The Capacity Market was introduced with a very clear and sensible objective – to ensure that Britain would always have enough firm capacity available to meet demand, even under stress conditions (particularly periods of low renewables output) by providing revenue certainty that would support both new investment and the retention of existing generating plant.

Essentially, it’s an insurance mechanism for the electricity system, and like any insurance policy, its value lies not in normal conditions, but in the extremes: those cold, still winter periods when demand is high, renewable output is low, and the system is under genuine strain. The problem is that the way the market is now being run looks more like a cost-optimisation exercise built around optimistic assumptions and a bias in favour of supporting official policy narratives, rather than a robust assessment of worst-case system needs. The latest T-4 auction suggests that this gap between theory and reality is widening.

The capacity market design no longer matches physical reality…

At the heart of the design is the distinction between the T-4 and T-1 auctions, with the former intended to secure the bulk of capacity four years ahead of delivery and the latter acting as a relatively minor top-up mechanism closer to real time. The choice of a four-year horizon reflected the typical real world construction period for new gas fired generation at the time the market was created. A CCGT can be built in about 18 months from breaking ground to commissioning, with additional time built in for permitting, securing supply chains, and other practical scenarios that mean plant is rarely built in line with the fastest possible timetable.

The T-4 auction is not just a procurement exercise, but an investment signal indicating the need for new capacity. Indeed the market was created with an intention to secure new large gas generators – it has completely failed to do this (the only newbuild CCGT – Carrington – delivered to date with a capacity contract took FID before it even entered the capacity auction, so was not dependent on securing a contract).

However, the four-year structure also means that any errors in the assumptions underpinning the T-4 procurement target are locked in for the medium term, because the system has very limited ability to correct for them later, and certainly not at scale. The T-1 auction cannot compensate for a shortfall of several gigawatts of firm capacity; it can only fine tune around the edges.

This makes the choice of procurement target critically important, and it is here that the recent auction raises serious questions.

