From 1 April 2023 the way that Balancing Services Use of System (“BSUoS”) costs are recovered could change – Ofgem is proposing to exempt generators from the charges and to recover the costs solely from end consumers. This would likely prompt a reduction in wholesale electricity costs as generators will no longer seek to recover these costs – to date, energy contracts typically reflect around half of the BSUoS cost as a “non-commodity” charge and the rest would be embedded in the energy price. The change will mean that the full BSUoS charge will be included in the non-commodity charge making it more transparent to end users. Ofgem is expected to approve the move next month.

At the same time, BSUoS charges will also be made more stable, being split into fixed winter and summer charges that will be reconciled annually, with any adjustments being recovered over the following year. Each year’s charges will be announced in the February a year prior to the start of the IFA year, on 1 April (ie with 14-15 months’ notice). Ofgem is expected to approve this reform in November.

Why are the changes needed?

Under the current arrangements, BSUoS charges allocate the cost of the balancing services to demand and transmission connected generation on the basis of a per unit energy charge (£/MWh) set after the fact. Interconnectors, small distributed generators and behind the meter generators do not pay BSUoS, while behind the meter generators are also able to help load avoid the charge. This creates a competitive disadvantage to transmission-connected generation relative to other forms of generation which could result in distortions to dispatch and investment in the wholesale electricity market.

