In 2022, National Grid ESO (now NESO, the National Energy System Operator) launched the Demand Flexibility Service (“DFS”) as part of its winter contingency against a backdrop of concerns over security of supply in the wake of the Ukraine war. In its Winter Outlook for 2024/25, NESO has determined that the spare margin is higher than in previous years, reducing the need for a contingency. Instead, it proposed to use the DFS as an in-merit margin management tool, and as a result, removed availability payments and reduced the overall economics of the scheme.

Changes to DFS make it less valuable to consumers

This year, NESO has determined that it does not require a contingency for security of supply and requested changes to the operation of the DFS, which Ofgem approved in late November. Since there isn’t a need for the DFS as an enhanced action, NESO will operate the DFS as an in-merit margin management tool which will only be dispatched when it is competitive against alternative actions, ie, the total cost of activating DFS volumes will be considered against the total costs of interconnector or Balancing Mechanism (“BM”) actions, be based on NESO’s forecast of its margin requirement within day.

Moving in to an in-merit service means that the Guaranteed Acceptance Price (“GAP”) has been removed. The GAP previously ensured providers received at least £3,000 /MWh during most events – without it, payments to customers under the DFS are expected to be as much as 90% lower than last year. While customers were paid £1-4 /kWh saved last year, they are likely to only receive around 10-30p /kWh this winter.

In Winter 2022, 1.6 million households and businesses took part in the DFS, rising to 2.2 million the following year. So far this year, 650 MW of DFS has been procured, but at no time has the amount procured matched the requirement, suggesting alternatives such as interconnectors and the BM have been more cost effective. This year there are 14 domestic providers registered, and 18 non-domestic, which aggregate demand across their customers.

So far there is no information about how many end users are signed up, but anecdotally, some 90% are apparently customers of Octopus Energy, as was the case in previous years, possibly because of the enhanced economics the company offered on top of the payments from NG ESO. Octopus expected participation this year to be much lower following the removal of the GAP. It surveyed 2,500 of its customers, 1,700 of whom responded, with 80% of the responding participants saying they were unlikely to engage with the DFS if the payments were cut.

However, it is difficult to justify paying DFS participants amounts which could be 10 times higher than the prices of alternatives such as interconnector and BM trading when the costs of the scheme are socialised across all electricity consumers. This would be deeply regressive, since the consumers most able to engage in demand-side response are those with high value assets such as electric cars, which are unaffordable to the poorest consumers.

The French experience of DSR is also poor

Countries with higher levels of electric heating rely more on demand-side flexibility than Britain does, for example, France where electric heating has been widespread for many years. The French grid operator Le Réseau de Transport d’Électricité (“RTE”) has developed sophisticated demand flexibility tools, with large industrial consumers typically representing the principle source of demand response. In the 1990s, the potential of demand response that could be mobilised was estimated to be around 5-6 GW, but this potential had fallen to 2.5 GW by 2017. France has set national objectives for demand side response of 4.5 GW in 2023 and 6.5 GW in 2028. In 2020, the available demand side response capacity was 3.2 GW, falling short of ambitions at the time.

The existing demand-side response schemes in France are managed through day-ahead forecasting and real-time adjustments, considering factors such as weather data and consumer behaviour, and include:

- The “Demand Response Block Exchange Notification” (“NEBEF”), where consumers reduce their demand in response to price signals or requests from the grid operator. This mechanism treats demand reductions similarly to energy generation, with remuneration provided to participants, and is open to consumers with demand of at least 1 MW (or aggregators who aggregate smaller loads which add up to at least this amount);

- Capacity Remuneration: this is similar to the Capacity Market in GB, where consumers and generators can receive payments for making capacity available during peak demand periods. In France, this includes both capacity (in MW) and actual energy reductions (in MWh), which are activated on request to help balance supply and demand;

- Policies and Targets: The French government has set ambitious targets for demand response as part of its Multiannual Energy Programme (“PPE”), aiming to enhance the flexibility of the electricity system in line with increasing renewable energy integration. The potential for demand response, especially from large industrial consumers and, increasingly, from residential and SME sectors, is seen as crucial for maintaining grid stability during extreme weather events.

