The electricity system is in transition. Transmission connected, centralised synchronous generation is being displaced by multiple small installations of intermittent asynchronous generation connected at the distribution level. Advances in sub-transmission technology including as storage, smart homes, electric vehicles, DSR and others are challenging the traditional design of networks.

Accommodating these changes though traditional DNO operations would require significant investments in passive grid infrastructure, much of which would sit idle for extended periods, leading to the need for Distribution System Operators (“DSOs”) to take a more active approach.

“To accommodate these changes whilst still operating as a passive DNO would require very substantial investments in grid infrastructure, which would be underutilised much of the time. Continued construction, maintenance and operation of passive distribution networks is no longer going to deliver the best outcomes for UK energy bill payers.

To ensure a cost-effective, efficient operation of the network, there is now a greater need to forecast and actively manage energy flows across the network. This will require DNOs to have better visibility of what is happening on the network and shift in the roles and responsibilities of DNOs – the so-called transition to Distribution System Operations.

Through its Smart Systems Call for Evidence, the UK Government is reviewing what this future energy system will look like. It is considering how roles and responsibilities should be allocated and what the regulatory and legislative framework should look like to ensure that the electricity network enables the move to a low carbon energy system in the most efficient, cost effective and secure way,” – Western Power Distribution

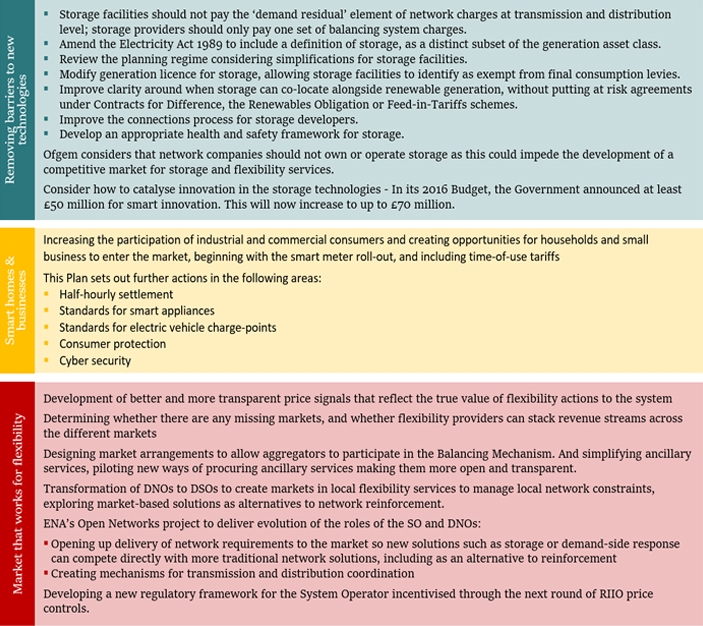

In response to these changes, Ofgem set out its vision for the networks of the future in its Smart systems and flexibility plan. In setting out the context of its plan, Ofgem describes some of the changes to date:

- an increasing need for greater flexibility across the power system, as more low carbon generation deploys and about 3 GW of new flexibility contracted since 2016;

- rapidly falling technology costs, eg average lithium-ion battery prices have fallen by over 50% since 2012;

- new IT-enabled business models which are cheaper than traditional engineering solutions, enabling greater aggregation of distributed resources across the system, and active management of distribution networks; and

- new offers for consumers on home energy management, smart tariffs, smart appliances and electric vehicles.

Predictably, Ofgem says that competition will be at the centre of its new approach, stating that markets can allow the best flexible solutions to flourish and help deliver a secure, affordable and clean energy system.

To achieve this, it intends to facilitate competition between new types of flexibility, such as storage and demand-side response, and other solutions, such as interconnection, generation, energy efficiency or network infrastructure, with the aim of allowing providers of flexibility to realise the full value of the flexibility they deliver.