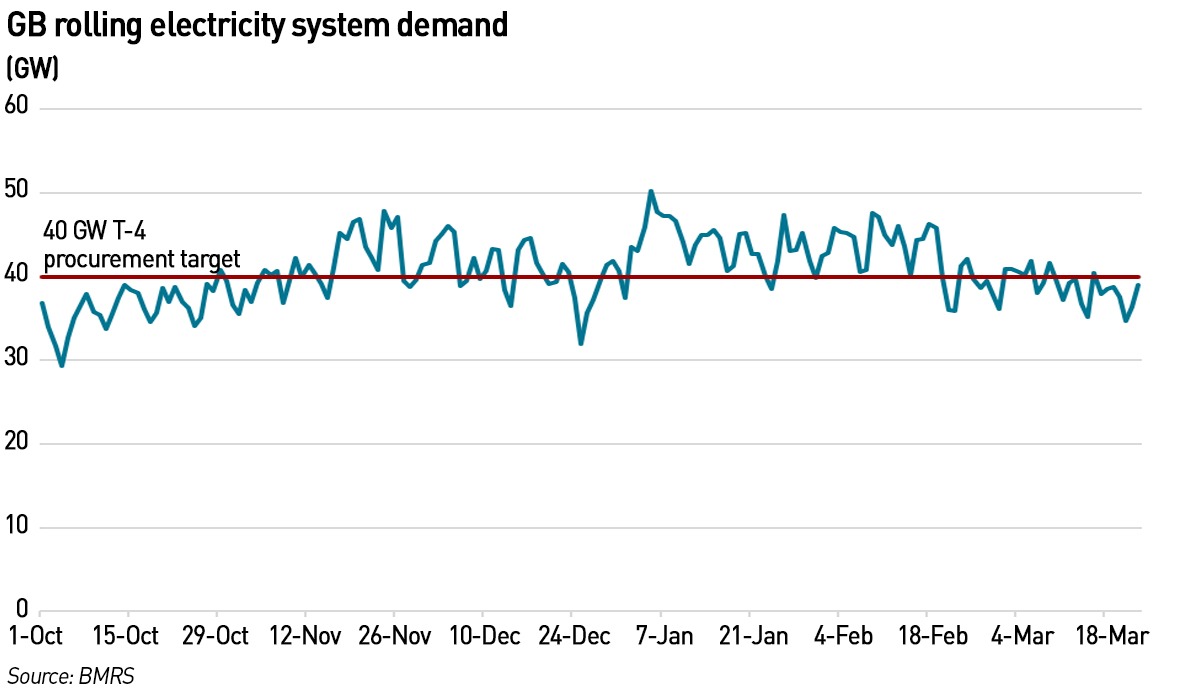

The most recent T-4 auction procured just over 40 GW of capacity against a target of 39.4 GW, with around 44 GW entering the auction at pre-qualification stage. Yet typical weekday peak demand this past winter was around 45 GW with the highest transmission system demand seen in Winter 2025/26 of just over 50 GW. A 40 GW T-4 target doesn’t even secure typical daily peak winter demand, never mind the expected demand in a period of system stress. With actual transmission system peak demand this winter over 50 GW, why was that not the auction target?

Of course only 44 GW entered the auction but it’s entirely possible for the capacity market to procure the entire pre-qualified stack – effectively there is no auction and capacity is awarded at the price cap (the reserve or “maximum clearing price”). This has happened before. A least this would have mostly covered the typical weekday peak.

But even 44 GW is completely inadequate. Not only does it fail to cover the actual peak demand, but it assumes there is no electrification. NESO’s Clean Power 2030 analysis assumes electrification will add around 11% to electricity by 2030 based on the 2023 peak demand (for the total system not just the transmission system) of 58 GW ie an increase of over 6 GW and data centres another 6 GW based on Government projections. So in 2030 NESO and DESNZ think peak demand will be 70 GW. So why are they only procuring 40 GW of capacity in the capacity auction for 2029/30?

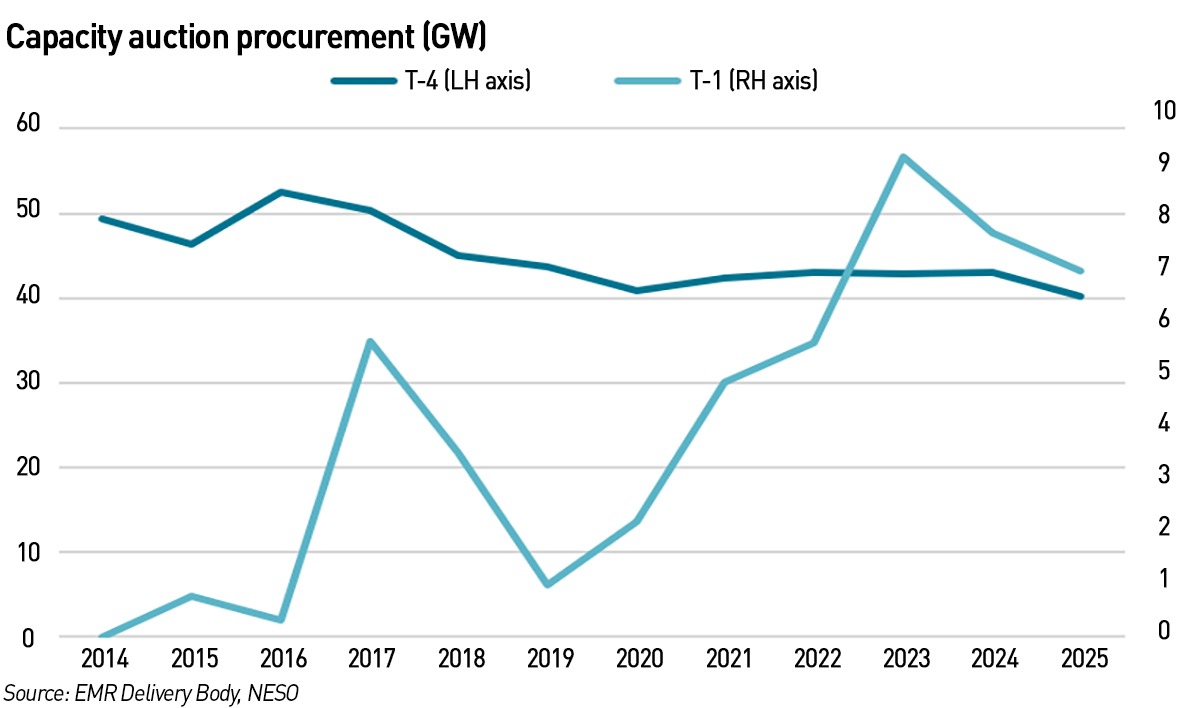

In fact, the capacity being secured in the T-4 auctions is falling. This implies that, despite the projections around electrification, the Government and NESO think demand is going to fall. This is consistent with what has been observed on the grid as deindustrialisation has been the dominant demand driver ahead of electrification, but it is not what policy is trying to achieve. Nor is it necessarily credible that we will see demand destruction on this scale.

