There has been a lot of noise recently about the prospect of a move to some form of location-based pricing in the GB electricity market. National Grid ESO is strongly in favour, seeing nodal pricing alongside a return to centralised dispatch as the best solution to the growing problem of network congestion. Energy System Catapult, Policy Exchange and Octopus Energy agree, while Regen disagrees, as do many people I have spoken with on the subject recently. Ofgem is considering the idea, among others. So what is location-based pricing and would it solve the problem of network congestion?

What’s wrong with the current pricing system?

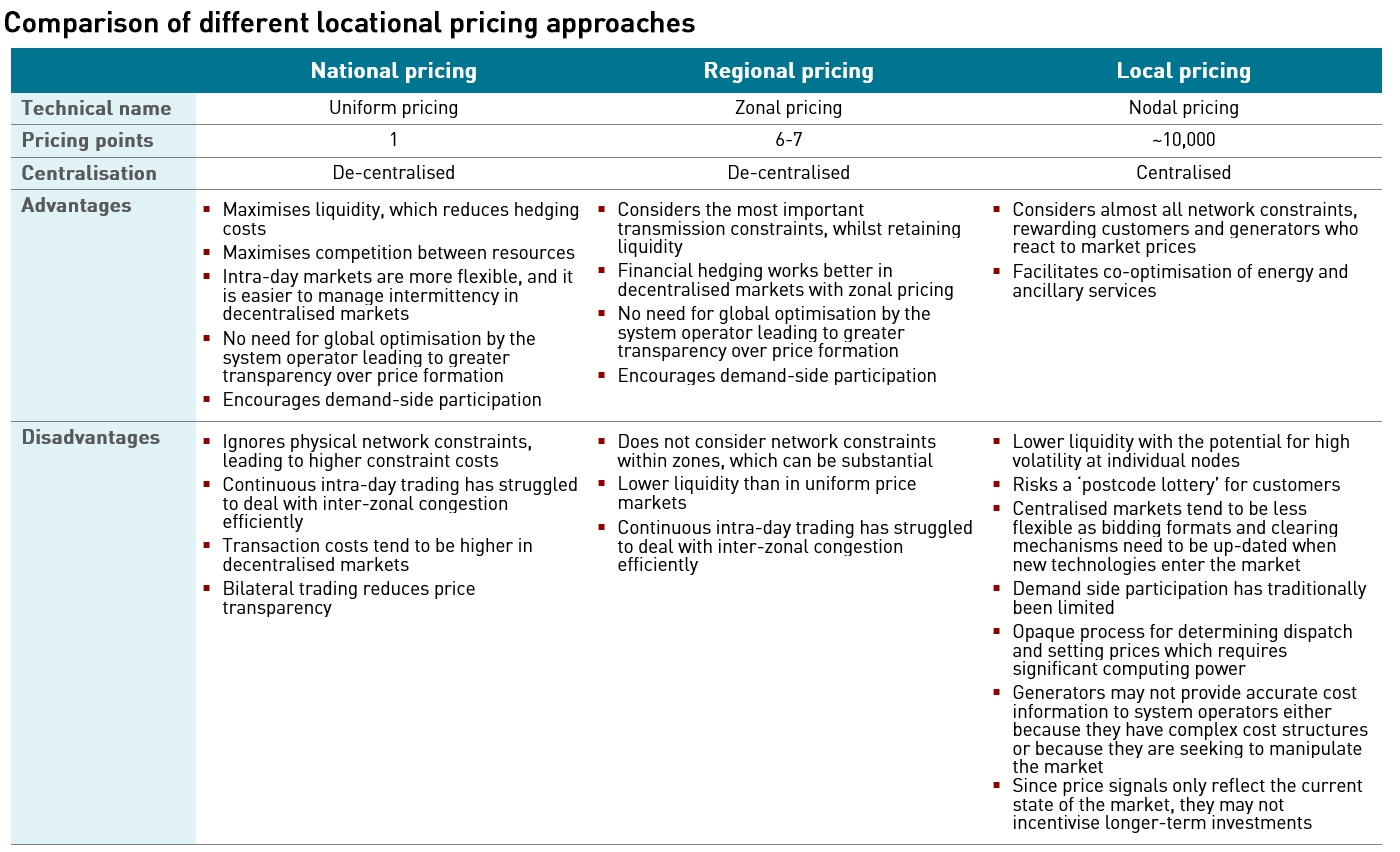

In Britain we currently have a uniform pricing system where all participants in the wholesale markets pay the same price for energy in each settlement period regardless of their location in the country / on the network. Various network costs, some of which are locational, are charged separately, but the price of the basic trading block for any individual delivery period at any time is the same.

The main problem with this approach is that the network is considered in a sub-optimal way ahead of real time, as forward trading generally neglects network congestion inside large trading regions. In Britain we are seeing increasing wind generation being built in the north of Scotland while the main demand centres are in the south of England. A lack of transmission capacity to bring this electricity from the north to the south means that increasing amounts of wind generation has to be curtailed, and generators paid curtailment fees, which is raising the network costs paid by consumers.

This problem can be mitigated by dividing countries into several zones as in Scandinavia, by introducing flow-based zonal pricing as in Central Western Europe, or with nodal pricing (which is used in both the de-centralised market in New Zealand, and centralised markets in the US).

