In addition to the electricity winter outlook, National Grid’s gas operations division recently published its outlook for the gas market this winter. Despite the wider crisis in the gas markets, which is driving gas prices higher globally, including in the UK, the security of the UK’s gas supplies is significantly more comfortable than for electricity.

“We anticipate LNG to act as the primary source of supply flexibility this winter, supplementing UKCS and Norwegian supplies, with imports from continental Europe only occurring during periods of elevated demand,”

– National Grid

National Grid expects total GB gas demand to be higher this winter than last, with reductions in demand from households and businesses due to high prices being more than offset by increased use of gas for electricity generation in the face of reduced electricity imports and indeed electricity exports to France.

GB outlook for winter 2022/23

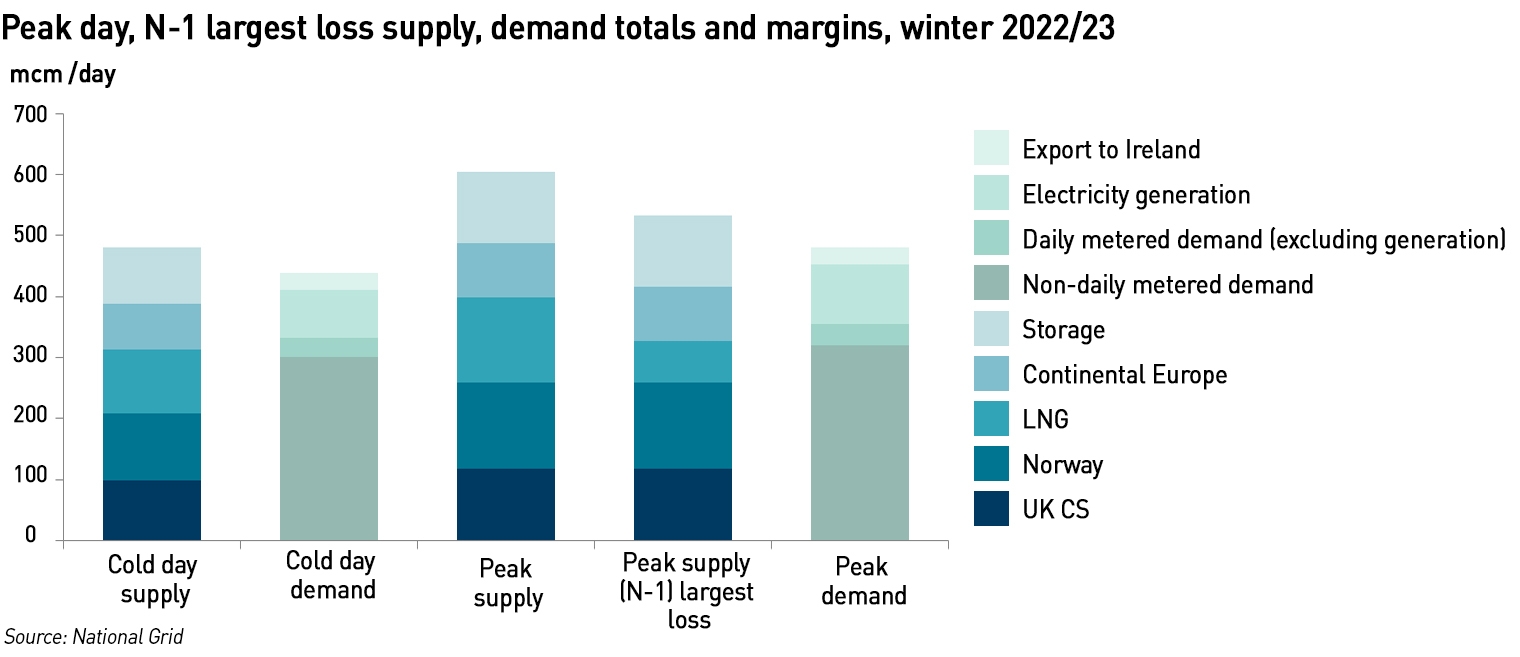

Although total winter gas demand is expected to be higher this winter than last, National Grid’s expectation of 1-in-20 peak demand has fallen by 22 mcm/d to 483 mcm/d from 505 mcm /d last winter. Peak supply is at a similar level to last year at 609 mcm /d compared with 605 mcm /d, although National Grid now expects LNG to form a higher proportion of imported supply given the impact of lower Russian gas on Continental Europe and resultant lower imports over the interconnectors.

The margin between forecast peak supply and 1-in-20 peak demand for winter 2022 23 is 122 mcm/d compared to a margin of 104 mcm/d last winter. Under N-1 conditions (an event resulting in the loss of the single largest piece of NTS infrastructure) the supply margin at peak 1-in-20 demand has increased from 32 mcm /d last winter to 50 mcm/d now.