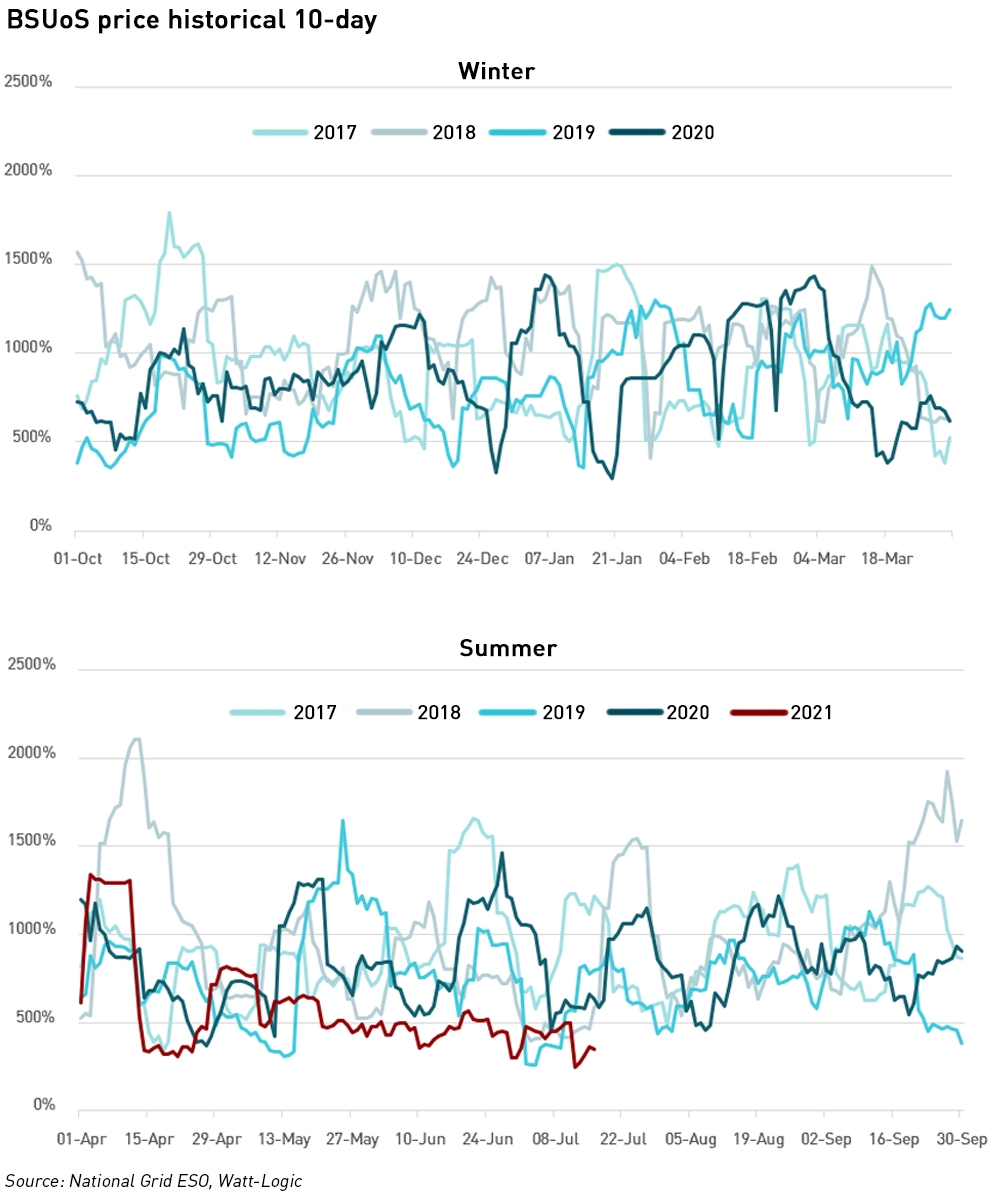

BSUoS charges are also highly volatile, ranging between 500% and 2000% (historical volatility was calculated as the annualised standard deviation over 10 days of the natural logarithm of daily price variations). This high volatility makes budgeting a challenge for market participants.

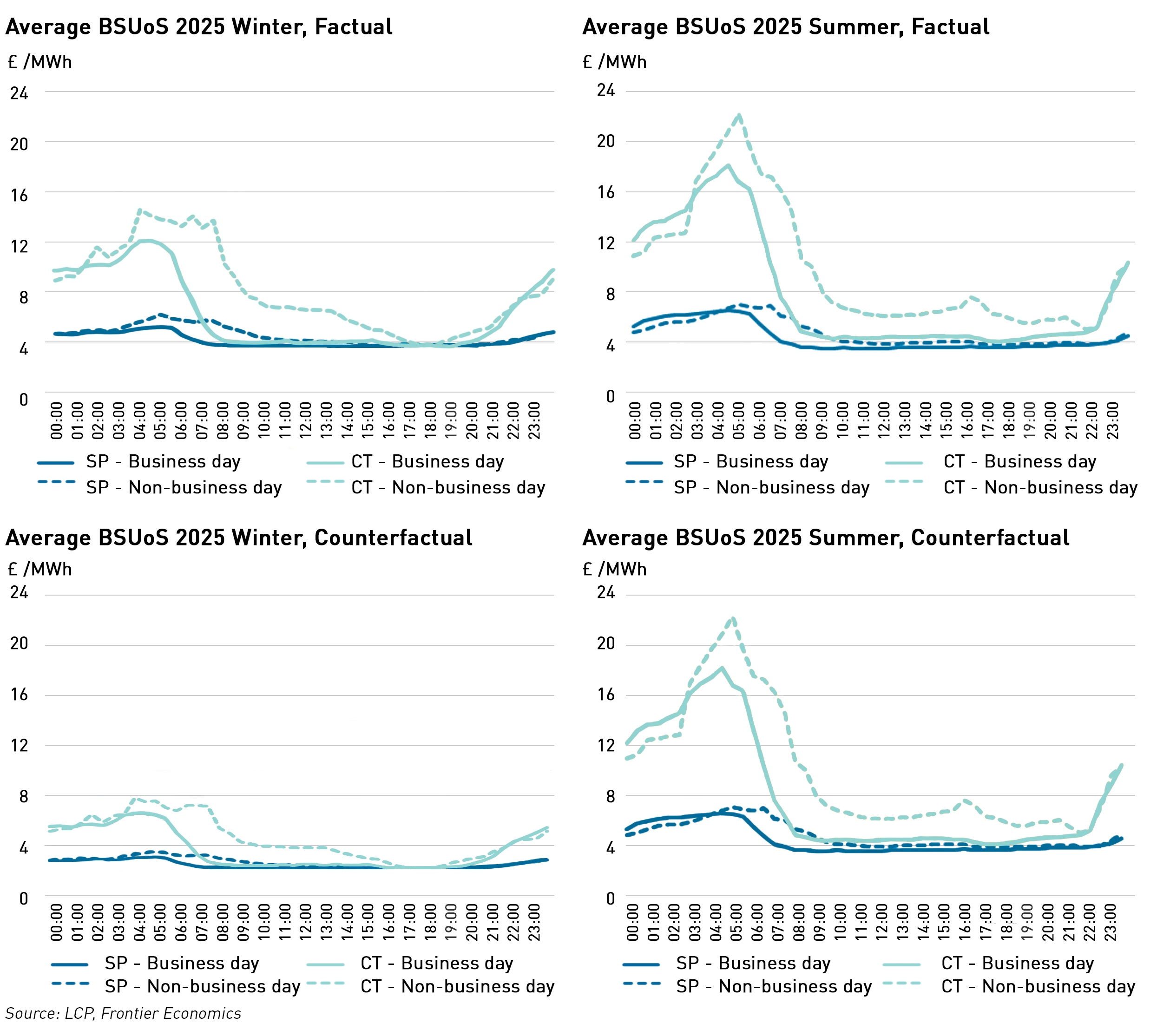

In the past few years it has been difficult to ascribe any clear seasonal patterns to BSUoS charging. In 2017 and 2020, BSUoS was higher in summer than winter, while in 2018 BSUoS was higher in winter. In 2019, the widest range of charges with both the highest and lowest levels was in the summer, but the average BSUoS was higher for the winter.

