Despite the recent high-profile approval of the Rosebank oil field in the North Sea, the picture for domestic oil and gas production remains bleak. The Conservative Government has recently spied an opportunity for re-election by deferring the costs of the energy transition at a time when many voters are worried about the high cost of living.

But it clings to the populist windfall tax on UKCS production, which was intended to neutralise complaints about high energy company profits, but in reality, harms independent producers while barely impacting the majors. Meanwhile the Labour Party is committed not only to retaining this harmful tax, it also wants to stop new licencing in the region, preventing new fields from being developed.

These policies are both short-sighted and counter-productive. No-one thinks the UK is going to stop using fossil fuels any time soon, so if we reduce domestic production, we will simply increase imports. Imported energy typically has higher production and transportation emissions, and reduces our energy security, which is unwise at a time of global uncertainty.

Falling North Sea production is worrying

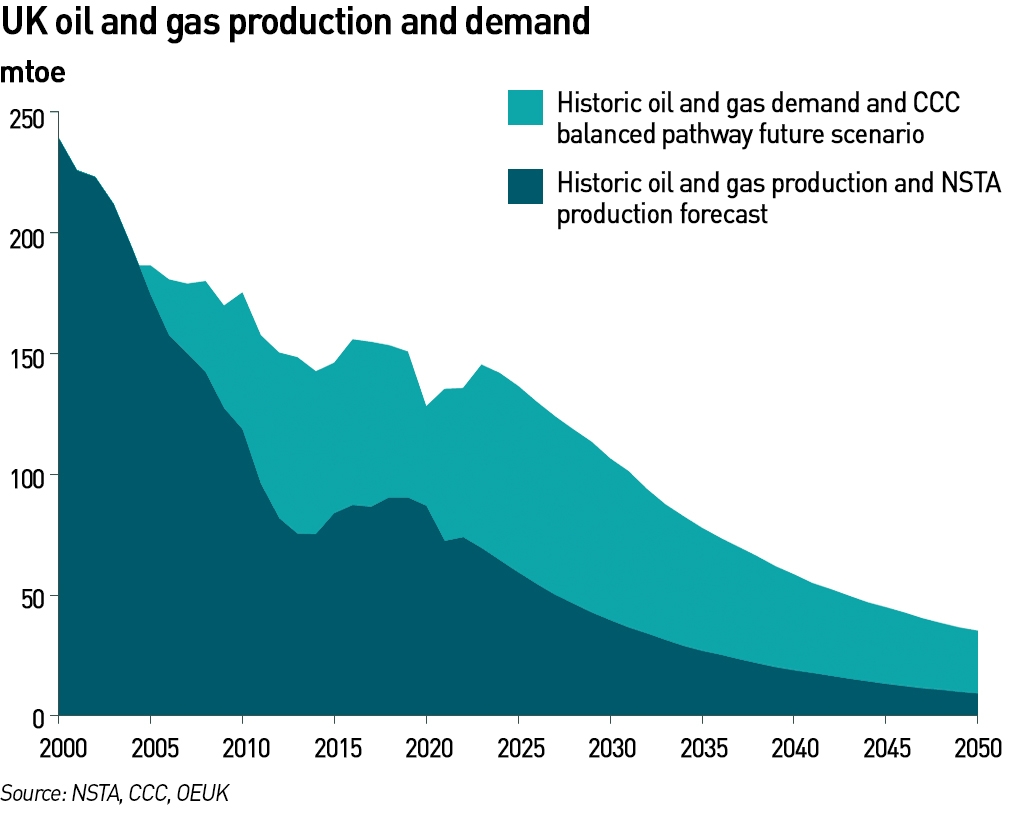

According to the latest Annual Economic Report by Offshore Energies UK (“OEUK”), North Sea oil production has fallen at its fastest rate in a decade as the windfall tax deters investment, and companies fear a further deterioration in the market outlook should the Labour Party win the next General Election. Crude oil output fell by 13% in the first six months of this year compared with the same period in 2022, to a record low of 16.2 million tonnes, roughly a quarter of what the UK produced at its peak in 1999.

OEUK says that the windfall tax had seriously destabilised the industry, and Labour’s pledge to ban all new oil and gas licences adds further uncertainty.

