Ofgem is in the process of reforming the way in which users pay for access to and use of electricity networks, which I have described in previous posts here and here. The Targeted Charging Review is the more advanced project and is tackling reform to the residual component of network charges, with a Significant Code Review addressing forward-looking charges and network access.

In May, Ofgem updated its proposed timetable for implementing its network charging reforms:

- TCR (embedded benefits reform): implementation by April 2020 has been ruled out and Ofgem’s preference is now for April 2021.

- TCR (residual charging arrangements): Ofgem previously indicated its preferred implementation date was either April 2021 or phasing between 2021 and 2023. April 2023 is now considered another leading option.

- SCR (network access reform): Ofgem is now proposing to implement all access reforms in April 2023 rather than having a phased implementation with changes to transmission charges being adopted in April 2022 and changes to distribution charges in April 2023. The SCR conclusions and impact assessment are due to be published in early 2021.

In addition, Ofgem has published a series of working papers and further consultations on both the TCR and SCR. On the TCR, Ofgem still intends to move to a fixed charge system, but is consulting on banding customers based on voltage levels rather than line-loss factor class (“LLFC”) as suggested in its initial minded-to decision. This would result in both a larger number of bands and greater variability of charges, as described below.

Ofgem has also described its current thinking on the SCR where it is leaning towards setting forward-looking charges based on long-run marginal costs, with locational granularity to the primary substation level. On network access arrangements, Ofgem is of the view that while a number of alternative approaches might be attractive, there are challenges in terms of being able to implement them in the time frames under consideration for the SCR.

Refinement of residual charging proposals

In its minded-to decision on residual charging, Ofgem indicated it preferred a fixed residual charge levied on final demand, a position supported by most participants in the subsequent consultation, but some concerns were raised in respect of the detailed design which has led Ofgem to refine its thinking.

Domestic customers: Concerns were raised about potential impact on low consuming and vulnerable domestic users, and about the implications of charging domestic customers with Economy 7 more than other households. Ofgem still believes that domestic users should be treated separately from non-domestic users due to their different characteristics, and is considering the approach to any segmentation of domestic consumers under a fixed charge option, including the combination of all customers into one charging band.

Non-domestic customers: Some stakeholders felt that the proposed fixed charges should take more account of the diversity of non-domestic users, with users within a given band varying meaningfully in size. In response to this, Ofgem is now considering fixed charges, with refined segments for non-domestic users at each voltage level, instead of using line-loss factor classes:

- total allowed residual revenue would first be apportioned between voltage levels, on the basis of net volumes, as set out in the November 2018 minded-to consultation; and

- segment boundaries would be set in terms of agreed capacity levels for users at higher voltages where this data is widely available, and net volume levels for low voltage users instead of segmenting on the basis of the line-loss factor classes.

Ofgem’s large user research suggests a number of factors would limit users’ ability or willingness to reduce their agreed capacity in practice, limiting any change to the economic efficiency of the proposed approach. Overall, Ofgem believes boundaries should be designed to avoid undue discrimination between similar users, and a low number of segments should help reduce incentives to change behaviour further.

Ofgem has identified five national level charging bands for low voltage non-domestic users and five charging bands for high voltage / extra high voltage non-domestic users, and proposes to set and allocate users to bands on a historic basis and update them periodically in line with price controls. There may some segments that contain relatively few users, so Ofgem is seeking views on how this should be accounted for in the banding.

The impact of the proposed change to the minded to position introduces a greater degree of granularity in charging bands and a greater variation in potential charges. Based on the illustrations shown for customers in the northeast, some low voltage users could see material increases compared with current charging levels, as could some extra-high voltage users, while some high voltage consumers may see their residual network charges fall.

Update on significant code review

This week, Ofgem has also published a set of working papers setting out its thinking on forward charging and network access arrangements.

The Significant Code Review includes the following areas:

- distribution network charges (Distribution Use of System (“DUoS”) charges);

- transmission network charges (Transmission Network Use of System (“TNUoS”) charges);

- the distribution connection charging boundary; and

- the definition and choice of access rights for transmission and distribution users.

Ofgem is exploring improvements to distribution locational charging signals, including new network cost models and changing the extent to which distribution charges vary by location. At a high level, Ofgem’s initial thinking is that distribution network cost models should continue to be based on the Long Run Marginal Cost (“LRMC”) but that the consistency of cost methodologies across different voltages should be improved to minimise distortions. The different approaches to calculating LRMC will be assessed for example whether spare network capacity should be factored in.

