Today National Grid ESO has published its early view of the Winter Outlook for 2022/23. Unbelievably, it believes the capacity margin will be slightly higher than last year at 4.0 GW compared with 3.9 GW. This strikes me as extreme wishful thinking which does no-one any favours.

“Our current assessment indicates that we expect system margins to be broadly in line with recent winters. It shows that we expect there to be sufficient available capacity to meet demand, with a de-rated margin of 4.0 GW, equivalent to 6.7%,”

– National Grid ESO

Looking at the detail (and unfortunately the data book has not been made available so far), it is clear that NG ESO expects to rely in interconnectors to meet peak winter demand which remains unchanged at 59.5 GW. I have no particular objection to demand being broadly flat, but I have a significant objection to the capacity margin improving when the past year has seen the loss of 2 GW of nuclear (Hunterston B and Hinkley Point B) and 2.1 GW of coal (1.6 GW of West Burton A and 500 MW at Ratcliffe).

NG ESO claims in its report that:

“Our Base Case assumes normal market conditions. this means that we assume there is no disruption to fuel supplies for thermal power stations and that electricity interconnectors between Great Britain and Europe continue to operate in response to market signals, including scarcity prices, as they have done in previous winters.

We assume that interconnectors are able to provide 5.7 GW net imports at times when GB needs it. This is consistent with their Capacity Market obligations. Our Base Case assumes 2.7 GW additional interconnector capacity that was not available last winter. This includes Eleclink which is now operational, and both IFA and NSL operating at full capacity.

There is uncertainty on the availability of the French nuclear fleet for winter. This could lead to more export flows from Great Britain to France when our system margins are not tight. We are continuing to monitor the outlook in France and will undertake further assessments ahead of the Winter Outlook Report in the autumn.”

Following a fire at Sellindge last year, the capacity on IFA-1 continues to be reduced. The latest REMIT disclosures indicate capacity will remain at 1 GW until 30 October when it will increase to 1.5 GW. There is currently no date given for a full return to service although there have been reports that it may not be until October 2023. NG ESO’s claim that it will be fully available therefore conflicts with the REMIT notices and needs to be challenged: asset operators are required to inform the market promptly of expected changes to their availability, and not to share these with third parties before informing the market.

This means that if we are guided by the publicly available information about IFA-1, the available interconnector capacity on a nameplate basis is 2.2 GW higher than last year for the majority of the winter (500 MW on IFA-1, 700 MW on NSL which was only operating at 50% capacity last winter, and 1,000 MW on Eleclink which was not operational last year), and not 2.7 GW. However, the behaviour of these interconnectors is likely to be markedly different.

“If you look at the forward prices, French winter prices are above GB winter prices. So I would be concerned that it’s not necessarily the case that we would be able to get what we need,”

– Thomas Edwards, senior modelling consultant, Cornwall Insight

It does not appear that NG ESO has adjusted the de-rating factors for the interconnectors despite obviously different market conditions.

France is now consistently importing from GB as a result of the problems with the nuclear fleet, and forward prices indicate that exports from Britain to France will continue this winter. Since France has more electric heating than Britain, its electricity demand increases faster when temperatures drop – it is likely that at times of high demand in Britain there will be higher demand in France. Assuming that the full import capacity will be available whenever Britain needs it seems extremely ambitious, and the reliability of interconnector provision under the Capacity Market has never been tested in practice – if it turns out not be possible to switch from export to import mode, then the payment of penalties will be of little comfort if blackouts result.

The situation in Norway is also a cause for concern. Statnett has declared the situation in south Norway (NO2) – the region from which the country exports – to be “pressed” with the reservoir filling rate at its lowest for the last 20 years with only 48.3% against the median rate for week 29 for 2002 to 2021 of 72.8%. East Norway (NO1) also has a historically low filling rate for week 29 of 66.6% versus a median of 79.8%. Reservoir levels are at their lowest since 1996 and there is growing talk of potential electricity rationing – Statnett has predicted a 5-20% chance of electricity rationing this winter, and has announced that Norway is likely to have a higher than normal reliance on imports this winter but that businesses should prepare for situations where “access to imports are lower than usual”.

Norway is unusual in that it has a “stock” of electricity in the form of its hydro reserves that are available for use. Interconnector flows are based on short-term price differentials, and do not account for the possibility that using this stock now means it may not be available later when needed. There are press reports that the government is considering its options to restrict exports.

“Restrictions on the export of electricity to Europe may be one of the measures that is needed,”

– Elisabeth Sæther, state secretary at the Ministry of Oil and Energy

This sounds drastic, but it would actually be in Europe and the UK’s best interest. Norway has electrified a significant portion of its offshore gas production infrastructure, and according to Equinor, can no longer revert to conventional fossil-fuel power. This means that if there are electricity shortages in the south of Norway, gas production including from the giant Troll field which supplies the UK, could be disrupted.

