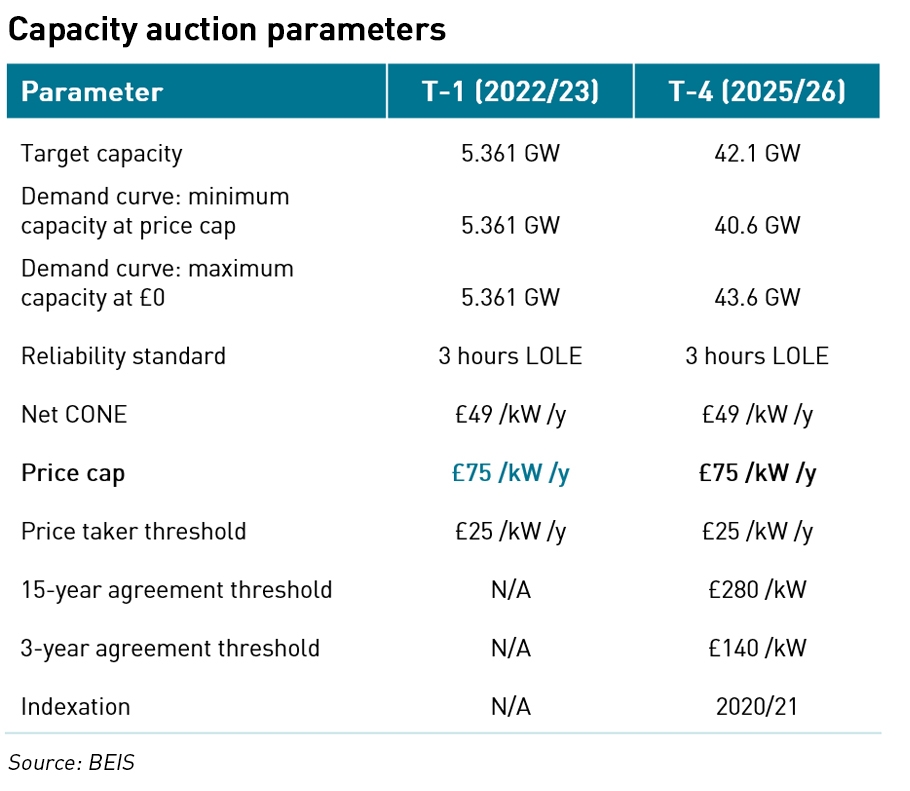

Last week the Government authorised the procurement volumes for the Capacity Market auctions to be held in February. While Kwasi Kwarteng accepted National Grid ESO’s recommendation for the T-4 auction to be held on 22 February, he decided to authorise a T-1 volume 650 MW higher than NG ESO’s recommended 4.7 GW, giving a procurement target of 5.361 GW for the 15 February auction. The reason given for this increase was “the broader uncertainties within the power sector.” Marlon Dey, research lead at Aurora Energy Research, described this T-1 target volume as a “shock move”.