“People want to see consistency of policy, but it’s clear there is political uncertainty with a general election next year. That is causing uncertainty with investors and that is part of the reason why we are not seeing much investment being unlocked,”

– David Whitehouse, CEO, OEUK

The UK has produced over 45 billion boe since 1975 and the North Sea Transition Authority (“NSTA”) estimates there could still as much as 10-15 billion boe left, although OEUK believes the final amount extracted will be lower than the additional 8 billion boe the NSTA estimates will be recovered. This, however, would require additional investment and exploration, which is threatened by the widespread loss of investor confidence following the introduction of the windfall tax. OEUK believes that as little as 4 billion boe could be extracted as capital is deployed elsewhere in the world. This is equivalent to only a quarter of likely enduring demand through to 2050.

Over the last two decades the UK oil and gas industry has produced around 14.5 billion boe, but only 6.5 billion boe in new field developments have been approved, or 45% of reserves. This means the gap between total recovery and remaining reserves has closed significantly. The UK’s off-shore production comes from 283 producing fields of widely varying sizes, of which over 180 are expected to stop producing this decade. These fields produced 45% of UK oil and gas output last year. At least 20 fields will stop producing this year alone but only two new fields will start up.

As a result, domestic oil and gas production is falling twice as fast as demand, meaning the country is increasingly reliant on imports. The UK currently imports about half of its oil and gas needs, and without additional investment, this could grow to 80% in the coming years. Of course, not only will control over production emissions be lost through this switch to imports, additional emissions from transportation of these products will also be incurred.