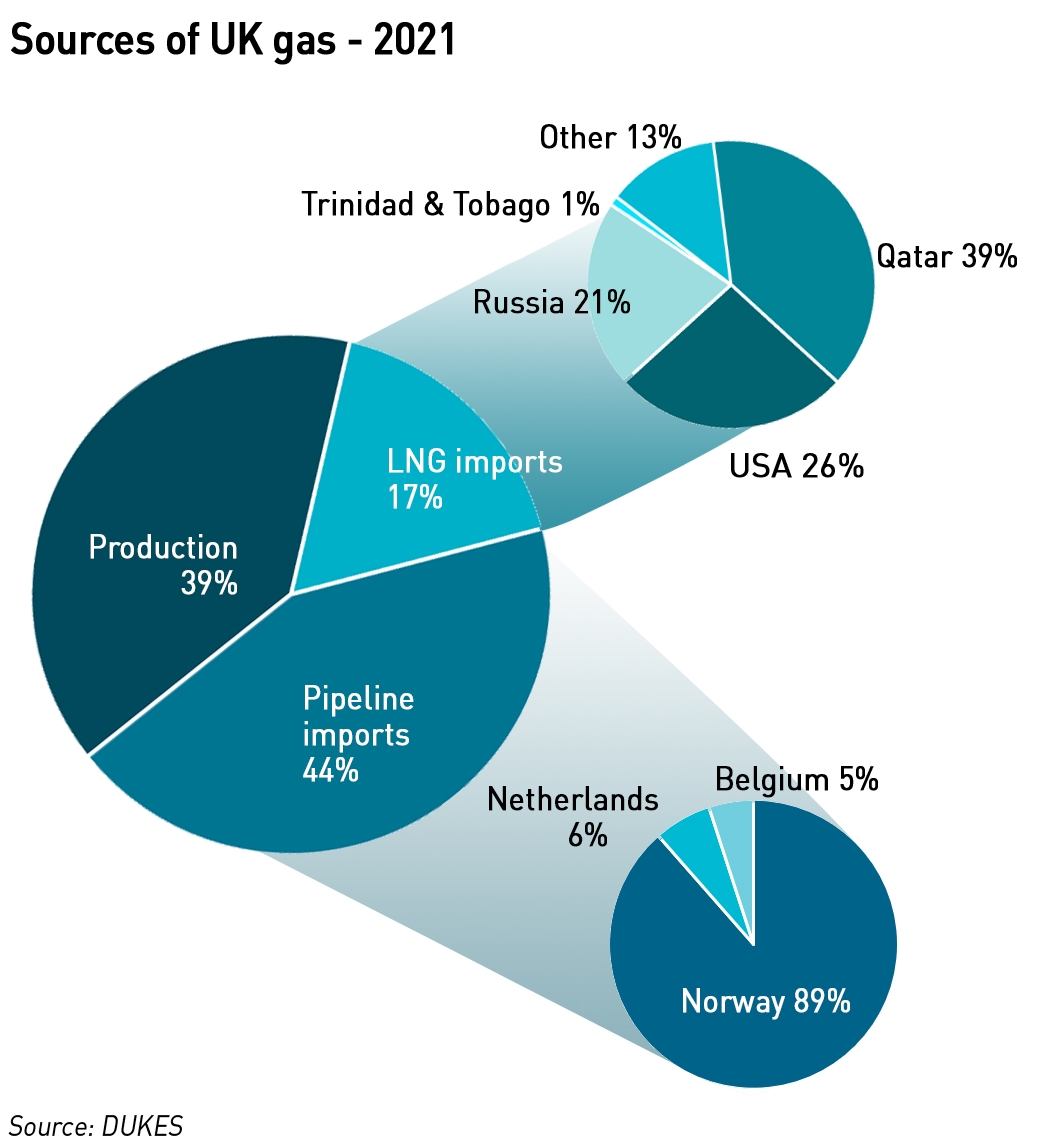

Great Britain produces just under half of the gas it consumes (39% in 2021 and 48% in 2020), and imports a significant amount from Norway, which means that around 80% of the gas consumed in GB is produced in the North Sea, with most of the balance being imported in the form of LNG primarily from the USA and Qatar.

Official UK Statistics (DUKES) are only published in July for the previous year, so these figures pre-date the war in Ukraine. In the first half of 2022, domestic production increased by 26%, and Britain no longer buys any gas at all from Russia which previously represented around 4% of the GB gas mix. The USA has been the largest supplier of LNG to GB in 2022 at 7.1 bcm in the first eight months of the year (compared with 3.9 bcm in the whole of 2021), followed by Qatar at 4.6 bcm. An additional 1 bcm has been contracted from Norway.