Ofgem is also looking at the design of distribution network charges, and has identified a number of options for structuring tariffs to send cost reflective signals about the contribution of users to network costs. Tariffs could be based on agreed capacity rights, maximum measured capacity requirements during a particular period, or actual usage during particular time periods. Charges could also to be set more dynamically, and there could be charging rebates at peak times for users reduce their network usage, however Ofgem believes there is insufficient network monitoring and forecasting capability for this to be feasible for a 2023 implementation date.

The scope of Ofgem’s work on transmission charging (TNUoS charges) is narrower than the review of distribution network charges. There are three high-level options for reforming transmission demand charges: the current dynamic charging approach could be reformed, or an agreed capacity approach could be introduced, there could be a static charging approach based on actual consumption or capacity used during peak periods. Ofgem’s initial thinking is that dynamically setting peak charging periods or moving to an agreed capacity approach would lead to the most cost-reflective signals, although there could be some implementation challenges.

Network access rights define the a user’s ability to import from or export to electricity networks in terms of capacity, timing, duration and firmness. Ofgem believes that improving the choice and definition of access rights would be beneficial to network users and enable more efficient use of networks, which would benefit consumers more broadly as costs are ultimately passed on to electricity consumers.

Ofgem believes that providers of flexibility can realise value either through network price mechanisms or contractual arrangements, and will consider within the access review how the value that flexibility can bring to network management is signalled.

Ofgem’s work will follow three basic principles:

- Arrangements should support efficient use and development of system capacity;

- Arrangements should reflect the needs of consumers as appropriate for an essential service;

- Any changes should be practical and proportionate.

More detail on location-based distribution charging

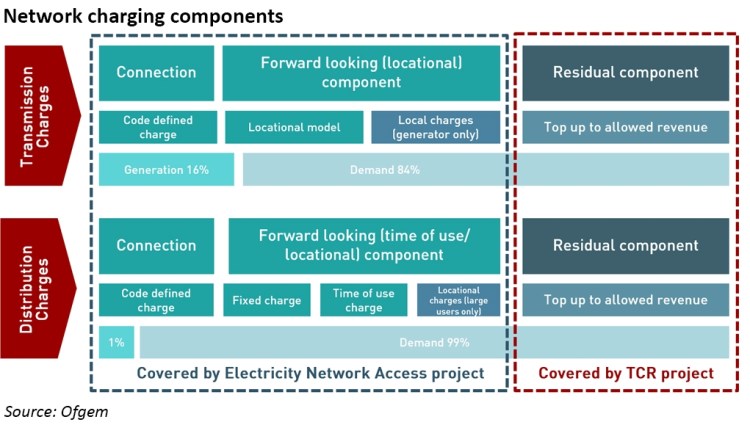

The elements of network charging are shown in the diagram below.

Model methodology

There are two main cost models under consideration: Short Run Marginal Cost (“SRMC”) where infrastructure costs are considered to be fixed and charges are based on the cost of increasing or decreasing generation in (close to) real time to manage constraint, which could mean that in the absence of constraints, SMRC could be zero in some cases; or Long Run Marginal Cost (“LRMC”), where infrastructure costs are not fixed, and charging reflects the costs of building new infrastructure and whether the behaviour of users can change the need for this development. SRMC is the current charging basis in the UK and most international electricity markets.

SRMC charges could be set ex-ante – by forecasting network conditions and the marginal cost of resolving any constraints ahead of time, or ex-post – calculating the SRMC price of each time period after the fact, based on constraints that actually occurred and any curtailment actions that were taken by the DNO. LRMC charges would involve deciding which costs to include, and whether to focus on signalling costs that would be incurred in the short to medium term or not, and whether existing spare capacity should be factored in.

Ofgem’s current thinking is that an ex-ante SRMC would not be feasible due to the difficulties with generating accurate cost forecasts. It could risk exposing users to a highly dynamic and volatile charge that does not accurately reflect the underlying network costs incurred. An ex-post SMRC regime would place the forecasting burden on users, who would need to try to predict what the charges might be in order to take mitigating actions. This would be similarly difficult and the charges, while accurate, are also likely to be highly volatile, meaning that this approach is also not favoured by Ofgem.

At this stage, Ofgem is leaning towards a LRMC-based approach, but has not determined whether it will take an incremental approach where the network cost model foresees that network reinforcement (and potentially replacement of existing infrastructure) to be needed within a certain timeframe, or an ultra-long run or allocative approach, or some combination of the two.