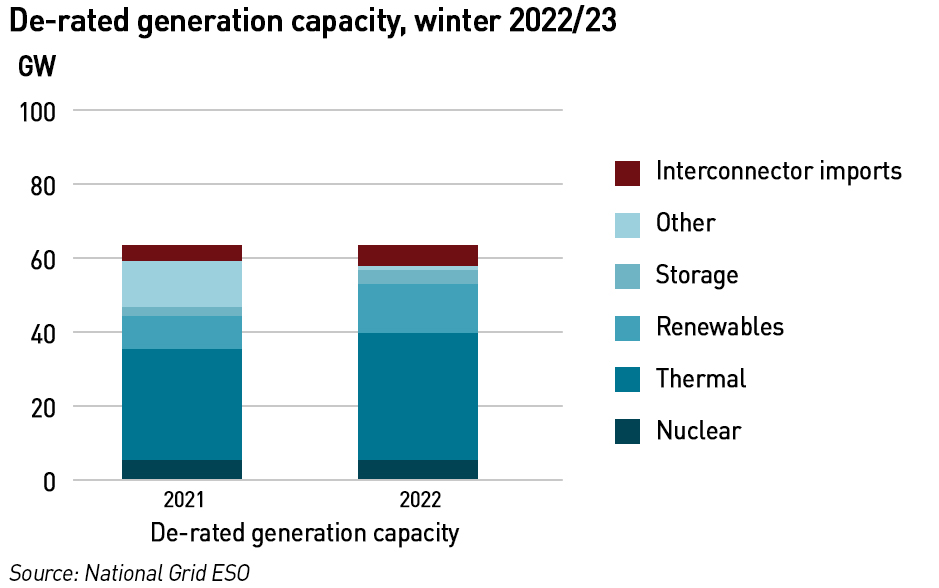

In addition to its (heroic) assumptions on interconnectors, we can see the following differences since last year’s outlook:

- Thermal generation has increased

- Renewable generation has increased significantly

- Storage has more than doubled

- “Other” has collapsed

Without the data book it is difficult to analyse these effects, particularly why the “other” category, which last year included demand-side response and embedded generation has fallen so much. One possible explanation is that thermal embedded generation has been re-categorised into the Thermal category (last year’s data book had a category called “Other embedded generation”, if this was primarily thermal that could account for some of the difference. The de-rated capacity of that category was 11.4 GW). The Thermal category does not include the standby deals done with EDF for West Burton A or Drax, so presumably the total excludes the full 3.4 GW capacity of these plants.

I have asked NG ESO if it can explain these differences more fully and will update this post if I receive any new information.

“National Grid is assuming that interconnectors behave by market rules. We believe this is a risky position to take. EnAppSys analysis suggests that the French Interconnectors (up to 4 GW) may be unreliable importers into GB in the winter. This is due to the problems with the nuclear fleet in France and the high price of gas on the continent due to the war in Ukraine and the well-documented issues with gas from Russia,”

– Phil Hewitt, director at EnApSyss

If National Grid has not adjusted its assumptions on import levels in light of the market changes described above, then it is seriously mis-leading the market as to the true picture this winter. It seems beyond wishful thinking to believe our winter capacity margin this year will be higher than last.

The Briefing Room: Can we keep the lights on this winter?

Soaring household bills have made energy the number one issue facing the government and consumers in Britain. But in addition to the cost, there may be another problem ahead as winter approaches. Experts are increasingly worried about the supply of both electricity and gas from Europe, and how that might affect the power system here.

So how worried should we be about energy shortages? And what can the government do to limit their impact?

Joining David Aaronovitch in The Briefing Room are:

- Kathryn Porter, Energy Analyst at Watt Logic

- Javier Blas, Energy Columnist at Bloomberg

- Elisabetta Cornago, Senior Research Fellow at the Centre for European Reform

- David Sheppard, Energy Editor at the Financial Times

- Michael Bradshaw, Professor of Global Energy at the University of Warwick.

So … National Grid is seemingly, and unsurprisngly, attempting to get a good price for handing over a serene ESO for nationalisation.

Kathryn,

similar thoughts to yourself in terms of NG ESO having high levels of wishful thinking.

Some other thoughts:

1) NG ESO are claiming they have secured 4 coal units for the winter. Presumably they are claiming 2 units at West Burton and 2 at Drax. However, as far as we know West Burton will only be able to run 1 of their 2 units. Even though not claiming this capacity as firm, NG ESO still seem unable to help themselves in putting at positive spin on this.