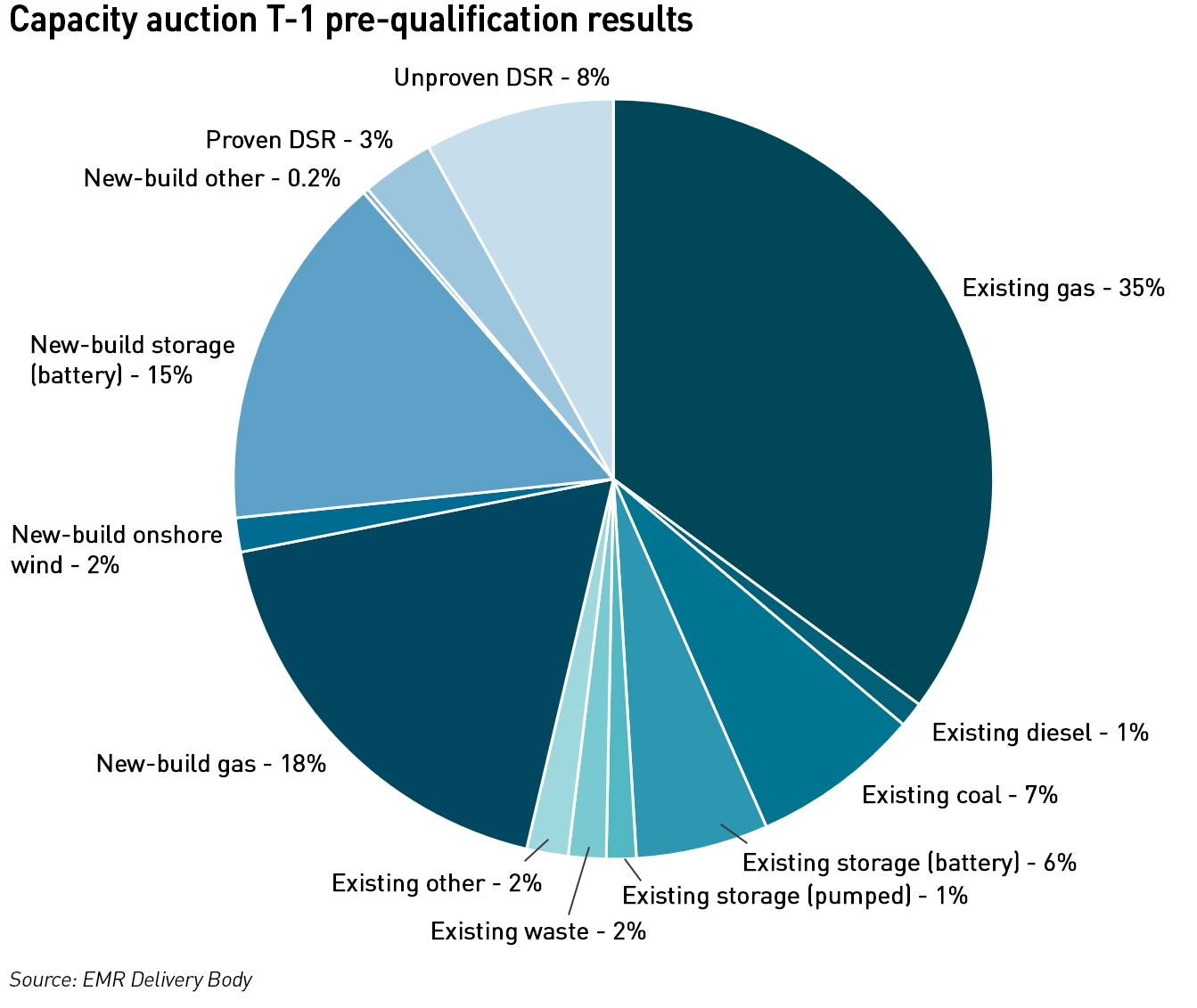

.5.361 GW is the total amount of prequalified and conditionally prequalified capacity for the auction, of which around 3 GW represents existing assets, meaning the auction for delivery next winter will rely heavily on new-build assets. This also means that the auction price will almost certainly clear at the maximum level of £75 /kW per year.

“It defeats the purpose of having an auction. It’s a massive and expensive safety net,”

– Andreas Gandolfo, analyst at Bloomberg NEF

This move means that this year’s T-1 auction will be very expensive, and part of a sharply rising trend: in 2020, 1 GW was procured in the T-1 auction at £1 /kW/y, in 2021, just under 2.3 GW was procured at £45 /kW/y, and this year we are likely to see 5.361 GW being procured at or close to £75 /kW/y. This will raise the cost of the auction to £402 million, roughly four times the cost of last year’s auction and four hundred times 2020’s T-1 auction, and is more bad news for consumers, who pay the capacity auction costs through their bills.

Most of the pre-qualified assets are gas (53%, of which a third is new-build). The second largest category is new-build battery storage at 15% of the total. Participants have until 1 February to confirm their intention to proceed with the auction…normally, some assets would be withdrawn, but given the likely high price of the auction, there will be a strong incentive for all pre-qualified assets to go ahead, even those not yet completed, although given the high default penalties, there may be some that feel the construction risk is too high.

