I have highlighted in recent posts some areas of regulatory reform that are needed in order to deliver the energy transition at the lowest possible cost. This is a complex challenge, so it is interesting to consider the work going on in the State of New York, where there a serious attempt to fully re-design the energy system for the future is well underway.

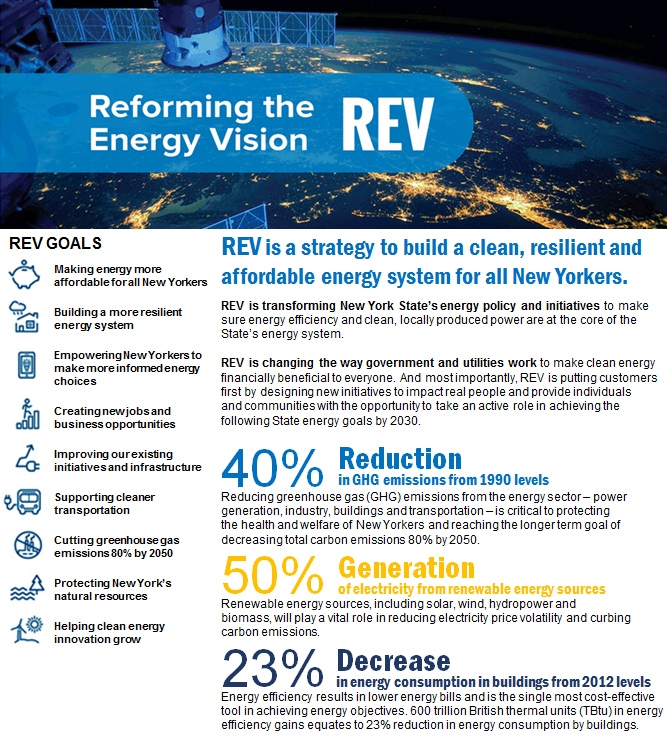

The New York State Reforming the Energy Vision (REV) was first formally proposed in May 2014 by the Department of Public Service (The Public Service Commission or “PSC”). A Green Paper, providing more detail on the overall vision was published in February 2015 (known as Track 1), and a White Paper setting out the regulatory details (Track 2) was published in July 2015. The overall NY State Energy Plan was released on 25 July 2015, which set out a number of targets for the scheme (see the infographic).

Subsequently, on 19 May 2016, the PSC issued a rate-making order setting out the anticipated utility revenue models under the REV and on 9 March 2017 three further orders have been issued:

- an order on net metering, the value of distributed energy resources and other related matters (“the VDER Order”);

- an order on distributed system implementation plans (the “DSIP Order”); and

- an order directing modifications to the interconnection earning adjustment mechanism framework (the “I-EAM Order”).

More information on the scheme are available here, including details of demonstration projects.

Background to the REV

The January 2014 draft State Energy Plan called on the PSC to:

“Enable and facilitate new energy business models for utilities, energy service companies, and customers to be compensated for activities that contribute to grid efficiency. Maximise the cost effective utilisation framework. of all behind the meter resources that can reduce the need for new infrastructure though expanded demand management, energy efficiency, clean distributed generation, and storage.”

In response, the initial REV proposal identified a number of factors placing significant stress on the traditional utility model, and concluded that in order to address these challenges two assumptions of the traditional paradigm need to be questioned:

- that there is little or no role for customers to play in addressing system needs, except in times of emergency; and

- that the centralised generation and bulk transmission model is invariably cost effective, due to economies of scale.

And that the roles of utilities, regulators, and consumers should all be re-thought.

The REV was preceded by a range of measures the State of New York had already been taking towards a decentralised energy system. These included demand response programs at the distribution and ISO levels; performance-based rate incentives and revenue mechanisms that made utilities indifferent to changes in sales volume due to energy efficiency schemes or distributed generation; time-of-use tariffs; energy efficiency programs financed by state-issued revenue bonds; a Green Bank to support clean energy projects; and implementation of statutory net metering requirements.

What does the REV hope to achieve?

Track 1 set out six initiatives:

- Enhanced customer knowledge and tools that will support effective management of the total energy bill;

- Market animation and leverage of customer contributions;

- System wide efficiency;

- Fuel and resource diversity;

- System reliability and resiliency; and

- Reduction of carbon emissions.

Specifically, the Green Paper proposed a new energy framework based around a Distributed System Platform Provider – defined as an intelligent network platform that will provide safe, reliable and efficient electric services by integrating diverse resources to meet customers’ and society’s evolving needs. The functions of the DSP would fall into three general categories: i) integrated system planning, ii) grid operations, and iii) market operations.

It is anticipated that over time, DSPs will increasingly rely on Distributed Energy Resources (“DER”) including distributed generation (solar, wind, combined heat and power), distributed storage, demand response, and end-use energy efficiency to maintain reliable system operations. Retail and wholesale operations would be coordinated to optimise system efficiency and fully realise the value of DER.

A number of models was proposed: the New York Independent System Operator (“NYISO”) could accept demand reduction bids directly from DER providers, dispatching demand side reductions in competition with supply side resources. Alternatively, the NYISO could accept bids from the DSP acting as an “aggregator of aggregators.” A third possibility is that the utility as DSP could rely on the contracted DER resources to help modify its load shape when it bids into the wholesale market to serve its own load.