“…the existing wholesale market design is contributing to a dramatic rise in constraint costs and inefficiencies in balancing the network, while undermining the capability to deliver demand-side flexibility. And if left unchanged, the current national pricing model will impose excessive and unnecessary costs on consumers,”

– National Grid ESO

NG ESO believes that the changes to the location and nature of generation in the energy transition means that locational issues are now of greater importance, and the current national pricing model fails to deliver sufficiently strong locational price signals to allow network costs to be optimised. It favours a nodal pricing model with centralised dispatch, and some element of self-commitment but with prices set in the electricity pool.

What are the different pricing options?

Uniform pricing

In a national wholesale market such as that in GB, the price of electricity in any settlement period is the same for all market participants (both demand and supply) regardless of their location on the network. The System Operator (“SO”) resolves congestion by ‘re-dispatch’ – instructing selected generators and/or loads to change their schedule. In the GB initial dispatch is determined by market participants themselves under a ‘self-dispatching’ model – market participants trade with each other in the wholesale markets and those trades determine their generation and consumption in each settlement period. At Gate Closure (1 hour before the start of the settlement period), market participants notify the SO of their positions, and the SO ensures that the system is balanced at all points on the network and at all times within the settlement period by increasing or decreasing generation or consumption through the Balancing Mechanism.

Locational signals come through transmission charging which is separate from the balancing process.

Locational signals come through transmission charging which is separate from the balancing process.

