In my second post on uranium I look at mining and conversion. My previous post can be found here.

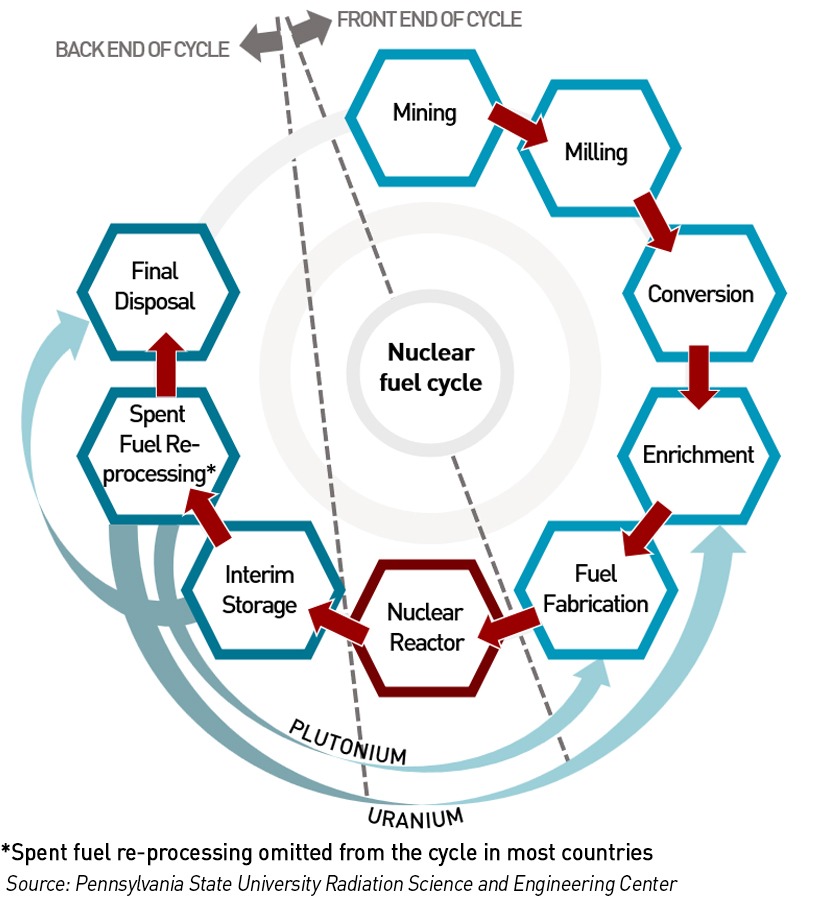

The nuclear fuel cycle consists of two phases: the front end which prepares uranium for use in reactors and the back end which ensures that used—or spent—but still highly radioactive, nuclear fuel is safely managed and disposed of.

The nuclear fuel cycle consists of two phases: the front end which prepares uranium for use in reactors and the back end which ensures that used—or spent—but still highly radioactive, nuclear fuel is safely managed and disposed of.

There are high levels of concentration in each phase of the nuclear fuel cycle:

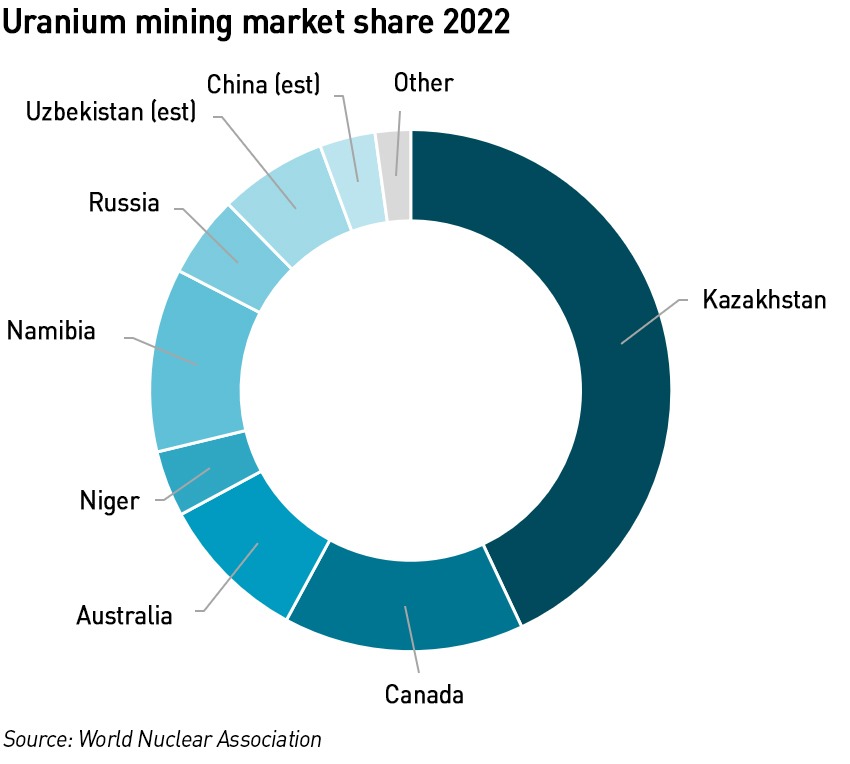

- Two thirds of natural uranium comes from mines in Kazakhstan, Canada and Australia

- 90% of conversion capacity is shared by four countries: France, China, Canada and Russia

- Russia and Europe (France plus Urenco) dominate enrichment with 90% of the market

