I began this post over the first weekend in September when I was interviewed by various news outlets to discuss the decision by Gazprom not to re-open Nord Stream 1 after a short maintenance outage. I was then distracted by the preparation for, and then the announcement of, the Government’s energy support plan, and within minutes of my blog on that being published that we heard the sad news of the death of HM Queen Elizabeth II.

It has been a moment to reflect that while the developments in the energy markets are a serious cause for concern, and will cause real hardship for many across Europe this winter, the Queen reigned over other times of difficulty and even worse hardship, during the War, the post-war years of austerity, the paralysing industrial action of the late 1970s and more recently the stress of the pandemic.

We remember that these times all passed, as the current troubles will, and we honour a monarch whose life of service, lived with grace and without complaint, is an enduring inspiration to us all.

Her Majesty Queen Elizabeth II

1926 – 2022

Closure of Nord Stream 1

Shortly before gas flows on Nord Stream 1 were expected to re-start in late August, Gazprom announced that an oil leak meant that the turbine at the Portovaya compressor station could not be re-started, and published some photographs purporting to show this oil leak. The turbine manufacturer, Siemens, has said that such oil leaks are neither uncommon nor a reason to not operate the turbine, and points out that there are other turbines at the site that could be used.

“Such leaks do not normally affect the operation of a turbine and can be sealed on site. It is a routine procedure within the scope of maintenance work,”

– Siemens spokesperson

So this was just another move in the gas war that is playing out between Russian and its European customers, which was almost certainly triggered by the prevous day’s announcement by the G7 countries that they would seek to impose a price cap on Russia’s oil exports as part of the effort to restrict funds that can be used to finance the war in Ukraine. Indeed, this position was broadly confirmed the following morning when Dmitry Peskov, a Kremlin spokesman, blamed the “collective West” for its decision to shut down flows through Nord Stream, rather than the “technical issue”. Subsequently there has also been talk of a gas price cap.

“The problems pumping gas came about because of the sanctions western countries introduced against our country and several companies. There are no other reasons that could have caused this pumping problem,”

– Dmitry Peskov, Kremlin spokesman

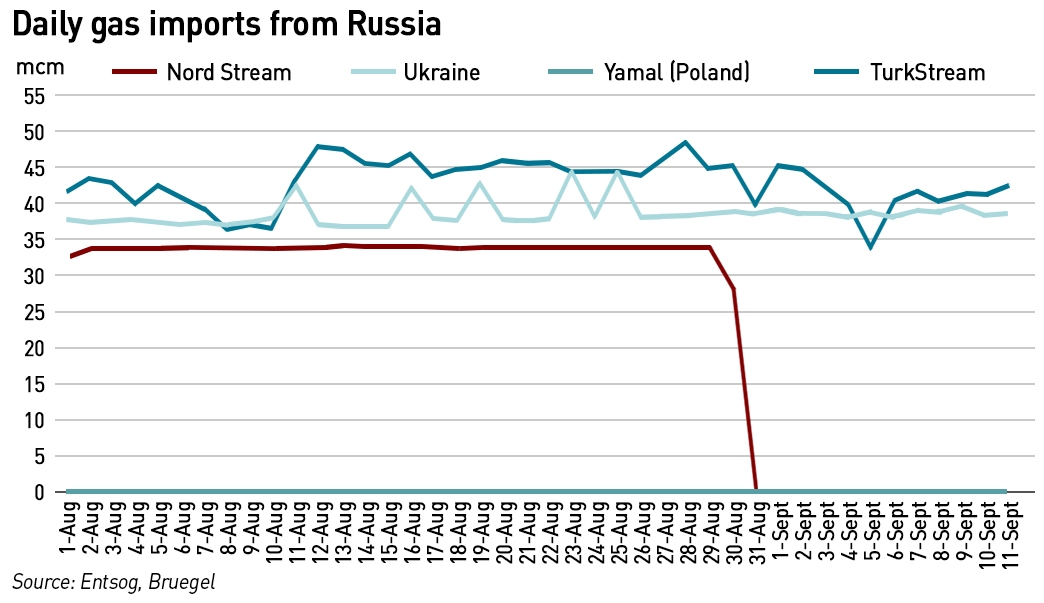

Flows on Nord Stream 1 had already been reduced to just 20% of normal capacity, which Gazprom has previously blamed on maintenance issues and the impact of sanctions which it says prevented a serviced turbine from being shipped back from a factory in Canada. The complete closure of Nord Stream, which runs under the Baltic Sea to Germany, leaves only two other major routes supplying gas to the EU from Russia: one via Ukraine and the Turk Stream pipeline through the Black Sea. Flows through Ukraine have also been curbed, while TurkStream to the south of Europe is operating without disruptions.