This means maximising access to the existing markets (capacity, wholesale, balancing and ancillary services), alongside new markets or revenue streams for example at the distribution level, and being able to stack value across them wherever appropriate.

The plan covers the following themes:

The transformation of DNOs to DSOs will be key to delivering many of these changes, given their position between the transmission system and (most) end users.

“This country’s distribution networks are arguably now at the centre of our energy transformation. They are going to have to be more flexible, more dynamic and far smarter. Distribution Network Operators will need to transition to new roles as Distribution System Operators empowered to locally balance capacity and energy,”

– Alistair Phillips-Davies, CEO of SSE.

Beginning the DSO transition…

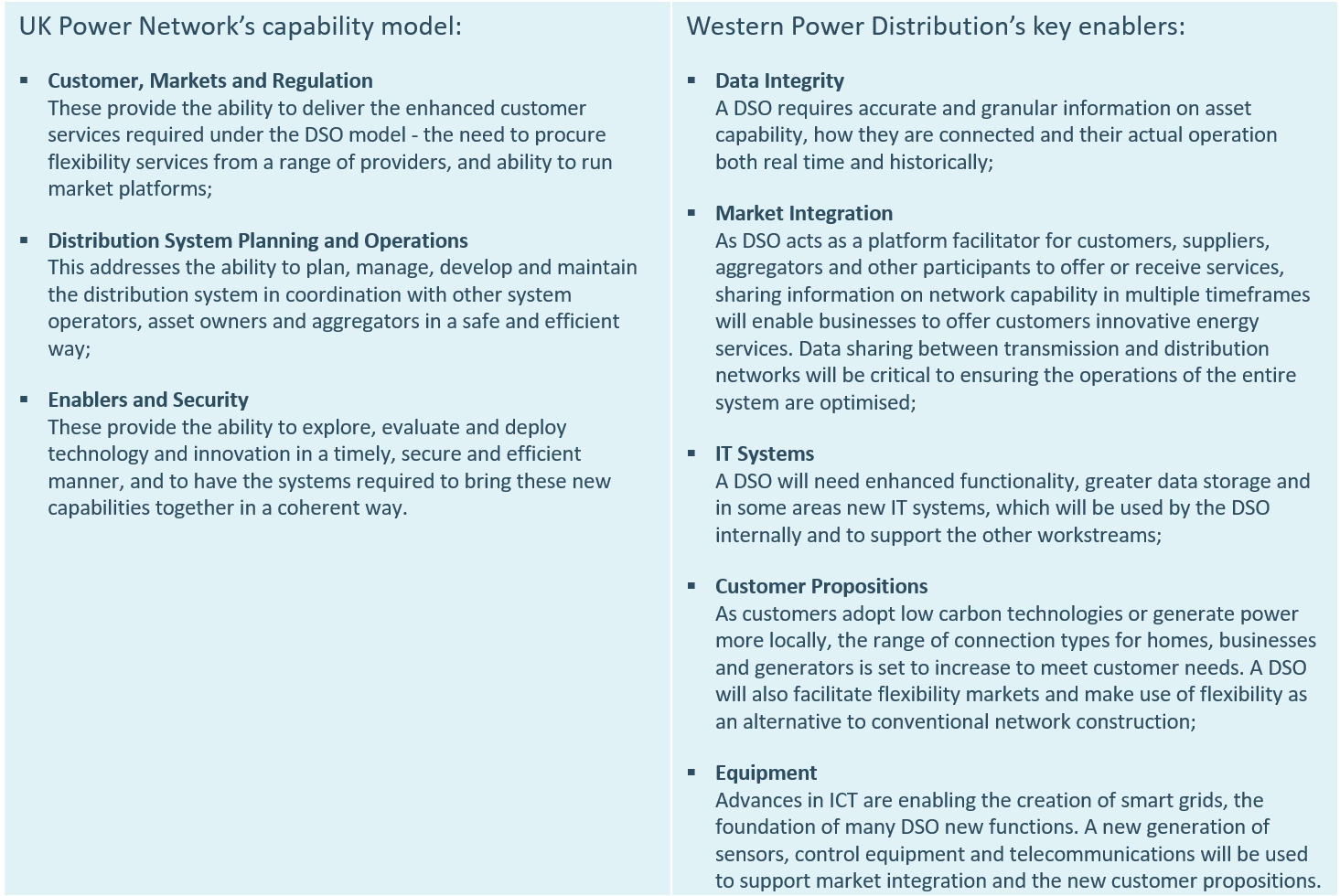

UK Power Networks and Western Power Distribution are among the leaders of the DSO transition. Both have recently set out a similar vision of the requirements for a successful transition:

UK Power Networks launches local flexibility services

UK Power Networks has recently launched a tender for flexibility services for delivery staring in January 2018. The company would like to contract with distributed energy resources capable of adjusting how much they consume or generate to support the local distribution network at times of high electricity demand.