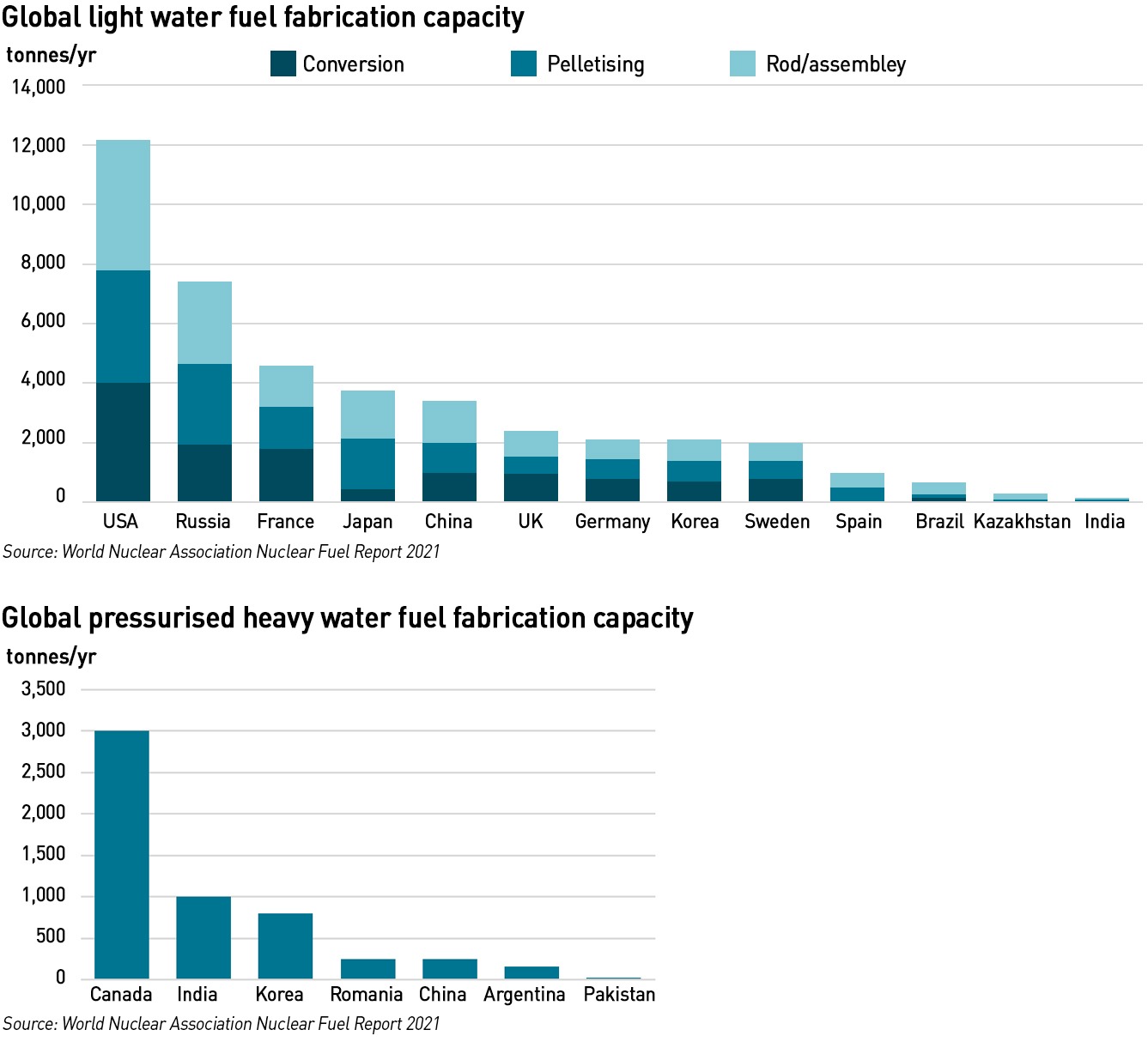

- Five countries (USA, Russia, France, Japan and China) dominate 75% of the production of fuel for light water reactors and three countries share 88% of the production of fuel for pressurised heavy water reactors (Canada, India and Korea)

There are concerns about both market concentration, and Russia’s position in the market in the wake of the invasion of Ukraine. According to Euratom, 77% of the natural uranium supplied to the EU in 2023 came from three countries, Canada (31.9%), Russia (23.8%) and Kazakhstan (21.3%).

However, natural uranium produced in CIS countries (former Soviet nations) accounted for 47.0% of all-natural uranium delivered to EU utilities in 2023, an increase of 21.3% by weight on the year before. Natural uranium originating in non-CIS countries also increased in 2023, by almost 30% compared with 2022.

In 2023, conversion service deliveries to EU utilities were more than 22% higher than in 2022. 97% of all uranium hexafluoride (the output of the conversion process) was received from just four companies: Orano (EU) – 28.7%, Rosatom (Russia) – 26.5%, Cameco (Canada) – 18.9% and ConverDyn (US) – 18.3%.

In 2023, enrichment service deliveries to EU utilities were 12% higher than in 2022, with nuclear operators opting for an average enrichment assay of 4.26% and an average tails assay of 0.19%. 54.9% of this enriched uranium was produced in the EU and 37.9% in Russia.

Most companies manufacturing actual nuclear fuel for EU reactors are the reactor vendors, with the largest fuel fabrication capacity being located in Europe (Germany, Spain, France, Sweden and the United Kingdom), Russia and the United States. This market is very competitive, which is driving continuous improvements in fuel design, focusing on enhanced burnups and improved performance. Most EU utilities have access to at least two alternative fuel fabricators.

Natural uranium resources are highly concentrated

While almost all the uranium mined is used for electricity generation, a small proportion is used in the production of medical isotopes. Some is also used in marine propulsion, particularly naval.

While almost all the uranium mined is used for electricity generation, a small proportion is used in the production of medical isotopes. Some is also used in marine propulsion, particularly naval.

Uranium is a naturally occurring element with an average concentration of 2.8 parts per million in the Earth’s crust. Traces of it occur almost everywhere. It is more abundant than gold, silver or mercury, about the same as tin and slightly less abundant than cobalt, lead or molybdenum.