The scope of costs needs to be considered – are network costs seen purely in terms of electrical assets, or would wider costs such as civil work or the cost of call centres be included. Ofgem’s initial view is that there are some costs that are more strongly correlated with the size of the network, such as the repair of faults, general repair and maintenance, business rates, tree and overhead line clearances, and diversions.

The model also needs to consider to whom price signals are being sent. Ofgem has identified two potential approaches:

- Generation and demand receive equal and opposite charges/credits, with signals covering upstream costs only – charges only apply to the impact users have on the network at the voltage to which they are connected and the voltages above; and where a user contributes to upstream costs, they would pay a charge, and if they help offset costs they receive a credit. This is similar to existing arrangements for extra-high voltage users.

- Users pay charges for either upstream or downstream flows they are contributing to, with no opposite credits – charges reflect the impact a user has on either upstream or downstream power flows. Those adding to dominant flows would pay a charge, but those offsetting dominant flows would not receive a credit.

Ofgem’s initial view is that an approach that does not involve credits would be more cost reflective, but that as this change would be very significant to network users, there would need to be a very strong justification for making it, which it does not currently feel is present.

Locational granulatiry

Currently, there are three models for calculating distribution network charges: Forward Cost Pricing (“FCP”) and Long Run Incremental Cost (“LRIC”) which are both defined under the EHV charging model (the EDCM), and the Asset Replacement Model (“ARM”), also known as the “500 MW model” used in the model for low and high voltages (the CDCM). Additionally, there is the Transport Model, which calculates TNUoS charges. The ARM charge is an “all the way charge”, which accounts for the user’s requirement for using the EHV network also.

Ofgem is considering changes to the approach, possibly by changing how users connected at low voltage and high voltage levels are charged for their impact on the EHV network, moving away from a model where EHV costs are averaged across a DNO region to one that is more locationally granular. EHV charges could be calculated for all primary substations and passed down to the customers connected to them.

In terms of implementing locationally granular charges, Ofgem is looking at three options, classified according to whether they would generate a “nodal charge” (specific to the location of each individual customer), or a “zonal” charge (where the locational charge could apply to multiple customers). A hybrid approach could also be taken involving nodal charging down to a certain voltage level and zonal charging below that point.

A granular signal is already calculated for customers charged under the EDCM who connect to primary substations at the EHV/HV boundary. This signal could be easily be passed on to users of the HV and LV network, and Ofgem sees some merit to this approach, particularly if existing distinctions in cost model methodologies between voltage levels are retained. Any change along these lines would need to be integrated with the options for varying CDCM charges by primary substation, or by groupings of primary substation.

In addition, the models used for the EDCM could be consolidated into a single model, as a standalone initiative, or in combination of a new apportionment for low and high voltage users.

The EDCM currently contains two different methods for calculating locational charges for customers connected at EHV or at a primary substation. Each DNO can choose which method to apply for customers in its area: LRIC is used by eight DNOs and produces a nodal charge, while FCP is used by six DNOs and produces a zonal charge based on network branches. Ofgem does not see a rationale for retaining different approaches for different areas, which are largely an artefact from historical charging reforms where a common approach was not agreed, and sees strong benefits to ensuring a harmonised model is developed.

Both LRIC and FCP take an incremental long run approach. In considering the potential for an ultra-long run approach, Ofgem is considering the possibility of extending the Transport Model (used to calculate TNUoS charges) to the EHV network.

Based on its work to date, Ofgem does not expect it will be feasible to develop and implement location-specific charging below the primary substation level, so forward-looking DUoS charges are unlikely to be locationally granular at the individual street or household level. There are a number of options for setting charges based on grouping primary substations including:

- Averaged charging across groups of electrically proximate primary substations (eg clustered substations within a postcode region);

- Charging based differences in cost drivers (eg urban vs rural areas);

- Charging based on asset mix (eg the average length and/or proportion of overhead lines versus underground cables); and

- Charging based on whether network reinforcement is driven by generation export or demand import constraints (ie generation or demand dominated areas).

Ofgem believes introducing generation-dominated and demand-dominated archetypes could have merit, as there is reasonable data to support such a classification at primary substation level, and this would allow clearly different cost drivers to be differentiated.

More detail on network access arrangements

Traditionally users have had little choice of access rights, however, Distribution Network Operators (“DNOs”) have begun to offer flexible, interruptible connections as an alternative to paying and/or waiting for network reinforcement required for a standard connection. For many small users, access rights are less well defined and may have been agreed a long time in the past by previous occupants of the site.