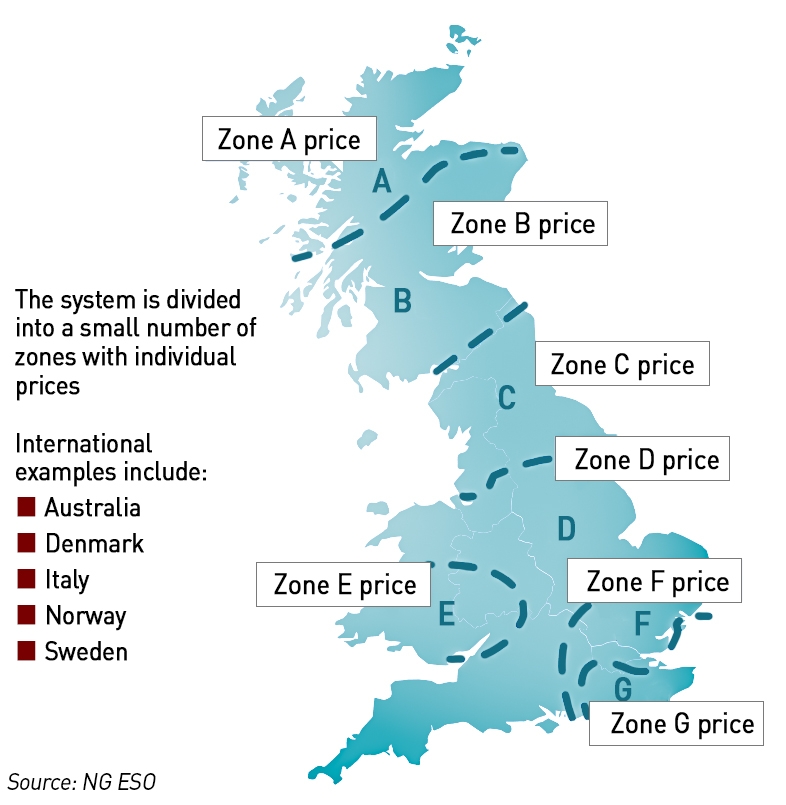

Zonal Pricing

In a zonal (or regional) wholesale market, the transmission system is divided into several zones and the wholesale price of electricity clears, for each settlement period, as a separate uniform price for each zone. The same zonal definitions are typically applied to day-ahead and balancing markets. There can be any number of price zones within a single country but in general it’s a small number – for example, Italy currently has seven zones, Sweden has four zones and Denmark has two.

When zone boundaries reflect transmission constraints, the wholesale price will vary between each zone. Transmission capacity limits between zones are reflected by variation between day-ahead energy prices for the different zones, and over time, zones that experience sustained high prices can expect to see increased investment in generation and can potentially greater investment in the transmission network to facilitate inter-zonal trading.

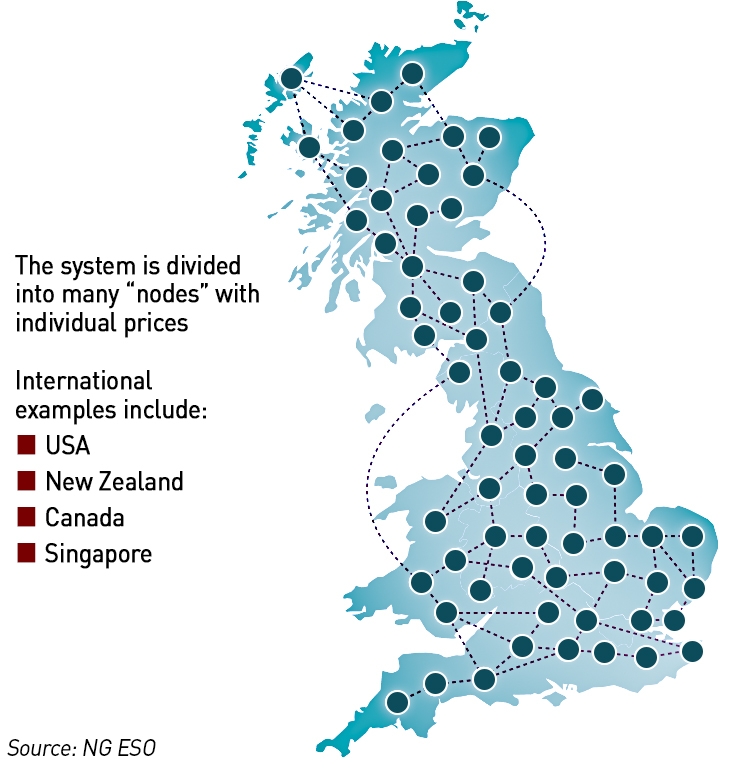

Nodal Pricing/ (‘Locational Marginal Pricing’)

In markets with nodal pricing, every transmission system injection point (such as a generator busbar), offtake point (such as a distribution substation), and transmission line intersections at transmission substations, can be defined as nodes, resulting in hundreds or even thousands of nodes, each with different prices. The price at each node reflects the locational value of energy, including the cost of the energy and the full cost of delivering it including network losses and congestion.

In markets with nodal pricing, every transmission system injection point (such as a generator busbar), offtake point (such as a distribution substation), and transmission line intersections at transmission substations, can be defined as nodes, resulting in hundreds or even thousands of nodes, each with different prices. The price at each node reflects the locational value of energy, including the cost of the energy and the full cost of delivering it including network losses and congestion.