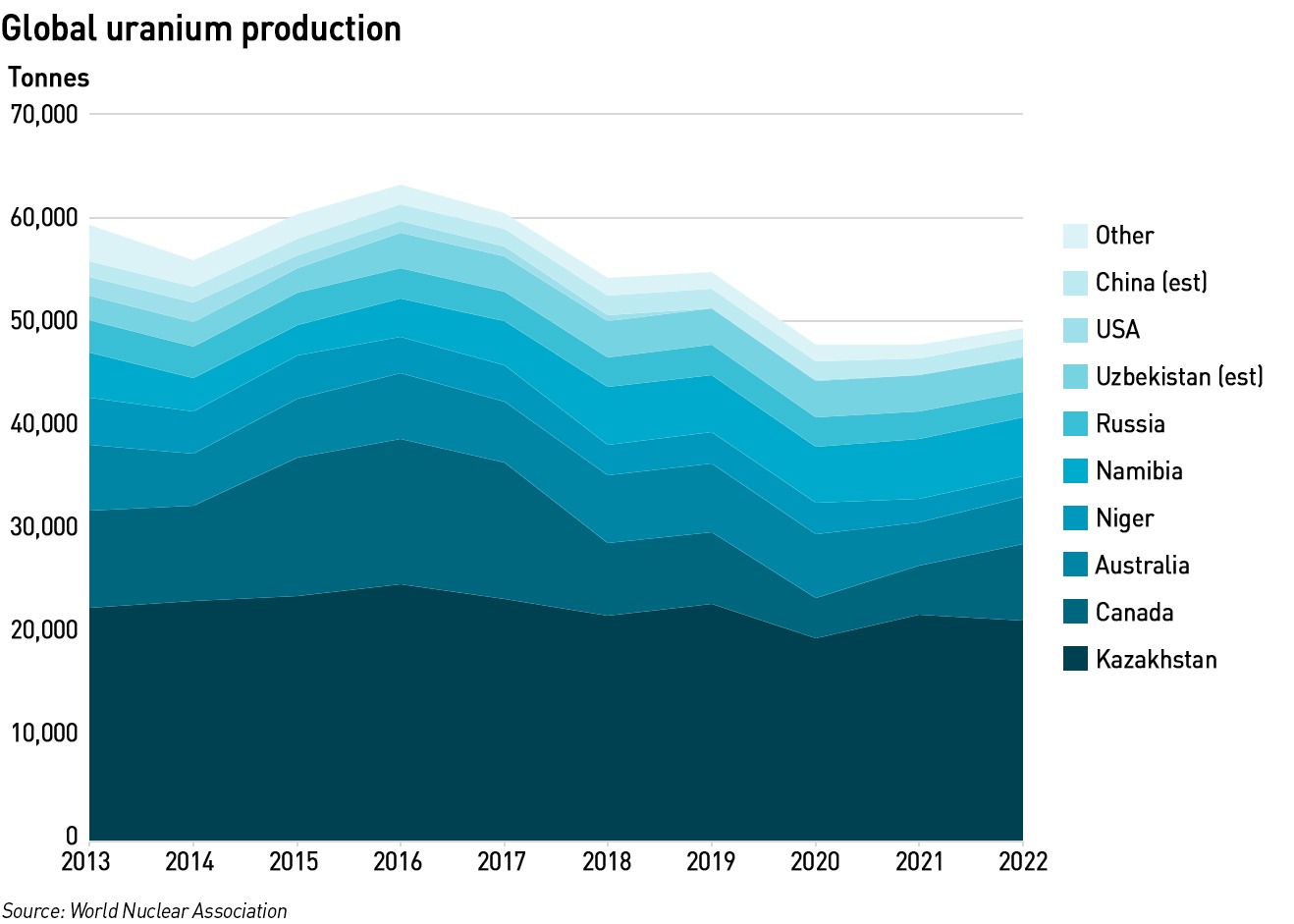

Vast amounts of uranium also occur in the world’s oceans, but in very low concentrations. About two-thirds of the world’s production of uranium from mines is from Kazakhstan, Canada and Australia.

Mining methods have been changing. In 1990, 55% of world production came from underground mines, but by 2022 in situ leach (“ISL”) mining accounted for over 55% of production. Conventional mining involves removing mineralised ore from the ground, breaking it up and then leaching it with sulphuric acid to dissolve the uranium oxides contained within.

In situ leaching, also known as solution mining (or in situ recovery in North America), involves leaving the ore where it is in the ground, and recovering the minerals from it by dissolving them and pumping the pregnant solution to the surface where the minerals can be recovered. As a result, there is little surface disturbance and no tailings or waste rock generated with ISL, however, the orebody needs to be permeable to allow liquids to come into contact with the minerals, and be located so that they do not contaminate groundwater required for other purposes.

Uranium ISL uses the native groundwater in the orebody which is fortified with a complexing agent and in most cases an oxidant. This is then pumped through the underground orebody to recover the minerals contained within it by leaching. Once the pregnant solution is returned to the surface, the uranium is recovered in much the same way as in a conventional uranium mill which processes mined ore.