In addition, Electricité de France (“EDF”), the main electricity supplier in France, operates a consumer tariff similar to the DFS. The “Tempo” tariff is designed to manage electricity demand and costs, incorporating a traffic light-like system with blue, white, and red days, each having different pricing. This system replaced the older “EJP” (Effacement Jour de Pointe) tariff, which had similar demand management features.

Under the Tempo system:

- Blue days are the cheapest, with users paying prices that are 30% lower at peak times (from 06:00 to 22:00) and 41% lower at off-peak times, compared to the regulatory price. This covers 300 days per year;

- White days are moderately priced, and occur on 43 days. Savings are still 10% at peak times and 34% at off-peak times;

- Red days are the most expensive with prices three times higher than the normal rate, and limited to 22 days during winter (1 November to 31 March). The price per kWh is three times higher than the normal rate in order to encourage consumers to reduce consumption during peak demand periods, in order to manage load on the electricity grid more efficiently. Even on red days, users can save up to 16% during off-peak hours if they cut down on usage.

Clients receive an alert by SMS or email notifying them that the next day will be a red day, or are notified through the EDF app and website. The colour also shows up on their electricity meter from 20:00 the night before.

While there will never be more than five red days in a row, and red days cannot take place on weekends and public holidays, combinations of successive red and white days are possible, which make it difficult for consumers to manage their demand. For example, there is only so long a household can go without doing laundry. In addition, reducing heating levels for extended periods can have very detrimental health implications for vulnerable consumers for example by exacerbating respiratory or circulatory illnesses.

EDF has 70% of the market for individual households and 55-60% of the market for business customers. However, despite the very long history of variable tariffs, only 500,000 or 1.6% of households are on the Tempo tariff, against a target of 5 million. The vast majority of households prefer to be on the regulated tariff. Although some studies have shown that up to 100% of households would be better off on Tempo than the regulated tariff, it suffers from low public awareness, and problems for households if a series of red or white days occur on consecutive days.

Due to the relatively low number of households using the Tempo tariff, the contribution to demand reduction from the residential sector remains low, despite this type of tariff having been a feature of the French market for decades. This suggests that realising the potential for demand-side flexibility from the residential sector could be challenging unless these schemes can be shown to deliver higher consumer benefits in terms of price, and are automated so that they rely on less on active demand reduction. Currently both Tempo in France and the DFS in Britain depend on consumers taking active steps to reduce consumption – grid operators hope that automated energy management systems will deliver larger results, but there are considerations to be resolved around customer autonomy and consent.

Business participation in demand reduction has collapsed

Winter 2023/24 was the first in which triads had been abolished. Triads were the three half-hours with highest system demand between November and February, separated by at least 10 business days. They were used in the determination of Transmission Network Use of System (“TNUoS”) charges – businesses were charged based on their demand during the triads.

This led businesses to engage in “triad avoidance” – a process whereby they paid consultants to advise them on the when the triads may take place, so they could reduce their consumption in those periods, thereby reducing their TNUoS charges. Eventually Ofgem decided to abolish triads on the basis that triad avoidance was largely a zero sum game – businesses participating in triad avoidance meant that those that did not or could not ended up paying more. There were some arguments that by reducing demand at peak times, grid expansion could be avoided, however, with the growth in renewable generation and electrification, grid expansion will be necessary, and it’s possible that the entire triad approach simply delayed rather than avoided network investment (possibly to the detriment of the market).

With the retirement of the triads, it was expected that businesses would sign up for the DFS instead, but so far this has not materialised in any significant way – the vast majority of participants in the DFS are households. The typical reduction in demand realised by triad avoidance was around 2 GW, which is far larger than the demand reduction achieved through the DFS, even when it was being used for security of supply reasons. This suggests that businesses do not see the same level of benefit from the DFS that they did in triad avoidance, where 25-30% savings on network costs could be realised.

