The USA has often been seen as at the forefront of the energy transition (or at least some states such as California have), although progress has been relatively slow – the first half of 2023 was the first time that wind and solar power provided more electricity than coal in the US. The Inflation Reduction Act (“IRA”) is designed to change this and is sucking up as much inward investment as possible for the development of the necessary infrastructure. Companies like Siemens Energy Are looking to build new production facilities in the US and scaling back ambitions elsewhere.

The US battery production capacity pipeline has experienced growth rates higher than Europe and even China, with businesses such as Volkswagen and Northvolt putting European plans on hold this year to pursue US alternatives. Asian companies including Panasonic, Toyota, Honda and LG Energy Solutions all announced billion dollar US investment plans since the IRA. Current estimates show that the Inflation Reduction Act is on track to encourage US$ 2.9 trillion in renewable energy investments by 2050.

Of course, while the US is celebrating, the rest of the world is suffering as capital flows outwards towards the US. Amitabh Kant, the Indian official responsible for leading this year’s G20 summit in India, described the IRA as “the most protectionist act ever drafted in the world” and said it was already harming the nascent Indian hydrogen industry. Despite the huge impact the IRA has had on green investment in the US, no region has responded with a similar scale of incentives.

Europe has introduced a piecemeal “temporary crisis and transition framework” (“TCTF”), which is part of the EU Green Deal Industrial Plan. This allows EU countries to provide faster state aid to companies manufacturing technologies required for the energy transition such as solar panels, wind turbines, heat pumps, electrolysers for hydrogen production and carbon capture and storage technology. While the TCTF has helped to stem of the flow pf capital to the US, this has been marginal as businesses prefer the simplicity of the US legislation compared with the complex processes for accessing multiple EU funding sources.

Canada introduced IRA-inspired tax credits to spark production of minerals and EV components, Germany is trying to stimulate battery cell production, hydrogen and chip manufacturing, while France is introducing tax credits for wind and solar power, and manufacture of heat pumps and batteries under the EU’s more flexible state aid rules. However little attention is being paid to developing nations – only 2% of global renewable energy investments as year were made in Africa, while the continent continued to attract investments in oil and gas projects, including from American and European multinationals.

Impact of the Inflation Reduction Act is significant….

In the first six months after the IRA was passed, more than 100,000 clean energy jobs were created in the US as a result of almost US$ 90 billion invested. According to the American Clean Power Association, a year after coming in to law, the Act had stimulated over US$ 270 billion of investment to develop utility-scale wind, solar, and storage projects, manufacturing facilities, supply chains in North America and 83 new or expanded clean energy manufacturing facilities, potentially creating 76 GW of manufacturing capacity. Two thirds of these for solar manufacturing. These figures exceed the total spend on clean energy in the 7 years prior to the introduction of the IRA.

185 GW of clean power projects have been announced during the first 50 weeks of the Act – equal to almost 80% of current clean power capacity in the US. The Department of Energy’s Loan Program Office has been reviewing more than 140 clean energy financing and guarantee requests totalling approximately US$ 121 billion. Solar PV capacity increased 47% in the first quarter of 2023, making up more than half of all new grid capacity, while new manufacturing investments could increase capacity from 9 GW to 60 GW by 2026.

There have also been announcements relating to hydrogen with 6.5 mtpa of low-carbon hydrogen (blue hydrogen with CCS) capacity and 2.4 mtpa of green hydrogen announced as of January 2023 to be delivered by 2030. This represents a 30% increase in blue hydrogen and a 350% increase in green hydrogen compared with the projects that had been announced prior to May 2022. To put it into perspective, the combined total of these new projects is equivalent to the existing 10 mtpa of mostly grey hydrogen production capacity in the US.

The IRA provided further incentives to the already well-incentivised carbon capture sector in the US. The DoE has also awarded US$ 23.4 billion to 16 projects in 14 states with locally tailored technical assistance to develop CCS technologies. The DoE has also recently announced that two direct air capture projects in Texas and Louisiana would receive up to US$ 1.2 billion in support. As an aside, with this level of support, and given the long and difficult road to developing a commercially viable CCS solution, I recommend the UK Government stays clear of this sector. The UK cannot hope to match this degree of support, and many billions have been spent to get to the current, rather unsatisfactory, state of play.

In transport, the IRA had attracted US$ 72 billion in private-sector investment announcements into the electric car industry by the end of July, covering EV manufacturing, battery manufacturing, recycling, and raw minerals. IRA tax incentives are cutting the cost of EVs by US$ 7,500, prompting a 66% increase in the sales of new electric vehicles in the first quarter of 2023, one million cars expected to be sold by the end of the year. However, prices are still comparatively high, providing a deterrent for many consumers. Policy-makers hope that supply chain investments incentivised by IRA tax credits will reduce production costs by as much as US$ 9,000 per vehicle, further lowering list prices. The Infrastructure Investment and Jobs Act has allocated US$ 7.5 billion for 500,000 EV charging stations nationwide.

