Retail market pressures continue with the news that Ofgem has confirmed this year’s record Renewables Obligation (“RO”) mutualisation of £218 million, and Elexon has confirmed the proposed record Credit Assessment Price level of £305 /MWh. There is also bad news for Ofgem as Citizens Advice published a highly critical report into its regulation of the retail market and its failure to protect consumers from the costs of supplier closures.

More cost pressures for suppliers

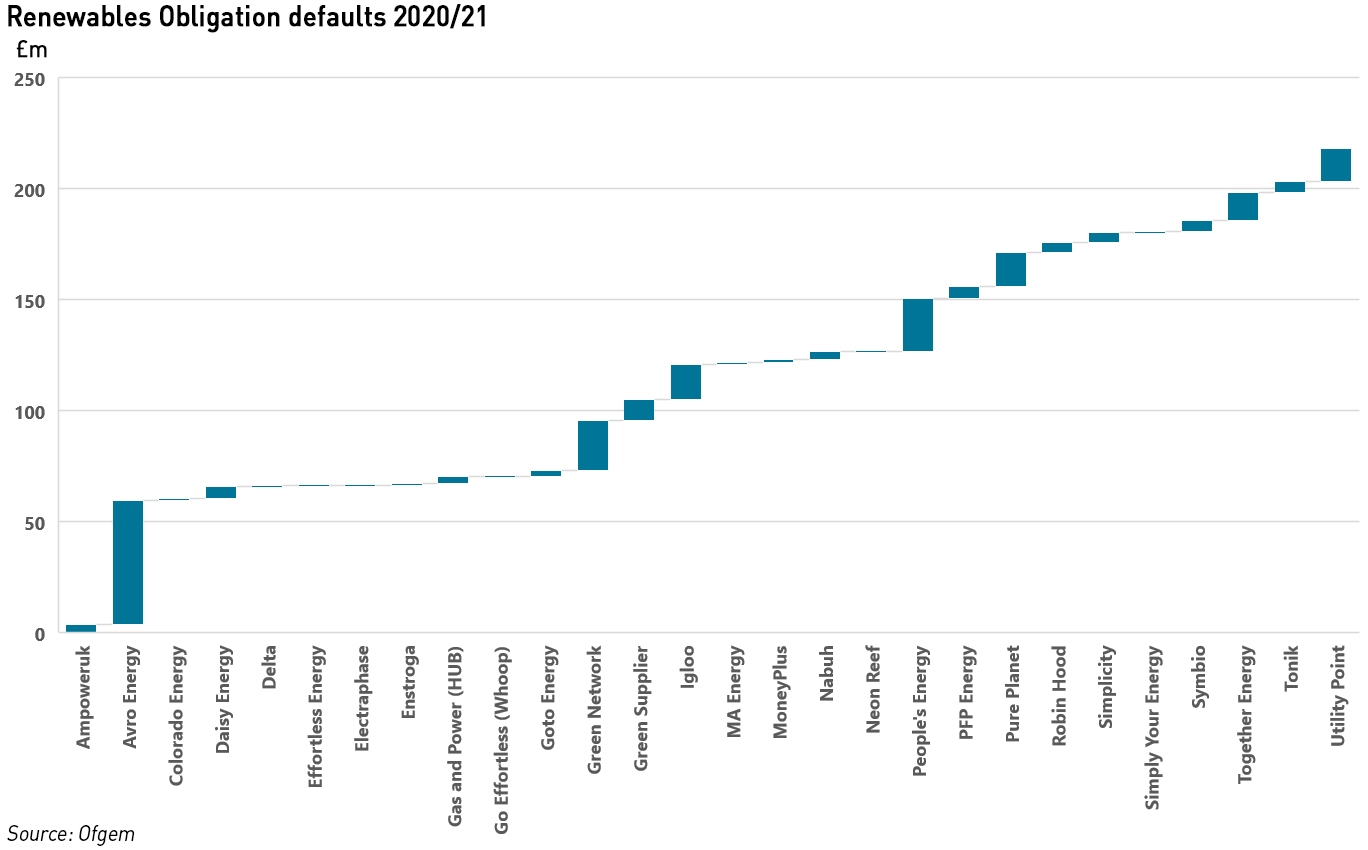

Ofgem has confirmed this year’s Renewables Obligation shortfall at £218 million for the 2020/21 compliance year, excluding interest, which is more than double the previous record mutualisation amount of £97.5 million in 2018/19. This is quite a bit above my estimate of £187 million which was based on a rough guess at what each company’s demand had been over the relevant period.

“Of the thirty-seven supplier groups across 66 obligations who failed to discharge their obligation by the 31 August and 1 September deadlines, 12 obligations were fully discharged by the late payment deadline of 31 October. The remaining 54 obligations were not met in full,”

– Ofgem

Of the defaulting suppliers, 25 are either in administration or have had their licence revoked. (Bulb was not one of the defaulting suppliers.) Ofgem cannot pursue enforcement action against suppliers which have ceased trading and had their licence revoked, but it can try to recover outstanding payments through their bankruptcy processes. However, the RO legislation does not provide for payments received after the late payment deadline, which means that the amount to be mutualised is calculated with reference to the shortfall at the late payment deadline of 31 October. Any payments made after the late payment deadline are re-distributed separately.

The bad news for suppliers is that they have to find the money for these mutualisation payments – even the most prudent suppliers were unlikely to have budgeted for something double the previous record, and will have had to start setting aside provisions while high market prices began to bite. One of my regular readers made a very good suggestion around this: unlike renewable generators receiving CfDs, those with ROs have been earning windfall returns from the current high power prices, to a point where the subsidy is unlikely to be necessary to support their project finance.

Why not cancel a portion of the 2020/21 RO payments to generators, or claw it back through a windfall tax, in order to insulate suppliers from the costs of mutualisation. RO generators could be guaranteed an income no lower than if the market price rises had not occurred in order to avoid harming investor confidence, and suppliers would be protected from a cost which is outside their control to manage or even meaningfully predict.