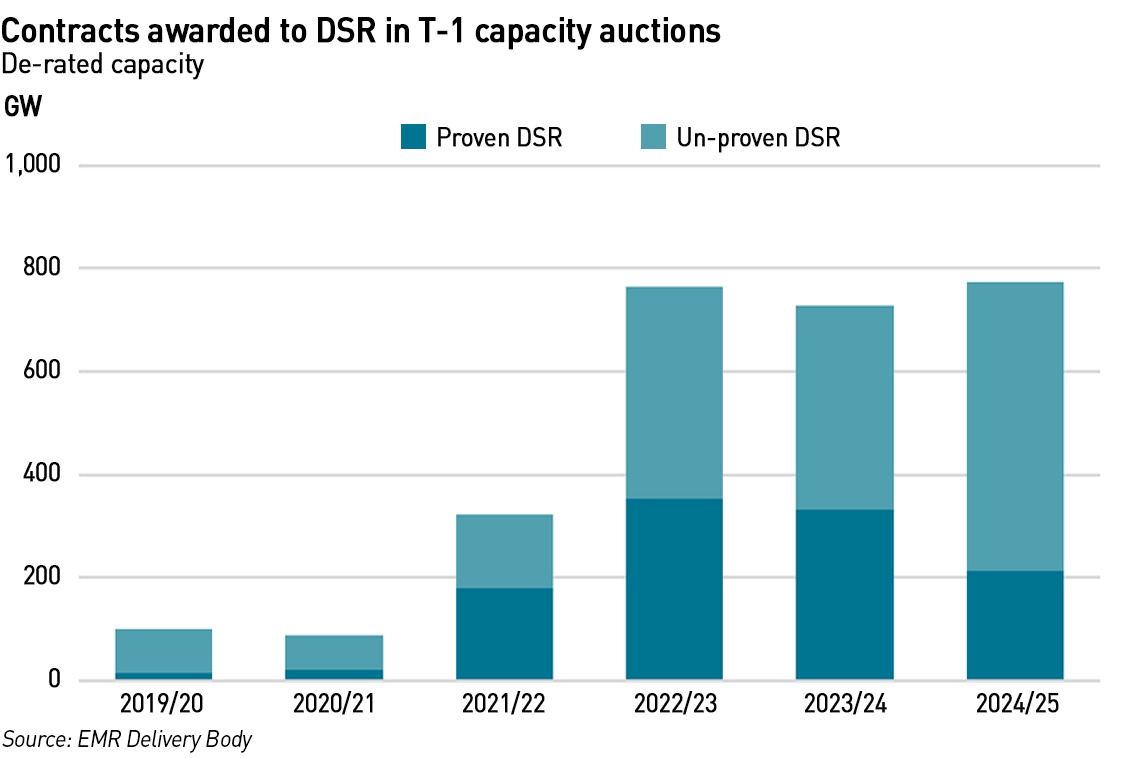

There was a small increase in demand-side response participation in the Capacity Market. In the T-1 capacity auction for WIN-24, 59 units comprising 773 MW of DSR (de-rated) capacity were successful in securing contracts, of which 600 MW was from Unproven DSR units. The previous T-1 auction for WIN-23 secured 726 MW of DSR. This increase is still far below the volumes realised through triad avoidance.

DSR should be a no-brainer but is proving to be easier said than done

Demand-side flexibility should be a no-brainer – so-called “negawatts” being, in theory, the cheapest form of supply (although in the case of businesses, this can mean on-site generation, so not strictly “negawatts”). But in reality things are not so easy. Where DFS must compete with other sources of supply, it struggles to demonstrate compelling economics for users, in large part because under normal market conditions, the entities with the greatest ability to flex demand are those with higher affluence and therefore a lower need to achieve savings. This is particularly true in the domestic market and explains why, in the absence of automation, it is likely to be difficult to realise large volumes of domestic DSR.

It would therefore make more sense to seek response from industrial and commercial consumers, but for these users, the schemes must be both easy to adopt and avoid interfering with business operations. The success of triad avoidance indicates that this can be done – 2 GW is a significant amount of peak shaving which is larger than the current largest single source of supply or generation in the GB market. But for whatever reason, neither the DFS nor the Capacity Market is delivering a comparable appeal to these consumers. In the non-domestic segment, automation is already well established by aggregators, with issues of consent being less fraught.