These resources could be generators, consumers, and electricity storage that are connected to a specific network asset such as a substations, and that can increase exports (generate more) or reduce imports (consume less) when instructed in exchange for payments from UK Power Networks, thereby keeping the network asset below the local limit.

The assets participating must be able to deliver at least 500 kW of flexibility across the portfolio, although this level is under review following the consultation. Any type of technology can apply as long as it meets the technical requirements of the service.

“We are on the verge of a change as significant for electricity as the advent of broadband was for telecommunications. We are working with policy makers, regulators, academia, SMEs and importantly customers to lay the foundations for an exciting future, which will place customers in control of energy usage,”

– Basil Scarsell, CEO UK Power Networks.

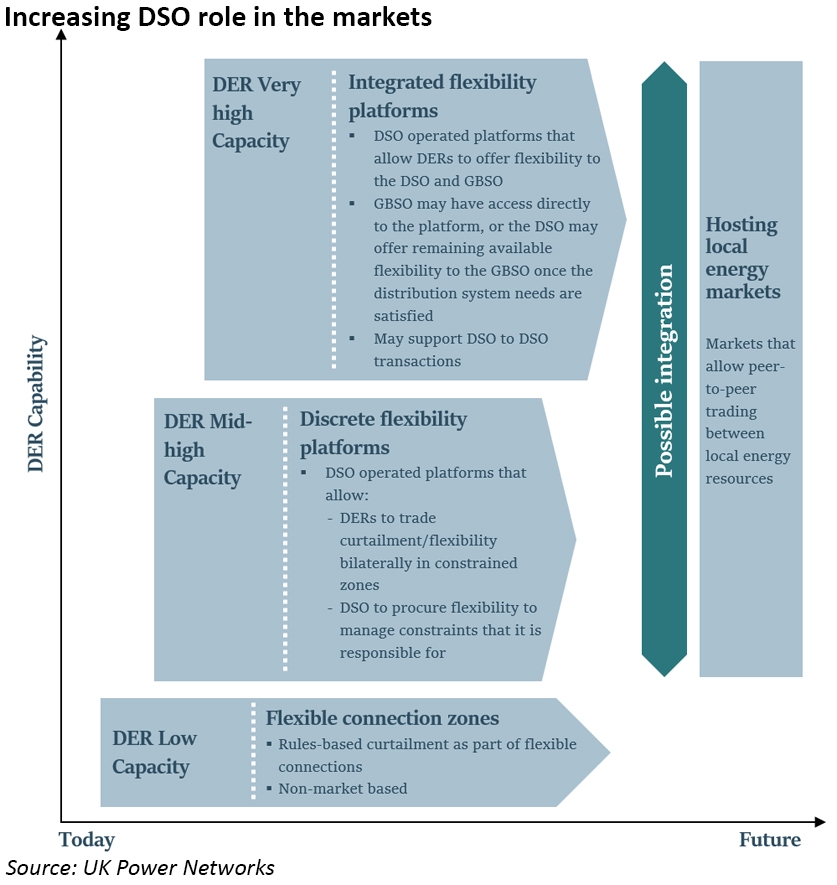

In its recent strategy paper, UK Power Networks describes the transition to a DSO, being in two phases, in the first phase, currently underway, new roles emerge as a natural consequence of making efficient use of flexibility to achieve positive outcomes for our consumers, such as reducing connection and reinforcement costs. The second phase involves a more expanded role in whole system optimisation and enabling markets for distributed energy resources.