Ofgem expects users to be charged for network access on a cost-reflective basis – if a user obtains an access right that avoids additional network costs (eg off-peak access), this should be cheaper than an access right that drives additional network costs. These costs should reflect the different access choices available.

In addition to firmness, time profiling and shared access, Ofgem is also considering whether short term rights should be offered, which would provide a limited duration access (eg one year) where long term access is not immediately available or where the user does not want to make a long term commitment. New access conditions are also being evaluated, for example, “use-it-or-lose-it” or “use-it-or-sell-it”.

Ofgem is broadly positive on introducing more connections based on different levels of firmness but notes this may be challenging with a 2023 timeframe in mind. Static time profiled access rights could give system benefits and should not be too difficult to implement, although more work would be needed to enable dynamic time profiled rights.

Some stakeholders have expressed concerns that introducing explicit shared access rights may reduce natural wider network diversity, creating complexity and inefficiency in the system. The trading of access rights might be easier to implement, however it would take time to develop orderly and liquid markets. Ofgem intends to work further on both of these areas as it believes they have the potential to create value for consumers.

The work on short-term access rights is currently a lower priority as, although Ofgem sees some value in this option, it is likely to offer lower benefits than the other approaches under consideration. New conditions of access such as “use-it-or-lose-it” would require standards to be set in relation to what would constitute “use”. Ofgem intends to look further at access conditions after the other reforms have been further refined.

Procurement of flexibility

Network operators are increasingly using flexibility in order to defer or replace physical network reinforcement. This raises questions as to whether the cost of procuring this flexibility should be reflected in the network charging cost model (ie should the forward looking charge reflect the cost of flexibility procurement as an alternative to the cost of network reinforcement, or a combination or the two). A further question is whether there is any case for a distribution-level version of the Balancing Service Use of System charge, as DNOs procure more flexibility services. Ofgem’s preliminary view is that no changes are warranted in response to either question at this stage. Ofgem’s detailed thinking on this can be found in its discussion paper.

The process of network charging reform if a slow one, however there are some positives in these recent announcements, not least bringing the timing of implementation for the TCR and SCR closer together. Fears continue to be expressed by market participants that the TCR changes in particular threaten the provision of flexibility, and flexibility providers do indeed face challenges over the medium term, with changes to network charging being more clearly articulated than changes to the revenue models for flexibility.

National Grid is undertaking a significant reforms of its balancing services procurement, which is the other side of the revenue/cost equation for flexibility providers, and there may well be timing gaps where some sources of income, particularly triad avoidance, fall away before new revenue streams fully emerge.

Providers of flexibility will need to develop robust business models to manage this transition, but the fundamental need for flexibility is only going to increase.

This is a very complex topic. Potentially OFGEM could have a much more radical review on the assumption that they are freed from the constraints of EU law that severely limit the level of locational charging for generators, who are subsidised to set up wherever they want with consumers forced to pick up the tab. This leads to inefficient network design and much higher than needed costs.

Perhaps one way to try to understand it is to consider what it may mean for different kinds/locations of generators and consumers. A nuclear plant tends to make good use of its network connectivity, but a peaker plant might pay dearly, even though its contribution is sorely needed. A wind farm that only occasionally produces at full capacity (and when it does so, may create transmission constraints because all its neighbours will also be producing at full capacity) is surely a very different beast. Generators on the other end of an interconnector continue to be subsidised as far as I can see. All consumers are disadvantaged by the sub optimal generation network. Some are disadvantaged still further by virtue of being more distant from where generators have set up. By keeping the whole treatment opaque, these injustices are being hidden.

I fully concur with the comment about network costs being opaque and hidden from the user- despite being a significant part of the bill for electricity.

The average cost per unit of power is not given publicity.

In the past I suspect that the costs of networks connecting to suppliers was not overly variable and more evenly distributed.

However with the move to lower power generators and more intermittent usage – means that some costs are higher per MW and some per MWhr.

In addition the connections to some generators are likely to be more expensive than others (due to distance or for being subterranean – or under water)

As the customer is, currently, paying then it is reasonable to expect that these costs are taken into account when contracts are negotiated with suppliers and they take the burden of the connection costs and any indeterminacy.

Unfortunately the costs of grid connection to suppliers (as well as their usage) is not something the National Grid or OFGEM make available (or at least not easily) – and may act as a hidden subsidy (paid for by the customers) for some generators.

If anyone knows how connection charges are paid by suppliers (and how fairly) it would be useful to hear – or know if NG or OFGEM have the figures .

What an excellent review of the situation. Many thanks for taking the time and trouble to set this all out!