Last week saw some updates to the new UK Emissions Trading Scheme (“UK ETS”) which is set to replace the EU ETS which the UK left on 1 January when Brexit took effect. The Government has published participation guidance, and the Intercontinental Exchange has issued its auction calendar.

Like the EU ETS, the UK scheme will work on a “cap and trade” principle, where a cap is set on the total amount of certain greenhouse gases that can be emitted by sectors covered by the scheme. The caps decrease over time, and the expectation is that they will be set to align with the UK’s net zero carbon target.

Under the cap, participants receive free allowances and/or buy emission allowances either in the auction or in the secondary market, which they can trade with other scheme participants as needed. Each year installations and aircraft operators covered by the scheme must surrender allowances to cover their reportable emissions.

The scheme will apply to energy intensive industries, the power generation sector and aviation and will cover activities involving combustion of fuels in installations with a total rated thermal input over 20 MW (other than in installations for the incineration of hazardous or municipal waste). The aviation routes covered by the UK ETS will include UK domestic flights, flights between the UK and Gibraltar, and flights departing the UK to European Economic Area states conducted by all included aircraft operators, regardless of nationality.

There will be simplified provisions for small emitting installations and hospitals with annual emissions below 25,000 tCO2e and a net-rated thermal capacity below 35 MW which will be subject to emissions targets rather than trading allowances. Separate simplified provisions will be available to installations with emissions lower than 2,500 tCO2e per annum.

“Our scheme is even more ambitious than the EU system it replaces and today’s publication will give businesses and operators clarity over this year’s supply of emissions allowances, enabling them to plan ahead, build back greener and better prepare for the transition to a low-carbon economy,”