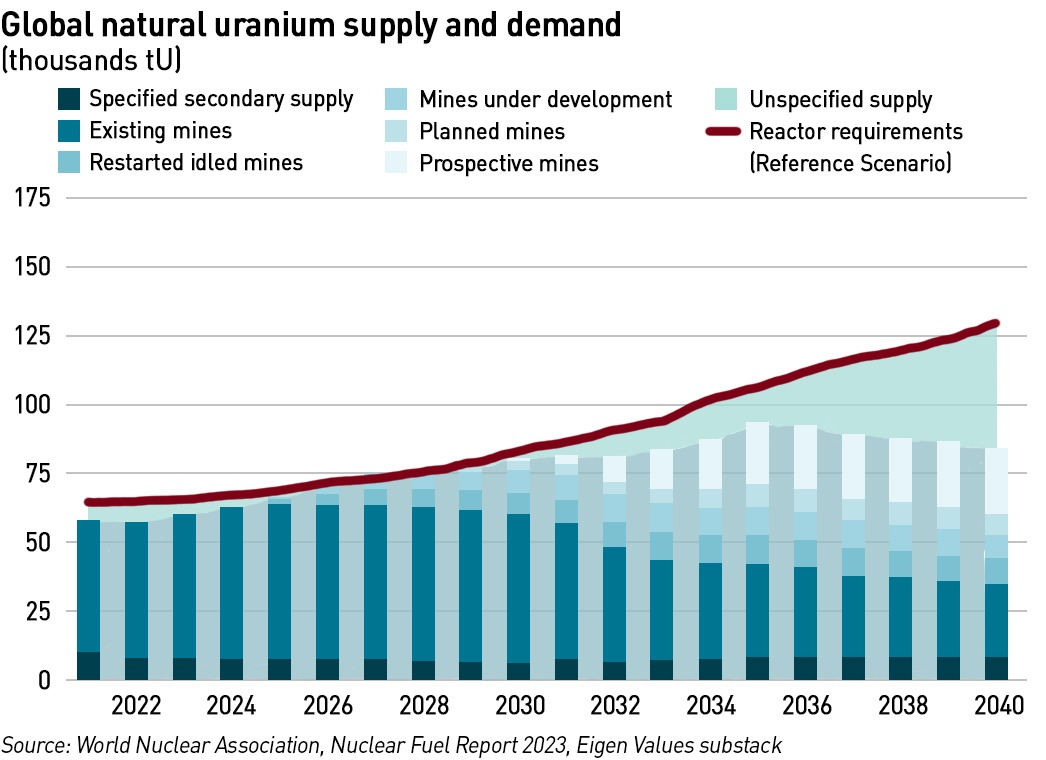

The World Nuclear Association (“WNA”) is predicting a supply deficit in natural resources from 2021 to 2026, a balanced market in 2027 and 2028, then a growing deficit out to 2040. Until recently, the supply gap was reduced by drawing down inventory, but recent steep increases in the price of U3O8 indicates that available inventories have been mostly used up. According to retired consultant David Turver, there are several reasons to believe the WNA’s estimate of the near-term supply gap is too low.

Firstly, the world’s largest uranium supplier, Kazatomprom which represents about 40% of global uranium production, announced a big downgrade to its production forecasts for 2024 and said its plans for 2025 are at risk. Its guidance for 2024 production was cut by 3,500 tU which represents about 6% of global primary mine supply. In addition, the coup in Niger disrupted production at Orano’s SOMAIR mine, and there are rumours that Russia is looking to take it over.

Secondly, enrichment prices are rising meaning enrichment supply is scarce. In recent years there has been a trend of “under-feeding”, due to an excess of enrichment capacity – essentially, a smaller amount of UF6 is fed into the enrichment centrifuges, which are then operated for a longer period, resulting in the same output for a smaller input (see below). This had been an important factor in keeping uranium prices low prior to the last three years. However, due to a shortage of enrichment capacity, not only are facilities expected to stop under-feeding, some may begin over-feeding, where additional UF6 is fed into centrifuges, which then can be run for a shorter period which is a more efficient use of enrichment capacity, but requires more UF6, which in turn increases demand for U3O8. It also reduces the amount of “secondary supply” of uranium which comes from under-feeding.

Thirdly, uranium demand may well be higher than the WNA expects as Japan accelerates restarts of mothballed reactors, and other countries extend the lives of existing reactors.

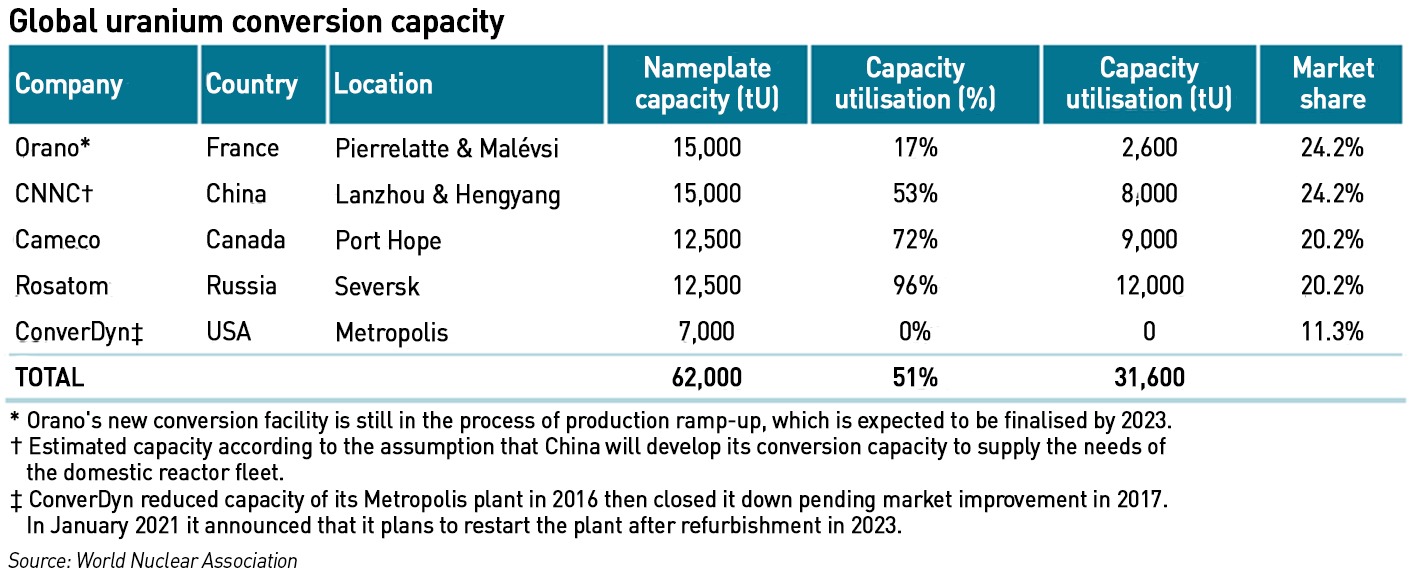

Uranium conversion capacity is even more concentrated

Uranium leaves the mine as the concentrate of a stable oxide known as U3O8 or as a peroxide (also known as “yellow cake“). At this point, it still contains impurities and must be further refined prior to enrichment, before or after being converted to uranium hexafluoride (UF6), commonly referred to as “hex”. Both processes are normally included in the step between the mine and enrichment plant, referred to as “conversion”. Yellow cake is typically packaged in 55 gallon drums and sent to the uranium conversion plant.