Here is some low level building of capacity once previous auctions are added – the 2029/30 total is just over 50 GW, far short of the 70 GW NESO and DESNZ apparently expect by 2030.

Or they are assuming renewables will make up the difference. But that logic would undermine the very purpose of the capacity market….the whole point of the mechanism is to ensure system adequacy during periods when renewable output is minimal – those cold, still winter days when demand is high and wind output is low (and there is zero solar in the evening peak as it’s after sunset). If the system is assuming tens of GW of renewable output in those periods, then it’s effectively contradicting its own founding assumptions of ensuring there is enough generation available to cover periods of low renewables output.

Alongside this sits further uncertainty in the form of construction and delivery risk associated with new build and refurbished assets that have secured contracts but are not yet operational. The four-year lead time of the T-4 auction is intended to mitigate this, but in recent years, supply chains have extended. The lead time for a new gas turbine is now 7-8 years, meaning and developer would need to bet 3 years ahead of any auction that it would secure a contract. There is no evidence that this is happening, which is not surprising, since any new large gas generator would need the certainty of a capacity contract to secure the financing it would need to go ahead with its project, and it’s unlikely to place (or have accepted) an order for expensive equipment on a speculative basis.

The situation with Drax further underlines the risks developers take – it built 3 OCGTs in time for the start of their capacity contracts in October 2024. However, only one has opened, having recently been commissioned, because the grid connections weren’t built in time. Despite having zero control over this, developers face the full risk of delivery. Unless you’re a windfarm where Connect & Manage allows windfarms to be built despite knowing most of their output cannot be used. For example, Seagreen which opened in October 2023 – in 2024 67% of its output was curtailed, rising to 75% in 2025. A total waste of consumers’ money.

The market needs to be redesigned to take account of longer lead times for key equipment, and potential delays to grid connections, bringing better alignment, and ensuring developers of dispatchable generation are not exposed to unreasonable levels of risk. And procurement targets need to be realistic.

…and the wrong type of capacity is being procured

The composition of the capacity that has been procured compounds these concerns, because a growing share of it is not firm in any meaningful sense, even if it is treated as such within the market design. In particular, the increasing reliance on interconnectors and unproven demand-side response introduces a degree of conditionality that flies in the face of what the market is intended to achieve.