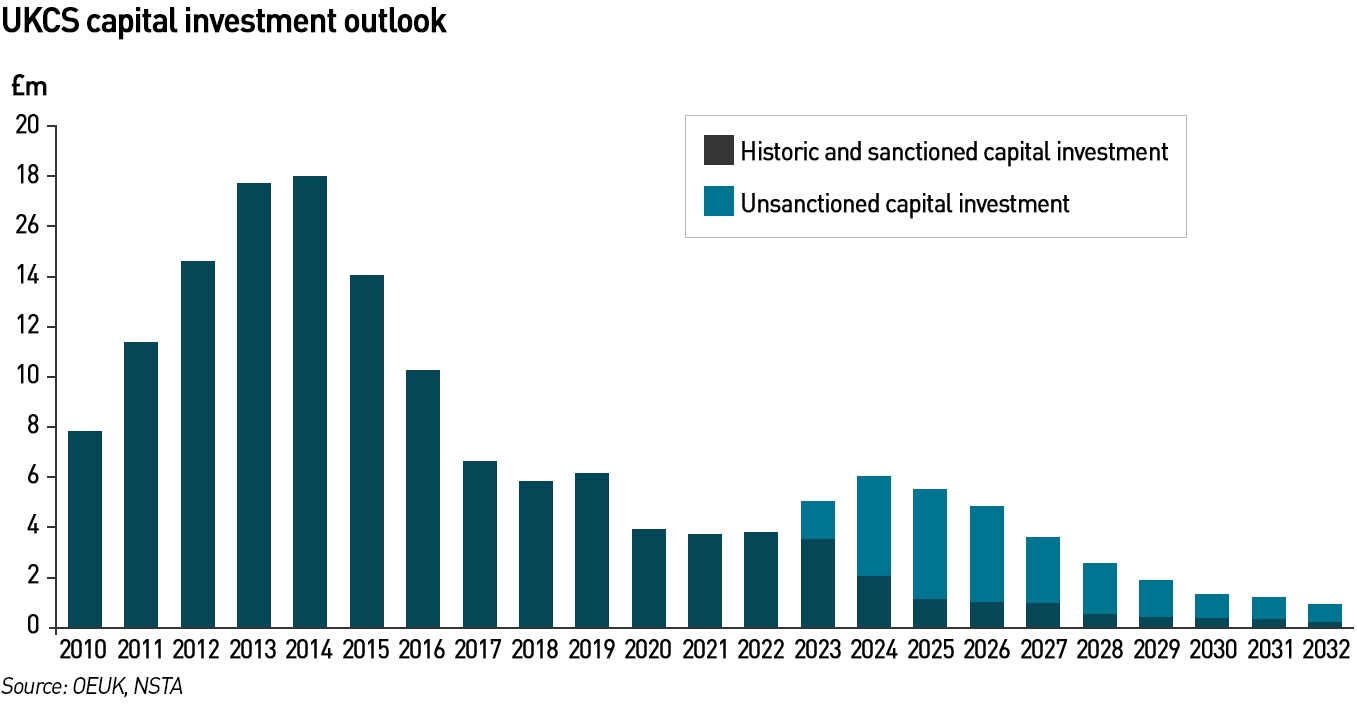

This means it is essential that investment in the UKCS is not only maintained but increased. Without new investment it is possible that the industry spend more on de-commissioning than production by 2025. Even in a high investment case, OEUK believes that de-commissioning spend may overtake production investment by the end of the decade, averaging around £2 billion per year.

A hostile political environment is scaring away investment…

OEUK expects there to be £3.5 – 4.0 billion of capital investment in the UKCS this year, which is lower than might have been expected at the beginning of the year, as new field approvals have remained slow. There is £35 billion of potential oil and gas capital investment over the next 10 years, of which around half would be on producing fields and half on new fields, however, only about 30% of this has been secured.

Recent technological advances and the scale of the infrastructure network means new discoveries can be brought to production much faster than in the past. Over the last decade, on average, new fields moved from discovery to production in five years, but more recently, some have started producing in under 18 months.

Unfortunately, exploration activity remains around all-time lows. Six wells have started drilling so far this year and at least one more is expected – similar levels to last year, although there have been some notable successes. Early estimates from the Deltic Energy, Shell and ONE well, Pensacola, which started drilling in late 2022, show potential recoverable resources of almost 100 million boe. Ithaca Energy and Dana Petroleum have announced a discovery at the K2 prospect with similar pre-drill resource estimates.

“A competitive and predictable fiscal regime is fundamental for investors, but the changes since May 2022 are significantly damaging their confidence in the UK and their ability to access finance. While the principle of a windfall tax in extraordinary circumstances is acknowledged, it is critical that when the windfall goes, so does the tax, if the UK is to deliver energy security, the energy transition and economic growth,”

– Ross Dornan, OEUK

Unfortunately, a combination of the windfall tax and hostile rhetoric from the Labour Party is undermining the UKCS investment case, at a time when the UK should be increasing not reducing domestic production. A survey of OEUK members has shown that a presumption against new licensing and exploration would have a significant negative impact on the way around the majority of companies view their UK business – with sentiment from supply chain companies being slightly more negative than operators.