There are conversion plants operating commercially in France (24% of global capacity), China (24%), Canada (20%), Russia (20%) and the USA (11%) – China’s capacity is expected to grow significantly to 2025 and beyond, to keep pace with growing domestic requirements.

The main, “wet” conversion process is used in Canada, France, China and Russia. In this process, the concentrate is first dissolved in nitric acid to give a clean solution of uranyl nitrate UO2(NO3)2. 6H2O is fed into a countercurrent solvent extraction process, using tributyl phosphate dissolved in kerosene or dodecane. The uranium is collected by the organic extractant, from which it can be washed out by dilute nitric acid solution and then concentrated by evaporation. The solution is then calcined in a fluidised bed reactor to produce UO3 (or UO2 if heated sufficiently). Alternatively, the uranyl nitrate may be concentrated and have ammonia injected to produce ammonium diuranate, which is then calcined to produce pure UO3.

The alternative, “dry” process is used in the USA, where uranium oxide concentrates are first calcined (heated strongly) to drive off some impurities, then agglomerated and crushed.

Crushed U3O8 from the dry process and purified uranium oxide UO3 from the wet process are then reduced in a kiln by hydrogen to UO2. This reduced oxide is then reacted in another kiln with gaseous hydrogen fluoride (HF) to form uranium tetrafluoride (UF4), though in some places this is made with aqueous HF by a wet process. The tetrafluoride is then fed into a fluidised bed reactor or flame tower with gaseous fluorine to produce uranium hexafluoride, UF6. Hexafluoride (hex) is condensed and stored.

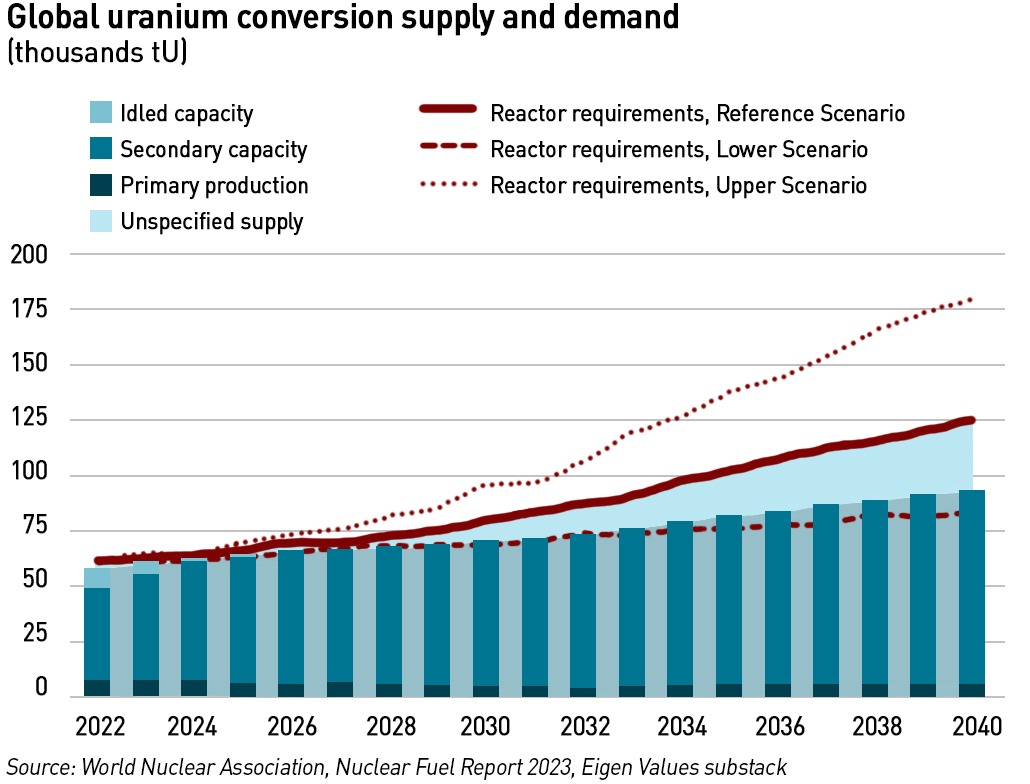

According to the World Nuclear Association, global conversion capacity is struggling to keep up with demand in its Reference Scenario, with a shortfall of around 30,000 tU emerging by 2040. Its Upper Scenario indicates a shortfall of 80-90,000 tU by 2040, which is larger than current capacity, meaning capacity would have to more than double in the next decade and a half to meet demand.

Enrichment over-capacity is expected to re-balance in coming years

After the conversion process, the uranium must be enriched before it can be made into nuclear fuel. Natural uranium typically comprises 0.7% U-235 with the remainder being mostly U-238. U-235 is used in nuclear reactors. Most light water reactors (pressurised water or boiling water reactors) require U-235 concentrations to be at least 3.5% (low-enriched uranium or “LEU”), but some for some applications there is a need for concentrations of 7% up to 20% (high-assay LEU (“HALEU”). Some reactors such as the Magnox reactors previously used in the UK and the CANDU heavy water design in Canada use natural uranium fuel.

U-235 and U-238 are chemically identical, but differ in their physical properties, in particular their mass – the nucleus of U-235 atoms contains 92 protons and 143 neutrons, giving an atomic mass of 235 units, whereas U-238 nucleus has 92 protons and 146 neutrons giving a mass of 238 units. This difference in mass allows the isotopes to be separated.