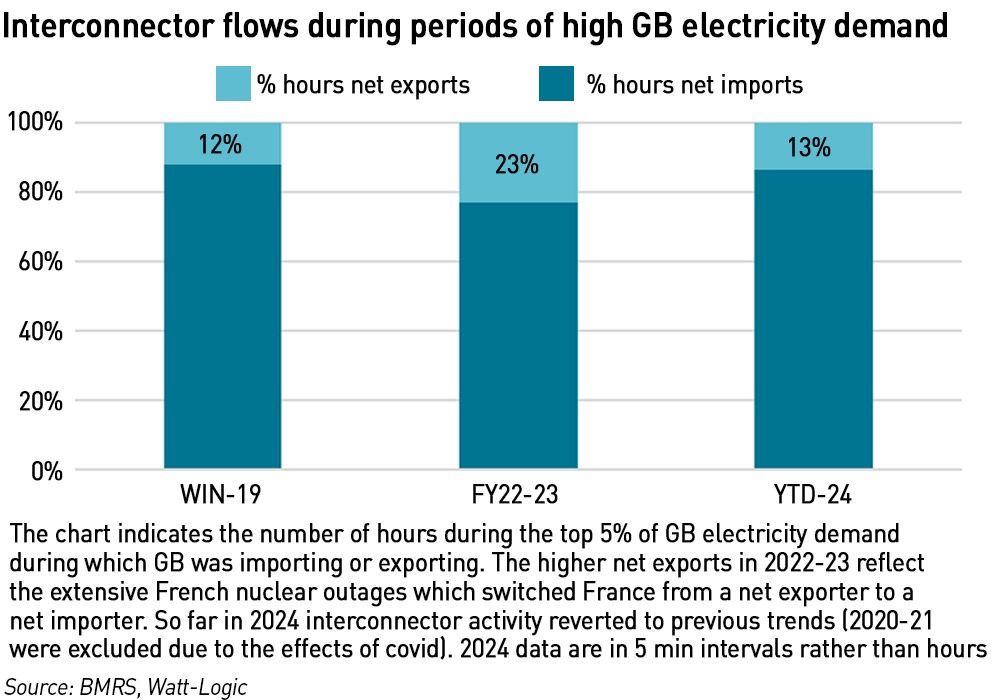

Interconnectors are generally counted as being equivalent to domestic generation, but they are fundamentally different: they do not create energy, they simply allow it to flow between markets. In a stress event, the UK can restrict exports, but it cannot compel imports, and if neighbouring markets are themselves tight, which is entirely possible given the high weather correlation with most of these markets, then the assumption that interconnectors will deliver power into Britain becomes highly questionable.

In fact, my previous analysis shows that at times of high demand in GB, we’re often exporting. France has a more weather sensitive electricity system than we do since electric heating is more widespread, so when temperatures fall, electricity demand rises faster than in Britain where gas dominates heating.

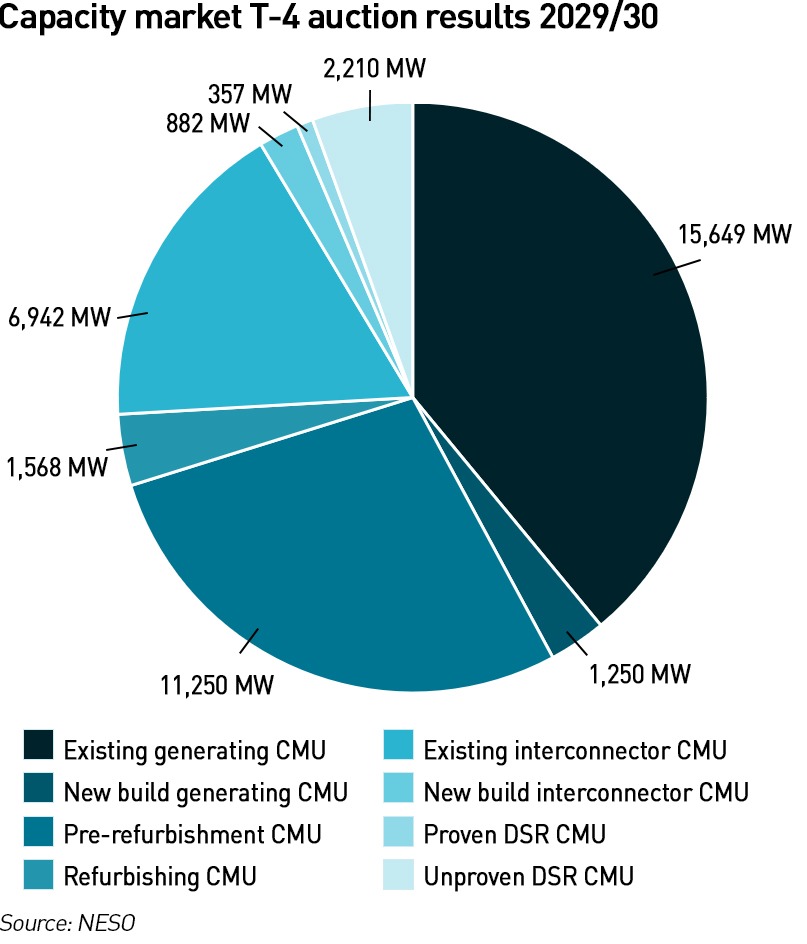

Yet interconnectors accounted for 20% of the capacity awarded in the most recent T-4 auction.