Unfortunately such sensible action seems unlikely. In addition to finding the money to cover the RO shortfall, suppliers have also been hit by the news from Elexon that the Credit Assessment Price and therefore the amount of collateral they must post, is going to be raised to on £230 /MWh to £305 /MWh from 17 December.

Elexon consulted on the proposed change last week, and while three respondents disagreed with the proposed value, the Credit Committee decided to do ahead with the increase. The Committee considered the consultation responses without holding a Credit Committee meeting, so the implementation of the increased CAP value would not be delayed – it plans to discuss the responses in detail at the next meeting, which will be held during in the week beginning 13 December 2021.

Damning report from Citizens Advice piles pressure on Ofgem

Citizens Advice has published a report into the crisis in the retail energy market, criticising the way in which Ofgem has regulated the industry for the past decade. The report not only highlights failures of regulation but also of supervision: the number of Ofgem staff working on enforcement fell by 25% in the past 4 years despite record numbers of suppliers in the market, and Ofgem ignored 10 separate warnings from Citizens Advice over Avro Energy, the second largest supplier to fail after Bulb and the largest to go through the Supplier of Last Resort (“SOLR”) process.

Although Ofgem introduced a requirement for suppliers to implement a Customer Continuity Plan in March this year, only 1 of the suppliers that failed since August had such a plan in place according to the SOLRs. Citizens Advice says there is no evidence that the suppliers that failed changed their behaviour in response to new financial stability rules introduced earlier in the year.

Citizens Advice has amassed significant evidence of rule-breaking by suppliers, yet Ofgem consistently fails to take enforcement action:

- Ofgem has never taken enforcement action over back-billing although Citizens Advice helped over 1,000 customers affected by this in the past year. The last formal investigation into domestic billing was over 5 years ago;

- Despite rules requiring suppliers to provide telephone lines for customer service, several suppliers have removed telephone lines altogether. It is over 2 years since Ofgem opened an investigation into quality of service;

- Citizens Advice has evidence of suppliers repeatedly breaking rules around prepayments and debt, but there has been no formal enforcement action in the past 3 years.