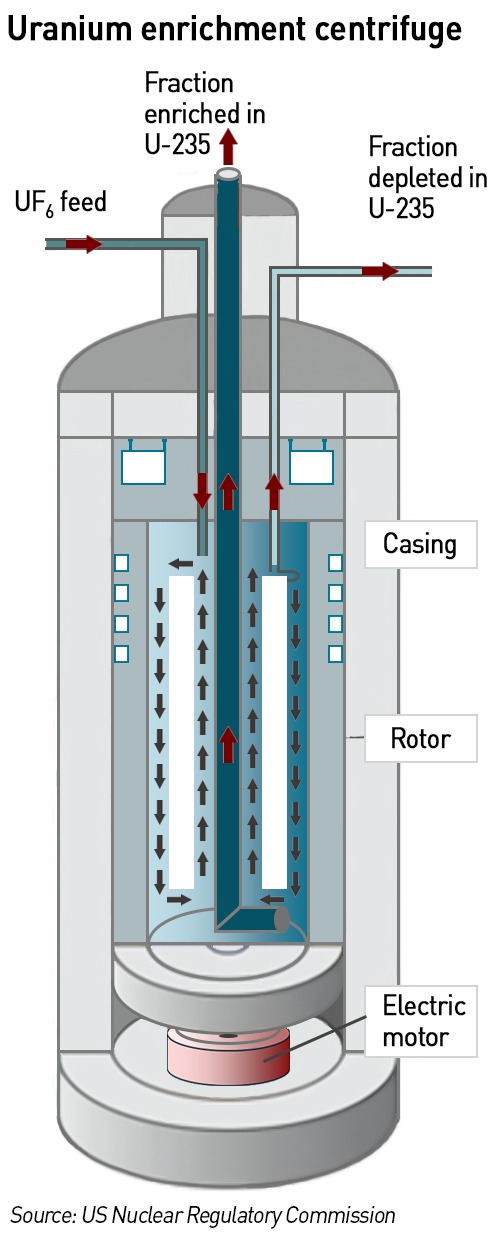

Enrichment processes require uranium to be in a gaseous form at relatively low temperature, which is why uranium ore is converted to uranium hexafluoride prior to enrichment. There are various ways of enriching uranium, but only two are used commercially: gaseous diffusion and centrifugation, with the latter being the only method currently in use. In both gaseous diffusion and centrifugation processes, UF6 gas is used as the feedstock.

The gas centrifuge process was first demonstrated in the 1940s but was abandoned in favour of the simpler diffusion process, however it was later developed and brought on stream in the 1960s as a second-generation enrichment technology. It is significantly more energy efficient than diffusion, requiring only about 40-50 kWh per SWU. (A “Separative Work Unit”, or “SWU”, is the standard measure of the effort required to separate isotopes of uranium during an enrichment process. 1 SWU is equivalent to 1 kg of separative work, and 1 tonne of separative work units or tSWU equals 1,000 kg of separative work.)

A gas centrifuge facility contains long lines of many rotating cylinders which are connected in both series and parallel formations to form trains and cascades.

In the process, UF6 gas is fed into a series of vacuum tubes, each containing a rotor 3 to 5 metres tall and 20 cm in diameter (those in the US are larger, while Russian ones are much shorter). When the rotors are spun at 50,000 – 70,000 RPM, the heavier U-238 molecules are pushed towards the cylinder’s outer edge, meaning there is a higher concentration of U-235 near the centre. A counter-current flow set up by a thermal gradient enables enriched product to be drawn off axially, heavier molecules at one end and lighter ones at the other.

The stream of slightly enriched in U-235 from the centre is withdrawn and fed into the next centrifuge, while the slightly depleted stream (with a lower concentration of U-235) is recycled back into the next lower stage. At the final withdrawal point, the UF6 is enriched to the desired amount.

5% U-235 is the maximum level of enrichment allowed for use in normal civil reactors, however, here is growing interest in higher levels of enrichment for new small reactor designs, and is sought for various research reactors. Various companies have licences in different jurisdictions to enrich to slightly higher levels, of between 5.5% – 8%, and Urenco USA has recently applied to the US Nuclear Regulatory Commission for a licence amendment to increase to 10% and later 20%. Centrus in the USA was licensed in 2021 to produce up to 600 kg per year of high-assay LEU up to 20% in its small centrifuge plant. Above 10%, HALEU requires enhanced physical security and different licensing.

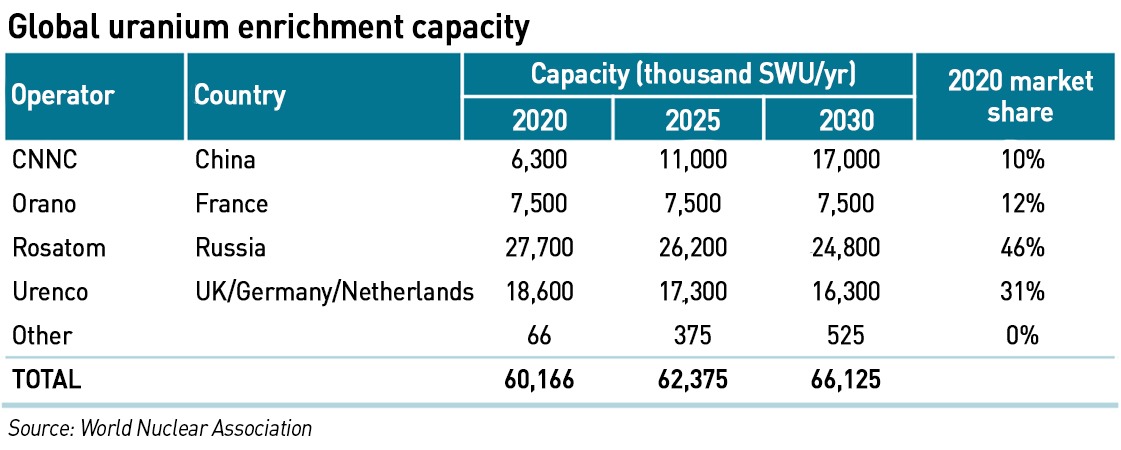

Uranium enrichment is strategically sensitive given the ability to create materials that could be used in munitions, and is capital intensive, creating significant barriers to entry. As a result there are relatively few commercial enrichment suppliers operating a small number of facilities worldwide. There are three major producers: Orano, Rosatom, and Urenco which operate large enrichment plants in France, Germany, Netherlands, UK, USA, and Russia. CNNC is a major domestic supplier and is pursuing export sales. In Japan and Brazil, domestic fuel cycle companies manage modest supply capability. Elsewhere, small non-safeguarded facilities are subject to international opposition.