Unproven demand-side response raises a different set of issues, but creates similar lack of certainty. These resources are, by definition, not yet demonstrated at scale under real system stress, and often rely on behavioural assumptions about how consumers or businesses will respond when called upon to reduce demand. While there is clearly some value in demand flexibility, particularly for short-term balancing, it’s much less clear that it can be relied upon to deliver sustained reductions during prolonged stress events, particularly as those events can coincide with periods of high economic activity or extreme weather.

Treating such resources as fully equivalent (on a de-rated basis) to dispatchable generation risks overstating the amount of genuinely deliverable capacity on the system, and the more heavily the market leans on them, the greater that risk becomes.

Unproven DSR secured 5% of the capacity in the lates T-4 auction, far more than the 1% secured by proven DSR (2,210 MW versus 357 MW) indicating that the market is increasingly favouring lower-cost, higher-risk capacity over demonstrably deliverable capacity. This is a real problem – unproven DSR has secured a non-trivial share (5%) of total capacity, despite having no operational track record, while proven DSR which has demonstrated delivery capability accounts for much less of the total capacity awarded.

The capacity market is a price-clearing auction where lower-cost resources are naturally favoured. Unproven DSR can bid at lower prices because it has lower capital requirements and less exposure to construction risk. But that doesn’t make it lower risk from a system perspective – on the contrary, it shifts risk from investors to the system operator, and ultimately to consumers, because the penalty for non-delivery is not necessarily high enough to guarantee performance in a genuine stress event.

Together with interconnectors, highly uncertain technologies account for a quarter of the capacity awarded. This is a huge proportion, particularly when the low procurement total is taken into account. This can result in a system that is not only tighter than it appears, but also increasingly dependent on capacity that simply might not materialise when it’s needed most.

.

What emerges from all of this is a system that appears adequately supplied on paper, but is significantly more constrained in reality, particularly under stress conditions. A procurement target that is too low, combined with a growing reliance on capacity that’s either conditional, not under our control, or not yet built (and may not be capable of being built or connected in the available time), creates a false sense of security over actual system adequacy. This is not an abstract concern, but a structural issue in how security of supply is being assessed and delivered.

A more robust approach would start from the recognition that the purpose of the capacity market is not to minimise costs in the central case, but to ensure reliability in the tail of the distribution, where the consequences of failure are greatest. That would imply a higher procurement target, more closely aligned with historical peak demand and forward-looking estimates of growth, as well as a much more conservative treatment of interconnectors and unproven demand-side response. It would require a clearer focus on securing genuinely firm, dispatchable capacity, even if that comes at a higher upfront cost.

And the market needs to take account of actual real world delivery timetables. If supply chains have lengthened, the auctions must be held earlier than 4 years ahead of delivery so that developers are not excluded by an expectation they would not be able to deliver on time and would incur penalties.

The capacity market was introduced to ensure that firm generating capacity did not leave the market when utilisation rates were pushed down by renewables, so they would be available to run on low wind, low sun days, and that new firm capacity would be built to cover increased demandfrom electrification or retirement of aging plant.

But there seems to be a growing reluctance to properly pay for this, fudging the issue with interconnectors and unproven DSR which is cheaper to procure but may well not deliver. Capacity that might not deliver in a system stress event has no place in a capacity market.

And setting procurement targets far below any realistic view of actual demand in a system stress scenario makes even less sense. This market will get tested at some point and is likely to be found lacking. The Iberian blackout taught us that lives are at risk when system adequacy is compromised, and the economic costs are significant, so this should not be taken lightly.

NESO and DESNZ need to explain why the procurement target is so low compared with actual realised demand and their own demand growth targets. They need to re-evaluate the reliance on uncertain and unproven technologies, and they need to better align the timetable with real world supply chains constraints. And Ofgem needs to ensure that the market is being run in a prudent way, avoiding undue complacency.

All very good questions. Look forward to

Reading the response

What concerns me more than the inevitable rolling and total blackout/s we are facing is that, this Government is totally against seeking advice from industry experts who actively support a different viewpoint, and this lack of understanding that advice from both sides will inevitably lead to a intelligent discussion and a range of solutions that will protect the integrity of the Grid – this stupidity is not just limited to Labour, Conservatives, LibDems, SNP the whole damn lot are supporters of economic destruction whilst calling it Green Jobs Growth.