“Supply is hard to come by, and it becomes harder and harder to replace every bit of gas that doesn’t come from Russia. When weather turns cold and demand starts to pick up in the winter in Europe and Asia, there’s only so much LNG out there that Europe can import to replace Russian gas,”

– Jacob Mandel, Senior Associate for Commodities, Aurora Energy Research

The EU has been scrambling to reduce its dependence on Russian gas, which accounted for 40% of imports last year. With concerns that Moscow would cut flows to exert political pressure on the EU for its support of Ukraine, the bloc has rushed to fill gas storage facilities and has now exceeded its 80% target, with Germany’s storage at 84%, well above expectations. According to the Oxford Institute for Energy Studies, pipeline flows from Russia to Europe averaged around 80 mcm /day so far this month compared with almost 490 mcm /day in the first half of September 2019, the most recent “normal” year.

Were Nord Stream 1 to remain closed, Gazprom can ship its gas to Europe through pipelines via Poland and Ukraine and the TurkSteam pipeline to the South. However flows through the Yamal pipeline across Poland ceased some months ago when the Polish operator of the pipeline was sanctioned by Russia. This leaves the pipes through Ukraine, which have obvious challenges, and then the route through Turkey. Flows through both have remained broadly constant over the past month, albeit with some daily variations.

It will be interesting to see how the developments in Ukraine this weekend might affect the situation – there is now a realistic possibility that Ukraine will win the war which will dramatically change the landscape. Putin’s position will be significantly weakened, and while it seems unlikely that European governments would be willing to restore relations with Russia in the near term, it might signal a smoother transition to diversified energy sources were a new and more moderate regime emerge.