Nodal prices are determined in real-time using an algorithm to calculate the incremental cost of serving one additional MW of load at each location subject to system constraints (such as transmission limits and maximal generation capacity). For this reason, nodal pricing is also known as locational marginal pricing (“LMP”).

Nodal pricing is used in several US markets (including PJM, MISO, CAISO, ERCOT), New Zealand and Singapore, and there are plans to introduce it in Ontario, Canada in 2023-24.

Most nodal markets require dispatching decisions to be centralised, as they were in the former Electricity Pool of England & Wales. This is also a core part of NG ESO’s proposal which would see both energy and ancillary services being co-optimised in a single centralised dispatching process.

Looking at the nodal markets in the US, they have the following features:

- Market participants engage in long-term trading in financially-settled products in order to manage their long-term electricity price risks. This is done bilaterally or on recognised financial exchanges (eg ICE, NYMEX etc);

- The system operator runs a day-ahead market which is the primary physical market which co-optimises ancillary services as well as energy. In some markets market participants can engage in bilateral trading with these trades clearing through the day-ahead market run by the SO – in some cases the prices are set by the parties and in others they are set in the pool;

- The SO also runs a real-time market which re-dispatches both generation and load to take account of any changes from the day-ahead stage. Some markets co-optimise ancillary services in the real-time market, and some do not;

- The SO provides financial instruments that allow market participants to hedge the price risks between nodes on the system. These effectively allow transmission rights or congestion charges/benefits to be traded between parties.

In the day-ahead market, generators and buyers of electricity submit their offer and bid prices to the SO, which dispatches generation to meet demand on a price merit order basis, with some adjustments to maintain system operability and the minimum run-times/capacity of assets. This process is highly automated (and also highly complex in a nodal market), where algorithms replace bilateral market trading and seek to minimise the marginal cost of energy at each node.

There are some obvious challenges with location-based pricing, which I have discussed before, the main ones being, that increasing the number of pricing points will reduce trading liquidity which is already low to begin with; it is difficult to extend locational pricing to the domestic segment – people tend to object to what they see as a “post-code lottery” for pricing; and in the limit it can lead to a lot of stranded assets outside the energy sector.

“Many people on the political side are not necessarily convinced by locational pricing because you would end up in a situation where many people for example in the Lake District would be paying much less or more than people in London or vice-versa. Those regional disparities are something that as elected officials we are very aware of and don’t necessarily want to see,”

– Kwasi Kwarteng, Secretary of State for Business, Energy & Industrial Strategy

Part of the rationale for strong locational price signals is that generation and demand will seek to co-locate. However, in practice, this does not appear to happen: renewables generators want to locate where they can optimise output, regardless of the relative location of demand, while large energy users such as industry have a wide range of factors to consider when selecting a location with access to staff and telecoms connectivity being often of greater importance than energy costs. And in the aforementioned limit, it such industries did re-locate to the north of Scotland where the proliferation of wind generation would likely result in lower electricity prices, new homes and schools and hospitals would need to be built for their staff. And what then of the homes and schools and hospitals they leave behind?

“The way that TNUoS is designed encourages generators to locate close to the demand. This was appropriate for a fossil fuel-based system but now leads to disproportional charges by locations as we move to a renewables-based system,”

– Scottish Renewables in written evidence to the House of Lords Industry & Regulators Committee enquiry into Ofgem and net zero

Renewables generators in Britain already object to the relatively weak price signals in the existing market framework saying that they raise costs and dis-incentivise investment in renewable generation, potentially undermining net zero ambitions. A nodal pricing system would exacerbate this problem.

“Ofgem sets out a commitment to protecting consumers’ interests, but its network charging agenda (which ostensibly seeks to encourage the development of energy assets in locations close to major UK demand centres, minimising the cost of grid maintenance as a result) disincentivises the development of renewable assets in locations of the UK which are most suitable to host these assets, with regards to natural resource and planning (as most are located far from major demand centres).