Unfortunately the only way that this message will get thru is a total collapse of the Grid, leaving millions in the dark for weeks- but, and this is not even funny, the Green Energy mob will claim that MORE intermittent wind and solar will mean more energy produced……..and so it will go on.

All this is now academic. Global Oil and gas markets are short and expensive.

How about looking at the realistic scenario for the winter of 2027?

Power-cuts , Rationing and 3 day week me thinks!

Oh dear. And I thought there were boffins out there doing robust calculations based on real data with a knowlege based on future demand and well known and understood weather patterns. I can’t see massive reductions in demand for domestic heating and I think the efficiencies of heat pumps are overplayed. An averaged COP for the whole year is meaningless. You need to know what it is on those very cold still nights in January. As you very correctly say, the issue at hand is how we deliver sufficient energy to industry and peoples homes at the worst of times. From what I read, nothing practical is happening. No wonder people want to hang on to gas. As someone off the gas grid, who has used off peak electricity for home heating for over 40 years, partly just because of my gut feel and, more because of your analysis, I will be filling the coal bunker this year.

These issues have been raised ever since Amory Lovins sketched his famous graph that “proved” that fossil fuels could be completely replaced by “renewables”. They continued to be raised when the magic accounting concept of LCOE was conjured. The response from the renewable community, then, as now, is that something magic will occur, and no one should talk about it because that sort of talk does not advance the climate change narrative. I.e., shut up.

Everyone likes to have extra margin built into their systems, to account for uncertainties, but no one wants to pay for it. This goe, in spades, for “renewable energy”.

Kathryn,

Brilliant, as usual.

Why are you not in charge of this??

Is there not a case to actually scrap the capacity market anyhow its never been called upon and is failing to procure firm dispatchable capacity and now seems like another hidden subsidy for the battery lot and DSR?

Also you didn’t specifically comment on the clearing price being over half of the last years T-4. This surprised me as the usual CCGT suspects stayed in the auction so are happy to sit around for another year being used even less by this delivery year at that rate. They of course can chose to pull out at anytime with no penalty before the delivery year I believe if they dont like the economics. Thus they could have an even bigger hole to fill at T-1 and maybe some of the nukes will be still be able to enter otherwise they wont have much left in the pot.

Anyhow you’ve plenty of pertinent issues but whether NESO or OFGEM will do anything with it is unlikely.

Good job Kathryn. A very good summary of the risk this country is sleepwalking into.

Not sure we can rely on Ofgem to make sure the market is run in a prudent way – they only have 2700 staff !!!!. They have all these staff gainfully employed in the price cap which is a useless smoothing mechanism anyway, so surely we cant hope that they would actually do anything useful like ensure there is acceptable risk in the capacity market.

The trouble with being a total pessimist about everything, all the time ,is that you end up being ignored.

– Octopus is financially unclear

– Ecotricity is failing

– Scottish generation is a timebomb waiting to go off

Etc etc. Just look even at the titles of the last dozen posts. One gets the impression that our blogger is just waiting for something, anything, to go wrong anywhere, so she can say that she told us so.

But it all lacks balance.

Can you tell me tje amount of sun and wind we will get over the next 5 years.

Looking at past data to spot trens will be highly risky

As usual a sensible, reasoned and competent piece from KP. One day the unqualified eco-maniac called Milliband might eventually realise the error of his destructove ways, but by then the damage has been done and we will br in very serious trouble.

Almost the sole benefit of democracy is the finite life of a government. Your detailed analysis falls of deaf ears now, but will be validated in the time scale you discuss.

Weather-reliant renewables require firm capacity to cover worse case demand, so we are paying for two generating systems. Wind and sun are free, but so is oil, gas and water. Extraction and distribution are expensive for all energy.

If we want to reduce CO2, which is plant food through photosynthesis, then nuclear is the solution. If we accept some CO2, then our own secure North Sea gas is the solution.

Thirty years of renewable subsidies underline that they are not viable or stable solutions in UK weather conditions.

Well written and thank you, Its intelligent people like you who know their stuff that keeps the pressure on those in power, unfortunately they appear to not be listening. Unless these people wake up to reality our country is doomed.

For the benefit readers not “au fait” with energy industry jargon, a brief explanation of T-1 and T-4 and how they relate to CfD rounds (e.g. AR7) would be useful. Also the acronyms FID (final investment decision) and DSR (demand-side response).