High price and high price volatility causing more stress for utilities

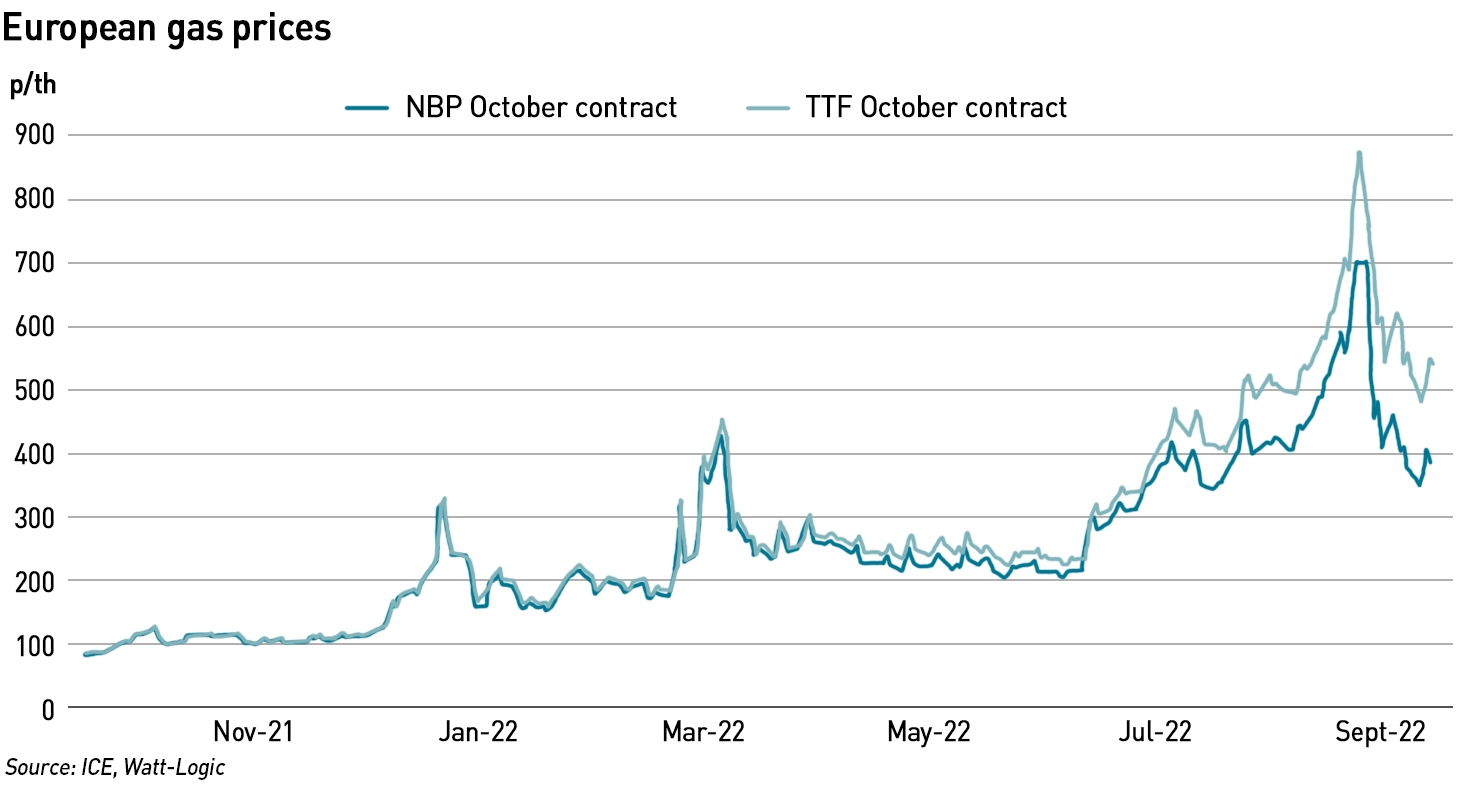

The front month (October) ICE TTF contract closed at €214 /MWh on the Friday immediately before the Nord Stream announcement, and opened the following Monday almost 30% higher at €275 /MWh, trading up to €281.00 /MWh, before declining to €240 /MWh at the close. Similarly, the front month ICE NBP contract closed on the Friday at 409.42 p/th, and opened on the Monday at 516.70 p/th (26% up on the Friday’s close) reaching a high of 560.30 p/th before also falling back to 450.23 p/th at the close. Since then, TTF has fallen back to €217.882 /MWh and NBP has dropped to 408.20 p/th in other words, both are more or less back to where they were before the drama blew up.

However, these levels are still much higher than they were a year ago, which is not only causing problems for consumers, they are also creating difficulties for energy companies trying to hedge their positions in the market. Even bilateral trading requires parties to provide credit support to protect their counterparty in the event they default on their obligations under the contract. As the value of these contracts rises, so too does the amount of credit support they are required to provide. Collateral requirements for exchange-based trading tend to be even higher – in August, Finnish utility Fortum said its collateral rose by €1 billion in a week to €5 billion, excluding funds posted by its German subsidiary Uniper. The collateral requirement on Nasdaq recently reached SEK 180 billion, up from around its normal level of around SEK 25 billion.

Over the weekend of 3-4 September, the governments of Sweden and Finland created emergency liquidity facilities to support utilities facing high margin calls when the markets opened after the weekend, since the news of Nord Stream 1’s closure was expected to (and did) send prices higher. These facilities, made up of loans and credit guarantees worth around US$ 33 billion were designed to help prevent energy companies going into technical defaults when higher prices triggered new collateral requirements in what was described as a possible “Lehman Brothers” event for the energy markets.

Sweden is providing up to SEK 250 billion (€23 billion) in credit guarantees, while Finland’s loans and guarantees are worth as much as €10 billion. Norway’s government said it is monitoring developments in the financial power market but currently does not see a need for measures of its own. Power exchange EEX has also asked for more government support to be provided to traders as the billions of euros they are forced to provide in collateral for trades is sapping liquidity and making prices even more volatile.

German utilities Uniper and now VNG have requested support from the German government. Other European firms including Axpo, EPH and PGNiG have been offered support by their governments, while the EU has confirmed the ECB won’t provide support directly but may fund banks providing liquidity for energy companies in their markets.