The IRA also includes a US$ 1.25-1.75 per gallon tax credit for bioSAF which is stimulating the supply of sustainable aviation fuel, and is expected to deliver increased production capacity over the coming years.

…but it is still not enough to de-carbonise the power sector, never mind the wider economy

Despite the massive investments arising from the IRA, the Act does nothing to address other bottlenecks standing in the way of net zero, in particular the problem of electricity grid constraints. As in Britain, there are long connection delays, and problems with congestion. The number of connection requests has increased sixfold on an annual basis since 2012, and the processes tend to be complex, although some network operators (and the FERC – the Federal Energy Regulatory Commission) have introduced reforms to streamline matters. Between 2000 and 2016, 72% of connection requests were withdrawn by the applicant, while waiting times for connections have grown by 19 months in the past decade to an average of 3.7 years. Just 23% of new projects progress through the queue to connection.

As in Britain, the main reason for connection delays is lack of network capacity. The problem is made worse by the fact that some developers submit multiple connection requests for projects in different areas in the hope one makes it through. Again, like Britain, the country is exploring whether it can move from a “first come, first served” approach to connections, to prioritising those who are ready first.

“We have a lot of power demand and a lot of power generation coming on and the grid in between that supply and demand is not keeping up. You have hundreds of different project developers trying to use whatever capacity there is and they apply for interconnection from the utility—and usually there is a lot more of those applications than either the grid capacity can handle, or the utility can process,”

– Rob Gramlich, founder of consultancy Grid Strategies

Aging infrastructure is also a problem. In 2021, the most recent year for which data are available, US electricity customers were without power for slightly longer than seven hours on average, according to data from the US Energy Information Administration (“EIA”), a significant increase on the three-to-four hour average for outages between 2013 and 2016. More than five of those seven hours were during what the EIA calls “major events,” including snowstorms, hurricanes, and wildfires.

According the Brattle Group, transmission infrastructure lasts between 50 and 80 years – replacing aging infrastructure is likely to cost an estimated US$ 10 billion a year. Transmission projects require at least 5–10 years to plan, develop, and construct. American Electric Power, a network company that owns 40,000 miles of transmission lines, has said 30% of its infrastructure will need replacing over the next 10 years. In addition to increasing age, the location of the existing transmission lines also presents challenges, since they do not run to/ from locations where renewable generation is being built.

Consultancy Marsh & McLennan estimates that more than 140,000 miles of US transmission lines will need to be replaced by 2050, at a possible cost of US$ 700 billion. A Princeton University study in 2021 suggested that for the US to reach its net zero goals, it would need to triple its transmission capacity – together with network upgrades, investment in excess of US$ 1 trillion may be needed. Princeton University estimated the costs could reach US$ 2.4 trillion by 2050.

Part of the problem relates to the way in which transmission needs are assessed, which tends to be on a project-by-project basis in isolation. This worked well in the days of large, centralised sources of generation, but is less suitable in a more distributed, de-centralised world, where the process ignores the impact of multiple projects requiring connection, and often fails to optimise solutions as a result. Transmission planning often is overly focused on addressing reliability and local need, and the lack of inter-state interconnection encourages grids to be treated in isolation rather than as part of a wider system. This is analogous to Wales and Scotland planning infrastructure independently to England.

Brattle also says that most transmission planning fails to adequately account for short and long-term risks affecting power markets. Planners typically only evaluate projects under “normal” system conditions, ignoring the potentially high cost of short-term challenges triggered by high-impact-low-probability events due to weather, transmission outages, fuel supply disruption, or unexpected load changes associated with economic booms or busts. Planners also fail to consider the full range of long-term scenarios for example the extent to which a less robust or flexible transmission system will affect costs under different scenarios of market fundamentals.