“Ofgem allowed unfit and unsustainable energy companies to trade with little penalty. Despite knowing about widespread problems in the market, it failed to take meaningful action…. An effective regulator would have seen these problems coming and acted to prevent them…”

– Citizens Advice

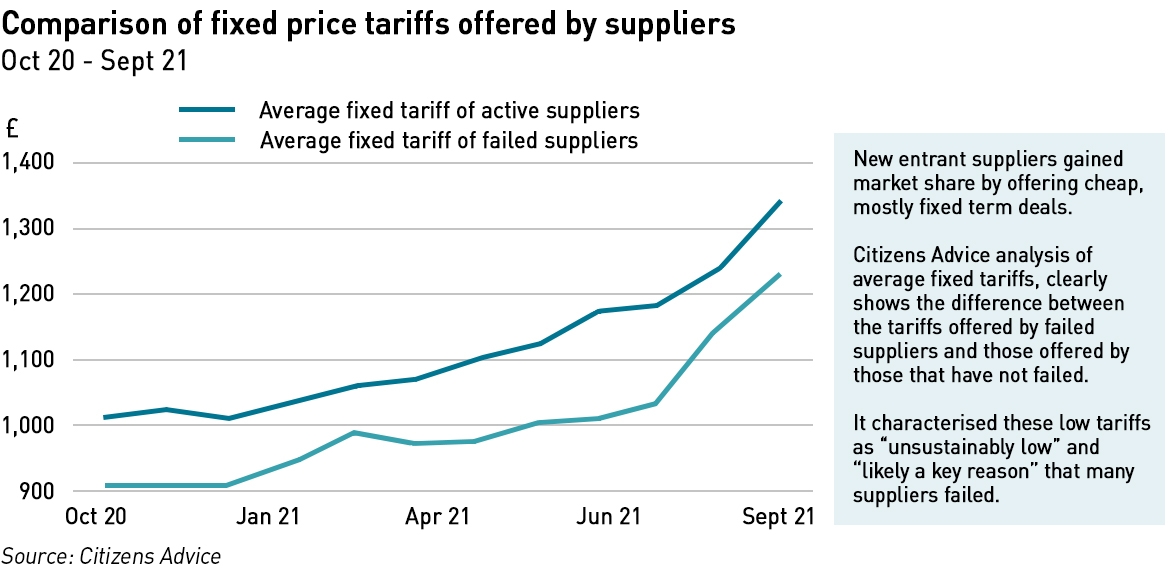

Citizens Advice estimates that supplier failures since August will cost consumers £2.6 billion, or around £94 per customer from 2022, excluding the £1.7 billion cost of Bulb’s failure. A large part of this cost arises from the habit of using customer credit balances to fund working capital – effectively borrowing from customers at no cost rather than borrowing from banks or increasing shareholder funds. Ofgem’s own analysis found that £1.4 billion was held in surplus credit balances as early as October 2018. In recent months there have been widespread reports of suppliers hiking direct debits despite accounts being in credit, and subsequently going out of business leaving those balances to be refunded by the SOLR and ultimately all consumers (including the ones whose credit balances had been lost).

The report also highlights flaws in the collection of RO payments, where suppliers make a balloon payment after the end of the compliance year rather than paying in instalments, despite this increasing the risks of default significantly. What the report doesn’t mention is that Ofgem actively prevents suppliers that want to act prudently from making regular payments.