Britain’s largest energy supplier, Centrica, is facing a similar challenge, and is reported to be seeking support for its own liquidity needs. It appears to be speaking with banks about extending its liquidity provisions rather than asking for Government support at this stage, which makes sense, since Centrica’s upstream gas business, while small by market standards, is providing the company with strong cashflows during the current high prices. This request may have been rendered moot by the Government’s announcement of a £40 billion liquidity facility to support energy companies’ trading activities.

Russia’s game plan is difficult to read – there are no real winners, even Russia

Before this year, Russia’s long-term strategy was to maintain its presence in the European market, and to also develop it sales to Asia, with the Power of Siberia projects and the further development of the Sakhalin fields. Gazprom controls the world’s largest natural gas reserves, enough to supply both Europe and Asia for decades. Before the invasion of Ukraine, Gazprom had been the biggest supplier of gas to Europe, providing around a third of the continent’s needs. Germany had been the largest importer of Russian gas in Europe.

It is difficult to know exactly what calculations were made in the Kremlin when the invasion took place. It appeared at the time that Putin expected to over-run Ukraine quickly, and that the West would respond as it did in 2014 when Russia annexed Crimea: with disapproval but little meaningful action. However, not only did Ukraine turn out to be a significantly more competent military opponent than expected, continuing to oppose Russia six months on from the invasion, the West responded with military aid to Ukraine, significant sanctions against Russia, and a promise to dramatically reduce imports of Russian energy to undermine its ability to fund the war.

Interestingly, analysis by the Wilfried Martens Centre for European Studies suggests that Gazprom began manipulating the European gas market in 2021, when an asymmetric response to covid saw gas suppliers respond more slowly to the recovery than demand, pushing up prices. By the company’s own admission, it had significant excess production capacity that could have been used to boost supplies into Europe, and its claims to have delivered record volumes of gas to the EU in 2021 are not supported by the data. The company was also much slower to fill its European gas storage facilities than other operators.

“Russia’s game plan is to keep exports to Europe flowing at a level which allows the government to collect sufficient revenues and taxes but potentially keeps Germany’s gas market short… Gazprom is not just losing a commercial opportunity – and taxes for the state – but also actively destroying its own market…Gas prices in Europe will eventually come off the boil but Gazprom will never recover its market share,”

– Nadia Kazakova, analyst at Renaissance Energy Advisors

These cuts were intended to take place at a measured pace, to limit the impact on European economies, however, Russia has responded by reducing gas flows itself. It has also insisted on being paid in roubles rather than the contractual currencies and has cut off buyers that have refused to comply. All of this has driven up prices, so despite selling significantly lower volumes of gas, Gazprom’s income has not been undermined.

But these actions are unprecedented – even during the Cold War, gas supplies to Europe were never interrupted for political reasons, and Russia has frequently described itself as a reliable partner in the gas trade. However, in just six months this reputation for reliability has been ruined, and whatever the outcome of the war, any meaningful recovery of this business is highly unlikely. Europe is now weaning itself off Russian gas – alternative sources are being sought, and although it will take maybe 3-5 years for enough new gas production to come on-stream globally to displace Russian gas, Europe hopes to manage with a combination of fuel switching, inventory management and demand reduction.

“What I do expect is that we cannot rely in any way on Russia, or on Gazprom… We should not count on gas coming via the Nord Stream 1 pipeline over the winter,”

– Robert Habeck, Germany Economy Minister

While Gazprom might be counting its record profits this year, boosted by high gas prices, its medium to long-term prospects have deteriorated significantly. Any deals with China for Power of Siberia 2 are likely to be on terms that greatly benefit the Chinese, and as new gas production develops elsewhere prices of gas will fall. With Russian domestic gas storage facilities now almost full, Gazprom may have to start shutting in production, and once that happens, re-starting might be difficult as the process can damage both equipment and the wells themselves. Re-starting once new infrastructure to Asia has been built would also occur after those volumes have been displaced by production elsewhere, putting further downward pressure on prices.