2) The outlook is claiming that there will be a slight increase in margin / capacity. Well potentially, this has only happened because the Secretary of State / BEIS increased (at the last minute) the capacity bought in the T-1 Capacity auction above NG ESO’s recommended value. Which suggests to me that NG ESO’s forward modelling of capacity requirements could do with some refinement.

3) NG ESO continue to blindly assume that there will be spare capacity in Belgium to provide imports via the NEMO link, despite 2 GW of nuclear closures in the next 6 months.

Belgium has deferred its nuclear closures until 2035, but that does not imply that they won’t have plant problems, as they have in the past already.

https://www.parisbeacon.com/63062/

The report claims that the secured coal capacity is 2GW on an equivalent firm basis.

I believe Belgium has only partially deferred its nuclear closures (the article you refer to, specifically references Doel 4 and Tihange 3). I understand, the following closures are still planned to take place; Doel 1 (445 MW, Feb 2025), Doel 2 (445 MW, Dec 2025), Doel 3 (1000 MW, Sep 2022), Tihange 1 (960 MW, Oct 2025) and Tihange 2 (1000 MW, Jan 2023).

NGSO will suffer severe reputational damage if this wishful thinking and group think continues. It is supposed to be neutral not a cheerleader for a particular lobby.

In NGSO’s recent superficial and deeply flawed report “A Day in the Life 2035” 20 GW of inter connectors are entirely at GB’s beck and call to attempt to deal with the feasts and famines.

The report is a future long term vision from a particular political and market theorists viewpoint. It is not a short term engineered plan for the next 12 years.

Does it work? The report is a vague and inconsistent “narrative” but does state that “success is uncertain”. It is silent on the outcome in terms of CO2 emissions – surely the sole aim of this “massive endeavour”.

I have done some modelling analysis that shows their suggested generation mix will be very expensive for the consumer and failure to reach net zero is guaranteed. They state a target of 10 – 20 gCO2/kWh but deliver 40 – 60 gCO2/kWh even with full inter connector usage. Demand is also not met on some winter days.

I have found that many other cost effective net zero options do exist – why is nobody trying to find them.

I’m increasingly cynical about NG ESO – it seems so desperate to not appear to be a barrier to net zero it has forgotten that the system still needs to actually work. We need fewer self-congratulatory reports about how “ready” they are for net zero and some reality checks for the Government about what all of this means in practice, particularly if aspects of the trilemma other than de-carbonisation are ignored…

Kathryn as I have posted before, I also have a cynical view towards NG ESO’s approach to interconnectors. It doesn’t seem right to me that one part of NG sets the capacity factor that has a direct bearing on the size of capacity payment that the interconnector companies (part owned by NG) receive.

NG ESO is supposed to be fully arm’s length from the rest of the Group to avoid conflicts of interest. Once the FSO model is operational, there will be a complete separation an the SO will be completely independent. I’m less worried about conflict of interest although I think announcing that IFA-1 will be fully available in contradition of the REMIT notices is somewhat dubious. I’m more concerned by the wider lack of transparency around this outlook, and the cheerleading approach mentioned above…

Kathryn in general I agree with you. I think the issue is more that in the corporate group think, interconnectors have become the solution to everything. The initial drive was probably due to the fact that interconnectors (along with LNG terminals) provided NG with an unregulated area of business they could invest in to increase profits. However that has morphed into solutions to address a lack of generating capacity and Black Start / grid restoration.

Much of what happens will be down to how Germany gets on with its FLNG terminals. The initial thoughts were that these would not be up and running until next year at the earliest but that will be too late. As far as I can make out the ships/terminals are available to take LNG but the connections to the German grid need to be built. Given the urgency you would have thought that everything would be done to get the job done. The local planning permissions have been given for one that I have seen, I would have thought the others would go through on the nod but I have seen nothing public. The European gas storage is generally looking as though it will be at 90% by the winter. It has been filling up nicely. But until now there has been some Russian gas. The UK has quietly been helping by sending electricity over and gas via Bacton. It does appear that LNG tankers are not arriving with quite the same frequency as they were during May and June.

Our own offshore wind power will have grown with the completion of Hornsea 2, whether SeaGreen is able to make a contribution is questionable but at least the jacket foundations are going in quickly at the moment. If half the turbines and cables are complete by November it is possible that 550 MW could be available from that source.

The problem is that if it isn’t windy then we will be very short, and the number of turbines will be irrelevant in this case. NG ESO seems to separate the peak demand from the low wind scenario but they may well coincide since low wind occurs during high pressure weather systems which deliver colder weather (and therefore boost heating demand) in winter.