Ofgem’s suite of network charging policies are therefore incentivising the development of less efficient forms of energy generation at the expense of more efficient forms of energy generation, e.g. onshore wind, one of the cheapest forms of energy generation,”

– Independent Renewable Energy Generators Group in written evidence to the House of Lords Industry & Regulators Committee enquiry into Ofgem and net zero

Evidence that nodal pricing reduces congestion is limited

The oldest US market with nodal pricing is Pennsylvania, New Jersey and Maryland (“PJM”). A recent report by the system operator into the impacts of the energy transition on the grid highlighted a need for market reform, since the current market design “procures less than a third of the reserves needed by the system and, with an average clearing price of $0.02/MWh, it also fails to send long-term market signals to incentivise flexibility”. The system operator is concerned that without market reform, it may be difficult to secure the levels of storage needed to support a high renewables system.

PJM has a relatively low amount of renewable generation – California’s nodal market has managed to deploy a larger amount of wind and solar, meeting 24% of electricity demand (solar: 13.2%, wind: 11.1%). California has relatively more solar compared to wind than other markets – in GB there is roughly five times more wind than solar capacity.

The data may suggest that the solar market might be better able to respond to locational price signals, but there are dangers with applying this conclusion to Britain where the levels of ‘sunniness’ vary significantly between the north of Scotland and the south of England. In May this year, California’s state energy officials warned of a potential 1,700 MW capacity shortfall which could lead to outages with drought affecting hydro output and wildfires threatening network infrastructure. Also in May, CAISO published its 20-year transmission plan, which identified a need for over US$ 30 billion in new network investment to support the energy transition – a step change in investment which highlights the difficulty of determining network investment signals in a market with nodal pricing.

“The assumption that low carbon generation would relocate in response to locational price signals is not supported by the evidence, although there could be a case that solar energy (both grid-connected and off-grid) is more locationally fluid than wind, hydro and nuclear,”