Perhaps we should not be surprised that government regulation of electricity behaves in this way. Certainly, in the USA, governments and corporations have had a long and sorry practice of overestimating returns on investment for pension funds, providing an excuse for underfunding their obligations. Of course, the private sector moved away from defined contribution retirement funding but governments have not. Most state systems are underfunded, some seriously so, while state constitutions place liability for such shortfalls on the backs of tax payers. In effect, this is a future obligation that politicians hope will be a problem long after they are gone. Optimism always reigns supreme at planning time. Politicians who build a career on denigrating the free market somehow become supreme optimists when predicting the future effects of their regulatory policies. We should not be surprised that we limp from crisis to crisis while seeming to learn nothing from past failures.

Thank you Kathryn. I take it you have pointed out these risks to the various Govenment quangos, because I’d love to see their replies.

It just seems like total madness, as we need to produce a lot more, not less electricity in the future to take into account EVS, Heat pumps, Data centers etc And, hopefully reindistrialisation, because relying on China is not a good idea.

I can only aasume that their demand reduction is based on rolling blackouts.

As usual a sensible, reasoned and competent piece from KP. One day the unqualified eco-maniac called Milliband might eventually realise the error of his destructove ways, but by then the damage has been done and we will be in very serious trouble.

So, with increasing electrification is deindustrialisation a central part of the energy policy rather than an unfortunate side effect of the world’s highest electricity prices.

How else does the capacity market balance supply and demand?

The GB capacity “market” provides fertile ground for my view that the power market experiment has failed. It is regrettable, because the idea of a market has its attractions, but when the facts change…. We need a much more radical approach to provision of power.

There was lots to complain about the CEGB, and the Thatcher government was persuaded to privatise the electricity industry. I supported this and spent a career in trying to deliver it. But, today, we are at risk of using “bad” to justify “worse”.

With the benefit of CEGB legacy assets, GB dined out on the illusion that markets could satisfy consumer demand for power. It is the decline of the CEGB legacy assets that proves that markets will not do as intended. Lots of people will yell that policy, regulation and heavy-handed interventions prevented the markets from flourished into the utopian free-market ideal. That’s an ideological position and will only make matters worse.

There is a serious mistake that consumers value only the electrical kWh, and markets should strive for kWh at lowest practicable cost , But this is completely wrong because consumes have many ways to get super-cheap kWh, and it doesn’t suit their consumption preferences. Consumers pay a value for money transaction in their power bills, an it is for SECURED electrical kWh. Markets lack the sophistication and detailed incentives to provide the “secured” part.

If the GB power market only provides electricity without the level of security consumers expect, many businesses will relocate to places where energy supply is more secure, and voters will seek to punish their governments. So it is not sustainable to see only price as the market outcome.

Kathryn has been very active in exploring and explaining what is needed for security in recent months/years. Explaining that electricity supply is technically complex. If provision of electricity supply is to be left to the market, private investors in generation would need to see the investment case for spending money on generating capacity, and the investment case for spending money on several types of ancillary and balancing services, and spending money on doing so at a particular location, and spending money on provision for fuel security, and for spending money on network security as the “route to market”.

The capacity market tries to do one of the above, and the rest comes down to hope that everything else will work out well in the long-term. But with no mechanism to create investable revenue expectations for balancing services, fuel security, etc, the private market is simply not going to spend any meaningful investment money on it. Without that revenue, private investment decisions would just see the various elements of securing supply as additional technical and commercial risk, and the best thing to do is to avoid them.

One further comment on the reluctance to procure more capacity. This is a symptom of the policy/political embarrassment that the consumer is paying twice for electrical generating capacity. Once, in the allocated CfD strike price, as the government publishes claims that CfD strike prices are competitive, when compared to their forward-looking replacement cost of (firm) generating capacity. The capacity market is a confession that CfDs do not provide the security to displace firm capacity, and the government’s comparison over-states the value of renewables (which displace energy, and therefore makes the same mistake that I first mentioned above). By keeping the procurement demand for replacement capacity as low as possible, the government is trying to hide its embarrassment.

.

We were on holiday in Portugal last year on Monday April 28th last year when the power failed for ten or more hours with no advanced warning.