Russian LNG is now starting to take the Arctic route to the Far East, as it did last summer and well into the autumn: I think they ended up with a vessel that had to be rescued from the ice in December. There has still been limited flow into Spain and Montoir in France in recent days, but the under the table shipments from Vysotsk to Zeebrugge appear to have ceased. Pipeline flows have been heavily chopped back. Stockbuilding will be slower from now on.

https://agsi.gie.eu/graphs/eu

The data book will only be available with the actual winter outlook published as usual in October, not this early preview.

That’s a shame. I don’t see why they can’t provide it now though…

by the sounds of it is because you’ve exposed it as being flawed!!

“Based on public announcements, we have assumed that

Baglan Bay, Severn Power and

Sutton Bridge CCGTs all remain unavailable. We assume all generating technologies

are de rated in line with the most recent Capacity Market de rating factors, with the

exception of nuclear and coal. We assume the availability of these technologies is

slightly lower, in line with their average availability over the last three winters.”

Technology Class ECR 2021 ECR 2022

Oil-fired steam generators 95.47% 95.18%

OCGT 95.47% 95.18%

Reciprocating engines 95.47% 95.18%

Nuclear 80.44% 78.25%

Hydro (excl. tidal / waves) 91.15% 91.13%

CCGT 90.92% 91.34%

CHP and autogen 90.92% 91.34%

Coal 80.11% 80.40%

Biomass 88.55% 87.99%

Energy from Waste 88.55% 87.99%

DSR 78.45% 71.45%

Technology Class ECR 2021 2022/23 ECR 2022 2023/24

Onshore Wind 7.81% 8.20%

Offshore Wind 11.33% 11.33%

Solar PV 2.15% 3.32%

So that looks like a further bunch of optimistic assumptions.

Having set the standard at around £10,000/MWh, are consumers really going to be prepared to pay for £57m per hour for imported power? This was last Christmas:

https://wattsupwiththat.com/wp-content/uploads/2022/07/12-Days-of-Christmas-interconnectors-1659024722.8591.png

I have complained about the nuclear availability assumptions before – the average of the past 3 years is really not appropriate for an end-of-life fleet. It feels like a lazy assumption.

For coal, since they are excluding West Burton and Drax from the thermal cataegory – or at least that was how I read the report – then the only one left is Ratcliffe. You can make the same end-of-life arguments there are well since the remaining 3 units are scheduled to close in October 2024.

This winter electricity is going to be very expensive. Relying on imports where we have to compete with buyers elsewhere for both gas and electricity will make us price takers and things can get very expensive.

On IFA1…. I presume you meant to write 1GW increasing to 1.5GW. I read this:

https://www.bmreports.com/bmrs/?q=remit/IFA202109152323G-ELXP-RMT-00000105/14/NGIFA

as implying an increase to 1.5GW on 30 October, and a return to 2GW as from 15 December (when the incident ends – see the outage profile), but with the caveat that there may be re-commissioning outages to be notified later. Perhaps not quite the normal way of signalling capacity at the end of an incident.

Haha, yes 1-1.5 GW not MW I’ll correct the typo.

Yes, I wasn’t sure what they were trying to signal with the dates since there is no clear sign of when the full capacity will return. The Outlook says the full capacity will be available for the entire winter which is clearly not what this says. The last update was in November, so I would have thought they would have some more information by now about the expected return profile…

At a national level Nordpool data shows that national reservoir capacity at a 3% less than last year although as you’ve highlighted NO2 is significantly adrift and the fill season is pretty much done. Other areas are not far off normal trend but NO2 had poor fill last year although I wonder if in part that coincided with firstly the German i/c 1.4GW going live in Q1/21 then our link NSL live in Q4/22 causing more drawdowns. There is also a Denmark i/c (1.7GW although isn’t fully exploited) also connected into NO2 grid area. Im also surprised Norwegians aren’t complaining how the power price is so much higher in NO2 than the rest of the country not sure whether that’s related to interconnectors or not.

I wonder how much coordination there is between all ESO’s if there trying to second guess each other or not? Surely NG can see that France won’t have all its reactors back on line by 1st Oct and even in the height of summer the daily price in France generally sits 15-20% higher than its neighbours. Certainly going to be interesting if any country is going to lets its own people suffer because they can get more money by exporting what they produce.

Presumably they’ve told Drax/West Burton to stock up on coal on a just in case basis? How much can they get there hands on given the notice everyone else is after non Russian coal. Also got to get transported to the power stations so hopefully rail has cut up all the wagons that were no longer needed!

I just wonder how elastic demand might be. Given that domestic consumer price is likely to be well above 40p a kWh and business use higher still we might just see voluntary reduction in demand. I am hearing anecdotally that businesses are demanding savings of electricity of their staff, consolidating workers to fill space on floors to close others and air conditioning being set at higher temperatures for cooling and lower temperatures for heating. How much reduction in demand will be enough to for NG to squeeze through the winter?