– Regen

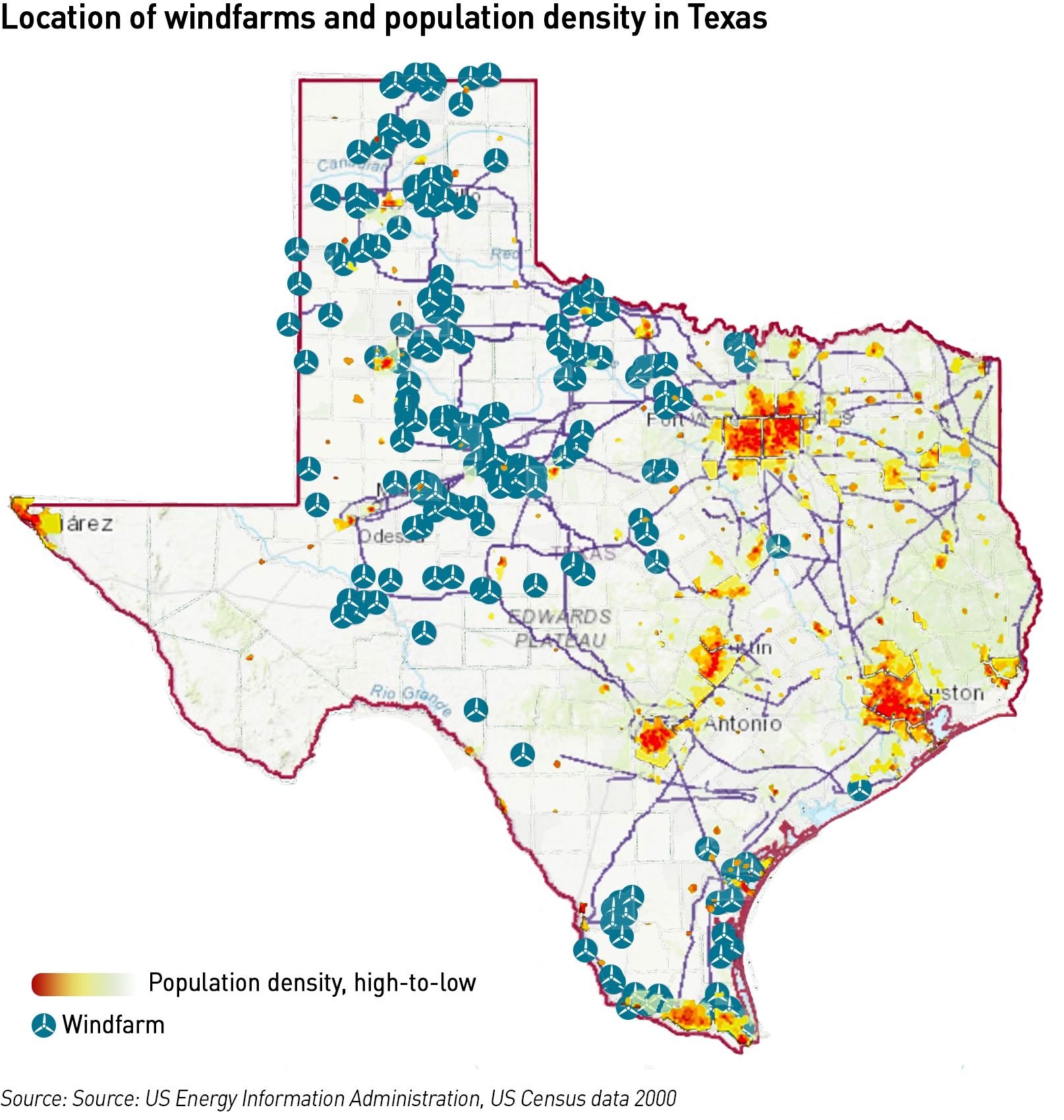

In ERCOT there are also concerns over high levels of network congestion, with congestion costs in the real-time market of US$ 1.4 billion in 2020, up 11% from 2019. Gulf coast LNG projects among others are increasing electricity demand in locations which already have high levels of industrial demand. These areas are remote from much of the new wind capacity in the state, requiring significant new transmission infrastructure.

The Texas Panhandle area continues to experience significantly more interest from wind and solar developers than was initially planned – stability challenges and weak system strength are expected to continue to be significant constraints for export from the region. The system operator is increasingly using generic transmission constraints to limit electricity flows over some parts of the network to manage grid stability.

While it is understandable that NG ESO as a network operator wants to minimise the costs for which it is responsible, Ofgem and the Government need to resist this pressure: these costs would not go away, they would at best be shifted to other parts of the energy market and/or the wider economy.

NG ESO encourages us to look at successful nodal markets in the US, but it fails to define what “success” looks like…that it is possible to create a nodal market that works in a basic functional sense (generators generate and sell electricity and consumers buy and consume electricity) is not either surprising or interesting. But the evidence that markets with nodal pricing have managed to reduce or eliminate issues of network congestion through the transition to renewables-based grids is absent.

The answer to network congestion is more network infrastructure, not locational pricing

Moving to nodal pricing might reduce network costs, but it would achieve this by moving these costs into other parts of the value chain: if costs for wind generators increase as a result of their location in windy places, those costs will be passed back to consumers, who won’t care if the cost is called a generation cost or a network cost.

The fundamental reason for network constraints is a lack of adequate network investment, which in markets of all types – uniform, zonal and nodal – is failing to keep pace with the needs of the energy transition. NG ESO even acknowledges this, saying that various stakeholders told it that “insufficient transmission network build is the fundamental cause of constraints, and this applies to any wholesale market design”.

In other markets with zonal pricing (Norway) and nodal pricing (CAISO, ERCOT and others) we see an ongoing need for major network investments. In fact it could be argued that locational pricing weakens the price signals and incentives for network investments while failing to reduce congestion by incentivising a more optimised use of existing infrastructure, leading to the worst of both worlds. There may well be a need for market reform, but a move to location-based pricing is not the answer to the issue of network congestion.

