In my last post I wrote about the nature of innovation and the challenges of delivering commercially successful innovations even when a clear need has been identified. In the energy sector those clear needs to innovate can be found across the board, from the cost-challenged E&P environment to the re-shaping of the power markets.

European governments face many challenges in re-designing their energy markets to achieve climate and other goals. The pace of renewables development has taken many by surprise, particularly in Germany where the huge success of wind and solar delivered in the north of the country poses real issues for grid operators trying to balance the system with the main centres of industrial demand being in the south of the country. In the UK, the government continues to make adjustments to market rules intended to stimulate the provision of new capacity against a backdrop of de-carbonisation and the need for a reliable and affordable system – the famous (or infamous!) “trilemma”!

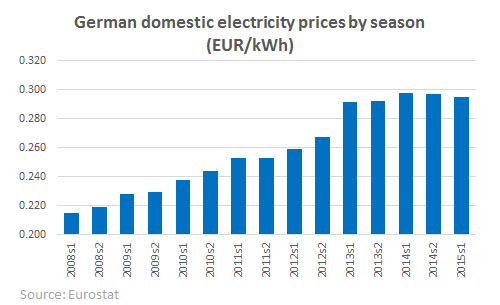

And the question of affordability is an interesting one. People naturally think that renewable energy is free to produce, so it would be reasonable to conclude that increased renewables penetration should lead to falling energy prices. In the wholesale markets that is largely the case, and in Germany where renewable generation must be dispatched if available, negative prices are not uncommon, yet consumer bills have risen steadily.

The reason for this mis-match is the need for subsidies to make the construction of renewable plant economic. New generation facilities need to be built and connected to the grid, which can be very expensive, for example in the case of offshore wind. As no sensible investor would back the construction of an asset whose output might be considered to have little or no cost/value, governments must provide a support framework to incentivise creation of renewable capacity. There has been some limited debate as to whether these costs should be met through customer bills or general taxation, but as most taxpayers are also consumers of electricity, the point is somewhat moot.

In September 2013 Ed Milliband, then leader of HM Opposition, announced in his speech to the Labour Party conference that a Labour government would fix retail energy prices. This marked the start of a wider public discussion on the cost of energy policy and the impact of subsidies on consumer bills. What wasn’t really reported at the time was that this idea was not new – in fact it had been tried and tested in California in the early 2000s. Tried, tested and found wanting, as the local utilities literally ran out of cash and the state had to step in, buying electricity in the wholesale markets for supply to consumers, since the utilities could no longer afford to do so.

The role of policy-makers is therefore a difficult one. Governments struggle to access the expertise required to properly design well-functioning markets, and it’s not at all clear such a top-down approach is feasible even if the best experts were all engaged on the project – the pace of innovation, whether fast or slow – can de-rail the best-thought out plans.

Similarly, governments tend to be quite bad at picking technology winners, so rightly try to develop technology neutral approaches that can have sometimes perverse consequences – Germany’s carbon footprint actually increased with the growth of renewables as the simultaneous exit of nuclear generation saw coal and lignite filling the gap. In the UK the success of small-scale diesel generators in the capacity auctions also flies in the face of the decarbonisation agenda. The holy grail is a regulatory framework that stimulates the emergence of the “best” combination of technologies and avoids locking the system into uneconomic or undesirable solutions as the market itself evolves.

.

Leave A Comment