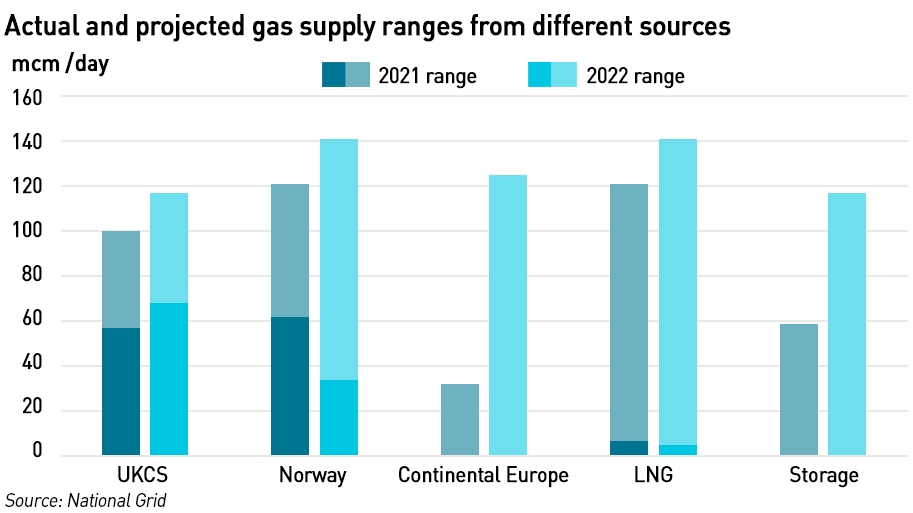

According to National Grid, the peak daily LNG send-out possible remains at 141 mcm/day this winter. Analysis by Mike Fulwood, Senior Research Fellow at the Oxford Institute for Energy Studies, cited in the outlook, suggests that the high volumes of flexible LNG coming into the EU and GB so far in 2022 is likely to continue, even in a cold winter, in the absence of a dramatic rebound in Asian demand.

Britain is particularly well positioned, with more than enough spare LNG capacity, compared to north west Europe whose terminals are running at very high utilisation levels. Analysis by Baringa indicates there are enough uncommitted cargoes available to meet GB demand providing prices are high enough to attract them.

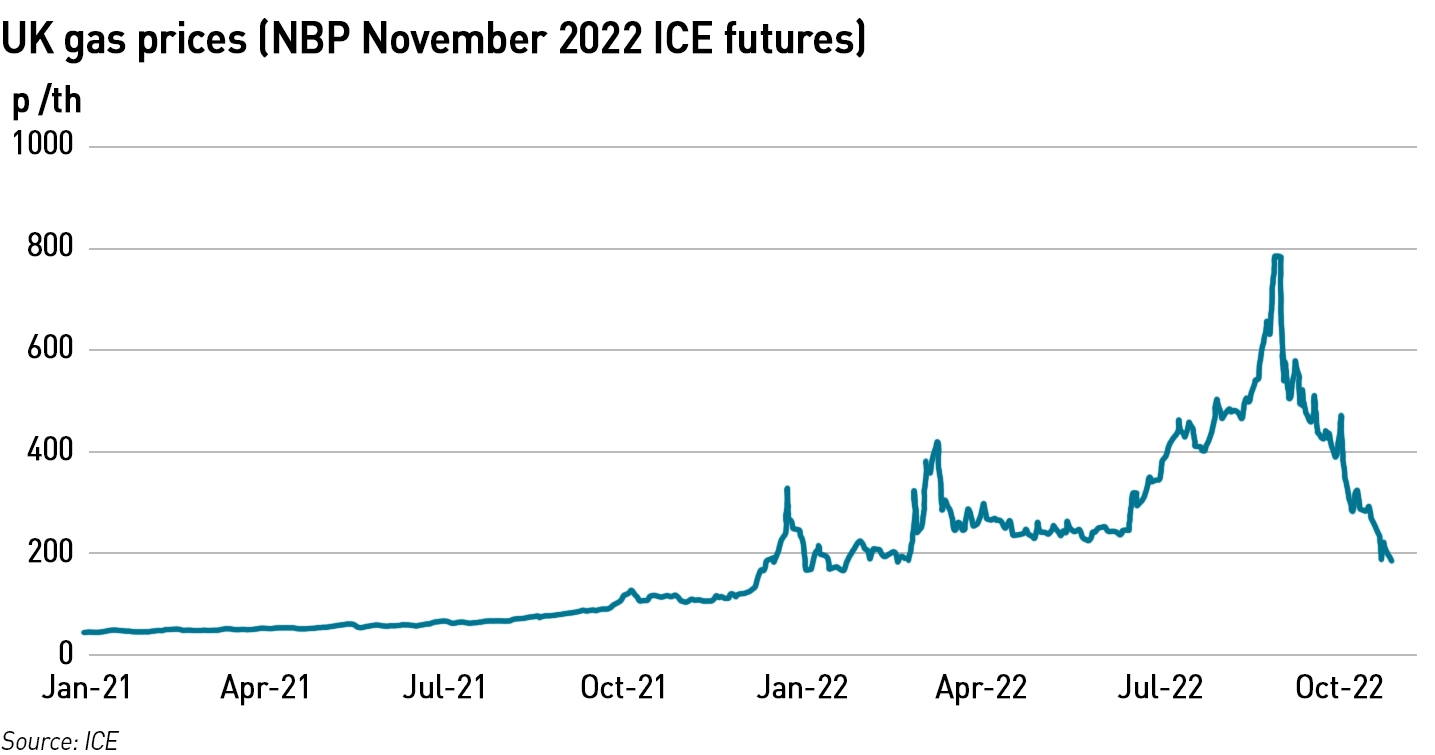

Gas prices in Britain have risen significantly in common with other European markets. The front month ICE NBP contract is trading 2.85 times higher than a year ago, however, this is significantly down from the highs of late August when prices were 8 times higher than a year ago.