Many thanks for another interesting and well informed post.

As an engineer I agree that more infrastructure is the answer. However we should be honest about the costs of this and whether there it is a true system need or merely to open up a business opportunities. Complicated ideas by market theorists are too clever by half. Perhaps generators should be incentivised or forced by planning requirements to site in locations that require little or negative reinforcement – however system constraints will become more unpredictable if we move to a renewables based system.

Against a ‘levelling up’ background and the need to maintain a fair and equitable supply for domestic customers they should not be charged differently or extra to enable business opportunities .

There is an ongoing battle between centralised and local. Centralised dispatch is the only simple and effective way of having a fierce focus on optimising CO2 emissions. Perhaps having a centralised and engineering focused plan (specifying both generation type, location and associated infrastructure requirements) is the only way of achieving a lowest cost, resilient system and the vital goal of net zero.

Please remember that wind and solar will not only be constrained by lack of transmission capacity it will also be constrained by lack of customer demand or storage capacity.

NGSO has looked at the possible and highly complex market solutions ‘A Day in the Life 2035’ and concludes in the Executive summary that the investment required will be huge “a massive endeavour” and yet “success is uncertain”. God help us. Will the last market economist to leave turn the lights out.

I don’t think they’ll need to turn off the lights…they could well be off already!

I agree we should have some proper analysis of the relative costs of optimising the grid or optimising renewables output, but my suspicion is that it’s better to put wind turbines where it’s windy and build enough grid to move it to where it’s needed. This also has the benefit of not cluttering up the landscape with turbines that attract public opposition, or the need to buy expensive land as prices are often higher the closer to main demand centres you go.

Agreed. However we are planning to build more wind turbines than there is demand requirement or storage capacity. NGSO A Day in the Life 2035 has 150 GW of wind and solar capacity to meet a predicted demand of between 35 and 80 GW. Is that a system need or a business opportunity ? – who pays for all the idle renewable plant and back up plant when there is a feast and the back up fossil fuel when there is a famine.

I never understood how we’ve allowed so much wind generation to be connected in Scotland when the transmission system can’t move it. Furthermore SSE and SP seem compelled to agree to connection agreements for even more despite existing transmission constraints and then go to OFGEM trying to get them to agree to funding transmission upgrades who then prevaricate for ages meanwhile constraints costs continue to climb.. Whilst im not fully convinced on net zero the fact is if it is the goal then the only way it will be achieved is to plan the whole system from generation through to transmission not the piecemeal approach we have now. What do they expect to happen with zonal pricing we all move to Scotland in the winter when its windy then migrate back South to take advantage of solar power in the summer. The system needs simplifying not making it more complicated giving opportunities for entities to exploit it.

This was a deliverate policy choice known as “Connect & Manage”. Unfortunately we forgot about the Manage part.

I fully agree about not making the system more complicated – nodal pricing is hugely complex and there is no transparency in price formation.

Hello!

I have read your article, and then re-read it several times. Thank you! It is, I guess, best summarised by one of your closing remarks:

“The fundamental reason for network constraints is a lack of adequate network investment, which in markets of all types … is failing to keep pace with the needs of the energy transition. NG ESO

even acknowledges this … “

So, to the point you pose in the blog title “More grid infrastructure not locational pricing is the solution to network congestion”. May I ask:

(1) in that respect, are you satisfied by the proposals put forward by the ESO in their document set ‘Pathway to 2030’ which apparently deal with transporting power both locally in the north as well as from northern climes to the south, where most demand lies? and

(2) are those proposals substantially dependent on the locational issues/options in the network (as you discuss above)? and

(3) do you think that the planned ESO transition into the FSO, as a state -owned and -run business, is sufficient or should the government ideally add to the re-nationalisation list the Transmission Owner (another regulated monopoly business, also currently owned by NG plc)

Many thanks.

tp

“Ofgem’s suite of network charging policies are therefore incentivising the development of less efficient forms of energy generation at the expense of more efficient forms of energy generation, e.g. onshore wind, one of the cheapest forms of energy generation,”

Perhaps renewables are neither more efficient nor cheaper if they have to be built at a distance from where the demand is?