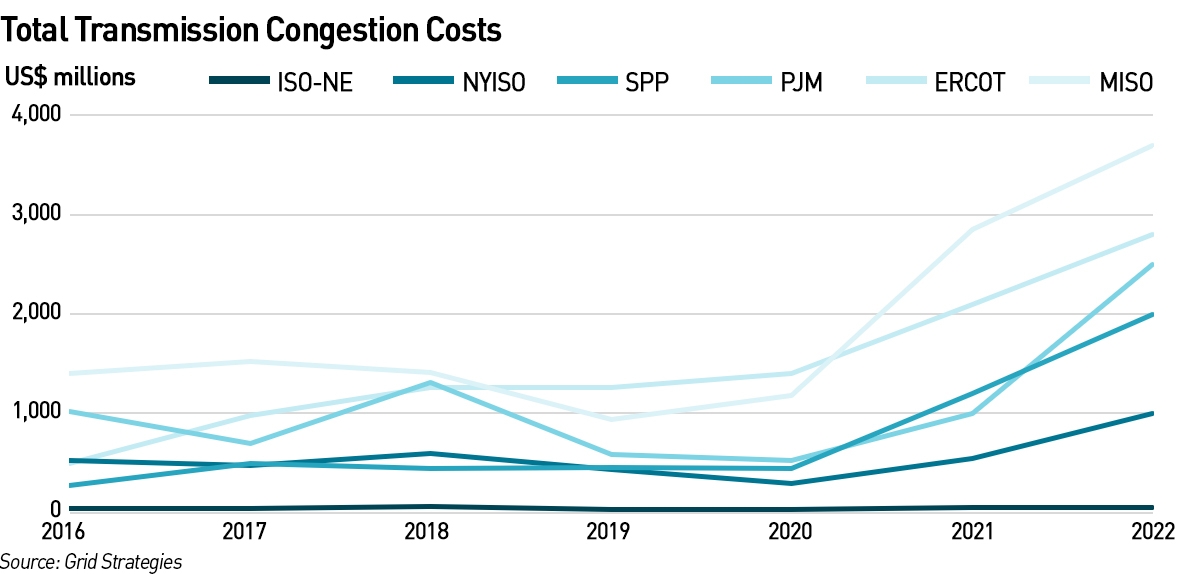

According to a study by Grid Strategies, costs to consumers from congestion on the US power grid increased dramatically last year, rising from US$ 13.3 billion in 2021 to an estimated US$ 20.8 billion in 2022, driven partly by fuel price volatility. These costs don’t include congestion between grid operators. MISO had the highest congestion costs in 2022, followed by ERCOT. ISO-NE consistently has the lowest costs.

Another problem is the country’s federal structure is reflected in its electricity networks. While the FERC regulates power prices, and the NERC (North American Electric Reliability Corporation) enforces certain reliability standards, neither has control over nation-wide grid planning, nor does anyone else. Responsibility for grid maintenance, upgrades and inter-regional connections is shared among state and local regulators, utility companies and the seven grid operators. The operators themselves have little power over modernisation since they are simply associations whose members are largely utilities and local regulators.

For example, there is an ongoing battle over how transmission upgrades by the Midcontinent Independent System Operator (“MISO”) should be paid for – MISO oversees transmission infrastructure for utilities in 15 US states and the Canadian province of Manitoba. These disputes have blocked progress on regional projects. The Public Service Commission in Louisiana, which is in the MISO region, has objected to paying for new transmission lines to renewable generation in the northern part of the region, on the basis that these projects don’t benefit the state, and there is limited transmission capacity connecting the northern and southern parts of the MISO region.

Elsewhere, the Electric Reliability Council of Texas (“ERCOT”) has avoided building interconnectors with other states in part to avoid coming under the FERC’s jurisdiction which only applies at the federal rather than state level.

.

The Inflation Reduction Act has been very successful in attracting investment to the US. The buildout of renewable generation, electric cars and other transition hardware will be built in the US. But it won’t be enough – net zero might come closer, but it might not – as I will describe in the next post, reliability concerns as well as lack of transmission infrastructure may be a drag on climate goals.

UPDATE

In my latest article in the Telegraph, I cover the topics raised in this blog post. Without significant investments in network infrastructure and reform of the grid planning and connections processes, the eye-watering sums being spent on the Inflation Reduction Act will fail to deliver the desired progress towards net zero in the US.

Hello,

Full of facts and infromation – but as I have been asking those people in Auto sector – aviation sector – housing sector for some years – how did the view an all electric economy — UK – when there was not sufficient Grid capacity to ensure there is not black outs in winter — would suggest majority of houses use Natural Methane Gas – others Oil both have to become Zero emssions – cars are not such a problem in this issue however day Trucks and and Heavy Goods are a major issue – each equal to between 6 and 8 cars – problem at the end of each working day 10 or 12 trucks at one logistics yard will need their own substation — 800,000 trucks – = 4.2 million cars equivalent each night

In 2017 I posted on Linked In that Auto Makers needed an easy to mass produce Hydrogen engine – as a generator – since the electric power train is much better than a mechanical transmission- with 1.5 billion fossil ICe vehicles to be changed by 2050 – Net Zero target from 2025 = 60,000,000 new or retrfit Zero emissions EVs each year we have people who simply have not really thought thorugh the issues stating the BEVs can hit the numbers – Musk on Tesla — we will manufacture 20,000,000 units by 2030 – all the others have no idea what ??? even then where are all the rare earths coming from-

Not to forget all electric will require major numbers of grid sized batteries for such as every motorway services areas and substation for a small town – –

Sorry to say not one Auto-maker or engine maker in UK or in the EU have replied – aviation sector – no interest – Where do these CEOs – Tech Officers and managers think breakthroughs come from – need to Google famous inventors – I doubt if any large company or corporation will figure.

