Subsidies and extra-market support now underpin every part of the UK electricity market, and as a result, some technologies benefit from double payments and others double charging, and since the double payments are going to diesel generators and the double charging to battery storage, the system is creating perverse incentives that conflict with core government policy.

Attention is currently focusing on the role of embedded generators in the capacity market, and whether the economic models applying to them are suitable. Part of this relates to how embedded generation affects use of the transmission network and the distribution of NTS costs. The current scheme for recovery of these costs was developed before the policy-driven renewables rollout, in a world where all generation was transmission-connected, so it is appropriate that these issues are examined.

Unfortunately, it appears that a piecemeal approach is being taken by BEIS and Ofgem, which risks further complicating and already highly complex system of payments and charges in the electricity market, risking inefficiencies and inintended consequences.

Layer upon layer of subsidies

To recap, financial support for grid-connected generation is now paid to:

- renewable generators (RO certificates, CfDs);

- conventional generators (SBR, CfDs, capacity payments); and

- payments for grid security and support (black start, EFR etc).

In addition, generation is increasingly connected to distribution networks – so-called “embedded generation”. Embedded generators also benefit from a range of direct and indirect support:

- “embedded benefits”, primarily payments from suppliers who are able to avoid transmission costs by contracting with embedded generators;

- capacity payments for plant participating in the capacity auctions (15 year contracts for new plant);

- tax benefits for plant financed through Venture Capital Trusts (VCTs), Enterprise Investment Schemes (EISs) and Seed Enterprise Investment Schemes (SEISs)…these can apparently enable investors to earn up to six times their initial investment in just four years with tax relief;

- payments from suppliers relating to reduced Capacity Market Supplier Charges which are based on the supplier’s net demand, i.e. after taking deducting embedded generation.

A review, commissioned by UK Power Reserve and compiled by consultancy firm Ecuity, has found that that some capacity market bidders were using investments that came with special tax relief, allowing them to bid very aggressively. James Higgins, a Partner at Ecuity, said:

“Being able to bid at a low level, while still getting high returns on their investment, means that the outturn price of the 2014 and 2015 capacity market auctions has been lower than anticipated and the government has not been able to secure the right generation mix via the capacity mechanism.

In particular, large gas fired power stations (CCGTs), have been squeezed out of the mix because they would not make a profit at the outturn price.

These investors, which we estimate comprised over 700 MW in the first two CMAs, are being subsidised in two ways: via their tax breaks which we estimate has cost taxpayers £145 million – or £5 for every person in the UK – and via capacity market payments, which are paid for by the UK bill payer.”

At the same time, new technologies such as turndown DSR and battery storage face hurdles to participation. T-DSR is only eligible for 1 year capacity contracts and must provide significant credit deposits, while batteries face double charging through addition of renewable subsidy recovery both when the battery charges and when the electricity is eventually delivered to consumers.

The net result of all this is that the winners of UK’s Energy Market Reform have largely been small embedded diesel generators, hardly the desired outcome of a policy aimed at driving decarbonisation of the electricity sector.

A series of consultations is now underway to address some of these distortions.

Embedded benefits may become less generous

Ofgem is evaluating changes to the embedded benefits regime, in particular looking at triad avoidance payments. A spokesperson was quoted in The Telegraph saying:

“We believe that the size of payment that embedded generators get during the periods of highest demand may be distorting the outcome of the capacity market and putting them at a competitive advantage. Any market distortions need to be addressed.”

This is causing concern for some market participants, who note that embedded benefits can make up between 20% and 50% of the revenues of small embedded plant. A report by Cornwall Energy outlines the dangers of making such plant uneconomic:

- loss of this generation would adversely affect both capacity margins and system flexibility;

- affected embedded generators may invest in their own transmission connectivity, potentially undermining local network resilience and moving system costs onto generators that remain on the system;

- investor confidence would be negatively impacted;

- reductions in capacity and increases in system costs would be passed on to consumers, resulting in higher bills.

A previous analysis by Cornwall Energy on embedded benefits concluded their removal would result in:

- a higher capacity market clearing price;

- higher wholesale electricity prices, reflecting an increase in the marginal cost of embedded generation;

- an increase in the cost of ancillary services as embedded generators need to make up for a shortfall in their revenue through higher contract prices;

- higher levels of reinforcement and other costs at the transmission network level as embedded generation is replaced by transmission-connected generation;

- higher levels of reinforcement and other costs at the distribution network level as the export from embedded generation is reduced;

- potentially higher balancing costs, as more volume enters the balancing market; and

- a higher cost of capital for all generation due to the increased risk associated with industry change.

I’m not wholly persuaded by some of these points. For example, the growth in embedded generation is a relatively recent phenomenon, and is often cited as a factor in the changing role of the transmission system. It therefore seems unlikely that the reinforcement question in general is valid as traditionally all generation was transmission connected. There may be a second-order point that new generation on the transmission system may be located in areas that are subject to congestion, or which lack connectivity, in which case investment at the transmission level would be needed.

An analogous point can be made in relation to the question of distribution network reinforcement. It is not clear that the removal of recently added generation would necessitate major network reinforcement.