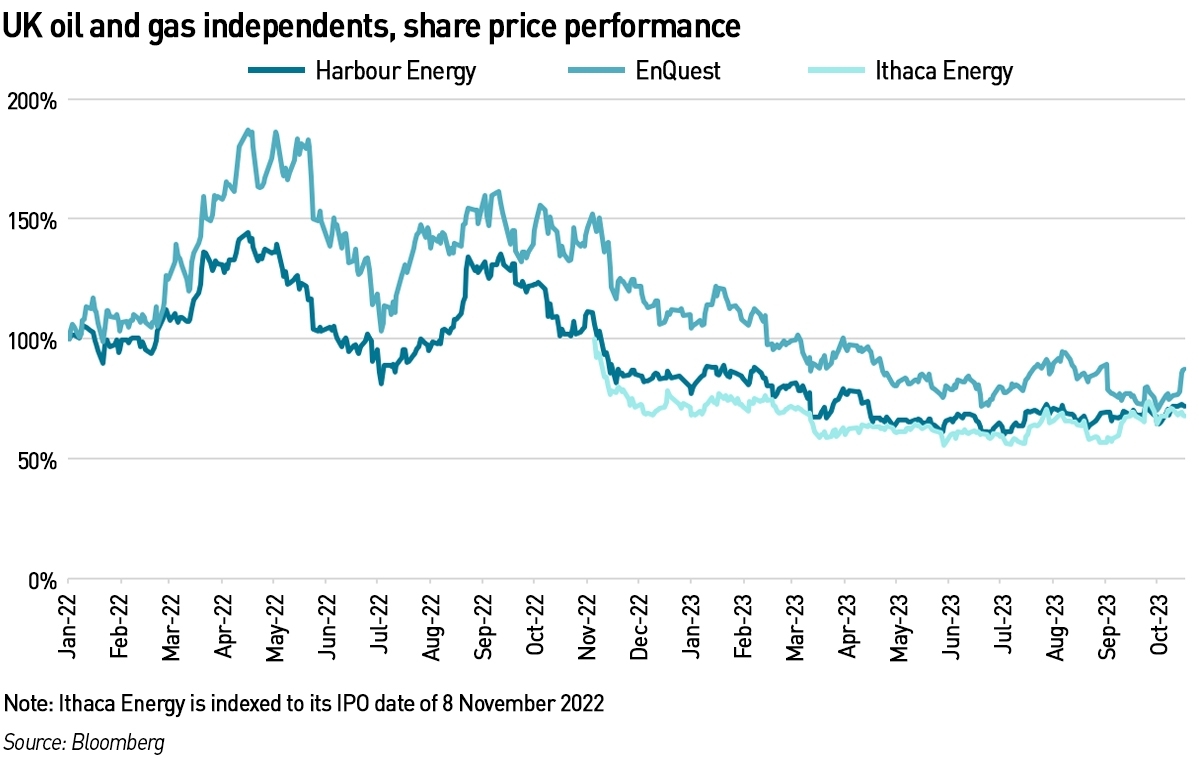

Ithaca Energy, one of the largest oil and gas producers in the UK, has reduced investments and is deferring some projects this year and next, due to the burden of the windfall tax, while Harbour Energy, the largest oil and gas producer in the UK North Sea, backed out of the latest licensing round. Shell has said it will re-evaluate each project comprising its £25 billion planned investment in the UK, while TotalEnergies has said it would slash its investment in the UK by 25%.

In its first-half results release, Ithaca said that until the fiscal regime is improved investment across its operated and non-operated portfolio has and will reduce, including the deferral and cancellation of certain 2023 and 2024 projects.

“The Energy Profits Levy continues to have a direct impact on investment in the UK North Sea and Ithaca Energy’s own investment programme across its diverse high-quality operated and non-operated asset base. We continue to constructively engage with the UK government to highlight the impact of the current fiscal regime to the industry’s outlook and to the UK government’s stated energy security and Net Zero ambitions,”

– Gilad Myerson, Executive Chairman at Ithaca Energy

Meanwhile investors are facing pressure to cut capital to the sector. The Treasury invited some of the world’s major banks to a meeting in August but attendance was disappointing with dozens of banks pulling out of investing in domestic fossil fuels due to concerns over the UK’s poor investment climate and growing pressure to fulfil ESG obligations. Most recently, BNP Paribas exited the market, following HSBC which left year, saying they would no longer finance freshly approved oil and gas projects.

While Shell and BP are sufficiently resourced to fund projects with their own cash flows, the majority independent producers, which make up the bulk of North Sea output, depend on bank finance. Securing such finance has become more difficult due to the windfall tax. The introduction of a price floor for oil and gas has not been sufficient to boost confidence, since the mechanism is not expected to be triggered during the life of the tax.

Growing expectations that Labour will win the next General Election are adding to concerns. Opposition leader Keir Starmer says he will maintain the de-facto 75% tax on oil and gas production, as well as banning new licensing rounds for further projects.

…as well as rigs which may never return to the region

Policies that end new licensing will constrain UK business opportunities at the same time that other countries are ramping up oil and gas production, which means people and equipment is likely to move from the UK to those areas. This is already being seen, particularly in the drilling sector as rigs are actively being marketed out of the UK to other regions.

“The North Sea is the only basin where the outlook is for a surplus of high specification drilling rigs, meaning other regions are more competitive for business – with longer work durations and higher rates on offer. Once these units leave the UK it is increasingly unlikely that they will return,”

– OEUK 2023 Annual Economic Report

Already this year, the UK North Sea has seen a decline in floating drilling rig activity, with some drilling contractors now expecting to move their rigs out of the North Sea to other regions. Harsh environment semisubs could be particularly impacted, as these high-demand rigs can be re-deployed for drilling campaigns off South Africa or Australia. For example, Odfjell Drilling sent its semisubmersible Deepsea Mira from the North Sea for a 300-day contract with TotalEnergies in Namibia earlier this year. The only drillship in the region, Deep Value Driller, has been bareboat chartered by Saipem and moved to Cote D’Ivoire to drill for Eni. Apache announced an early contract termination for Diamond Offshore’s Ocean Patriot, making the semisubmersible rig available more than 400 days earlier than planned. Apache said the cancellation followed the changes to the windfall tax.