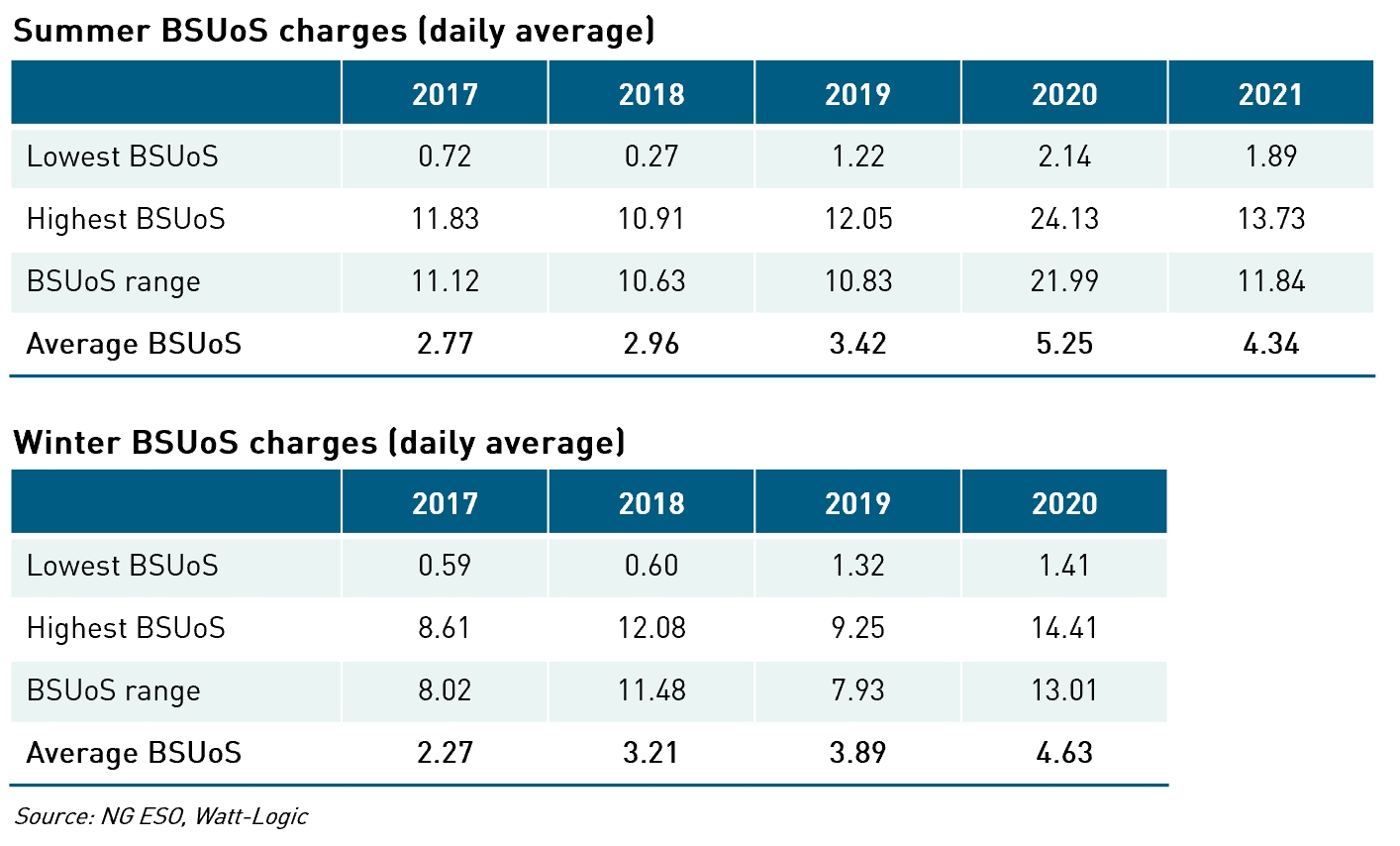

Balancing charges were significantly higher in 2020 for both the summer and the winter, but the summer showed a much greater increase on the previous years than was the case in the winter. Summer 2020 also saw a significantly wider range of charges than had been seen before, with the daily averages ranging from £2.14 /MWh to £24.14 /MWh compared with £1.22 – £12.05 /MWh for Summer 2019, and £1.32 – 9.25 /MWh in Winter 2019. While the early part of summer 2021 saw higher charges, they have since fallen within historical norms as the effects of the pandemic reduce.

