial as to the extent of the risks, which is not encouraging. I would urge NG ESO to consider whether its de-rating methodology is appropriate in the ACS case and reduce the contribution from wind. It should also recognise that the behaviour of interconnectors in system stress situations has never been tested in real life, and could deliver undesirable results such as exports rather than imports.

We need additional measures to ensure energy security this winter. The Government should:

- Negotiate to return the Calon CCGTs to the market as soon as possible

- Lift emissions regulations limiting the use of on-site diesel generation

- Explore dual-fuelling of CCGTs to protect gas supplies in the event of a gas disruption

- Negotiate with Norway to secure imports in times of system stress in exchange for exports at other times

I am no more re-assured by this updated analysis that I was by the early winter outlook. While I hope that capacity margins will remain comfortable through the winter, hope is not an appropriate way to manage risk. We need a more honest and accurate appraisal of the downsides, and appropriate action, if we are to avoid harmful supply disruptions this winter.

Hi Kathryn

A really good analysis as always. I attended the National Grid Winter Outlook briefing and agree that there is a certain level of optimism going on in what seems to be more of an attempt to reassure the public instead of being upfront about both the challenges faced and the actions that need to be taken. Two points in your analysis stand out for the GB market – firstly getting the two Calon plants operational should be a mjor priority, I wish someone could explain why it is seen as better value to pay hundreds of millions to keep coal units on strategic reserve and (ideally) never run whereas for a (presumably) smaller amount the Calon units could be made operational and would then actually run commercially over the Winter as they are both efficient and would be well in the money.

Secondly the UK govt needs to get real about the energy saving messages to consumers and set up a notification system to help people reduce demand at peak time in a managed way. However the govt seems terrified of being portrayed as telling households that they cant heat or light their homes in Winter but that is not the same as delaying running your washing machine, tumble drier or dishwasher for a few hours. None of those is essential but could shift enough demand if done in an organised fashion.

Like you I think the risks of power outages are very low, however it will be interesting to see how much needs to be paid to secure gas and / or interconector volumes if it is cold and still across Western Europe.

As if to support my comment about the UK govt’s irratational reluctance to help consumers ‘load shift’ this seems to be the current attitude – https://www.theguardian.com/politics/2022/oct/07/climate-minister-britons-not-be-told-use-less-energy-winter-nanny-state

The government are completely scared by the prospect of power cuts. It will undermine any possibility of being seen as competent. Fingers will point rightly at Kwarteng who failed to start taking action when we started seeing EMNs and rising gas and power prices almost two years ago now. The whole net zero plan is at risk if it gets seriously questioned. Hence the disinformation in the Winter Outlook, doubtless fully approved in advance by government.

Actually I can see some logic to their position…asking the public to reduce demand to avoid blackouts should only be done when it’s needed…if you start asking people now you risk them getting bored with it all and not doing what’s needed when it’s needed. Only asking people to load shift if there is an actual blackout risk will make it a lot more effective. It is different in Europe where they are aware that any gas they use this winter is potentially gas they won’t have next winter given the uncertainty around next year’s injection season. So Europe has an outright need to cut demand across the board whereas we only need to worry about when it’s not windy and imports are low.

But I do agree that there is a reluctance to admit that the approach to the energy transition is responsible for this vulnerability, and it’s not going away. What will they say in 2 years when the winters are even tighter and the Ukraine issue is largely resolved…

If we have a severe gas crunch then having the Calon units available won’t be much help at least with the coal units thats an alternative fuel source.

An excellent post. I am not reassured. Avoiding power cuts will be down to luck rather than careful forward planning. This is a vital national utility not a casino. Using untested methods of reducing demand is a desperate measure. Should the advice be specific or general, both have their downsides. Voluntary action taken at inappropriate times (particularly if set the day before) could make the demand more unpredictable and the peak sharper and larger. There is no mention of the tried and tested voltage reduction measure.

This mess will not be resolved in the short term but there is still time (just) to plan a path to a successful future. NGESO’s recent report “A Day in the Life 2035” states that on the current path “success is uncertain”. Lets leave the exciting casino and plan a boringly predictable but workable future.

A Day in the Life was prepared by sock puppet green consultancy/think tank Regen. It’s a Goldilocks world where the wind shortages are just right to be covered by V2G discharges and demand response and horrendously costly green hydrogen. Its relationship to any kind of reality is non existent. It does make a good fairy tale for those who are credulous and unable to think about 10 days of Dunkelflaute with snow on the ground, let alone the consequences of seasons and years with low renewables output. When they show a system that is robust on a 30 year timescale of real weather at hourly resolution then they will have started to look properly at what is needed.