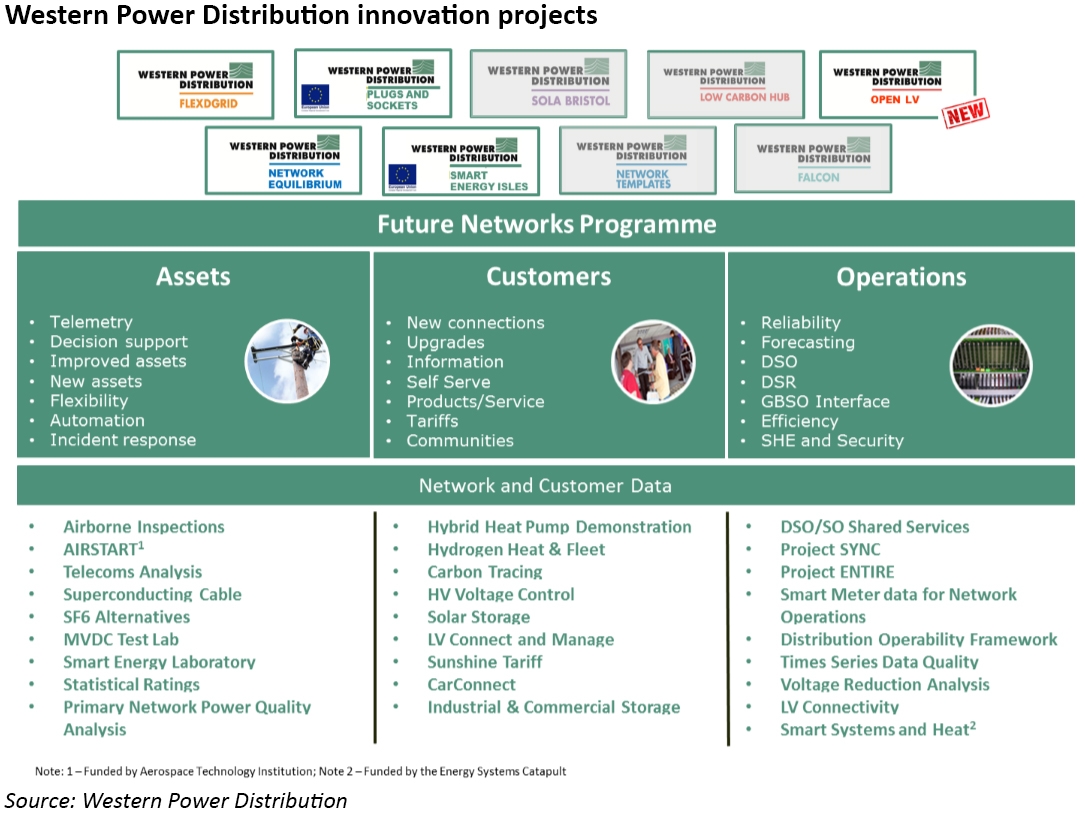

Western Power Distribution intends to become a fully “smart grid”

Western Power Distribution has launched Flexible Power, an innovation trial which will offer various revenue streams to half-hourly metered businesses in the East Midlands with the flexibility to adjust their load when required.

The scheme allows companies to participate in either a local constraint managed zone service (“CMZ”), or a fully managed service incorporating CMZ alongside STOR and Triad avoidance. WPD will aggregate the capacity offered by its customers offer demand side response to National Grid, and is hoping to deliver 100 MW of capacity through the scheme.