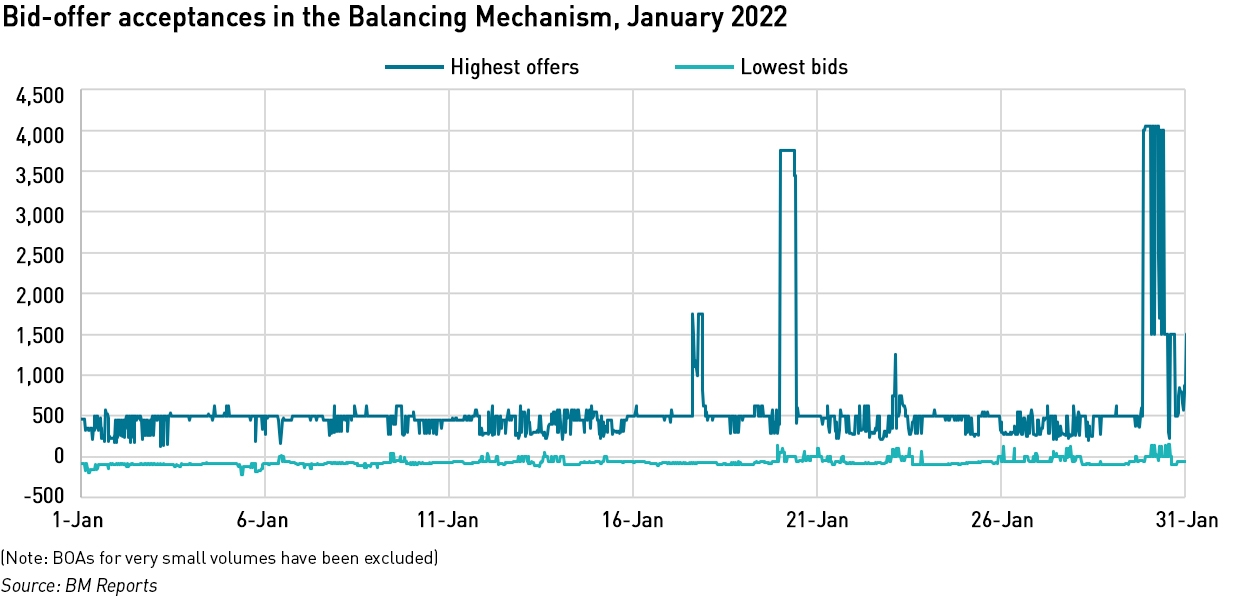

This follows the first Capacity Market Notice of the year last Monday, and a string of high prices in the Balancing Mechanism – Drax units 5 and 6 (coal) fired up for the first time since November in the BM at £4,050 /MWh and £4,000 /MWh respectively. West Burton 1 and 2 were also accepted at £3,000/MWh and £4,000/MWh, as low wind hit prices. CMNs are triggered when the surplus above the forecast demand and operating margin four hours ahead falls below 500 MW.

So far, this winter has been relatively mild, which has seen gas prices, and consequently power prices retreat from the highs of late December. But there is still scope for cold weather to cause havoc, and the market continues to be vulnerable to low wind conditions. Clearly the Government has concerns over next winter as well.

UPDATE:

The T-1 capacity auction for Winter 2022/23 closed on 15 February with 4,996 MW being procured at a record price of £75 /kW /year, which was the reserve price. 365 MW of capacity that had pre-qualified withdrew, meaning there was a shortfall of this amount against the target set by BEIS.

A quarter of the capacity was awarded to new-build generation, meaning there is significant delivery risk, although it is to be hoped that the high cost of delivery failures would have deterred developers from remaining in the auction if delivery was in doubt.

We have just demolished many GW of serviceable coal fired plant with the remaining stations closing in the near future. Coal and Gas are in the same ball park when aiming for net zero emissions. On calm days the existing wind can produce as little as 400MW. 40GW of future additional wind capacity could produce as little as 1000MW. Why is wind in the capacity auction?

Any sensible govt would mandate that the remaining coal stations are mothballed until there is more certainty on where energy market is headed. However, this lot have the demo men in before the boilers are cold and then turn up for the photo opportunity to blow them up.

I’m not sure about mothballing….these assets are pretty old and I wouldn’t bet on them being able to re-start after being mothballed. But I would just keep them in the market at least until Hinkley Point C opens – an extra 2 years of emissions from 4 GW coal is pretty negligible in the scheme of things given the likely utilisation, but would be much better than risking supply disruptions.

In reality, it is probably too late to retain most of the remaining coal fired units. As the stations head to closure, maintenance tends to be reduced to a minimum and things like statutory inspections are not performed. These issues can be addressed, at a cost, but it will take time.

A further problem, which is harder to address, concerns the people required to operate and maintain the assets. Again as the assets head for closure, the O&M staff tend to disappear and you cannot magic up the 200+ staff needed to operate a coal fired power station at the drop of a hat.

Looking back, I see that the T-4 auction for 2022-23 never happened because of dispute with the EU over state aid. That was replaced by a T-3 auction in 2020, commented on ahead of taking place by Timera

https://timera-energy.com/uk-capacity-market-back-in-play/

The chart of impending capacity deficit should have alarmed BEIS at the time. In the event, the market cleared at £6.44/kW, and they could have had another 10GW by being prepared to pay £25/kW, comfortably cheaper than the present panic. Closing down coal capacity and leaving what remains to operate in the balancing mechanism has resulted in inadequate competition in the balancing market and sky high costs and real capacity shortages relieved by demand destruction in industry.

I’ve used that capacity deficit chart a few times – it should be mandatory reading for anyone in an energy decision-making position in BEIS.

How much of the 35% new build is actually under construction I wonder or even has relevant statutory approvals to allow construction. Seems risky for T-1 for 1st October 22 to have them allowed to bid but presumably the pre qual process does those checks?