Track 2 dealt with rate-making reforms setting out the basis for utility revenues under the REV.

“As DSP capabilities and DER markets develop, utilities will have the opportunity to increase revenues earned from serving as a platform for customers and DER providers to employ DERs and manage customer bills, thereby participating in achieving system efficiency and other policy objectives. Increased MBEs [market-based earnings] will have the dual benefit of 1) encouraging utilities to support access to their systems by DER providers who can improve the economics of the system and add value to end use customers, and 2) offsetting required base revenues derived from ratepayers.”

It is anticipated under the REV, that utilities would increasingly derive income from acting as DPS (subsequently described as “Platform Service Revenues”), with the mixture and pricing of MBEs being driven more by market forces and innovation than by regulatory requirements. Examples of market-based services outlined in the White Paper are: customer origination via the online portal; data analysis; co-branding; transaction and/or platform access fees; optimisation or scheduling services that add value to DER; and advertising.

The White Paper also set out a range of Earnings Impact Mechanisms (subsequently described as Earnings Adjustment Mechanisms (“EAMs”)) relating to peak reduction, energy efficiency, customer engagement, affordability and interconnection.

The White Paper advocates incremental regulatory change to achieve the objectives of the REV, to avoid unintended consequences.

Evolution of utility revenues

The May 2016 Order confirmed utility revenues as follows:

- Platform Service Revenues: new forms of utility revenues associated with the operation and facilitation of distribution-level markets. In early stages, utilities will earn from displacing traditional infrastructure projects with non-wires alternatives. As markets mature, opportunities to earn with PSRs will increase.

- Earning Adjustment Mechanisms: outcome-based earning incentives centred around to system efficiency, energy efficiency, customer engagement, interconnection and affordability.

- Greenhouse Gas reductions: utilities should have earning opportunities tied to reducing the overall cost of achieving the state’s clean energy goals. Utilities will also be encouraged to apropose programs to accelerate the conversion of transportation and building end uses to efficient electric alternatives.

The Order also set out measures for avoiding market abuse, regulation of data-sharing, incentives to replace capital investment with DER investment, standby tariff reform, time-of-use and smart-home rate-design processes, use of scorecards, and analysis of the impact of rate changes on customer bills.

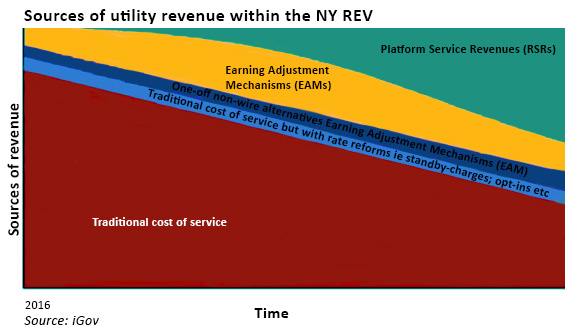

The transition of utility revenue models is described in the following chart from iGov:

Traditional cost-of-service revenues continue, but form a decreasing element of the utility business model. Being gradually replaced by performance-based income and new revenue streams from the DSP activity.

Currently, New York utilities earn just under 6% of their revenues from performance-based measures, and in the initial phase of the REV this should not increase by more than around 2%. However, the Order sets out a range of metric which will be measured under the scorecards initiative and it is likely that these will become EAMs in future, increasing the degree of performance-based income further.

This article explains how the additional measures described in the Order should facilitate market development though information sharing and customer empowerment and engagement. By making grid data and usage information widely available, utilities can signal to DER providers where their technologies can add the most value to the grid and displace traditional system upgrades, allowing them to optimize the design and development of new DER initiatives.

“The sharing of distribution-level data by New York utilities can fundamentally change the way utilities and third-parties operate,”

– Jon Wellinghoff, former chair of the Federal Energy Regulatory Commission and chief policy officer for SolarCity.

This article from Utility DIVE describes the challenges around information sharing and the benefits that can accrue.

Further detail added

On 9 March 2017, the PSC issues a further three Orders, adding further detail to the REV development.

The VDER Order

The VDER Order introduced a new pricing mechanism, the “Value Stack” which adjusts for four separate pricing components for distributed resources and is a first step away from retail rate net metering, particularly for larger installations such as solar arrays on “big box” retail stores and warehouses.

The PSC wants to move away from net energy metering (“NEM”) for retail customers, since although it is a simple way to compensate distributed resources, it is not effective in optimising their location. When every project receives the same rate, projects are built where they are cheapest to deliver without reference to overall grid requirements.

The four components of the Value Stack are:

- Energy Value, based on the Day Ahead hourly zonal locational-based marginal price, inclusive of losses;

- Capacity Value, based on retail capacity rates for intermittent technologies and the capacity tag approach for dispatchable technologies based on performance during the peak hour in the previous year;

- Environmental Value, based on the higher of the latest Clean Energy Standard Tier 1 Renewable Energy Certificate procurement price published by NYSERDA or the Social Cost of Carbon; and

- Demand Reduction Value and Locational System Relief Value, based on a deaveraging of utility marginal cost of service studies, and performance during the 10 peak hours.