In the CMZ service WPD will provide customers with a week-ahead notification of its probable requirement. An “arming fee” will guarantee a level of income for participants, while a utilisation fee will cover operating costs. Under the fully managed service, Flexible Power will declare participants in and out of the different revenue streams.

Flexible Power falls under the umbrella of Project ENTIRE, a four-year project that seeks to address the conflicts between a DNO and National Grid’s contractual requirements.

UK Power Networks and National Grid collaborate on local grid management

In June, UK Power Networks and National Grid launched a new active network management scheme to boost grid capacity in the South East of England and simplify the connections process for generators.

The electricity grid in the South East has become increasingly complex, with large volumes of renewable generation and multiple interconnectors located in the region. Transmission network constraints mean generators in some areas of Kent and Sussex face significant costs connection costs.

The idea of the new scheme is to allow new generators to connect to the grid without the need for expensive reinforcements by active management of the local distribution network and distributed energy resources supported by detailed models. The connection process is also being simplified.

…but the Government needs to play a co-ordinating role

The recent report into the second phase of the government-sponsored Future Power System Architecture programme was published, suggesting that the government should take the lead in shaping the transformation of the energy sector.

“Without the necessary co-ordination, there is a real risk that these developments will have adverse impacts on the power system, leading to lost whole-system opportunities, and potential incompatibilities in the way that technology is implemented and the way that markets operate.

There is currently no shared vision or even shared understanding of how to bring all the elements together in a way that addresses whole-system issues and is efficient, effective, secure and reliable. All parties, including customer representatives, now need to come together as a whole to create that vision and, with the catalyst of government, put in place the mechanisms that will make it a reality,”

– FPSA project delivery board chair Simon Harrison.

The programme was established to develop a blueprint for the re-design of the power system that will be needed by 2030. The first phase of the project was commissioned by BEIS with Innovate UK supporting the second phase. It is being produced by the Institution of Engineering and Technology and the Energy Systems Catapult.

The core message from the second phase is that government cannot take a passive approach leaving the power sector to transform itself without risking adverse or sub-optimal outcomes.

The report identified the following areas of concern:

- Governance: the current method of amending industry codes is insufficiently flexible to respond to the degree of change expected. The transition of DNOs to DSOs may require the introduction of a balancing code at the distribution level;

- Regulatory framework: licencing arrangements need to be updated to reflect the entry of new technologies and services into the markets, and the framework as a whole needs to be reformed to take account of the system as a whole, bringing the RIIO price controls for electricity distribution and transmission into better alignment.

- Commercial arrangements: commercial arrangements have resulted in unintended consequences, for example the success of polluting diesel engines in the capacity market. Commercial arrangements can be slow to adapt to new technologies and services, making market access difficult for new participants, so new models are needed to improve efficiency, particularly around procurement of balancing services, where some distribution-level activity may be desirable.

- Technical challenges: as network complexity increases, a whole-system modelling approach is needed. In particular there is a gap between real-time forecasting capabilities at the transmission and distribution levels, and in future there will need to be standardisation and interoperability in the monitoring, control and communications systems at all levels of the grid.

The increasing presence of generation and storage at the distribution level alongside the opportunity for greater exploitation of turn-up and turn-down demand mean that management of local distribution networks can no longer be a passive exercise.

The FPSA correctly identifies the main challenges for effecting this transition, and many of these lie outside the responsibility of either DNOs/new DSOs or National Grid as the transmission system operator, meaning that the Government and Ofgem will need to take an active leadership role.

However, the task is significant, and the Government has many other priorities. In the meantime, DNOs have the opportunity to explore different solutions in their own areas, which can inform future developments at the national level. The entry of emerging DSOs into the flexibility markets can help to develop consumer interest and the required infrastructure and systems for the wider transition.

Leave A Comment