High gas prices have had a knock-on impact on prices of electricity and concerns over rapidly rising fuel poverty and inflation led the UK Government to implement new price controls on both gas and electricity. Unlike other European markets, these controls have been implemented only at the retail level through subsidy schemes aimed at both businesses and households. Households and businesses will see their prices capped for the six months of the current winter, with further support (yet to be announced) being developed for households and industries seen as particularly vulnerable to high energy prices.

Gas prices have fallen steadily from their late August highs

Gas prices continue to be highly volatile, but have fallen significantly since late August when Nord Stream closed. This is for a mixture of reasons – some of the price increases had not been a reflection of fundamentals either in the UK or in Europe, and there is some optimisim due to a mild start to the winter. By late August Nord Stream flows had dwindled in any case, and gas inventories had built faster than expected, so there was no reason to fear deep shortages this winter. Since the UK no longer buys gas from Russia, and pipeline flows from the Continent are less than 4% of UK gas supplies, the price increases were not justified and were soon reversed. Lower winter gas prices reflect a market expectation that both the UK and the EU will have enough gas for the winter.

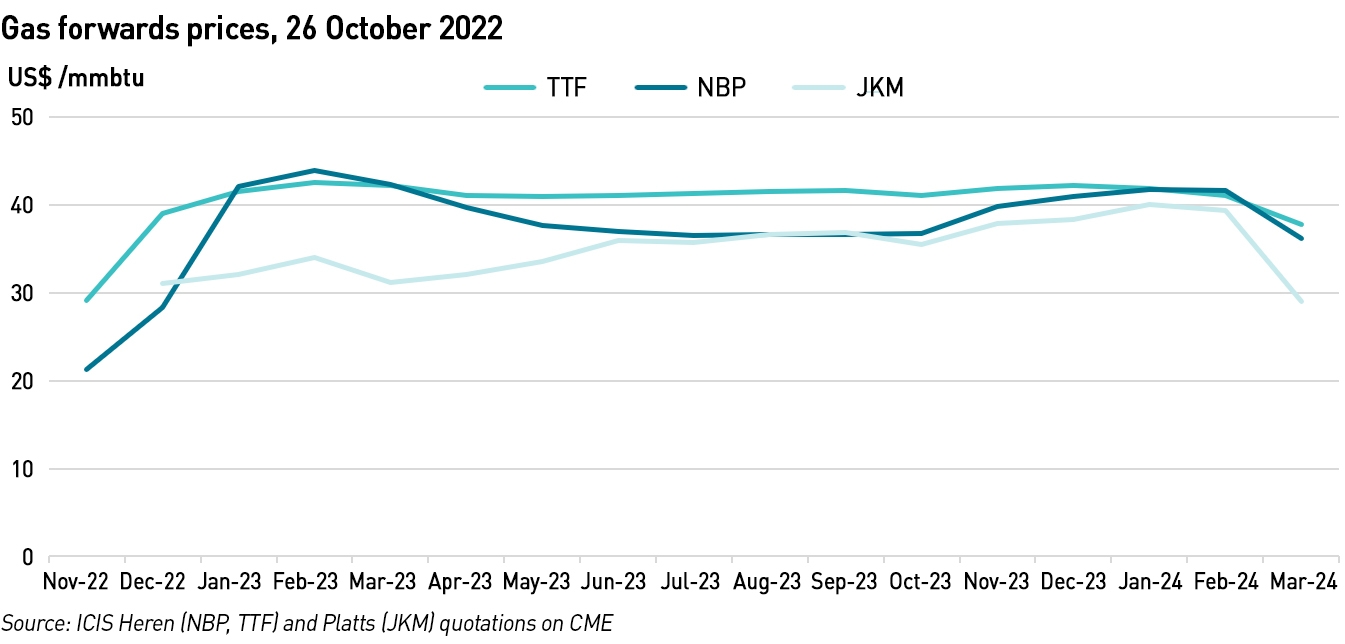

The price divergence between NBP and TTF which took hold back in April continued to widen although in the last couple of weeks it appears to be narrowing. NBP and TTF usually trade within a tight range, but the spread between them grew to more than €60 /MWh, with TTF also diverging from Spanish and French prices. The main reason for this is access to LNG – France, Spain and the UK all have significantly more LNG regasification capacity than the Netherlands.