That it is difficult to identify any country which is successfully harnessing DSR to deliver meaningful volumes (10% of peak demand or more), confirms that this is not a simple problem to solve. This report from ACER sets out some of the challenges, which are relatively straightforward to describe but harder to solve. Equipment upgrades such as smart meters, device automation (eg programmable appliances) and control software need to be deployed at scale. And market frameworks need to be upgraded to provide access to all aspects of the market and sufficient price signals for response.

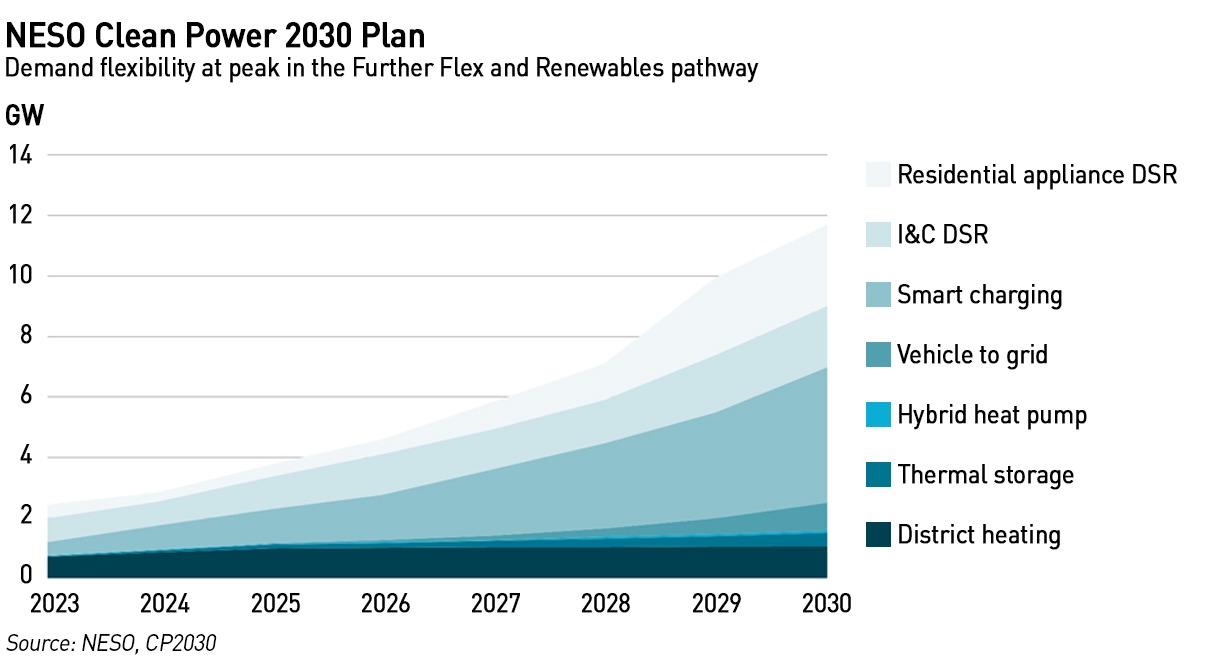

Policymakers love the idea of flexibility. The Clean Power 2030 Plan calls for demand-side flexibility to increase between four and five times to 2030, from 2.5 GW today to 10-12 GW in 2030.

Most of the growth is expected to come from smart EV charging. But there are headwinds – growth in electric car sales is slowing, despite reports that manufacturers are rationing the sale of petrol cars to meet Government targets. Increasing insurance costs for electric cars are starting to dent their popularity. In addition, access to smart charging does not mean people will use it – a Government study in 2022 found that 26% of electric car owners and 49% of plug-in hybrid owners with private charging facilities opted to use a three-pin plug instead of flexible charge facility.

Which is to say that an awful lot needs to happen for the growth in demand-side flexibility required by CP2030 to be realised, and right now, things are moving in the opposite direction with the changes to the DFS and the removal of triads as a basis for network charging. There will need to be a significant change to deliver the demand-side participation policy-makers are hoping for.