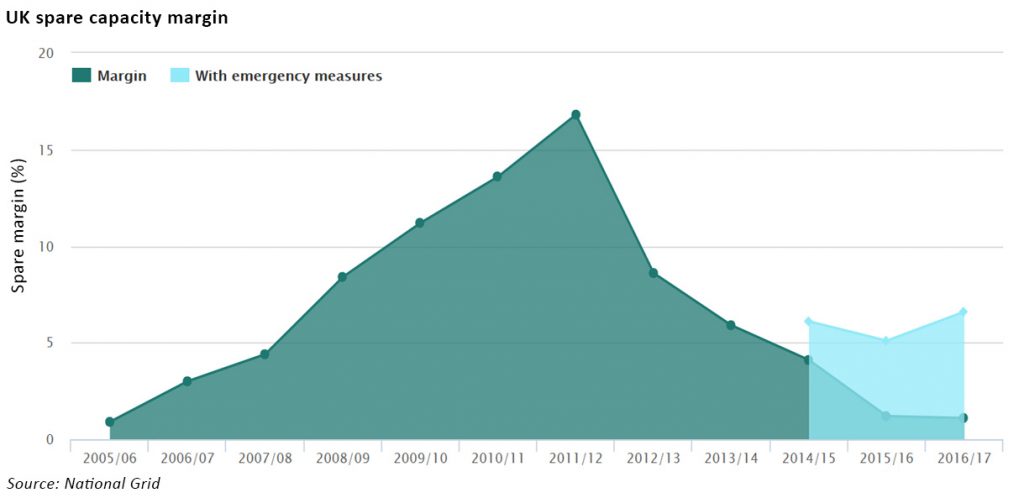

The reduction in capacity if some embedded generators close could be significant. According to Cornwall Energy, Ofgem’s changes could adversely affect the economics of up to 8 GW of existing small plants and 2GW of new small plants due to be built in coming years. When the capacity margin for this winter is forecast to be just 3.4GW including emergency schemes, this is very significant.

This would certainly lead to higher capacity market prices, as this generation would need to be replaced, and as some of this plant was able to bid very aggressively in the auctions due to the range of benefits outlined above, it is likely that new embedded generation would need to assume a less generous economic landscape and therefore require higher capacity payments.

Where the Cornwall Energy report makes some very good points is in relation to the regulatory approach, which at present is rather piecemeal. They advocate a wholescale review of transmission charging principles, to ensure that demand and generation are treated equitably, and that all energy market interactions are taken into account. This is highly desirable, and the decision by Ofgem not to conduct a Significant Code Review in this area appears to prioritise speed over completeness, risking further changes in the short-to-medium term.

However, the concerns raised by Cornwall Energy relating to the risks of embedded generators closing are likely to fall on deaf ears, as the government may well be pleased to see the closure of embedded diesel plant, which undermines its decarbonisation goals. The incentivisation of such generation under the EMR has proved to be embarrassing for the government, so much so that Defra is consulting on new emissions restrictions that will severely limit the operation of diesel engines.

The capacity market is also changing

BEIS is currently consulting on changes to the capacity market. Of particular relevance is the proposal to calculate the Capacity Market Supplier Charge (“CMSC”) based on gross rather than net demand. The reasoning behind this is that embedded generators benefit from capacity payments, however as they typically contract their output to suppliers, they act as a source of negative demand which reduces the supplier’s CMSC, a benefit that is often shared with the generator. This effectively means the generator benefits twice from its capacity contract, which is seen to provide embedded generators with an unfair advantage in the auctions.

There are a number of other, largely technical elements to the consultation, but many would like to see the changes go further, particularly in relation to new technologies such as turndown DSR and battery storage. The Energy and Climate Change Committee has argued recently that the growth of new technologies is being inhibited by outdated rules.

A number of industry participants gave evidence to the Committee along these lines. According to Colin Calder, CEO of PassivSystems,

“What’s really important is that we reform the capacity market so that it isn’t biased towards capacity, but is biased towards buying three different types capabilities in the network. One is storage, the second is demand-side response and the third is generating capacity itself. This is not picking technologies. It’s about picking different capabilities.”

Sara Bell from Tempus Energy stated:

“We need to ensure that those conservative tendencies to support generation are not allowed to take precedence over new technologies and that’s definitely happening today.”

While Jim Watson, director of the UK Energy Research Centre added:

“If we’re interested in the least cost, then it seems crazy to me that we’ve got this capacity mechanism, which is supposed to be technology neutral, but is simply not.”

The Committee wants to see longer contracts for DSR providers in the Capacity Market, the removal or the requirement for DSR developers to put down a deposit before bidding into the capacity auction, and a review of rules currently preventing storage providers from stacking other revenues on top of capacity market payments.

The Committee also proposed use of a merit order in the capacity auctions, to give priority to DSR over diesel generators when the margin between bids is tight, and a specific subsidy for storage.

A holistic approach is needed

While these measures are all worthy of consideration, there is a risk that the adding more subsidies and specific rules will further distort the market, and investors will react with caution to the prospect of uncertain economic frameworks in a complex and changing landscape.

A better alternative would be to allow the full cost of delivering electricity in all delivery periods to be reflected in energy and balancing market prices. By valuing flexibility as well as capacity, the markets should deliver the required investment signals for new provision, be that generation, DSR or storage.

In addition, a full and technology neutral review of transmission charging should be undertaken. Keeping transmission costs separate from energy and balancing costs makes sense as it removes the need for regional energy pricing, hence increasing trading liquidity, however, the full cost of delivering electricity in all delivery periods includes the cost of transmitting it, so it is important that an equitable scheme is developed.

Further separating the role of the provider of transmission capacity from the system operator would help remove mismatched incentives and allow a more technology agnostic approach to develop.

The energy trilemma speaks to the need for delivering a low carbon system at low cost while ensuring ongoing security of supply. Tinkering with a highly complex set of market rules that are not fit for purpose risks all three nodes of the trilemma and is bad news for both market innovators and end consumers.

Leave A Comment