Interestingly, now that the contracts have rolled to December, this divergence is much less apparent, and in the past month the spread between TTF and the French gas price (PEG) has narrowed from €31 /MWh to €12 /MWh.

Storage dynamics will drive the markets going into next winter

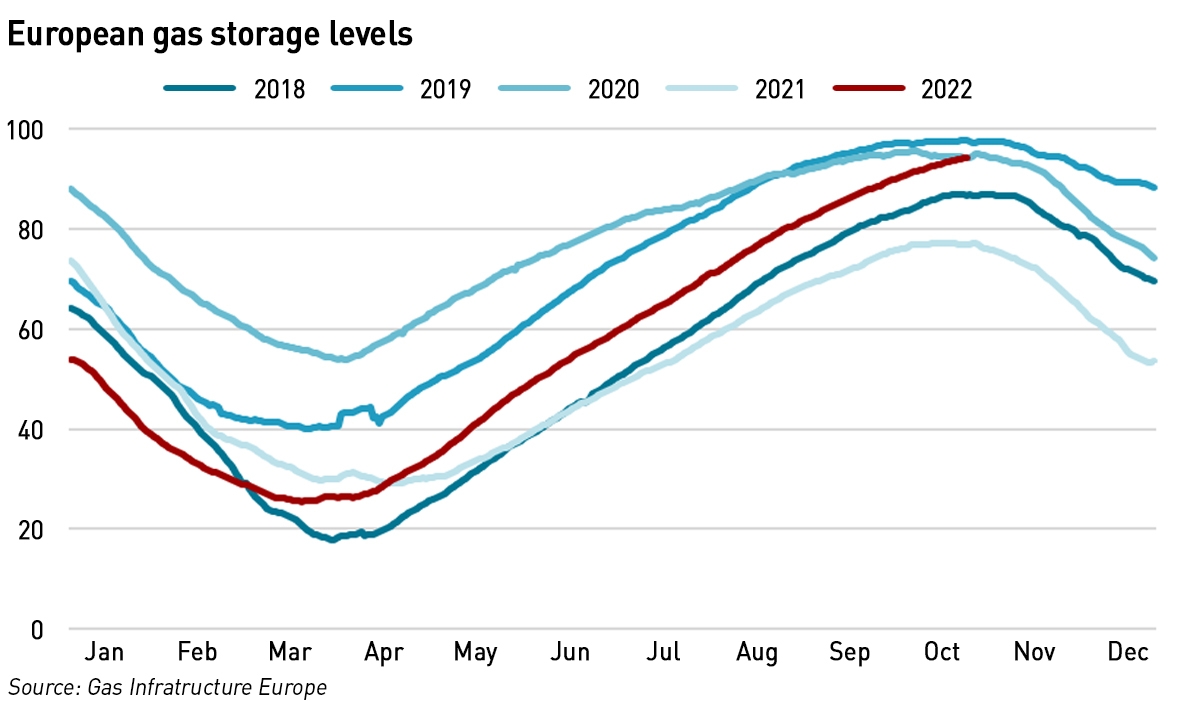

In response to the war in Ukraine, the European Commission outlined its intention to require underground gas storage across the EU to be filled to at least 90% of capacity by 1 October each year. To put this target in context, in only two of the past six years have inventory levels exceeded 90% (although in one year they were only very slightly under) at the beginning of winter.

At the start of this year’s injection season on 1 April, EU gas storage facilities were 26.4% full, which is at the lower end of what is normal for the time of year, but a mild winter and an influx of LNG helped levels to recover.

Market prices jumped on the news of the storage mandate, forcing the Commission to modify its proposal for this year to a target of 80% full by 1 November, rising to 90% in future years. In fact, storage levels are now almost 95% full having recovered significantly over the summer despite the pressure of the heatwave.

Much of what happens next depends on two things: the first is normal: the weather, and the second is the situation in Ukraine. If the winter is unusually cold, gas demand will be higher, driving prices up.

It is also unclear how gas will flow between Britain and the EU – the forward curve just about indicates that the usual winter flows to GB will be seen this year, but these price differentials could easily reverse. Looking further forward we see spreads between the UK and Asian markets narrow particularly in the summer, when GB demand falls due to warmer weather and low storage capacity, which will have implications for LNG diversions. The NBP/TTF spread should also narrow as 20 bcm of new LNG regas facilities are connected up in north-west Europe.