This places Gazprom and the Kremlin in a bind. No doubt Putin is wagering that the EU’s commitment to sanctions and to Ukraine will waver as winter and possible gas shortages begin to bite – there are already calls in some parts of Germany and Austria for a negotiated settlement with Russia. But countries along the Russian border take a robustly different view. In Poland, memories of the Cold War occupation are still fresh, and the 19th century partition of the country has not been forgotten. Parallels have been drawn with the appeasement of Hitler in 1938, with many people across Europe believing that appeasing Putin now would simply delay the day of reckoning.

Ukraine has its own role to play in the gas wars since the alternative routes Russia plans to use with Nord Stream 1 closed run through the country. And even if the EU were to weaken on sanctions, it is unlikely that the UK and US would follow suit, and indeed they would probably continue to provide military aid to Ukraine meaning that the EU’s ability to negotiate with Russia would be limited to the scope of EU sanctions and other aid it is providing to Ukraine.

However Ukraine’s recent battlefield successes are providing encouragement to European politicians, and if anything strengthening their resolve both on sanctions and wider actions. In her annual state of the union speech in the EU’s parliament, Ursula von der Leyen, President of the European Commission said sanctions were having a real impact on Russia and would remain in place, saying the EU is “in it for the long haul”.

“This is not only a war unleashed by Russia against Ukraine. This is a war on our energy, a war on our economy, a war on our values and a war on our future. This is about autocracy against democracy. And I stand here with the conviction that with courage and solidarity, Putin will fail and Europe will prevail… This is the price for Putin’s trail of death and destruction. And I want to make it very clear, the sanctions are here to stay. This is the time for us to show resolve, not appeasement.”

– Ursula von der Leyen, President of the European Commission

Both sides appear to be escalating the economic war, but once the “gas card” is played by Russia, it cannot be played again. A couple of weeks ago there was some doubt as to whether the closure of Nord Stream 1 would turn out to be permanent and that the “technical issues” would be “resolved” allowing some flows to be restored, letting Putin continue to threaten the Continent. There has been no sign of this, but European governments appear to be increasingly confident that with alternate supplies, fuel switching and demand reduction, things actually won’t be too bad. High gas prices may trigger recessions in several countries, but these may not necessarily be deep or long-lived, and absent a cold winter the EU would break its Russian energy habit and be in a much stronger position for the future.

What next for the European gas markets?

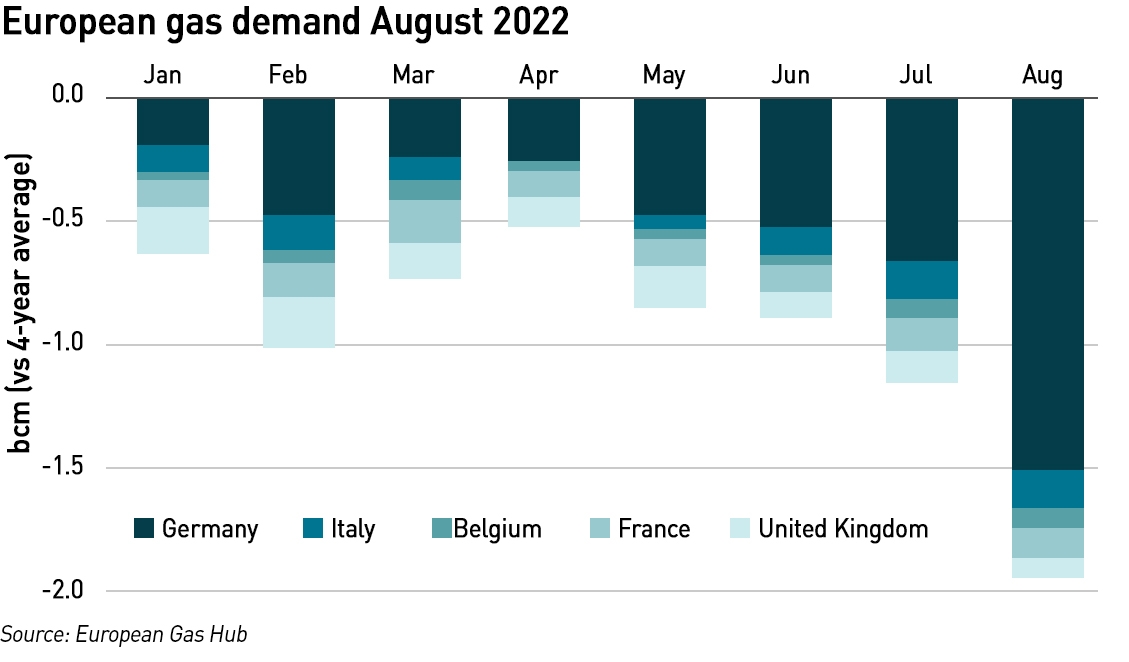

High gas prices are driving demand destruction across Europe, particularly in energy-intensive industries. By the end of August, 70% of Europe’s fertiliser production had been curtailed, although gas burn in the power sectors has grown as low wind and hydro conditions and the French nuclear outage strain electricity systems.