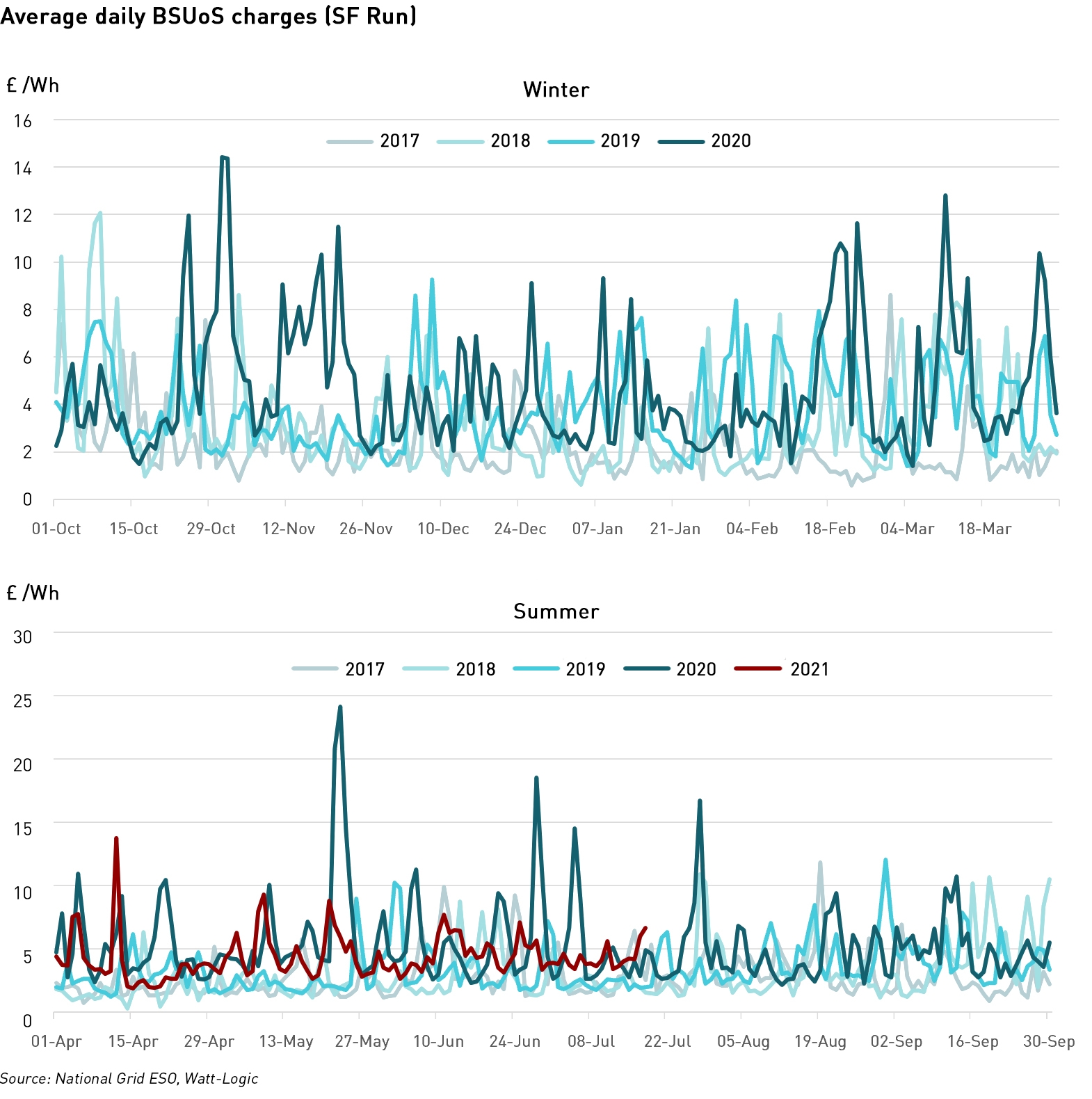

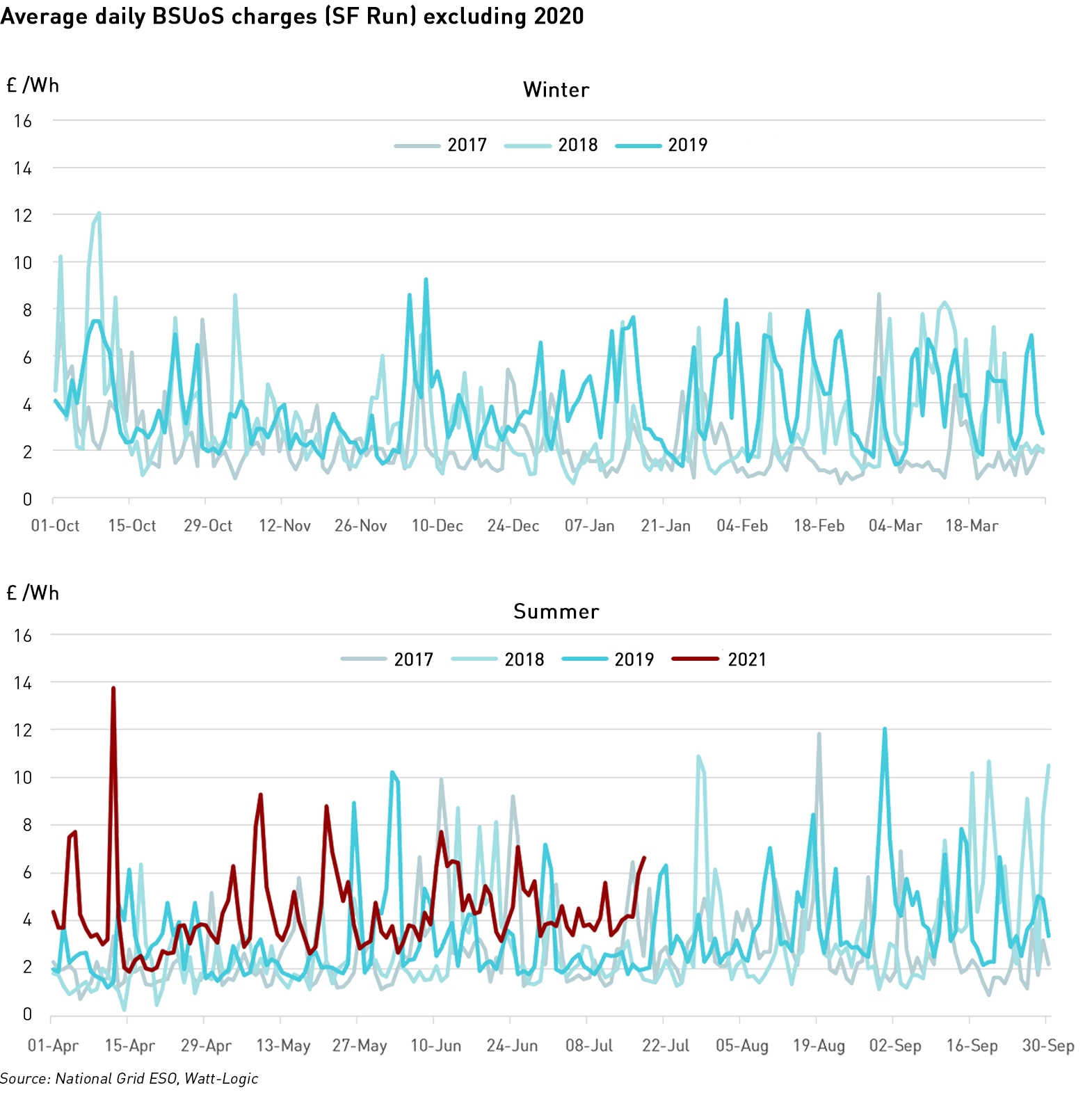

But what is clear from the analysis is that average BSUoS charges have been rising steadily (excluding 2020 due to the impact of covid):

Summer 2020 has been held up some analysts as a precursor to the future energy markets, where higher penetration of renewable generation acts to both increase the costs of balancing actions and reduce the demand base from which costs are recovered, essentially because greater use of solar power reduces gross summer demand which is already lower than winter demand. The increase in working from home enforced by the pandemic was also seen as a potential route to achieving net-zero ambitions by reducing the energy requirements from transport.

Some aspects of this analysis are likely to hold true. The costs of balancing actions will certainly rise with the greater penetration of renewable generation and the reduction in sources of inertia connected to the transmission system. Solar deployment is likely to grow, and because it is almost always distribution-connected it serves to reduce transmission-system demand which forms the basis of the recovery of BSUoS costs.