When you speak to ops people in NG ESO they are worried about DSR because they’re not sure how they would manage a large chunk of load responding to the same price signal all at once. They’re very aware of the “be careful what you wish for” risk with V2G etc

DSR, V2G, price dependent usage and voluntary action are all in effect forms of control system without real time feedback. Some will be extremely complex and prone to faults, maloperation or sabotage. Victorian engineers knew the importance of feedback to stabilise systems. The now dominant market world view refers to whipcrack and tends to like unstable systems.

NGESO tell a superficial story (in their words a narrative not analysis) for a calm winter day in 2035 and fail to reach a satisfactory outcome. They mention the possibility of a calm week but are silent on the result – that narrative would scare the children. They state an emissions target (which is the surely the only reason for this “massive endeavour”) but are silent on whether they meet it – using their figures I calculate they hugely exceed it. I have a simple model that shows current plans to be both very expensive and guaranteed to fail, we need some complex modelling and a properly engineered plan not a fairy tale.

I fully agree with this. Unfortunately I see signs of ESO positioning itself rather than managing the realities of the system. This needs to be above politics, but increasingly it isn’t…

With respect to voltage reduction, I suspect that this is becoming progressively less and less effective as a demand reduction measure as more and more of the load sits behind various forms of electronic control.

This is another case where the old solutions need to be rethought, much like the low frequency demand disconnection scheme where, with the rise of embedded generation, it is worth checking that the load is actually a load and not a source of generation before automatically disconnecting it in the times of grid stress…

Excellent analysis. I conclude that NG are still trying to hide the system realities. To admit that wind is useless during Dunkelflaute is to admit that wind is useless and undermine the investment case in the Saudi Arabia of wind and all the attendant network expansion. Likewise interconnectors are big money earning assets for NG. The reality is that we have inadequate dispatchable capacity, and closure have made that worse.

If we go back to the Dunkelflaute that lasted over a week before last Christmas we find that day ahead prices ran to £1,500/MWh for a peak hour and that all available generation was cranked into action, alongside imports on every interconnnector. Since then we have seen more closures, and we face the possibility that interconnectors become a bidding war amid general European shortages. Adjusting for at least 5.6GW of interconnectors plus the lost capacity, it seems hard to see how cuts can be avoided. LCP did an analysis recently that estimated 10 hours LOLE over the winter.

The situation on the Continent remains dire. It seems highly likely that the NG view of French nuclear is wildly optimistic. Reading Die Welt I see than Germans are being warned to prepare for power cuts that last longer than 72 hours, while Ampion has stated they don’t expect to be able to meet demand for exports over the winter, aggravating French and other shortages. Generally, rotating power cuts are now widely expected on the Continent despite demand destruction through industrial closures.. Timera outlined their gas supply vulnerabilities.

https://timera-energy.com/european-gas-market-winter-outlook/

On gas supply, our risk is limited because of our regas capacity. So long as that is sufficient to meet demand with keeping storage topped up unless it is really needed there is a good chance that we can avoid having to rely on imports via Bacton, as we have more or less in recent winters. Of course, new LNG terminals in the Netherlands and Germany will increase competition for supply as they come on stream. Shipping has now become much more expensive, which puts a premium on being able to discharge a ship when it arrives.

https://timera-energy.com/lng-charter-rates-climb-sharply-into-winter/

For the UK gas supply perhaps the most important revelation from the Winter Outlook is this:

Norway’s maximum supply capability to GB is 141mcm/d, approximately 40mcm/d of this supply capability is price sensitive at maximum production

rates. GB market conditions need to be favourable to continental Europe for this additional 40mcm/d of supply capability to flow to GB.

There is a clear expectation that higher prices on the Continent will imply that Norway provides no winter flex to the UK. Yet throughout the summer we have been seeing extra volumes using the UK as a transit route – albeit those volumes fall within the lower priced term element. If Norway’s direct pipeline deliveries to the Continent are maxed out then the UK becomes the market they can reach, and more supply will flow if they can deliver. It may even be exported, but by going through the UK we fain supply security. A higher Continental price to justify export from the UK would mean extra earnings for Norway on flex volumes, so it might suit them.

The paid for power cuts via DSR are plainly going to rankle if rotating power cuts come without compensation. I think the plans are best described as work in progress, particularly as there is yet to be agreement in Europe on how they will handle shortages.

There are some interesting other dynamics here…

The EU is making noises about capping gas prices paid to Norway – that may well change the view on flex to GB. Norway is also offering LTC contracts which Germany is turning down in favour of LNG because it’s worried about having too much gas in future and wants diversion rights…I don’t think Germany is within 10 years of being long gas so should grab these Norwegian contracts. I’m hearing that British buyers are starting to bite. Overall I think there are reasons to believe that GB may turn out to be a better LT partner for Norway that the EU. And we’re not shutting down functioning nuclear power stations early which is going down very badly in Norway in the context of demands for Norwegian energy exports.

