To provide some light relief from the pervasive discussions of the novel coronavirus, I thought it might be nice to look at an interesting aspect of the Brexit negotiations. Brexit sentiment has swung significantly if perhaps not yet decisively towards a “no-deal” Brexit, and this would mean that after the transition period ends on 31 December 2020, the UK would no longer be part of the EU emissions trading scheme, the EU-ETS.

In response to this risk, the UK Government has published a paper that indicates that it would create its own carbon trading scheme to replace the EU ETS, to begin on 1 January 2021. I was quite surprised to hear about this, and my initial response was to wonder what the point of this would be in the context of the Carbon Price Floor.

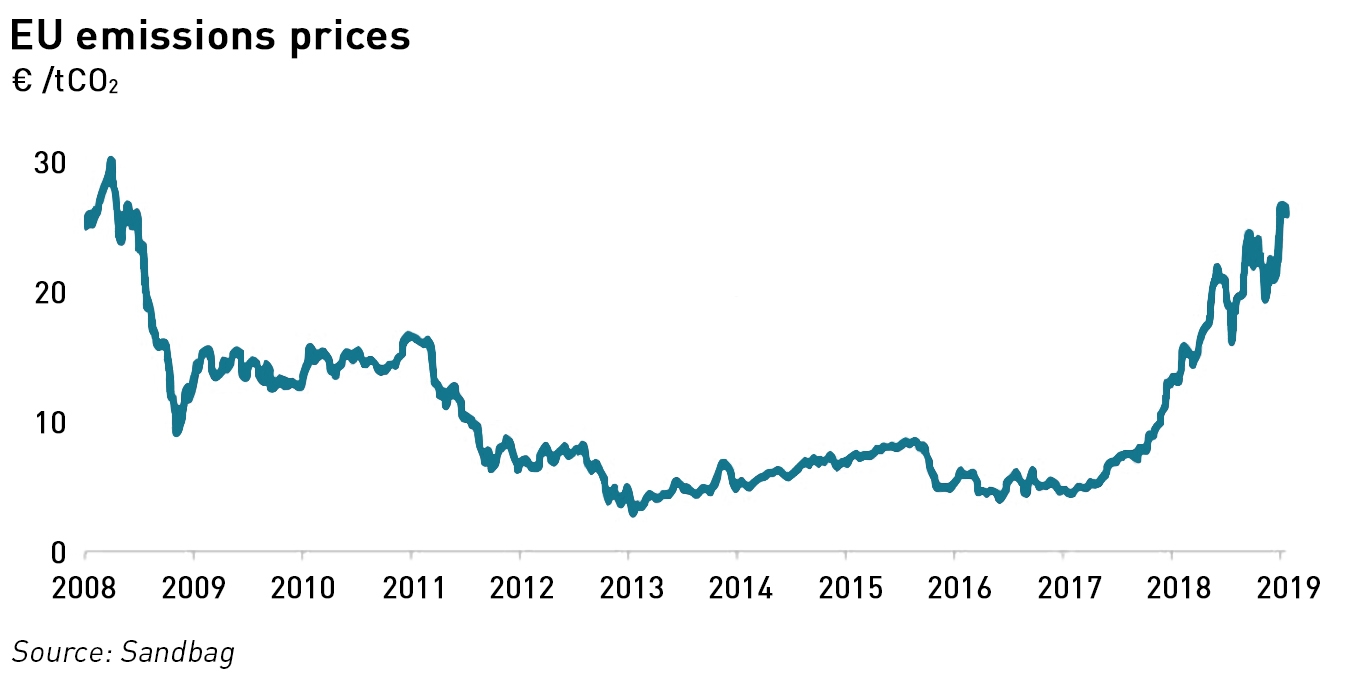

To recap, the CPF was introduced in April 2013 in response to concerns that EU ETS prices were too low to promote meaningful switching from higher-carbon generation such as coal, towards lower-carbon generation such as gas. On inception, the CPF level was £9 /tCO2 it was intended to increase every year a price of £30 /tCO2 in 2020. In the 2014 Budget, the Government announced that the Carbon Price Support component of the floor price would be capped at a maximum of £18 /tCO2 from 2016 to 2020 to limit the competitive disadvantage faced by business and to reduce energy bills for consumers. This price freeze was extended to 2021 in the 2016 Budget.

At current exchange rates, the CPS is just over €20 /tCO2 which is just below current EU ETS prices.