This is all going to go horribly wrong.

With failing real incomes, the affordability of electric cars, even much cheaper secondhand ones, is going to nosedive.

Heat pumps will put excessive demand on the grid so people will end up freezing.

Nuclear was the answer, but it’s too late now.

Disaster beckons with a destroyed economy and social disorder.

Remember the name – Ed Miliband.

There’s a lot to be gained by having a battery in every residence, but how big would it need to be?

Having a buffer of a reservoir of power would help enormously, where there can be a complete uncoupling of instantaneous demand from the end user to what actually needs to be generated. With battery packs in every home, we could have no need for hydrogen generation by electrolysis, to be burnt inefficiently in CCGT, no worries of dunkelflaute. The distribution of excess generated power when it occurs to all users, no CCGT at all, only CHP, with renewable gaseous/liquid fuels.

We can keep adding to centralized facilities, which may be needed for poorer people that don’t have the capital to make investments but as battery storage costs decrease, the economic benefits of cheaper power can be used by richer, high demand users.

With all new technology, you have the early adopters, and as Musk showed with the latest iteration of electric cars, it is the richer people who need to be the early adopters who can reduce their inefficiencies, not burning 3-5kwh per mile, but just 0.3 to 0.5kwh per mile, up to 20x energy efficiency improvement……….not 200%, almost up to 2000% improvement

Surely, to avoid causing problems with businesses and the poor, where businesses will be pushing for efficiencies to maximise profit, and the poor who have to work at maximum efficiency because their income is so low that every penny counts already, isn’t it controlling the richer people where excessive consumption causes the unnecessary problems, that is the essential part of all this?

I cannot reduce my demand, as I have very little, in the evening, 7x 7w-10w LED bulbs, a gas fire burning 4kw/hour, a TV and possibly 2 computers + 1 laptop, 1kw microwave one or two 1kw rings, not on all at the same time, but varies, and a dishwasher and or washing machine, fridges and freezer. I could change from a gas fire to a separate isolated air-air 1kw input heat pump for one room.

Isn’t cheap electric power storage the critical technology to get all this working, such that when a heat pump is working, that the instantaneous demand to the grid doesn’t spike? Wouldn’t the additions of battery storage act as voltage spike suppression, from the noisier electric supply with so many high power devices (users) switching on and off, or high power supplies coming online? Wouldn’t having a battery as a buffer enable ramping of power supplies as they start to generate?

Isn’t it the rich high power users that need to have legislation aimed at how they have to behave, or their usage modified?…….surely no one else has that flexibility, or the money to invest in early adoption, else we would be socializing the higher costs onto poor people as well through increasing electricity bills, e.g. like the example of high standing charges.

Isn’t it the resource profligacy of the rich that has to be curbed?

TS : “Isn’t it the resource profligacy of the rich that has to be curbed?”

This IS the purpose of Net Zero and not just for electricity and the “rich” but all energy, food, heating and travel is intended to be rationed for everyone bar a few elites. See the tax-payer funded Cambridge University Department of Engineering “Absolute Zero” report:

https://www.eng.cam.ac.uk/news/absolute-zero

BTW, the problem with DSR, household electricity storage, evs, heat pumps and ToUTs is that 80% or more of local grids cannot supply more than 1-2KW/household continuously. So massive upgrades to the local grids will be required, only to be used for a few winter months:

https://committees.parliament.uk/writtenevidence/82722/html/

Sadly, li-ion batteries are not environmentally sustainable. We need cleaner battery technologies before we start going down the road of trying to get batteries in every home or similar

There is very little to be gained by having a battery in every home.

Almost anything which can be done with domestic batteries can be achieved more cheaply by doing it at greater scale. The only benefit on a per household battery is cover for supply failure but even then it could be argues that in cities that is best done at LV transformer level or higher.

Domestic batteries are only economic (if they actually are once depreciation is taken into account) because the commercial electricity storage market is currently too small.

You only need to consider what the spot price of electricity would look like if everyone had a battery – the economics would be such that no-one would buy one – the margins would be too slim.