But the other aspects of the analysis are more questionable. The pandemic has illustrated that for many, working from home is entirely viable, but it is unlikely to ever fully replace office-working other than in a public health context. Hybrid forms of working where people divide their working time between home and the office are more likely. But with this comes increased demand for domestic heating and lighting, and even air-conditioning (on very hot days, people may well either prefer to be in an air-conditioned office, or install a domestic ac system, which are increasingly affordable).

The drive to de-carbonise heating will almost certainly also drive higher demand for electricity as a portion of homes currently heated with gas will migrate to electric heating, and similarly de-carbonisation of transport will also boost electricity demand.

This means there are competing pressures on electricity demand. In the summer, where there is the greatest sensitivity, there will be lower demand for heating and lighting, so the de-carbonisation of heating will have less impact. It remains to be seen whether air-conditioning demand will grow enough to offset downward demand pressures and it may be that in the summer, net system demand will continue to fall with higher solar deployment.

What will the changes involve?

Ofgem asked NG ESO to create a Balancing Services Charges Task Force to explore updating BSUoS charging. The Task Force recommended that:

- BSUoS should be recovered from “final demand” so would no longer be recovered from transmission-connected generation, in line with other supply sources

- that the charges should be fixed in advance with a combined notice period of 14-15 months

- that NG ESO should manage the forecast risk associated with fixing the charge

Ofgem commissioned independent analysis by LCP and Frontier Economics of the proposals which found that recovering BSUoS costs entirely from demand is likely to reduce overall system costs and customer costs. The system benefits arise primarily from removing the disparity of treatment between different forms of generation and the disadvantage to transmission-connected generation. Consumer benefits arise because the increase in the BSUoS demand charge is more than offset by reductions in wholesale prices and low carbon support payments.

Annual BSUoS cost projections were developed based on three components:

- Thermal constraint costs based on annual projections provided by NG ESO

- Non-thermal constraint costs based on the same profile, but assuming that thermal rises from 40% of total constraints costs to 75% between 2022-2026

- Other BSUoS costs based on current levels, scaled in line with total demand in real terms

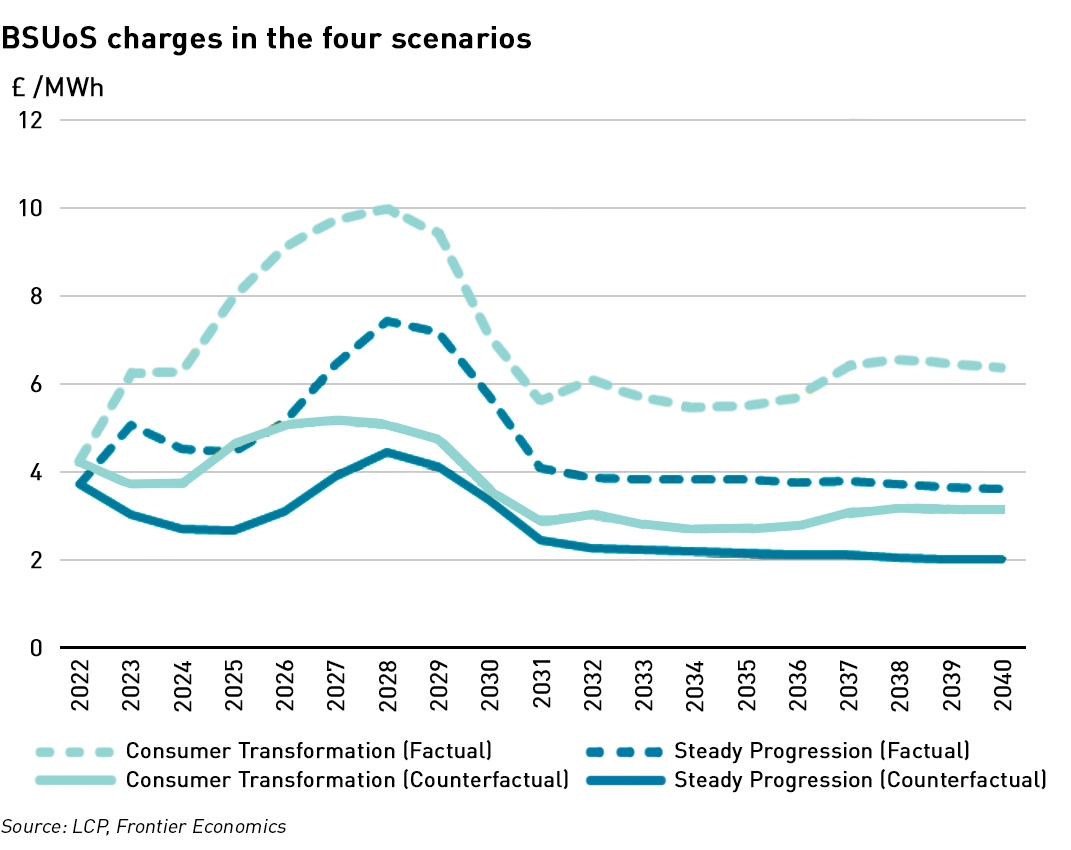

The charges used in the four scenario runs are shown below (with reference to National Grid’s Future Energy Scenarios):