I suppose the question is whether the increased output gained by locating in a windy place provides more or less overall benefit than lower output located closer to demand. I don’t know if anyone has actually calculated this but if renewable generators want to locate where it’s windy and do so regardless of higher costs as in ERCOT then that provides some level of an answer.

Thanks, Kathryn. I’m sure it’s cheap and efficient from the generators’ perspective. Possibly not in terms of overall benefit, especially when viewed from the consumers’ perspective.

Perhaps future contracts should make the renewable generators responsible for delivering an agreed minimum energy output 24/7, giving them the problem of what to do when it’s not windy? Then the strike price might bear some relation to the real price of meeting the nation’s energy needs.

The real solution is not relying on renewables. Then we don’t have to have a grid to deliver power from remote locations to demand, handle surpluses for storage, and with 100% backup capacity that remains heavily underutilised. We must remember that National Grid in their role as custodian of Future Energy Scenarios have been pushing renewables (and electrification) because it means their business has to grow enormously to enable it, not because it is in consumer interests. This is about to become a huge factor as we move to further renewables capacity expansions and the volumes of curtailment start to soar.

NG recently announced a £54bn programme to enable the 23GW of offshore wind to meet the 50GW target. That’s over £2bn/GW on top of the cost of the wind farms for assets that will have modest average utilisation factors, and where the actual costs may prove substantially higher than the estimates. Claiming that optimisation shaves some £5bn off the total is an insult when the entire cost could be avoided.

Well there is that of course, and I agree we shouldn’t rely on renewables and in fact can’t rely on renewables if we’re to have energy security (note 2 CMNs today when wind output was low). But I very much doubt we will see a reversal on renewables, so the question is where we go from here.

NG ESO has its own particular interests and perspectives, and in some ways I don’t disagree with the approach where it aligns with their own self interest. I have the same view about Drax – I hate the biomass model, but give credit to the Drax management for getting subsidies to do something dirtier than the dreaded coal. It’s the job of BEIS and Ofgem to place limits on the self interest of various market players, not for companies to limit themselves.

I’ve been giving this year’s FES a first read through. The main reason given by NG for locational pricing is to encourage the location of storage in the right places. It’s the usual confection of unicorn assumptions of course, even if some of them have been tempered a little. We have a first estimate on the costs of the electricity system – a rather loose £280-£400bn of “investment”. For me the key page is 190. The footnote reveals: Our FES scenarios do not model specific flexibility services and model an unconstrained network, as such these graphics are indicative only and do not directly align to FES modelling and the Data Workbook. So they are still living in cloud cuckoo land. But the casual logarithmic chart is the first sign I’ve seen that they might be having to recognise the need to provide 100TWh+ of storage for a viable (or is that unaffordable?) system.

Scratching the surface I found this in their data workbook:

2021

Selected technologies

Generation type Capacity (GW) Load factor Generation (TWh)

Biomass 4.05 43.3% 15.36

BECCS 0.00 0.0% 0.00

Gas CCUS 0.00 0.0% 0.00

Gas 34.85 15.5% 47.45

Hydrogen 0.00 0.0% 0.00

Nuclear 7.64 76.2% 50.96

Offshore Wind 13.06 46.3% 52.99

Onshore Wind 13.31 39.0% 45.46

Solar 13.24 11.9% 13.79

Which bears no relation to the actual 2021 numbers as revealed e.g. in Energy Trends, which shows 108.77TWh of gas and just 35.44TWh of offshore wind for example. Fills you with confidence if they twist history more than the Met Office does the weather record.

I haven’t had the chance to look at it yet. I got a bit jaded when I looked at the historic evolution of the FES scenarios and found that in some years the actuals fell outside any previous FES ranges. I didn’t ever publish the analysis becuase I got busy with other things…I might resurrect it now, but it made me less inclined to spend time looking at FES since it makes it look like a series of largely un-related hypothetical exercises that have limited read-through into real life…