21st century – should we be continuing with the same systems which had to be developed for Fossil Fuel production and distribution -centralised electricity generation.

HyPulJet Integrated Hydrogen Power Unit – if developed successfully – will allow house builders to cut out the cost of Grid connection and homeowners will own their own generation for house and same with their car –this will be a major change in how things happen – homeowner will have nore to spend in local economy – Local taxes since Governments have proved that they can enact policy which chooses one place over another – where their voters are.

Wont be seeing £GB billions going to overseas owners in dividends

Independent energy generation – the incentive for people to decarbonise

HyPulJet Ltd will be Crowd Funding – we cannot enter funding competitions as the criteria – does not allow outside the Box True Innovation.

Hydrogen can be produced literally anywhere — small volume in my lounge – for the Toy Hydrogen fuel cell car my son bought me as Christmas present 2012 – since 2012 I have had a clear vision – if Hydrogen is the future then it has to be produced where it is used – I have been clear that needs to be onboard the EV –in the garage /on the balcony /wall hung for Zero emissions Grid Free housee

The HyPulJet website seems to describe just another hydrogen burning engine. It is still necessary to make the hydrogen fuel. Does the comment suggest making the hydrogen in a home electrolyser powered by roof top solar ? There would need to be some inovation for the electrolyser and storage of compressed hydrogen (350 bar or 700 bar) on the vehicle..

So can I just check a few things?. How much has each ‘green’ job cost? How much do the big US Automakers lose per EV car produced and how much non-moving inventory do they have? How often does California ask people not to run AC or charge their EVs? What is the efficiency of H2 gas generation (and where does the energy come from)? Ditto CCS? How much spare money for food and clothes does a typical American household have nowadays and when will the (misnamed IRA) be able to taper the subsidies it is spewing forth? How much will THAT taper put up energy prices? How much is housing now (rental or mortgage). I don’t think the IRA has helped any Americans except the same troughers that suck up all the money this side of the pond. It’s just not a cottage industry over there.

I talk about the blackout risks in my next post (https://watt-logic.com/2023/09/07/closing-fossil-fuel-power-stations-risks-shortfalls/) – premature closure of conventional generation is already causing problems but now the EPA has decided that because of the IRA tax credits for hydrogen and CCS it can press ahead with strict emissions rules which would force more coal and gas plant to close. Grid operators are up in arms – they actually said, as I use in my title. “Hope is not an acceptable strategy”. Very well said!

I also mention rising household electricity prices. Policy costs will add to this, either though higher bills or higher taxes. Either way, Americans will have to pay for all of this. And despite all of that cost, the IRA isn’t going to deliver what Biden et al want either in terms of net zero or inflation reduction (it will probably increase inflation if it makes energy more expensive).

Nice article, thank you.

Did anyone trouble to check whether the programme is feasible? It will collapse whit it proves not to be the case. The damage it will do to the US economy in the mean time should ensure that it struggles to regain competitiveness for decades afterwards. The European and UK economies look set for an even worse fate. Since our civil service masters have decided (Energy Bill [Lords]) that the only way to enforce net zero is via imprisonment and massive fines, and our politicians have rolled over in agreement we seem to be headed for some dark times, both metaphorically and actually.

We need politicians who will not just break the mould, but break the straitjacket of insanity that we are being tied into.

Indeed, lack of impact assessments (or inadequate ones) is a common theme. In my next post I talk about the EPA’s new Rule 111 where there hasn’t been an IA to check that closing all those coal and gas power stations won’t lead to more blackouts, but who cares, if there are blackouts then emissions will fall…

“Since our civil service masters have decided that the only way to enforce net zero is via imprisonment…”

Care to explain?

An interesting article, thank you. But one thing puzzles me: Where are the Americans getting all this money for investment in renewables ? Are they increasing the risk of their bankrupcy (defaulting on their debts) or have they discovered the Magic Money Tree ?

If I discovered a Magic Money Tree I’d probably keep it secret, so I guess we’ll only know when they start printing money to pay their debts!