The EU ETS scheme works on the “cap and trade” principle, where there is a limit to the total greenhouse gas emissions allowed by all participants that is converted into tradable emission allowances. These tradable emission allowances are allocated to participants in the market through a mixture of free allocation and auctions.

One allowance gives the holder the right to emit 1 tonne of CO2 (or its equivalent). Market participants are required to monitor and report their carbon emissions and surrender sufficient emission allowances to cover their reported emissions in each year. However, various policy interventions mean that the EU ETS has evolved into a “hybrid-price control instrument” with the introduction of the Market Stability Reserve (“MSR”) in 2019, as described in this paper from a group of Dutch academics.

“Opinions about the desirability and functioning of ETS differ among climate policy-makers, stakeholders and scholars (Cramton et al., 2015). For example, Gollier and Tirole (2015)are strong proponents; Schmalensee and Stavins (2017); Woerdman and Nentjes (2019)are conditionally in favour of ETS; Pearse and Böhm (2014) reject ETS as a preferred climate policy choice.

Striking a common understanding is difficult for some reasons. Unclear and divergent meanings are assigned to essential concepts, such as ‘carbon price’, ‘emissions cap’ and ‘efficient emission reductions’. Institutional, political, social, economic, and technical realities may conflict with economics textbook’s assumptions,”

– Anatomy of Emissions Trading Systems: What is the EU ETS? – Verbruggen et al, 2019

Because the supply of EUAs into the market is by allocation, the instrument behaves more like cash than a typical commodity whose prices are driven by supply and demand. Indeed there is evidence of a high degree of speculative trading by financial traders with no fundamental carbon exposure in the EU ETS.

As the chart indicates, after seeing some high prices in its early life, EU ETS prices languished for a number of years before recovering from late 2017 onwards. From around mid-2018 the CPF was reached without the need for additional support from the CPS. The beginning of the Covid-19 lockdown saw prices dip below the price floor, before recovering again, driven in large part by technical trading and price speculation, since the fundamentals of low energy demand would not support any price recovery.

Regulators have attributed the price recovery from 2018 as a sign that the market expects the supply of allowances to be tighter in future, as a result of the MSR. However, research has found that speculative behaviour by traders undermines this conclusion:

“Our results suggest that the reform triggered market participants into speculation, and question regulators’ confidence in its long-term outcome. This has implications for both the further development of the EU ETS, and the long lasting debate about taxes versus emission trading schemes,”

– Understanding the explosive trend in EU ETS prices – fundamentals or speculation? Michael Pahle

In its communications on a potential UK ETS the Government has indicated that the creation of a UK ETS would have no impact on the economy or on individuals (which implies it sees no impact on energy bills).

However, given that any UK ETS would have, by definition, lower liquidity than the historically unsatisfactory EU ETS, and also given the long bedding-in period for the EU ETS, it seems rather strange and somewhat inefficient for the UK to move forwards with a direct replacement of the EU ETS.

I have argued in the past that the CPF should be abandoned because it made GB power prices uncompetitve where interconnected markets were not topping up the ETS price with an additional tax, however, if the UK leaves the EU ETS, this argument falls away.

Charging generators that create emissions is a reasonable way to encourage switching to lower emission technologies, but this does not have to be done primarily through a trading scheme, particularly given the various problems encountered by the EU ETS. As designing an effective carbon market is very challenging, a more rational approach would be simply tax emissions directly – a method which is less prone to gaming and indeed fraud than the EU ETS has been.

Replicating the EU ETS seems like the worst of all worlds, and against the backdrop of implementing a no-deal Brexit while trying to recover from the economic shutdown caused by Covid-19, it seems like an act of pointless bureaucracy. The Government is apparently now exploring taxing emissions rather than continuing with its plan for a UK ETS. This approach should be encouraged.

I am uncertain that measuring & taxing powerstation emissions is necessarily an effective way of reducing CO2 production associated with electricity generation – as some of the CO2 emissions would not be seen in this country

For example biofuels burnt, for example at DRAX, derive from forests chopped down in USA (said forests might require up to a century to recover and so to recover their full carbon sequestration potential – i.e. effectively increasing the amount of CO2 over that period) ; said wood is chipped and dried and then transported – all of which involves a significant amount of CO2 production – but elsewhere.

Also. Interconnects to Europe might well be sourced from coal burning in Germany or elsewhere – so who taxes, or should tax, these emissions?