Following the Fukushima incident in 2011, there has been a significant over-supply of enrichment capacity worldwide, but despite this, most enrichment plants continued running due to the high costs of shutting down and restarting centrifuges. However, with the upturn in demand for nuclear fuel as new reactors come online, and the Japanese re-start process continues, some producers are expanding capacity. Earlier this year, Urenco USA announced a 15% capacity increase at its Eunice facility in New Mexico.

The World Nuclear Association believes that global demand for enriched uranium will exceed supply in 2034 in its base case, Reference Scenario – in the Upper Scenario the shortfall emerges five years earlier in 2029. Increased commitments to nuclear power at COP28 in November 2023 suggest the Upper Scenario may be more likely to apply. However, not all of the available supply will be available to the world market. Chinese capacity is likely reserved for its own nuclear expansion plans, and, for the moment at least, western governments are keen to reduce reliance on Russian energy supplies. This could mean shortfalls are more acute than the global supply /demand picture suggests.

Enrichment costs are driven by the energy used to power the process – modern gas centrifuge plants require only about 50 kWh per SWU. Enrichment accounts for almost half of the cost of nuclear fuel and about 5% of the total cost of the electricity generated. Enrichment plants are able to benefit from some operational flexibility due to possible differences between the operational tails assay and the contractual (transactional) assay, set out in contracts with utilities which buy uranium directly from mines and supply this to the enrichment facility.

Where the operational tails assay is lower than the contracted assay, the enrichment process results in surplus natural uranium which the operator is free to sell – this is known as under-feeding. The opposite is also true – where the operational tails assay is higher the enricher must supplement the natural uranium supplied by the utility with some of its own (over-feeding). However, utilities are increasingly seeking to capture this flexibility themselves to get some benefit from under-feeding.

Nuclear fuel production is highly concentrated

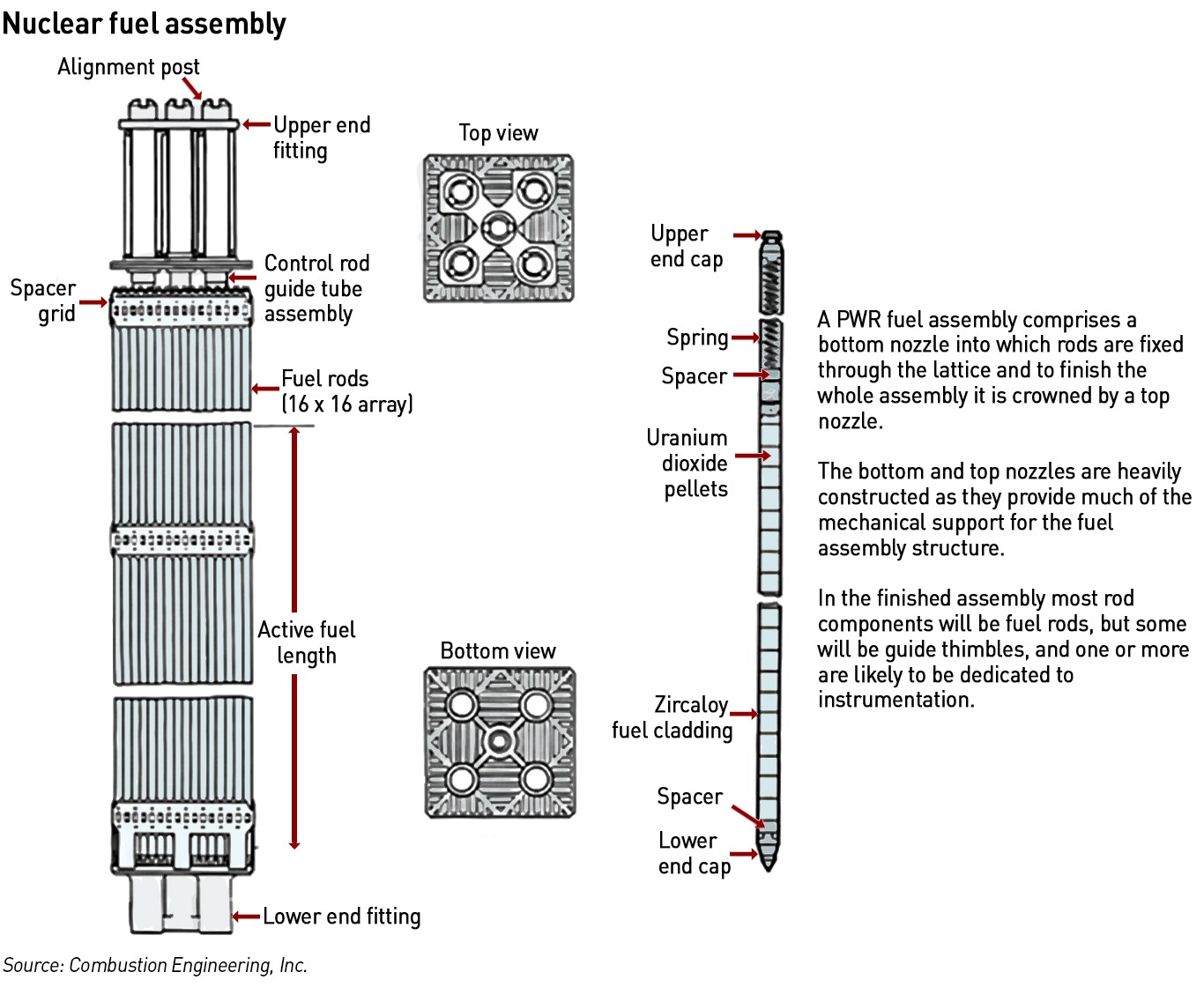

Fuel fabrication is the final stage in the process of turning uranium into reactor fuel. As noted above, the fissile material used for nuclear fuel: U-235 and/or Pu-239, must be held in a robust physical form capable of enduring high radiation levels and high operating temperatures. These fuel structures, which are held in the reactor core for a number of years, must maintain their shape and integrity without leaking fission products into the coolant.