There are of course those who argue that domestic batteries come for free by having an electric car parked on the drive but that often only works on the assumption that people use electric cars in a different way to how people currently use cars (e.g. that those cars are somehow on the drive and fully charged from 17:00). Not to mention consideration of the effect that widespread V2G would have on electric car battery warranties

Re domestic storage: A rich solution?

The value of the electric car I bought in 2020 has dropped to a level where, rather than sell it as a vehicle, I could keep it in my garden and use its 50kWh battery for domestic storage cheaper than buying 12 kWh home battery.

I think my car battery is 400 volt but what is a domestic (eg Tesla) battery voltage? Can all/any car batteries be put in parallel with current domestic batteries? Are the present DC to AC converters compatible? Who makes conversion kits?

There’s devilry in the detail, as you clearly recognise.

Not many of today’s EVs are equipped for vehicle-to-grid (V2G) and, afaik, none of the existing domestic chargers (actually a connection box) are “reversible”.

Quite a few EVs have domestic sockets fitted: vehicle-to-load/home (V2L/H) but that entails running an extension lead from the car to whatever you need to power so is hardly a regular option.

In addition, for V2G, extra electical kit is required by law to isolate the supply if the mains shuts off – to avoid pushing volts back into the grid when people may be working on repairs.

So, for V2G to become widespread, it would require: the majority of EVs to be equipped for it; all domestic chargers to be replaced or uprated; all candidate switchboards to be fitted with the protective kit.

There are other challenges: don’t hold your breath!

I’m not looking for a car mechanic to come up with a solution. But if I no longer need the vehicle, I have a 50kWhr battery available. Could an electrical engineer use this additional storage to connect to my existing domestic battery which supplies power to my house? My solar panel/domestic battery system already has isolation to prevent power getting back to the grid.

Of course you could hook up a battery from an electric car to an (appropriately specified) inverter charger system, just as you can with pretty much any battery.

The battery chemistry of the car is likely to be NMC rather then the LiFePO4 used for most domestic static systems so it would need a separate inverter / charger to the one you already have as the battery voltage characteristics will almost certainly preclude operation in parallel on the DC side.

Adding an additional inverter will need re-evaluatiion of your supply by the DNO as the DNO rightly or wrongly assume that all connected inverters can deliver full power simultaneously and they will want to make sure that you can’t lift the supply voltage to neighbouring properties to a unacceptable level.

If you only want to add energy rather than power rating then it is usually easier to add more batteries of the existing type, or replace the whole battery system with one of larger capacity.

Hi, did your isolation from the grid come with your package, or did you pay more later.

Thanks

All part of the battery (Tesla) package. I was a chemist so am ignorant of electrical engineering but wouldn’t every battery system have to be supplied with grid isolation?

Theoretically every battery system doesn’t have to be supplied with grid isolation, however, they are because that allows it to be used as a back-up system when the grid fails. Saves having to have an onsite back-up generator burning fuel, or a UPS. It’s basically a larger version of a UPS that you can buy for computers, that used to have a lead-acid battery. With a mains power battery, that gets rid of the UPS industry/businesses and back-up generators as well. There are many more industries that will be affected by these changes other than just the oil and gas industries.

The issues are whether the battery back up correctly islands the circuits concerned and how it deals with the required earthing. Very few systems do either correctly.

Kathryn,

Just a small comment about DSR in France. We have been using an apartment in the Alps for many years which has always been on a split tariff, not the “tempo” that you mention. It has a simple peak (heures pleines) and off-peak (heures creuses) structure which runs automatically. Off-peak is most of the night, mainly for water heating, with a couple of short periods in the middle of the day and early evening.

It is my understanding that this tariff is very widespread – it may be the default option – and probably explains why France has a much smaller difference between peak and off-peak demands, proportionally speaking. That helps to keep the nukes well-loaded, of course. Its established availability may also explain the poor take-up of the more elaborate – and possibly less convenient – tempo.

Mike

That sounds like the E7 or E10 that used to be rolled out with storage heating in the UK.