The report makes the following recommendations that should be taken to restore consumer confidence in the energy market:

The report makes the following recommendations that should be taken to restore consumer confidence in the energy market:

- An independent review of the causes of the market turmoil which considers the role of delays in policy changes, Ofgem’s approach to compliance and enforcement, and recommends improvements;

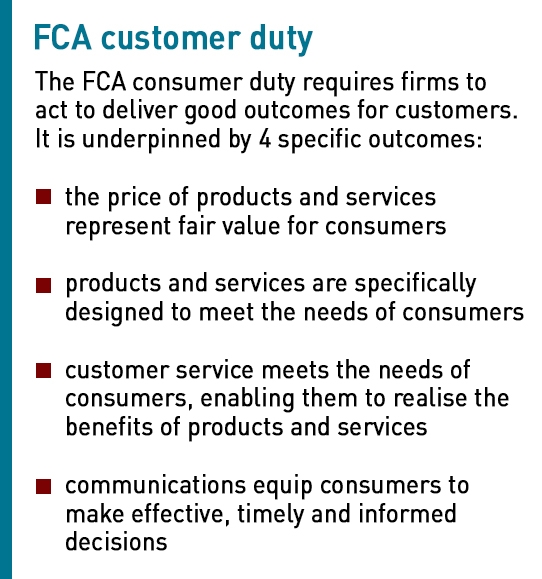

- Introduction of a new consumer duty, similar to that being introduced in financial services by the Financial Conduct Authority (“FCA”), which would put the onus on companies to ensure good consumer outcomes in future;

- Consumer protection from immediate bill hikes resulting from recent supplier failures; and

- Clear strategies for the retail market and its role in supporting de-carbonisation which consider how to enable consumer engagement and innovation in a more consolidated market.

While of course I agree with borrowing from financial market regulation, and would go further by transferring retail energy regulation to the FCA, I don’t agree that consumers should have their tariffs protected if their suppliers ends up in SOLR – this would impose un-manageable costs and risks onto the SOLR and would reduce the number of companies willing to take on the customers of a failed supplier. The better approach to protecting consumers would be to limit supplier failures in the first place by imposing the sorts of capital adequacy, risk management, skill, care and diligence, and protection of client money rules that are set out in the FCA Principles.

.

There are growing calls for an investigation into the retail market crisis and Ofgem’s role in it. But we don’t need a review to see that Ofgem has consistently failed to both create appropriate regulation and to enforce its own rules appropriately.

Time and again Ofgem has shown that it does not understand fundamental aspects of the market, and, together with BEIS, it has taken an extremely adversarial approach to suppliers. Clients and industry colleagues tell of highly burdensome information requests from Ofgem, many of which are irrelevant to their businesses, but which take significant time and resources to deliver. Like the five consultations issued recently, this is all “busy-work” – time-consuming, expensive, but not productive, particularly since this apparent oversight failed to prevent the bankruptcies of more than half of the domestic supply market.

In his recent evidence to the House of Lords Industry and Regulators Committee, Jonathan Brearley, CEO of Ofgem admits that “we have a retail sector that needs to become much more financially resilient” and sets out some thoughts on greater prudential regulation. But at this point, surely the obvious solution is to engage an organisation that already has the expertise and the systems and process in place to deliver prudential regulation, specifically aimed at capital adequacy and risk management?

Rather than wasting time on yet another review into the market, the Government should take decisive action, removing retail market oversight from BEIS and Ofgem to the FCA and the Treasury. Perhaps that will inject the competence and market knowledge that has been so badly lacking.

What’s in a name?

The Ministry of Fuel and Power (1942) after several iterations became The Department of Energy and Climate Change – both elemental titles stating a clear direction. This then became the the department of Business, energy and Industrial Strategy – whose direction is unclear but seems to be encouraging business opportunities at home and overseas.

The Office of Electricity Regulation (1989) became the Office of Gas and Electricity Markets. Regulation disappeared from the title (and the role) and they became the uncritical peddler of a particular narrow market theory. Electricity and Gas were lumped together because in their market world (where the real world of engineering and science are not a consideration) they are the same.

Now Citizens Advice (whose name suggests their main focus is on consumer interest) has stepped in acting as OFGEM’s regulator.