BSUoS charges in the factual scenarios are much higher due to the smaller charging base. In Steady Progression and early years of Consumer Transformation, factual charges are less than double (1.6-1.8 times) the counterfactual charges because the generation charging base in the counterfactual is smaller than the demand base and therefore was recovering less than half of the costs. In the later years of Consumer Transformation, charges in the factual scenario are more than double those in the counterfactual, as the generation charging base is slightly higher than the demand base due to significant interconnection exports resulting in higher domestic generation.

Across all of the models, BSUoS charges are seen falling compared with historical levels. It should be noted that the counterfactual scenarios are with respect to the proposed BSUoS changes and not in respect of the FES for which there is no counterfactual scenario (in other words, NG ESO does not include a counterfactual, “do nothing” scenario within the FES).

“Based on the system modelling results set out in this section, the removal of BSUoS from generation seems likely to have a positive impact on system and consumer benefits,”

– LCP, Frontier Economics

NPVs for system cost benefits are £0.49 billion under Steady Progression and £0.29 billion under Consumer Transformation, and the NPVs for consumer benefits are £0.37 billion and £0.32 billion respectively.

High costs during covid led to the introduction of special measures

In May last year, National Grid predicted that the costs of balancing the system between May and August 2020 would be around £500 million higher than for the same period the previous year as a result of covid, leading to higher BSUoS charges. In response these significantly higher costs, Ofgem approved a modification to the Connection Use of System Code (“CUSC”) capping BSUoS at £15.00 /MWh for each period, from 25 June. This was superseded by another modification that came into effect on the 14 August capping BSUoS at £10.00 /MWh until the 25 October, with a limit of £100 million to the total amount deferred. These costs will be recovered uniformly across 2021/22.

In addition to allowing some degree of BSUoS cost deferral, two additional measures were introduced – the Optional Downward Flexibility Management (“ODFM”) scheme and the “Last resort disconnection of Embedded Generation” (Grid Code Modification 143).

OFDM allowed NG ESO the ability to control output from providers that are not currently accessed through either the Balancing Mechanism or existing Ancillary Services. Eligible participants needed to be capable of sustaining service delivery (ie continuing reduction of export to the grid, or increase in site demand) for a minimum of 3 consecutive hours, at a level of 1 MW or larger (aggregation of separate assets behind the same Grid Supply Point was allowed). Up to 3,000 MW of net demand reduction was required each time ODFM was triggered. Generators were required to curtail completely and could not participate in an active network management with their Distribution Network Operator (“DNO”).

The “Last resort disconnection of Embedded Generation” provision, allowed NG ESO to instruct a DNO to disconnect embedded generators connected to its system under emergency conditions and as a last resort. This would only be possible once demand reduction through the Balancing Mechanism and other commercial means had been exhausted. Embedded generators subject to such a disconnection would not receive any financially compensation, so were encouraged to participate in the ODFM service to enable them to secure revenues for reducing output.

Although these measures were temporary, they indicate the range of options that can be considered in the context of rapid adverse market change.

BSUoS reforms are an important step but there are risks

The proposed reforms will remove certain market distortions putting transmission-connected generation on the same footing as other sources of generation, and will make the management of costs to end users more predictable. However risks remain. Fixing BSUoS charges exposes the system operator to risks that the charges will be insufficient to cover balancing costs, undermining NG ESO’s solvency.

It also means that end users could be subject to steeply rising costs year-on-year, and although there will be a decent notice period for these changes, there will be little that consumers could do to manage the associated risks.

BSUoS charging errors

In April this year, NG ESO notified stakeholders of an under-recovery of around £44 million of BSUoS costs that were incurred during 2020. This figure comprised £34 million related to trading activities and £10 million related to the Accelerated Loss of Mains Change Programme (“ALoMCP”).

The £34 million trading error was due to a formatting change in a trading systems’ export excel file which meant that data were only being pulled through from the top row of a file used for invoicing purposes (possibly meaning that only data for the first settlement period of each day were collected and the remaining 47 periods were missed). This affected trades for the period from 30 September 2020 to 9 March 2021, and as a result £34 million of energy trading costs were accidently missed from BSUoS charges.