Overall I think our gas position is OK (absent an issue with infrastructure), supported by strong flows from the N Sea and lots of LNG. I’m pretty confident we can outbid enough other countries to get the LNG we need…particularly since the EU seems to want to use its “marker power” (which I think people like von der Leyen are over-estimating) to try to cap prices. This will make GB a more attractive LNG market as well.

In terms of electricity, while I think the risk of blackouts is higher than it’s been in decades, I still think we can use demand reduction to mitigate this risk. I strongly disapprove of this, and shedding industrial loads, which may very well be needed at times, is a terrible way of “meeting” demand. I would feel happier if the Government put in place some of the measures I’m suggesting around the Calon CCGTs (although time is running out for them to be open at all in the winter), allowing the use of diesel generation, and negotiating with Norway to secure imports when needed. Dual-fuelling CCGTs would help if we did have a gas shortage, so while I don’t think we will, I still think we should plan for it and put as many mitigations in place as wel can.

Excellent article as are the additional measures suggested.

I think politics is blocking sensible action, politicians mostly don’t see energy as a problem and the regulator who should be able to warn of the issues is prevented from doing so by the Energy Act 2010 which requires prioritising future harms from climate change.

While the Truss government has made some encouraging noises on energy this is plainly not enough given the precarious state of the government and the declared policies of opposition parties and large elements of the Conservative party.

As such what we could really do with is a new energy act that re-prioritises security and affordability above decarbonisation and makes the regulator responsible for delivering both, a bit like a central bank role but instead for energy, where the government sets targets that the regulator then has to try and meet. The targets should be for security in terms of firm indigenous capacity and gas in terms of domestic production and long term contracts, and; affordability in terms of retail costs as a proportion of average household income and commercial costs by some metric. The regulator could achieve these through market design, directives, impact modelling and official recommendations/warnings to government (perhaps analogous to the OBR’s role with budgets).

This would not prevent government from energy policy initiatives but would require them to properly consider costs and security.

The end goal would be to somewhat decouple energy from politics and return to rational markets and policies.

As a colleague pointed out to me today, the amount of domestic load reduction available through DFS, may be limited by the fact that the customers that are likely to be capable (e.g on Octopus Agile tariff) / interested in reducing demand during peak times, are probably ‘early adopters’ and are probably already doing so.

The Agile tariff isn’t very agile.

https://agileprices.co.uk/?fromdate=20220930

Mostly used by those with excess solar I believe as they get a more generous export price than elsewhere.

You seem to indicate Doel 3 in Belgium is about to shutdown, when it already has.

Also Tihange 2 is scheduled to shutdown end Jan 2023.

I attended the National Grid Winter Outlook webcast briefing yesterday. One of the things that struck me was the repeated assertion that we would still be able to import over the IC’s from France at our times of peak demand (I recall 6 PM to 9 PM was stated as the GB peak).

Meanwhile the French system operator seems to think they also have an evening peak demand that appears to partially overlap with the GB peak….

You suggest dual-fuelling CCGT’s. This is not a feasible solution for this winter. The changes required on large industrial GT’s are too large and complex to perform in a matter of weeks. The plant needs to be built with the capability and sadly very few of the CCGT’s in the UK / GB were built with liquid fuel capability. In part, as NOx emissions limits have dropped, it becomes harder to meet the limits when firing liquid fuels and there has also been assumption that there is no longer a requirement for diverse fuel options. As far as I know, the only CCGT’s built (both in the 1990’s) with liquid fuel capability were:

Keadby 1 (diesel / distillate)

Teeside (naptha) – long since demolished.

I don’t know if Keadby still has the distillate capability. It may have been lost when SSE upgraded the GT’s?

Agreed little or nothing would be possible this winter, but one of the issues exposed by the energy crisis is the lack of diversity in generator fuel, so I think this is something that should be investigated to determine what might be possible.

Also it seems to me we are now in a situation where firm capacity generation is insufficient to meet possible peak demand, and this will only get worse. So surely there need to be incentives to build new CCGT plant and an additional incentive to dual fuel would also seem worthwhile.

This week we’ve had good wind output with above 10GW continuous since Mon evening till this morning but the i/cs are flipping around daily between import and export. My expectation would be our system price would be lower with higher wind and incentivise more export but there doesn’t seem to be any correlation that would help inform what may happen as we progress through Autumn into Winter 23.

BEIS really is in a mess.

https://publications.parliament.uk/pa/cm5803/cmselect/cmbeis/761/report.html