In addition, utilities are directed to develop options for a fee-based portfolio service under which distributed generation projects can be aggregated into a virtual generation resource.

Existing projects that are presently net metered will be grandfathered and will be entitled to continue receiving compensation based on net metering for 20 years before transitioning to the new compensation method, as will new DER projects interconnected between now and January 2020 serving residential and small commercial customers.

The DSIP Order

The DSIP Order is significantly shorter at just 36 pages, and essentially requires the utilities to further develop their plans for establishing DSPs. In particular, the PSC identified the following areas for further work:

- Hosting Capacity: utilities must accelerate their timeline to deliver hosting capacity data for all circuits > 12 kV by 1 October 2017;

- Interconnection Portals: also by 1 October 2017, utilities are to implement the first of three phases of increasingly automated functionality to review and approve interconnection applications submitted through an online portal;

- Non-Wires Alternatives (NWA): within 60 days of the Order, utilities must file revised criteria by which traditional solutions to system needs are deemed suitable for comparison to NWA portfolios, including how NWAs are considered in planning processes, an assessment of projects in the current capital budget against the suitability criteria, and an indication of when an RFP would be issued to address those needs;

- Energy Storage: by the end of 2018, each utility must have two operational energy storage projects, performing at least two separate grid functions (e.g., peak load reduction, increasing hosting capacity)

- Aggregated Customer Data Privacy: within 90 days of the Order, utilities must propose building energy management and benchmarking data standards.

The NWA provisions and building energy data sharing provisions have been well received, but there has been criticism of the Order for setting unambitious targets on storage, and for failing to develop the area of clean DERs and in particular energy efficiency measures. According to Sara Baldwin Auck, regulatory program director for the Interstate Renewable Energy Council, the 9 March Orders represent a “milestone in a long and multifaceted proceeding,” but ultimately said the DSIP decision could have done more:

“It fell short of the blueprints needed to really build the grid if the future,”

– Sara Baldwin Auck, Interstate Renewable Energy Council.

Auck explained that the missing details on the capacity available for distributed interconnection at the circuit level, and the value of that capacity were necessary for long-term planning.

The I-EAM Order

An even shorter order (17 pages) was issued to deal with the specific area of performance-based incentives for utilities to improve their interconnection processes. The Order requires utilities to carry out interconnection customer satisfaction surveys to assess the current and future state of the interconnection process. Three core timelines of the process are to be tracked.

The Order has been criticised by limiting the tracking to only three metrics which could inhibit the ability of the public to monitor the performance of the utilities. The PSC has also allowed each utility to have a different interconnection performance metric target which arguably undermines comparability.

Grand ambitions but little concrete progress

Three years on from the initial proposal, cracks are beginning to show, possibly due to the sheer ambition of the project. The PSC has issued a number of high level designs, but specifics are still lacking. Utilities will have to undergo radical transformation in order to deliver the role envisaged under the REV, and there is little information on how this will be achieved.

This lack of data makes planning difficult for the entrepreneurs and innovators on whom the state is relying to develop businesses to supply many of the services that will underpin the new system.

According to this paper by technology consultants West Monroe, while the overall framework developed by the PCS has been well-designed to account for the many inter-related moving parts, in practice, some areas, such as rate design, may be moving too slowly and falling out of sync with the others.

The lag of fifteen months between the Track 1 and Track 2 Orders means that implementation of many DSPP components were underway long before changes to rate design and utility business models could begin to be adapted. On top of this, the Track 2 Order provides relatively long timelines for action to be taken by utilities on certain tariff reforms, and given the amount of time required for rate pilots and final negotiation and implementation of rate cases, it is likely to be many years before New York utilities are able to update their rates to sufficiently account for the DSPP reforms required by REV.

“In spite of these challenges, however, the reception of REV by key stakeholders has largely been positive. Environmental advocates and intervenors have lauded the initiative as a major step forward for clean energy and carbon reduction.31 While REV is challenging New York’s electric utilities to push themselves to be ever more innovative and collaborative at a fast pace, for the most part they have expressed support for the proposed reforms” – West Monroe.

Decarbonising the electricity system requires changes to every segment of the market – a complex, multi-dimensional problem with may inter-dependent elements. New York State, with its Vision for energy market reform is unusual in its attempt to devise a holistic way of approaching this process, working with industry stakeholders – particularly the utilities – to try and design a regulatory framework that will allow the markets to deliver the State’s energy goals.

The creation of DSPs and the proposed changes to utility revenue are of particular interest – if executed well they have the potential to deliver an efficient platform for full engagement of distributed generation and storage, demand-side response and energy efficiency with properly aligned incentives for all market participants.

If badly executed, market distortions will persist and even become worse, decarbonisation will be delivered at high cost, and energy security may be at risk. The stakes are high, but the State has explicitly recognised the risks of not reforming the system while trying to achieve clean energy goals. Policy-makers elsewhere would do well to pay attention to the REV with a view to applying successful elements in their own markets.

Leave A Comment