What an expensive mess – but never mind its keeps many professions in well paid employment.

I don’t think OFGEM’s responses to criticism announced today really begin to address the issues deeply enough.

https://www.current-news.co.uk/news/ofgem-unveil-stress-test-for-suppliers-after-cascade-of-collapses

Frankly it is a farce to have different regimes for tiny suppliers with under 200,000 and under 50,000 customers. Your repeated suggestions to get rid of all the green support programmes triggered by those levels and park them elsewhere if needs be must make much more sense. Requiring businesses to be scaled such that they can take on necessary hedging programmes, including being adequately capitalised, and having a large enough market share to be able to tailor hedges to demand shape is surely obvious. Any business not able to manage that should be required to contract for the service of balancing between monthly futures and half hourly balancing. They need to force mergers among the smaller suppliers to give them adequate scale. I note they are concerned to protect RO payments to subsidised generators, rather than think about consumers.

Adding insult to injury, I see they are launching tendering for the next round of interconnectors. We have Moyle and E-W on restricted/zero export to the UK, IFA1 now out until next autumn and not fully back until next December, IFA2 had a sudden outage yesterday (albeit it was importing to France at the time), and NSL, not content with extending its 700MW export limit until end December in order to protect Norwegian hydro reservoir levels now expects to remain limited to that level until at least mid February because of problems with thyristors at Blyth. The day ahead price is over £400/MWh for tomorrow on Nordpool as wind output dips. Do they really think interconnectors are reliable?

I’m wading through the mountain of consultations Ofgem has just published…talk about the Grinch that stole Christmas – suppliers will have the joy of figuring this out and getting their responses in by 22 January.

The 200,000 customers threshold makes even less sense when you realise that the trigger levels for ECO and WHD were reduced to 150,000 customers!

So far I’m reading a heap of additional reporting requirements – Ofgem already gathers A LOT of information from suppliers but somehow failed to see the crisis coming. It also plans to actually enforce some of its rules on adequate resourcing, which most people would have assumed it was doing anyway – isn’t that a fundemantal part of the job of a regulator?

Stress testing and other prudential regulation makes sense, but do we believe Ofgem has the skills and experience to properly design these stress tests? And the proposals for a new set of short-term interventions just increases the distortions from the price cap when removing the cap, or at least adjusting it more often, would be a better solution.

On interconnectors, I’m hoping to do some analysis of Norway’s interconnectors. Norwegian hydro levels are not looking particularly healthy and there are clearly limits to the ability of the system to actually balance all of N Europe. The plan that Norway would import cheap renewables doesn’t seem to be materialising. Apart from the NSL limit, the other interconnector restrictions are all good for GB as they stop us exporting when domestic demand is high, something we do far more than anyone in any kind of position of responsibility seems to understand. I was positive about the previous IFA outage for this reason, and nothing has happened since to change my view… (the question isn’t whether interconnectors are reliable, although there clearly are some issues there, it’s whether they can be relied upon to be IMPORTING when we need them to!)

The trouble is that BEIS and OFGEM seem to think that interconnectors are a substitute for dispatchable capacity. Anyway, it seems I got someone’s attention…

https://twitter.com/johnredwood/status/1471398244156645378

On Norway I would recommend reading Roger Andrews’ analysis of its potential as a balancer here:

http://web.archive.org/web/20160801042131/http://euanmearns.com/how-much-wind-and-solar-can-norways-reservoirs-balance/

The archive version retains the original figures and diagrams. See also lively discussion in the comments involving hydro engineers. There are also a number of posts at P-F Bach’s site that include valuable insights.

http://pfbach.dk/

I made a number of points in this recent WUWT post:

https://wattsupwiththat.com/2021/12/13/norways-power-surplus-disappearing-rapidly/

Hi Kathryn – loving the blog post as always.

One question I have is why monthly fixed Direct Debits (and credit balances) are even still allowed for consumers who have smart meters?