A typical nuclear fuel rod comprises a column of ceramic pellets of enriched uranium oxide, stacked and sealed into zirconium alloy tubes. 200 or more fuel rods are then bundled together to form a fuel assembly. The majority of a reactor core’s structure consists of dozens of fuel assemblies, depending on power level. The specific assembly design varies by type of reactor.

Uranium arrives at a fuel manufacturing plant as either uranium hexafluoride (UF6) or uranium trioxide (UO3) depending on whether it has been enriched or not. This must be converted to uranium dioxide (UO2) prior to pellet fabrication. Most fuel fabrication plants have their own facilities for this chemical conversion which can be done using either “dry” or “wet” processes.

In the dry method, UF6 is heated to a vapour and mixed with steam to produce solid uranyl fluoride (UO2F2). This powder then reacts with H2 which removes the fluoride and chemically reduces the uranium to a pure microcrystalline UO2 product. Wet methods involve the injection of UF6 into water to form a UO2F2 particulate slurry which is then mixed with either ammonia (NH3) or ammonium carbonate ((NH3)2CO3) to produce ammonium diuranate (ADU, (NH3)2U2O7) or ammonium uranyl carbonate (AUC, UO2CO3.(NH3)2CO3). The slurry is then filtered, dried and heated in a reducing atmosphere to pure UO2.

A 1 GW pressurised water reactor core generally contains between 120 and 200 fuel assemblies each containing around 500 kg of uranium oxide, capable of generating about 200 MWh of electricity over its lifetime – each assembly spends around five years within the core. A reactor of this size discharges around 40 spent fuel assemblies each year, containing approximately 20 tonnes of uranium oxide. Every 18 – 24 months, the plant will power down for re-fuelling, with a third of its fuel assemblies being replaced.

The fabrication of nuclear fuel structures for light water reactors and pressurised heavy water reactors consists of three main stages:

- Production of pure uranium dioxide (UO2) from UF6 or UO3

- Production of the high-density, shaped ceramic UO2 pellets, and

- Production of the fuel assembly which involves constructing a rigid metal framework, primarily from zirconium alloy; loading fuel pellets into the fuel rods which are then sealed; and loading the rods into the fuel assembly structure.

Reactor designs set out the precise physical arrangement of the fuel rods in terms of their lattice pitch (spacing), and their relation to other features such as water (moderator) channels and control-rod channels. The physical structures for holding the fuel rods are engineered with extremely tight tolerances and must be resistant to chemical corrosion, high temperatures, large static loads, constant vibration, fluid and mechanical impacts. They must also be as neutron-transparent as possible, while allowing coolant water to flow around the fuel rod.

There is considerable variation among fuel assemblies designed for the different types of reactors, which means there are few suppliers capable of producing fuel assemblies, particularly for pressurised water reactors (“PWRs”). PWRs are the most common type of reactor accounting for two-thirds of global nuclear capacity. PWRs use normal water as both moderator and primary coolant, which is kept maintained at high pressure (about 10 MPa) to prevent boiling.

Fuel for western PWRs is built with a square lattice with fuel rods typically held in 17×17 arrangement. A PWR fuel assembly is between four and five metres high, about 20 cm across and weighs about half a tonne. The assembly has vacant rod positions to allow for the vertical insertion of control rods.

PWR fuel assemblies are more uniform than those in boiling water reactors (“BWR”), and those in any particular reactor will have substantially the same design. An 1,100 MW PWR may contain 193 fuel assemblies with over 50,000 fuel rods and 18 million fuel pellets. Once loaded, the fuel remains in the core for a number of years depending on the operating cycle. During re-fuelling one third or one quarter of the fuel is removed, the remainder rearranged to a location better suited to its remaining level of enrichment. Fuel assembly performance has improved since the 1970s to allow increased burn-up of fuel from 40 GWday/tU to more than 60 GWd/tU.

The industry is dominated by four companies providing fuel assemblies for light water reactors in the West: Areva, Global Nuclear Fuel (“GNF”), TVEL and Westinghouse. GNF primarily provides fuel for BWRs, and TVEL for PWRs. The majority of the fuel for the UK’s nuclear power stations is produced by Springfields (owned by Westinghouse) near Preston, Lancashire. Fabrication of fuel assemblies represents less than 20% of the final cost of the fuel.

The fuel assemblies for Advanced Gas-Cooled Reactors (“AGRs”) which form the bulk of the UK’s nuclear fleet comprise fuel elements made up of uranium oxide pellets stacked inside stainless steel tubes. These tubes are then grouped together in a graphite “sleeve” to form the assembly. An AGR assembly is made up of 36 steel tubes, each containing 64 pellets. The pellets are larger than for LWRs.

Unlike other western European countries, France does not rely on Russia for its nuclear fuel. It imports natural uranium from Niger, Kazakhstan, Uzbekistan and Australia, which is then converted and enriched at Orano’s facilities at the Malvési and Tricastin sites, in southern France. Fuels are then manufactured by Framatome or Westinghouse.

.

In my next post I will look more closely at the geopolitical risks associated with the market concentration identified above.

there seems to be an error in the statement: “A 1 GW pressurised water reactor core generally contains between 120 and 200 fuel assemblies each containing around 500 kg of uranium oxide, capable of generating about 200 MWh of electricity over its lifetime”. it should be thousands of TWh not 200 MWh.

A very informative piece. It does in my view bring into question UK energy security being partly based on nuclear when the UK does not possess any feed stock.