– Anne-Marie Trevelyan, UK Energy Minister

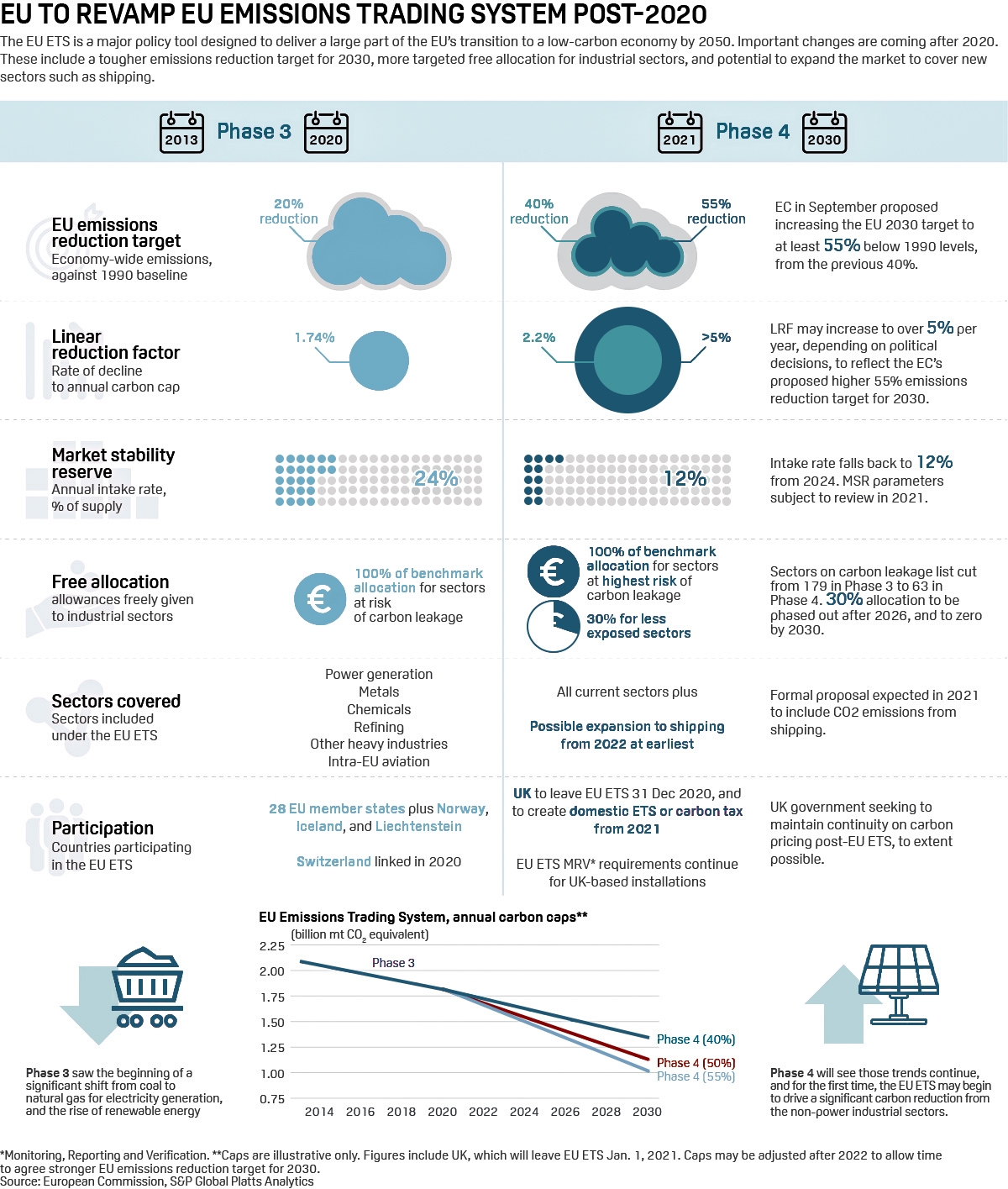

The cap on UK ETS annual allowances will be set at 5% below the UK’s expected notional share of the EU ETS cap for Phase IV of the EU ETS (2021–30), which equates to approximately 156 million allowances in 2021. The overall approach to free allocation of allowances will be broadly the same in the UK ETS as in Phase 4 of the EU ETS. The Government intends to mirror the EU ETS rules on banking and borrowing allowances.

Auction details

ICE plans to launch ICE UK Allowance (“UKA”) Futures contracts on 19 May coinciding with the first auction, with UKA Daily Futures following on 21 May subject to regulatory approval. The auctions will then take place on alternate Wednesdays until the final sale of the year on 15 December, with a bidding window of 12:00-14:00 UK time.

Auctions from May-July are scheduled to contain 6.052 million allowances each, and those in September-December approximately 5.188 million each. The August auction will contain 2.594 million permits, mirroring the halving of EU ETS volumes in that month due to the expectation of lower demand due to the summer holiday period. It will be interesting to see whether this reduced demand is met in practice given the much weaker trend to take August off in the UK than on the Continent.

Earlier this month, the Government increased the transitional auction reserve price (“ARP”) for UK ETS auctions to £22 /tCO2e, up from £15 /tCO2e as set out in its original plans for the system. Bids below this price will not be successful in the auction. The Government expects to withdraw the auction reserve price “as the UK ETS matures”, a consultation on which will likely form part of the wider consultation to align the UK ETS cap with a net zero trajectory due later this year. The ARP value was set in the Auctioning Regulations published on 11 February, and the Government does not expect to make any further changes to its level before its likely withdrawal.

There will also be a Cost Containment Mechanism (“CCM”) which will allow the Government to address any significant extended price spikes in the market. The CCM will have lower price and time triggers than the equivalent EU ETS mechanism during the first two years of its operation to allow for faster intervention if necessary. If the CCM is triggered, a meeting of the UK ETS Authority will be called to consider what intervention, if any, it should make. If there is no agreement, the final decision on any interventions will be taken by the Treasury. These interventions could include:

- redistributing allowances between the current year’s auctions;

- bringing forward auctioned allowances from future years to the current year;

- drawing allowances from the market stability mechanism account; or

- auctioning up to 25% of the remaining allowances in the New Entrants Reserve.

.\

The Government has stated its intention to formally link with the EU ETS as soon as possible. Since the UK scheme follows the EU scheme quite closely, this should be more straightforward than the linkage between the Swiss and EU ETS schemes. However, the Government has also signalled changes which would take it further from the EU ETS, with possible alignment of the cap with net-zero targets and a potential expansion of the scheme to cover other sectors. This means the uncertainty around carbon trading for UK-based businesses is set to continue.

Of course, this could all be hugely simplified if the Government abandoned its attempts to replicate the EU scheme and simply opted for a carbon tax instead.

.

As I read this some “renewables” would not be allowed – i.e. biomass. Sometimes the use of the inclusion of (wood) pellets, with their emissions, from logging is described as “greenwash”. Is this the case?

And geologic and nuclear power would so be classed as zero-emission.

If only emissions from the use of the fuel are the criterion then all forms of hydrogen (green or blue…) would be allowed – despite any emissions in creating them (effectively exporting the generation of CO2, similar to the situation for bio-chips )?

So does the US company keep track of emissions in creating and delivering fuels? Not clear on this

I strongly believe wood pellet biomass should be excluded and that companies should not be allowed to import wood pellets from countries that don’t have a carbon pricing mechanism (or if they do, they require UK permits for the end-to-end process and not just the electricity generation part).

I think with hydrogen, the hydrogen production facility would require its own permits if it’s a separate facility from that which consumes the hydrogen. The importing issues is probably less of a concern here since most hydrogen production will need to be integrated with other infrastructure, but where it is imported, the same rules should apply.

Bottom line: this is a stealth tax of about £3.5bn, while the tax and cap will serve to drive jobs offshore and close down industries.