The issue with connecting EV battery to the mains for V2G is the disastrous CCS2 standard foist upon us by the German legacy manufacturers via the EU. The previous Chademo standard works well, but CCS2 was poorly written and inconsistently implemented by the manufacturers. Instead they are promising AC coupling via the onboard charging system (avoiding the need for another expensive AC/DC converter as part of the EV charger), but this has yet to find an agreed connection standard. The cynical would say this is similar to Toyota and the “revolutionary” solid state batteries that are always just a year away meaning that you should delay an EV purchase and instead buy one of their horrible hybrids.

Duncan B,

Yes, it probably is similar to that old system except that, aiui, the signal was transmitted over the mains rather than by an ancient radio frequency (which is shutting down this summer with no replacement organised!). These days the French system is run by smart meters.

Wrt V2G, there’s still the need for extra kit to avoid back-feeding the grid which aiui, is quite expensive. Also, if I’m understanding your comment correctly, the Chademo standard requires an additional converter in the domestic charger which would add to the cost.

Duncan H,

Apologies: I should have read your post more carefully – I missed that you are talking about re-purposing an end-of-life car battery rather than a running EV.

I see these comments are mostly about domestic. Business DSR has (at least) 2 challenges: Flex providers frequently need the horrendously bureaucratic AMVLP accreditation from Elexon to isolate and use flex loads and b) Businesses on a fixed price supply contract haven’t been shown a compelling way in which the profile that has created that fixed price can be used as a benchmark against which load shifting flex actions earn them money. We trialled some electric forklifting load shifting very successfully, but struggled to overcome organisational inertia whereby the main job was making cosmetics, and the marginal gains from this sort of load shifting just wasn’t material enough.

We also saw an electric bus site doing some very successful load shifting. Only thing is that the supplier had put them onto a flex supply contract, so whilst against the day to day peak/off peak price they were doing very well, they got rinsed in a rising market by NOT having the overall supply contract locked in as a fixed price.

The Triad system was inaugurated in 1990 with the twin aims of reducing the need for extra transmission capacity and extra generation capacity at a time when there was extensive investment in new CCGT plant in the Dash for Gas. With demand having peaked 20 years ago transmission is no longer determined by demand, which runs at only about 70% of the peak levels: in any event real transmission constraints were not often binding other than as the perverse result of initial dispatch under both the pool system and NETA. However, the demise of the coal fleet and reductions in the nuclear fleet have made the issue of replacement dispatchable capacity increasingly pressing. We now have a confused Capacity Market (with no clarity on potential asset life or prospective utilisation for newbuilds). The main effect of the Triad system was to replace transmission connected generation with behind the meter generation, almost exclusively from diesel, which was always the economic choice (see diesel STOR). It did flatten the afternoon peaks to the point where they were little different to the shoulder hours of demand, and this made triad avoidance an increasingly expensive cost with many more periods potentially at risk of being Triad qualifying. It was an embarrassment that the system was leading to rising diesel use. Transmission investment is now dictated by the need to service a renewables intensive grid, and the charges are simply passed through in standing charges, offering little incentive for economy in transmission investment. The fact that so much industrial demand has simply shut down also undermined the value of the Triad system: indeed, it was probably a contributor to the loss of process industries, undermining their international competitiveness.

Those interested in monitoring the DFS consumer DSR service might like to look at the data. The historical record is here:

https://www.neso.energy/data-portal/demand-flexibility-service

with the current data listed here:

https://www.neso.energy/data-portal/demand-flexibility

The initial trials paid up to £6,000/MWh to aggregators, and resulted in a lot of gaming of the system with consumers artificially boosting demand when their baseline was being established. It was very costly, and yet the real demand reduction was very slight. Even the official measure peaked at around 300MW – a modest OCGT unit. Magnify this chart to see if you can spot the use of DFS in January 2023:

https://i0.wp.com/wattsupwiththat.com/wp-content/uploads/2024/08/Generation-jan-2023-1722888879.3157.png

So far this season just 326.5MWh has been procured at an average cost of £467/MWh, with a peak rate of 111.4MW – useless against the 10GW scale that NESO imagine for the future.