The International Association of Drilling Contractors’ North Sea Chapter wrote to all 650 UK MPs and 129 MSPs warning that further harsh-environment rigs could be “lost for good” to the UK due to the windfall tax changes. According to Westwood’s RigLogix, North Sea rig supply is now 40% its level in March 2017, with 13 rigs departing the region in the past two years either for work elsewhere or retirement. Two more – the semis Hercules and the aforementioned Deepsea Mira – will relocate this year to eastern Canada and Namibia.

In contrast, drilling activity off Norway is picking up, boosted by a tax regime that is actively incentivising new activity, in stark contrast to the UK. According to Rystad Energy, the overall capex of greenfield investments proposed in 2022 will be US$ 42.7 billion after the Norwegian Government implemented a temporary tax regime during the 2020 market downturn to secure future development spending. The measures increased the uplift rate on all ongoing investments in 2020 and 2021, and on new projects sanctioned before 2023, up until first oil flows.

Operators on the Norwegian Continental Shelf rushed to submit development and operation plans before the new standard regime took effect at the start of this year. Of the 35 projects sanctioned within the temporary regime, 24 were approved in 2022, a record for Norway in a single calendar year, with the total value of these projects likely to reach US $29 billion. The combined resources are estimated at 2.472 billion boe. Rystad estimates the additional supply of gas in 2028 at about 24.9 bcm, close to 6.25% of demand in the EU and the UK combined.

Windfall tax is also hitting the profits of independent North Sea producers

Shares of independent oil and gas producers have fallen on the back of the Energy Profits Levy (“EPL”), a new tax introduced last year which brought the effective tax rate for UK oil and gas producers to 75%. The windfall tax applies to profits arising on or after 26 May 2022, and from January 2023 the rate was increased from 25% to 35%, and extended from December 2025 to March 2028.

Leading independent producer Harbour Energy blamed the windfall tax for wiping out its profits, saying the tax had pushed its effective tax rate to 102%. The firm provides roughly 15% of Britain’s oil and gas. Harbour swung from a near US$ 1 billion profit to an US$ 8 million loss during the first half of the year. It also warned that the scale of its tax bill has forced it to abandon new oil and gas projects in the UK and shift investment into overseas projects primarily in Indonesia and Mexico.

“The UK’s oil and gas sector faces significant challenges and loss of competitiveness due to uncertainty following the adverse changes to the fiscal regime. While we appreciate the Government’s intentions to improve the attractiveness of the sector through the Energy Security Investment Mechanism, we believe timely legislative reform is required to restore confidence in the UK oil and gas sector to protect jobs and deliver both energy security and decarbonisation,”

– Amjad Bseisu, CEO, EnQuest

EnQuest reported a first-half loss of US$ 21.2 million for the six months to June, compared to a profit of US$ 203.5 million for the same period last year, driven by a US$ 76 million charge related to the EPL, which accounts for more than half of its total tax bill.

Falling oil and gas prices caused pre-tax earnings to fall about 38% to US$ 112.9 million, after revenues dropped by more than US$ 200 million to US$ 732 .7 million. In the first half of 2023, global oil prices averaged US$ 75.8 /bbl, up from US$ 89.9 bbl the year before, while the average day-ahead gas price fell from 182 p/th to 108 p/th. Production levels had also fallen 8.5% to 45,480 boe /day. Production at the Kraken field fell by about a third after the failure of some hydraulic submersible pump transformers, while production at Golden Eagle also fell. In February, the company said it would stop new drilling in the Kraken field due to the impact of the EPL.

The company said that the windfall tax had left it facing an overall effective tax rate of 118%, and made it far harder to fund the company’s investment plans including those involving hydrogen production and carbon capture and storage, saying the levy was “taking cash out of the system and limits our ability to invest in such projects”.

.

Despite the recent sanctioning of the Rosebank field, the current political environment regarding domestic oil and gas production is resulting in significant self-harm. It should be clear to everyone that UK oil and gas consumption is not falling to a degree that enables domestic production to be reduced – all that production cuts achieve is an increase in imports.