Wood Mackenzie expects overall European gas demand to fall to 7% below the five-year average through March, leaving a best-case scenario of storage levels at 31% at the end of the winter, in line with the five-year average.

“Strong LNG and non-Russian pipeline imports have helped get Europe gas storage levels to 80% at the end of August, beating expectations. We expect this to rise to 86% by the beginning of October. If Russian flows from Nord Stream resume at current levels following the three-day maintenance in September, Europe could be in a position to get through this and next winter without demand curtailments,”

– Massimo Di Odoardo, vice president, Gas and LNG research at Wood Mackenzie

A 7% demand reduction – less than the 15% targeted by the EU – along with record levels of LNG imports, facilitated by new LNG infrastructure next year could see gas storage levels reach 90% ahead of winter 2023/24. Even if Nord Stream 1 does not re-start, European inventories could still end up at 26% by the end of this winter, although in this case they might only reach 81% ahead of next winter. However, the weather remains a key risk – an extremely cold winter could add up to 30 bcm to winter demand and risk reducing European gas inventories levels to 4% by March meaning they could only be 63% full at the start of next winter, which would likely result in demand curtailment.

Analysts at Goldman Sachs believe that Europe has “successfully solved” the immediate issue of gas supplies “with a combination of gas demand destruction within Europe and across LNG buyers elsewhere in the world, resulting in above-average inventory builds”. As a result, it expects TTF prices to decline through winter, dropping to below €100 /MWh in Q1 23, with supplies being supported by above-average storage withdrawals, leaving inventories over 20% of full by the end of March, broadly in line with the Wood Mackenzie view.

However, it believes that the policy focus on addressing energy costs rather than curtailing demand might end up incentivising higher gas consumption – as has been seen in Spain – making the deficit worse. This poses a tightening risk to 2023 gas balances, which already look challenging, since with lower Russian flows rebuilding inventories in 2023 will be that much harder than it was this year, requiring incremental demand destruction. As a result, it expects summer 23 prices to be higher, at €235 /MWh.

“Ultimately, we believe European gas prices will only sustainably move below industrial-demand-destruction levels once global LNG supply increases more significantly, from 2025, when several liquefaction projects already under construction from the US, Qatar and Canada, among others, start to come online,”

– Goldman Sachs Commodities Research

Absent particularly cold weather, it does appear that Europe is positioned to weather the gas storm, but it will be important to ensure that poor policy decisions do not de-rail the progress that has been made, and that the efforts to secure alternate fuel sources and demand reductions persist into next year allowing inventories to build ahead of the following winter. Ultimately only the development of new global sources of gas to displace Russian volumes will see the markets return to normal operations, likely over a 3-5 year horizon. This expectation is reflected in the futures and forwards markets which see prices declining steadily over the coming years.