The other £10 million related to an earlier error. NG ESO had realised that it had over-recovered ALoMCP charges in previous years and so had temporarily ceased cost recovery in 2020. Later in the year once the over-recovery had expired, NG ESO failed to resume collecting these costs, meaning that a further £10 million of costs was missed from BSUoS charges.

It has subsequently been agreed that these costs will be recovered over 2021-22.

One aspect of concern in relation to this situation is that it took six months for the errors to come to light, which suggests that neither NG ESO or those being billed for BSUoS have adequate invoice validation processes. It also raises questions around the use of spreadsheets by NG ESO, which is extensive.

Errors in NG ESO materials are not new. Last year I found some errors in the monthly balancing reports, which were subsequently re-issued by NG ESO. The nature of the error was down to the way in which Excel is being used, and the fact that the published workbooks are altered to remove all calculations and simply paste in static numbers.

This makes an audit trail very difficult, and if, as happened in the case of the errors I found, an incorrect sheet is referenced by mistake, it is difficult to trace back the impact of the error.

NG ESO would help itself and the market by making its worksheets more transparent – retaining the formulae would enable market participants to see more easily how the worksheets are constructed and identify errors more quickly.

This particularly applies to trivial reporting errors, where, for example, the wrong tables or charts are copied and pasted from a spreadsheet into a report (in this case the prior year comparisons were mixed up with current year data).

I have made comparisons with financial services regulation before, and this is another area where the parallels are relevant. The Section 13.7 of the Financial Conduct Authority’s Handbook states:

“A firm should establish and maintain appropriate systems and controls for managing operational risks that can arise from inadequacies or failures in its processes and systems (and, as appropriate, the systems and processes of third party suppliers, agents and others).”

Given the impact on market participants on consumers of errors made by NG ESO, it is arguable that similar standards should be applied to the electricity system operator, and Ofgem should explore whether NG ESO’s use of spreadsheets is appropriate.

Another source of risk is that the cost-benefit analysis by LCP and Frontier Economics relies on the most recent NG ESO Future Energy Scenarios. I have been working on some analysis of the 10-year history of the FES, and have found significant volatility within the scenarios where some parameters in one year’s scenarios fall outside the range of outcomes from the previous year’s scenarios. (I will be publishing a blog on this shortly, once I complete the analysis). The carbon emissions for 2020 published in FES 2021 fall outside the range of any of the scenarios in the entire history of the FES. This raises some credibility issues surrounding the use of the FES as the basis for a cost-benefit analysis of the proposed changes.

I tend to be sceptical of the quantum of benefits identified in impact analyses of this type due to their sensitivity (acknowledged by the authors) to the assumptions used. But the different treatment of different types of generation lacked justification, and the removal of this distortion should be positive for wider confidence in the market.

The real question is whether the annual fixing of BSUoS will be beneficial for the market, and this depends on how well costs can be forecast upfront by NG ESO when setting the charging levels. If realised costs turn out to be significantly higher than predicted then NG ESO will have to fund the difference, and consumers will see potentially sharp increases when this is recovered. If those increases turn out to be large it will create incentives for consumers to flex demand in response, for example temporarily increasing production to take advantage of lower costs ahead of published increases. Since only certain types of consumers would have the capability to do this, it would create new market distortions, in which case futher changes could be expected.

I thought that the attempt to charge generators for balancing costs was designed to penalise them fro the problems they cause by failing to perform as advertised at gate closure. That some of them were exempted was of course ridiculous. Nothing could be much more upsetting than losing 1GW on an interconnector instantaneously. Of course, some of the algorithms used were capricious in their operation, which did not greatly help. However, it is unclear to me that simply lumping all charges onto consumer bills directly provides the right (or indeed, any) incentives to reduce costs. The attitude at National Grid seems to be that so long as they can find a way to avoid any significant blackouts they don’t care what the cost is at all. At OFGEM, it’s much the same, with both caring far more about pursuing low carbon goals than low consumer costs.

Generators are already penalised for deviating from their FPNs through imbalance pricing, so I’m not sure I see why they need to be penalised twice. When most generation was transmissoin-connected you could argue the toss, but now so much is connected to LV networks it creates too much distortion.

As for the cost point – NG ESO’s mandate only extends to its own actions to balance the system. So all the other consequences such as high wholesale prices are outside the scope of its targets.

I think I’m right in saying that offshore windfarms get an uplift to their CfD, based in part on BSUoS increases. Would these changes mean they get a windfall?