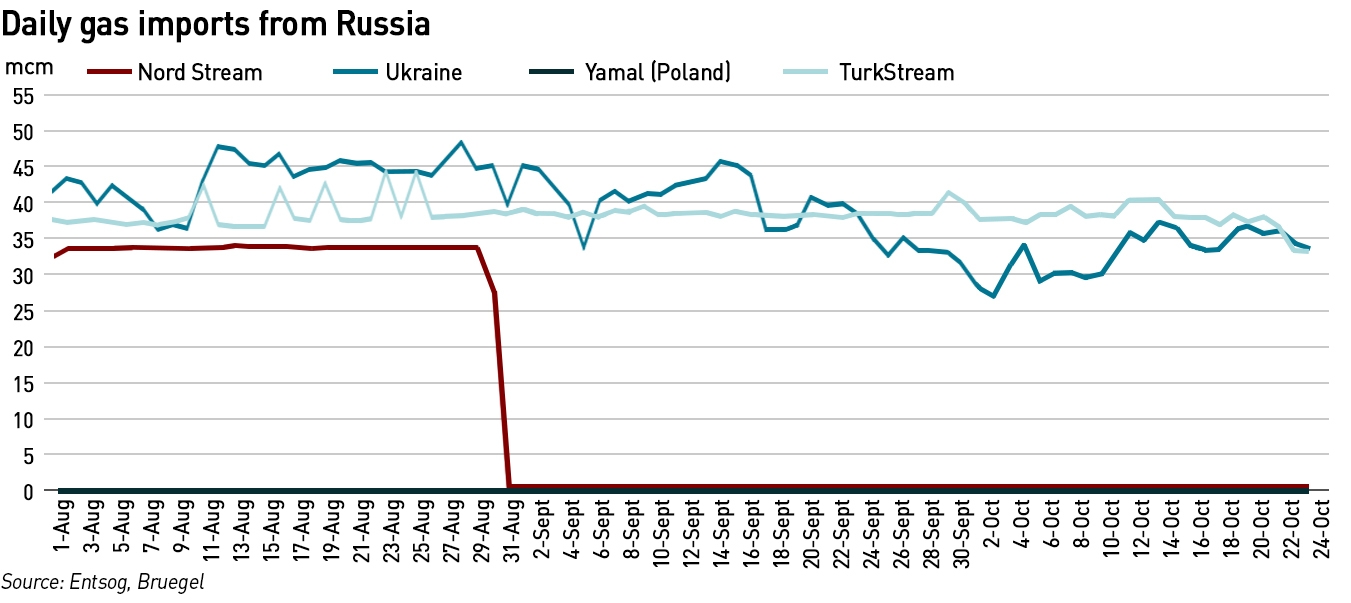

The impact of the war in Ukraine is impossible to predict. The market has adjusted to the loss of Nord Stream and Yamal, but any reductions in flows from Russia via Ukraine or Turk Stream will send prices higher and make it harder to build inventories next summer.

Volumes from Russian have fallen dramatically. While EU buyers indicated a desire to taper purchases from Russia, Gazprom responded by aggressively reducing flows to the Continent. Flows on Nord Stream gradually declined and then stopped completely in late August while flows through Poland were terminated in the spring when the Polish gas operator was sanctioned by the Russian government. There are fears that similar sanctions may be imposed on Naftogaz, putting flows through Ukraine at further risk.

But there are concerns as to what will happen next. Even if the winter is not cold, without Nord Stream it is unclear whether the EU will be able to secure enough gas to refill its storage facilities next summer. Over this year’s injection season, the EU received about 16.7 bcm of gas through Nord Stream – in theory the 20bcm of new floating LNG capacity could offset this, but that would require it to have a utilisation rate of about 83%. The TTF/NBP spread for next winter is much more ambiguous than for this, as the market prices in potential tightness in Europe in Winter 2023. In addition to its new LNG re-gas capacity, the EU is negotiating for additional pipeline imports from Norway and North Africa. The Baltic Pipe linking Norway with Poland via Denmark is now operational, but is not expected to bring incrementally more gas to Europe than before.

This all means that demand reduction measures will be key to protecting inventories to allow gas stocks to be sufficient for next winter, which is why these measures are being aggressively pursued within the EU but not in Britain which does not expect to be short of gas.

The recent proposals to cap the prices of gas-fired generation in the EU might yet de-rail those demand-reduction measures. A similar cap was imposed in Iberia in May, and gas demand grew as a result – any measures to cap the price of gas used for electricity generation would risk increasing demand. The proposals have other challenges, since lowering European electricity prices would likely see subsidised EU electricity being exported to non-EU countries such as the UK, Norway and Switzerland. This would be politically unpalatable and would threaten capacity margins in France while its nuclear fleet is still operating well below par, but any measures to sell to the UK at higher prices than those available in the EU would risk violating the Brexit withdrawal agreement. With the Northern Ireland Protocol still being re-negotiated, that would place the EU in a greatly weakened position.

There are other ways the EU is not necessarily acting in its own best interests. Although Germany has finally decided to extend the lives of its last three nuclear power stations that were due to close at the end of this year, but they will only stay open until mid-April. These plants are being shut down before the end of their useful lives for political reasons. The Doel 4 reactor in Belgium is also closing, and Germany also closed three working reactors at the end of last year. These reactors could all have continued to supply non-fossil fuel electricity, easing pressure on gas supplies. This has not gone un-noticed in Norway, which is under pressure to boost gas supplies to the EU and continue exporting electricity. It will also make any moves to cap the prices paid for Norwegian gas a hard sell to the Norwegian public who could reasonably expect EU countries to optimise their own energy supplies before asking for discounts on imported energy.