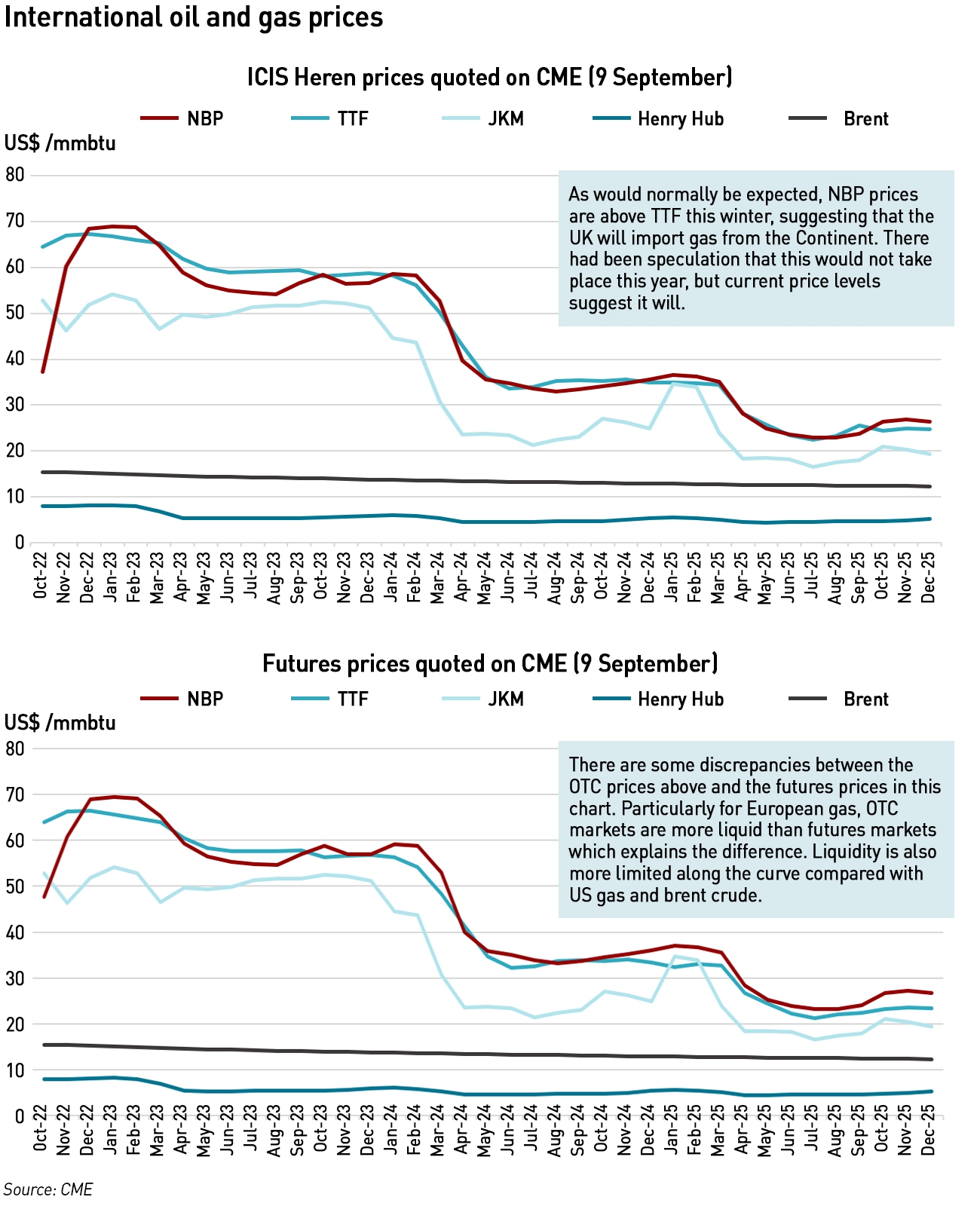

Interestingly, forward markets still expect Britain to import gas from the Continent this winter, as it would in a normal year.

Kathryn very comprehensive article showing how multi faceted this situation is. One thing that could derail this is if Putin starts looking like he’s achieved nothing will start using the nastier weapons to make a come back. Anyhow ICE has Oct 22 NBP down a stonking 21% today to stand just above £3/therm although of course still well above long run average but takes the level back to what it was two months ago and lowers the amount of money the government may need spend pressure.

Its also impressive how well EU have done in filling storage as we ahve been without the cargoes from Freeport for several months and will only start seeing them again from mid November. It also looks like Chinese are content to ramp up coal usage for the time being and dial back on expensive gas so in the short term EU has come out on top but note the forecast that next year will be a tougher ask with minimal Russian gas available.

UK has been doing well and kept its albeit low storage levels full and even LNG tanks are being kept towards the upper end of capacity with multiple cargoes a week coming into Milford Haven and allowing for high daily export rate of both gas and electricity being generated in part by gas. Its going to be interesting to see how this plays out for the UK has both gas and electricity have capacity in the summer to go into full export mode but both systems aren’t setup to do that when domestic demand is much increased.