If I want to get a mobile phone contract (which is also a usage-based pricing model in principle), the mobile network supplier will run a credit check on me, sign me up to a contracted rate-card for the various different call types, charge me (by Direct Debit) specifically for what I’ve used each month, and report my payment performance to the credit rating agencies.

Isn’t this is how smart-meter-based electricity and gas retail supply should work? I’m curious if you know how other countries with smart meters price their energy supply products in the same way.

I get that a fixed monthly DD allows consumers to smooth out the costs of their high usage in winter and low usage in summer, but consumers with a decent credit history and good ability to pay shouldn’t have to keep credit balances (which earn no interest or return) with their energy supplier. I’d even venture that a pay-only-for-what-you-use pricing model may incentivise such consumers to become more energy efficient during winter.

On top if it all, the monthly fixed DD approach is so confusing for the average consumer. My Mum bases her energy deal performance on the amount of the fixed monthly DD, when it’s the tariff’s usage charge and standing charge she should actually be focusing on… I know quite a few people who think like this, which I think is a shame.

The main difference between a phone contract and an energy contract is seasonality – people use more energy in the winter but probably don’t make more phonecalls/use more mobile data in winter. But for most people they don’t earn more income in the winter, so fixed monthly payments allow them to spread the cost of their energy use evenly through the year to match the way they get paid. I think the majority of people would find this useful – yes, they pay more in the summer and build up a credit balance, but then they pay less in the winter and use up that credit balance.

The alternative would be paying less in summer and more in winter which could make affordability more difficult just around Christmas when there are many other expenses to consider. I’m afraid I don’t agree with your point about incentivising lower consumption in winter – for households on low incomes, energy is already difficult to afford and you run the risk of people self-disconnecting. Thousands of people die from under-heated homes in the UK alone each winter – we need to be very careful not to fall into the trap of viewing consumption choices through the lens of affluence and privilege.

The fixed DD is also cheaper to administer – if you paid monthly based on actual consumption per month both the customer and supplier have to take steps to manually process the payment and ensure it is correct. This is one of the reasons suppliers might charge more if you opt not to have a DD. Although the tariff should be the main value indicator for consumers, there should be a good correlation between the DD amount and the tariff if consumption inputs are hed constant, so it’s not a bad way of looking at it. Because of the interplay between standing and variable charges, tariffs can be difficult to compare, so the annualised cost (or monthly equivalent) is a good metric for comparison.

Unfortunately, the DD approach is open to abuse, with a temptation for suppliers to use credit balances for working capital. Ofgem is looking at this, and it shouldn’t be difficult to limit the amount of credit any customer can be allowed to build up and require suppliers to ring-fence customer money.

I absolutely agree that under no circumstances should a payment model disincentivise essential use of energy. I guess the economist in me just despairs that energy bills are too complicated to dissect for most people, with many conflating the fixed DD (or payment ‘statement of account’) with the cost and volume of energy they’ve used.

I’d also suggest representing tariff comparisons as straight line graphs (x being kWh consumption, y being total annual cost, the gradient being the usage charge, the y-intercept being the annual standing charge) so it was easier for consumers to visualise. The fixed DD figures are not in my experience a very good barometer of how good a tariff is – you need to know the slope of the line to decide how much price risk/certainty you want to take. It all feels so unnecessarily opaque for the average joe and I genuinely feel the fixed DD is something the retail supply market uses to bamboozle consumers.

On low-income households: my assumption when I wrote the comment above was that the low-income households would be most likely to have a prepayment meter (and therefore directly feel winter costs much more than those on fixed monthly DDs). Genuine question – is there not a strong correlation between households in fuel poverty and households with a prepayment meter?

Also, I wasn’t suggesting replacing fixed DDs with varying manual payments. DDs can be variable – for example my mobile phone DD and my credit card DD charge my bank account a different figure every month. My assumption was that a variable DD wouldn’t be significantly more complex or costly to administer than a fixed DD (as the figures they need to charge already appear on bills).