The scope for further fuel switching in the power sector is very limited since the high prices at the end of last year already prompted a large degree of switching, and gas prices are likely to remain above the fuel switching range for the next couple of years, unless caps on gas prices artificially disrupt this dyncamic.

The general consensus is that UK and European energy prices will remain high in 2022, with seasonally higher prices in winter, before declining in the coming years. Even before the destruction of sections of the Nord Stream pipes, it was difficult to see any meaningful return to gas trades between the EU and Russia. It is doubtful that even a complete reversal of Russia’s position in Ukraine would be enough to restore the relationship that existed prior to the invasion as the EU will now forever be wary of allowing any single nation to exercise so much market power, particularly a country whose friendliness has been ambiguous at best.

It is likely to take 3-5 years for enough new gas projects to come on stream globally to fully displace Russian gas, and so it will take roughly that amount of time for prices to revert to previous norms.

Recent changes to the British gas market will have mixed results

Boosting domestic gas production is helpful

On 8 September, then Prime Minister Liz Truss announced the energy support scheme for households, but in the same speech she signalled an intention to boost domestic gas production, both in the North Sea and through lifting the moratorium on fracking. On 7 October a new licensing round was announced by the North Sea Transition Authority (“NSTA”) (formerly known as the Oil & Gas Authority). 898 blocks and part-blocks available are available in this round with priority “Priority Area” blocks that should lead to fields producing more quickly.

“NSTA has identified four priority cluster areas in the southern North Sea, which have known hydrocarbons, are close to infrastructure and have the potential to be developed quickly – and will seek to license these ahead of others. Applicants will be encouraged to bid for these areas so they can go into production as soon as possible,”

– North Sea Transition Authority

Under normal conditions, the average time between discovery and first production is close to five years and falling, according to NSTA analysis. Earlier this year leading operators were asked to supply details of their production and investment plans and to look at how they might go further and faster wherever possible. The application period will run until 14:00 hrs GMT on Thursday 12 January 2023.

Unfortunately, last week the new Prime Minister, Rishi Sunak reversed the decision to lift the moratorium on shale gas exploration, so there is no prospect for the development of shale resources to boost GB gas supplies.

Re-opening the Rough facility is unlikely to make any difference in the near term

According to the gas winter outlook, GB gas storage levels are currently at the high end of the 5-year range. The re-opening of Rough, which was officially announced last week, has not been factored in to its analysis.

In its heyday, this depleted gas field provided 70% of the UK’s gas storage capacity. It has been granted a licence to operate at 25% of its historic capacity during winter 2022/23 and 50% in winter 2023/24. However, since closure, Centrica has extracted all of the cushion gas and a good proportion of the tail reserves from the reservoir. It has also not addressed the well integrity issues which were the reasons for its closure in 2016, although the reduced gas volumes have significantly lowered the reservoir pressure and hence the risk. However, in the absence of compressors on the production wells, the greatly reduced reservoir pressure significantly degrades the rate at which gas can be delivered from the facility.

At the current very low deliverability rates (roughly 3 mcm/d compared with around 44 mcm/d historically), Rough will make no impact on the GB gas market this winter, and its ability to contribute next winter in any significant way is open to question. Much depends on Centrica’s plans for operating the facility which have not been made public. This includes whether the cushion gas will be replaced and how this would be funded, whether compressors will be installed on the production wells, and how the well integrity risks will be managed. Unlike other European countries, the UK Government has not imposed any targets for gas storage.

The Energy (Oil and Gas) Profits Levy undermines plans for more domestic production

Oil and gas producers in the UK pay higher taxes than other businesses. Instead of the usual 19% corporation tax, they pay the Ring Fence Corporation Tax (“RFCT”) of 30% and the Supplementary Charge to Corporation Tax (“SCT”) at a further 10%, however, certain losses and costs such as de-commissioning costs are tax deductible. In light of current high oil and gas prices, a windfall tax has been imposed on oil and gas producers. The Energy (Oil and Gas) Profits Levy Act 2022 received Royal Assent on 14 July 2022 and is a new tax on the profits of oil and gas companies operating in the UK and on the UK Continental Shelf. This Levy applies in addition to the RFCT and SCT.

The key features of the Levy, which lasts until 31 December 2025 are:

- An initial rate of 25% which takes the headline rate of taxation for oil and gas companies to 65%. The rate will be tapered down if prices revert to historic levels;

- It will apply to profits arising on or after 26 May 2022;

- There is a deduction of up to 80% available for qualifying expenditure which includes capital and leasing expenditure, and operating expenditure that improves oil or gas recovery or increases tariff receipts and is not routine repair and maintenance;

- There are no deductions for financing and de-commissioning costs;

- Losses generated under this Levy can be surrendered to group companies for utilisation against their Levy profits, however RFCT and SCT losses cannot be used to reduce Levy profits;

- There are no adjustments for commodity hedges – these should follow the same treatment as for RFCT.