We were camping in a very rural area and the consequences were far less severe than for those in towns or cities.

It will happen here we just don’t know when, or for how long the power will be off.

I guess this is partly why energy firms are trialling new and dynamic TOU tariffs like EDF FreePhase to try and learn how to manage peaks on a day by day basis.

It’s a risky game with potentially fatal consequences.

In addition to my solar panels and Tesla battery, I think I’ll plan to take an extended winter holiday somewhere warm from now on.

The UAE is particularly hot at the moment…

Thank you. A very clearly written description of future planning of our grid. Our politicians are taking a big gamble on this, and sooner or later the stack of cards will fall down.

Can’t think of sufficient adjectives to applaud the findings in these papers.

Fuels. The UK Government is encouraging the use of hydrogen by combustion in ICEs and as a fuel cell to produce electricity. It doesn’t appear to know or appreciate, Humphrey Davy’s work on catalytic hydrogen combustion (CHC) in 1816, producing heat without CO2 or H2 generation.

CHC is understood, but not applied, in other countries. Has Watt-Logic looked at it?

This is who we are, and what we are doing; https://pitch.com/v/diesel-replacement-external-combustion-engine-x4fgku

Looking forward to answwering your questions.

Philip

Sounds good Philip, but why are most of those guys so old? Really though, the system you describe does tick the boxes. As with most things in the UK, are we just going to let others convert this into a commercial product or get making them now? Also, as per the Royal Society report, which seems the state that hydrogen ICE is the answer, has there been any progress in generating and storing hydrogen? BTW – how do I invest?

I think they are using Cuba as a blueprint for the future.

Or, could we go back to the early 60’s when in January, the prefab classroon for the 11 year olds had a coke stove which was allowed to go out for the weekend at midday. By 2.30 it was getting cold, so Mr King would get us to put the desks into a square arena and put boxing gloves on a couple of boys, for an afternoons excercise and entertainment.

Thanks Kathryn – a very good piece.

From my perspective its really important to re-define capacity as “enduring capacity” – meaning capacity that is not time-limited like batteries, flexible demand (rather than demand destruction), interconnectors imports etc. If we re-defined capacity as being able to deliver with no time limit (or, say up to 2-4 weeks), then we would address some of these concerns.

In addition, as you say, we need to ensure demand levels are appropriately forecast and at the level of resiliance that the consumer is really prepared to accept, as opposed to a theoretical economic level of resiliance.

Finally, its really concerning that we are inefficiently procuring new capacity over old due to the capital requirements to get longer-term contracts, This could also get worse if the multi-price capacity market is ever implemented. “Enduring Capacity” is a product, not a technology or an “age” – therefore there should be a single market for a single product to ensure economic efficiency.

Everything you say makes such sound common sense, backed obviously by your extensive subject knowledge. It makes no sense whatsoever for our energy matters to be in the hands of the fool Ed Miliband. Do you have the ear of any sensible people in government? We are approaching a bleak future that just should not be happening and there seems to be absolutely nothing we can do about it – especially as I understand that Miliband is likely to take over as Prime Minister! What a total joke. Well, it’s not funny at all. I remember petrol shortages and power cuts in the 70s when my children were small and now it seems we will be repeating this in my ‘golden’ years when I need a warm house and a little bit of petrol to get around. (I live in a rural area with no real bus service.) I do realise that the petrol crises is brought to a head by the war in Iran, but the government could help by lessening the taxes on fuel. Why does no government ever consult with experts in their field when setting policies? As an ex teacher, I wish I had a pound for every mistake they make with educational policy. My husband and I very much enjoy reading Watt Logic papers: it gives us hope for the future that someone, some day, may have a better handle on vitally important energy strategies.

The technology is dormant, only old folk know how it works, and the ‘youngsters’ ignore it because they are funded to work with electricity. https://pitch.com/v/diesel-replacement-external-combustion-engine-x4fgku We’d welcome your investment offer, or anyone’s!

Thanks for another informative article, Kathryn.

On interconnectors and the Capacity Market, I understand that National Grid ESO considers: “Interconnectors are generally non-dispatchable, however we do have arrangements that we can deploy if we need them to be dispatchable in the event of a major …”

Another superb analysis, many thanks