For production cuts to make sense, consumption needs to be reduced, and the trajectory for that remains slow. Trying to drive the energy transition from the supply side will only push up prices, and create economic hardship, but it will not have a meaningful impact on demand other than through reducing overall economic activity.

The only way to achieve sustainable demand reductions is to provide viable alternatives to fossil fuels, and so far progress in this regard has been slow. Even the much vaunted renewable energies are struggling to compete in the current high cost environment, hugely undermining the “cheap renewables” narratives.

The UK urgently needs to take a leaf out of Norway’s book, and not only reverse the EPL, but implement tax incentives for new E&P activity on the UKCS. Displacing imports will in itself have the effect of reducing emissions – prioritising domestic production is the cleanest and greenest way to meet our fossil fuel needs while they continue, while boosting our energy security. It’s time for more politicians to recognise this reality and stop their counter-productive virtue-signalling.

.

This post was co-written by James Porter.

An excellent article. Thank you.

I wonder how the political elite who seem to think a four letter unmentionable world is ‘coal’ and think the very mention of ‘oil’ is worse than physical crime can square the evident corner cutting that has taken place in wind turbines – to the extent Siemens face a significant global warranty bill? Since one way or another the bill is paid by consumers, perhaps quangos like Ofgem should be removed due to their inability to communicate, formulate policy or do anything of benefit to the people paying for the whole show?

All I can say is, I agree. I don’t understand the details but worry that populist policies of both major parties will lead to power cuts.

In practice this means I cannot use my clean electric boiler and will create clouds of coal smoke from my chimney.

Kathryn great article again highlighting many of the big issues in the energy world. Ive no truck with conspiracy theories but it is very concerning how our society has been so brainwashed ( i know this from friends and family who wont have it that renewables and batteries are all thats needed to get off oil & gas) that it doesn’t realise the level of self harm that is slowly being inflicted on themselves. Of course none of them will like the consequences but until we get politicians who are prepared to speak out and say it as it is can’t see anything changing.

Kathryn,

I’m usually very impressed with your energy comments; but ,this time, I’m disappointed.

Your comment seems to be confined to ‘oil’ v. ‘less oil’ and ignores all the other factors in play.

Sir John Armitt, for example, proposes a roll-out of heat pumps across the country. I would modify that and propose district heating systems for all concentrated groups of buildings, new build houses and offices. Houses and offices do not need high grade energy in the form of electricity; they could manage quite well on hot water for heating and electricity usage confined to TV, computers, lighting, etc. You ignore all the ;possibilities for reducing demand.

The Government could improve its energy game considerably; what a disaster it was recently when no bids were received for new wind farms.

SMRs have considerable potential for bridging the demand/generation energy gap; but have been too long neglected.

I suggest that all these other factors, and many not mentioned, need to be considered and not ignored in any discussion on energy.

Peter Stevenson

stevenson4237@gmail.com

With respect, Nicholas, I think you’re missing the point. Yes all these other technologies are coming along but nowhere near fast enough. We will need oil and gas for many years to come so we’d better optimise our sources.

I think I should have addressed my last comment to Peter, not Nicholas!

I checked out the HMRC tax receipts data, which splits out offshore RFCT from general CT as well as reporting the new windfall tax. Obviously there was some boost to tax take last year mainly because of the spike in gas prices (oil was relatively little affected) – but the tax take is now significantly down on RFCT, and it is starting to look as though the windfall tax plus RFCT will harvest less than the earlier simpler ring fenced regime. Most of our oil production is now exported, as it is less suited to UK refineries now that much of it is heavier and more sulphurous and also some grades are naphthenic rather than paraffinic – we import from the USA and Norway mainly to feed the refineries. However, the gas is landed here, and is a key component of supply that has meant that in summer months the UK has not had to rely on expensive LNG imports (any LNG imports were for re-export to the Continent, which has used the UK as an offshore LNG terminal). This will now change, especially since Norway is seeking to maximise its gas pipeline exports to the Continent: Norwegian gas supply to the UK is down in consequence. The switch to year round LNG imports will increase the prices UK consumers are faced with, as we will now be bidding against our Continental neighbours all year round, instead of just in winter. I guess Ed Miliband might finally be right that our gas prices will be determined on international markets, rather than being at a discount to them when we are self-sufficient in pipeline gas.