The Levy is expected to raise £5 billion in its first year. The investment allowance means that companies can reduce their exposure under the Levy by making investments that increase UK oil and gas production. This is important since the UK Continental Shelf has become a more challenging and expensive region for oil and gas production as the easier to access fields have been depleted, but despite this carve out, the willingness of the Government to impose ad hoc additional taxes on the sector is likely to raise the hurdle rates for new investment.

Fingers pointed at the UK over Nord Stream

Finally, and somewhat bizarrely, Russia has declared that the Royal Navy was responsible for the destruction of the Nord Stream pipes. No evidence or explanation was offered, and UK Government has denied the claims. It seems pretty unlikely that the British would have sabotaged the pipelines…there is really no benefit to the UK in doing so, and even if the motive was to harm Russian interests, since the pipelines were not in use, it would be a very risks and provocative action with minimal benefit. EU members such as France, not known for its enthusiasm for defending the British, have similarly rejected Russia’s claims.

Britain and Europe face different energy market challenges

Gas market dynamics in Britain and the EU are fundamentally different. Britain benefits from significant domestic production, strong ties with Norway and significant LNG capacity. The EU has much less domestic capacity with the decline of Dutch production, and has historically had relatively lower LNG capacity. While the EU’s extensive storage capacity has typically been used to meet winter demand, much of this gas came from Russia and will be difficult to replace. While the EU and Britain will increasingly compete for LNG, the likelihood is that it will be developing nations that suffer most – Pakistan is facing significant energy shortages following a failed gas tender last month. A reversal of China’s zero covid policy leading to demand recovery could add further pressure to the market, although there are no signs of this happening any time soon.

These differences explain why there is a much stronger focus on demand reduction in Europe than in Britain. The EU has an outright energy short, while Britain faces temporary electricity shortages on days when there is low wind output. These are fundamentally different dynamics which require different responses…while high prices will encourage demand reduction in Britain, the public may be needed to enact load shifting and peak demand reduction measures to mitigate blackout risks in January and February. The impact of appeals for such actions could be reduced if there are public campaigns to reduce demand now. I cannot claim that such concerns are actually behind the Government’s reticence to act on demand reduction at the moment, but in its shoes I would be mindful of keeping my powder dry for when it is most needed.

In Britain we must keep our fingers crossed we avoid cold, still weather, while in the EU, fingers are crossed against cold weather of any type. It is to be hoped policymakers learn that praying for warm weather does not constitute an appropriate energy policy.

A jewel of data based reasoning amongst the sludge of opinionated internet ignorance. Thank you.

Kathryn as usual a very comprehensive article unpicking all the background for us.

The new BEIS SoS Shapps is more bullish on Rough!!

“The reopening of the Rough gas storage facility ahead of the winter will further strengthen the UK’s energy resilience and make us less susceptible to Putin’s manipulation of global gas supplies.”

I can understand why Shapps wants the British public to think that but am rather worried he might actually believe it himself.

Same here. It’s hard to be optimistic when energy ministers appear to know next to nothing about the realities of the energy markets…

Given that the UK’s building stock is both heavily dependent upon burning natural gas to keep warm AND is notoriously amongst the least energy efficient in Europe, it is peculiarly perverse of this Conservative government to be overtly ignoring opportunities to help reduce unnecessary consumption.

I can understand why they don’t want to run a campaign for the reasons outlined above, but I don’t understand the reluctance to get to grips with the underlying problem. A huge issue is around lack of measurement – the Government could immediately do two really useful things:

1. Commission studies using test properties to gather data on which are the most effective demand reduction measures. This study (https://journals.sagepub.com/doi/abs/10.1177/0143624416684641) had some interesting findings, but we need more, on different types of properties

2. Amend the EPC to include thermal imaging tests any any other sensible tests to quantify actual heat losses rather than relying on potentially incorrect assumptions and biases.

I think someone in Russia is a James Bond fan. Or at least its probably the best propoganda idea they have right now.

(JOKE) The new 007 movie; “007 Nordstream”

James (Jane?) Bond goes on his/her most dangerous mission yet to save Europeans from themselves and the former Eastern block from a gas rich dictator. With evil bases, container ships of wheat held hostage, henchmen being pushed from windows and beautiful Ukrainians showing their gratitude on Telegram; join Mx Bond and pals from the SBS in blowing up an intracontinental £5B pipe before its grand opening in submarine infested waters and without being seen. (End JOKE)

I’d watch that.

I think the only viable way to decarbonise residential space heating is air source heat pumps. The high gas component in UK electricity generation reduces the impact of this move. It’s decades too late, but we need a much larger nuclear base-load provision in my view to replace the ‘dash for gas ‘.